Keurig Dr Pepper Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

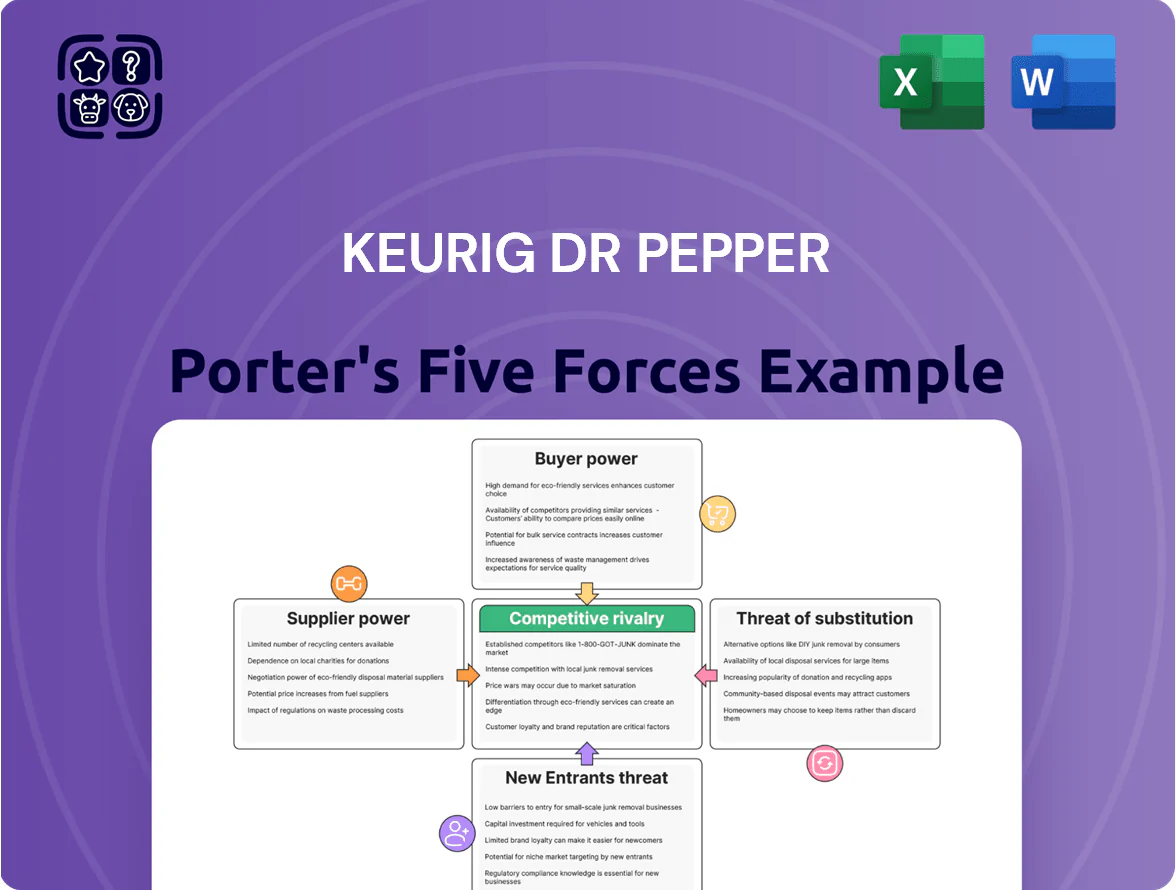

Keurig Dr Pepper faces moderate rivalry with strong brand portfolios and scale advantages, while supplier and buyer power remain balanced due to diversified sourcing and broad retail reach; substitutes and regulatory pressures pose notable risks to margins and innovation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Keurig Dr Pepper’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Keurig Dr Pepper relies on green coffee, sugar, and aluminum; in 2024 these inputs represented about 18% of COGS, and coffee futures rose ~22% year-over-year through Dec 2024. Global price swings can cut gross margin by multiple points—here’s quick math: a 10% coffee cost rise could lower 2024 gross margin (~32.5%) by ~0.9 percentage points. The company hedges short-term exposure but sustained commodity uptrends remain a material margin risk.

Concentration of Specialized Inputs

Certain Keurig brewing components and specialty flavoring ingredients come from few specialized suppliers, concentrating supply and raising supplier bargaining power; in 2024 Keurig Dr Pepper (KDP) reported about 18% of COGS tied to such proprietary parts and flavors.

That supplier concentration lets vendors demand higher prices and tighter contract terms—KDP noted supplier cost inflation added roughly $120 million to input costs in FY2024.

If a key supplier disrupts or exits, KDP would likely face delays and higher replacement costs; industry data show qualifying alternate suppliers can take 6–12 months, raising unit costs by an estimated 5–10% during transition.

Impact of Climate Change on Agriculture

As of late 2025, climate-driven yield drops in Brazil and Colombia cut Arabica output by ~12–18% versus 2019–21, raising premiums for high-grade beans; this scarcity boosts bargaining power for growers and cooperatives. Keurig Dr Pepper faces higher input costs—sustainable sourcing programs and farmer premiums pushed coffee procurement expenses up ~6–8% in 2024–25. The company must expand long-term contracts and ESG sourcing investments, adding recurring operational overhead and capex.

Logistics and Transportation Costs

Suppliers of freight and 3PLs wield leverage because Keurig Dr Pepper ships heavy, bulky beverages; in 2024 U.S. trucking spot rates rose ~12% Y/Y and diesel averaged $3.78/gal, driving higher carrier pricing.

Keurig Dr Pepper’s need for on-shelf continuity forces it to absorb or negotiate higher transport costs—transport and distribution make up a meaningful portion of COGS and pressured margins in 2023–24.

Labor shortages in trucking (truck driver vacancy rates ~80,000 nationwide in 2024) gave carriers bargaining room to push rates and reduce schedule flexibility.

- Heavy volume increases carrier power

- Diesel $3.78/gal (2024) raised costs

- Trucking spot rates +12% (2024)

- Driver shortfall ~80,000 (2024)

- KDP absorbs costs to protect shelf presence

Switching Costs for Technology Partners

Proprietary software and hardware in Keurig Dr Pepper’s latest brewers creates high switching costs; replacing tech partners would likely require $50–150m in R&D and 12–24 months of integration per platform, based on comparable appliance rollouts in 2023–2024.

That stickiness lets tech suppliers keep firm pricing on essential modules, supporting supplier bargaining power and margin protection for suppliers versus KDP.

- High one-time R&D: $50–150m

- Integration time: 12–24 months

- Supplier pricing power: sustained

Suppliers Squeeze Margins: +$120M Input Shock, Logistics Shortage & $50–150M Tech Hit

Suppliers hold moderate–high power: commodity swings (coffee +22% Y/Y to Dec 2024) and concentrated specialty vendors raised input inflation (~$120m in FY2024). Transport and driver shortages (trucking spot +12% Y/Y; diesel $3.78/gal; ~80,000 driver gap in 2024) further squeeze margins; tech/hardware lock-ins add $50–150m replacement costs and 12–24 months integration.

| Metric | Value |

|---|---|

| Coffee futures (Dec 2024) | +22% Y/Y |

| Input inflation FY2024 | $120m |

| Trucking spot (2024) | +12% Y/Y |

| Diesel (2024) | $3.78/gal |

| Driver shortfall (2024) | ~80,000 |

| Tech replacement | $50–150m, 12–24m |

What is included in the product

Tailored exclusively for Keurig Dr Pepper, this Porter's Five Forces overview uncovers competitive pressures, supplier and buyer influence, substitution risks, and entry barriers shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Keurig Dr Pepper—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Retailer Concentration and Leverage

Major retailers like Walmart, Target, and Costco together represented roughly 35–40% of Keurig Dr Pepper’s net sales in 2024, giving them strong leverage to push for lower wholesale prices, steep slotting fees, and exclusive promotions.

Those buyers’ scale lets them secure promotional funding worth millions; a 10% reduction in shelf space at a top account can cut category sales by double digits within weeks, directly hitting quarterly revenue.

Low Consumer Switching Costs

Low consumer switching costs mean buyers can swap sodas or coffee pods instantly; private-label pods now hold about 18% US pod market share (2024 IRI data), and supermarket own-label sodas grew 4.2% (2023 Nielsen).

That ease forces Keurig Dr Pepper (KDP) to spend: KDP’s 2024 selling, general & administrative expenses were $1.8B, with heavy marketing and loyalty investment to defend share.

Price Sensitivity in Inflationary Environments

By end-2025, CPI-driven inflation near 3.4% and U.S. household real income stagnation raised CPG price sensitivity; Keurig Dr Pepper (KDP) risk: NielsenIQ showed private-label share rose ~1.8 points in beverage categories in 2024–25. If KDP raises prices to cover input-cost rises (reported COGS up ~6% YoY in 2024), price elasticity may push consumers to value brands, constraining margin preservation and threatening share.

Growth of Private Label Brands

- Private-label beverage share ~17% (US, 2024)

- 42% of shoppers perceive parity (NielsenIQ, 2024)

- Better shelf placement and promos lower KDP volumes

Digital and E-commerce Influence

Online shopping and subscription growth lets buyers compare Keurig Dr Pepper prices across retailers in real time; US e-commerce beverage sales rose ~12% in 2024 to $18.6B, increasing price sensitivity.

Platforms like Amazon offer wide choice and reviews, cutting through brand marketing—Keurig Dr Pepper’s 2024 e-commerce channel sales exceeded $1.2B, still vulnerable to comparison shopping.

Digital transparency commoditizes beverages as buyers chase value, raising churn for premium SKUs and pressuring margins.

- 2024 US e-commerce beverages $18.6B

- KDP e‑commerce sales >$1.2B (2024)

- Subscription models increase repeat-buy leverage

Retailer Power and Private‑Label Pressure Force KDP into $1.8B Defense Mode

Large retailers (Walmart, Target, Costco) drove ~35–40% of KDP net sales in 2024, giving strong leverage to demand lower prices and promotions; private‑label beverage share was ~17% (US, 2024) and 42% of shoppers saw parity with national brands (NielsenIQ, 2024), forcing KDP to spend ~$1.8B on SG&A in 2024 to defend share; e‑commerce transparency (US beverages $18.6B, KDP e‑commerce >$1.2B) raises price sensitivity.

| Metric | Value |

|---|---|

| Retailer share of KDP sales (2024) | 35–40% |

| Private‑label beverage share (US, 2024) | ~17% |

| Shoppers seeing parity (NielsenIQ, 2024) | 42% |

| KDP SG&A (2024) | $1.8B |

| US e‑commerce beverages (2024) | $18.6B |

| KDP e‑commerce sales (2024) | >$1.2B |

Preview the Actual Deliverable

Keurig Dr Pepper Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Keurig Dr Pepper you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy.

No mockups or samples: what you see is the final, professionally written analysis file available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Keurig Dr Pepper faces moderate rivalry with strong brand portfolios and scale advantages, while supplier and buyer power remain balanced due to diversified sourcing and broad retail reach; substitutes and regulatory pressures pose notable risks to margins and innovation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Keurig Dr Pepper’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Keurig Dr Pepper relies on green coffee, sugar, and aluminum; in 2024 these inputs represented about 18% of COGS, and coffee futures rose ~22% year-over-year through Dec 2024. Global price swings can cut gross margin by multiple points—here’s quick math: a 10% coffee cost rise could lower 2024 gross margin (~32.5%) by ~0.9 percentage points. The company hedges short-term exposure but sustained commodity uptrends remain a material margin risk.

Concentration of Specialized Inputs

Certain Keurig brewing components and specialty flavoring ingredients come from few specialized suppliers, concentrating supply and raising supplier bargaining power; in 2024 Keurig Dr Pepper (KDP) reported about 18% of COGS tied to such proprietary parts and flavors.

That supplier concentration lets vendors demand higher prices and tighter contract terms—KDP noted supplier cost inflation added roughly $120 million to input costs in FY2024.

If a key supplier disrupts or exits, KDP would likely face delays and higher replacement costs; industry data show qualifying alternate suppliers can take 6–12 months, raising unit costs by an estimated 5–10% during transition.

Impact of Climate Change on Agriculture

As of late 2025, climate-driven yield drops in Brazil and Colombia cut Arabica output by ~12–18% versus 2019–21, raising premiums for high-grade beans; this scarcity boosts bargaining power for growers and cooperatives. Keurig Dr Pepper faces higher input costs—sustainable sourcing programs and farmer premiums pushed coffee procurement expenses up ~6–8% in 2024–25. The company must expand long-term contracts and ESG sourcing investments, adding recurring operational overhead and capex.

Logistics and Transportation Costs

Suppliers of freight and 3PLs wield leverage because Keurig Dr Pepper ships heavy, bulky beverages; in 2024 U.S. trucking spot rates rose ~12% Y/Y and diesel averaged $3.78/gal, driving higher carrier pricing.

Keurig Dr Pepper’s need for on-shelf continuity forces it to absorb or negotiate higher transport costs—transport and distribution make up a meaningful portion of COGS and pressured margins in 2023–24.

Labor shortages in trucking (truck driver vacancy rates ~80,000 nationwide in 2024) gave carriers bargaining room to push rates and reduce schedule flexibility.

- Heavy volume increases carrier power

- Diesel $3.78/gal (2024) raised costs

- Trucking spot rates +12% (2024)

- Driver shortfall ~80,000 (2024)

- KDP absorbs costs to protect shelf presence

Switching Costs for Technology Partners

Proprietary software and hardware in Keurig Dr Pepper’s latest brewers creates high switching costs; replacing tech partners would likely require $50–150m in R&D and 12–24 months of integration per platform, based on comparable appliance rollouts in 2023–2024.

That stickiness lets tech suppliers keep firm pricing on essential modules, supporting supplier bargaining power and margin protection for suppliers versus KDP.

- High one-time R&D: $50–150m

- Integration time: 12–24 months

- Supplier pricing power: sustained

Suppliers Squeeze Margins: +$120M Input Shock, Logistics Shortage & $50–150M Tech Hit

Suppliers hold moderate–high power: commodity swings (coffee +22% Y/Y to Dec 2024) and concentrated specialty vendors raised input inflation (~$120m in FY2024). Transport and driver shortages (trucking spot +12% Y/Y; diesel $3.78/gal; ~80,000 driver gap in 2024) further squeeze margins; tech/hardware lock-ins add $50–150m replacement costs and 12–24 months integration.

| Metric | Value |

|---|---|

| Coffee futures (Dec 2024) | +22% Y/Y |

| Input inflation FY2024 | $120m |

| Trucking spot (2024) | +12% Y/Y |

| Diesel (2024) | $3.78/gal |

| Driver shortfall (2024) | ~80,000 |

| Tech replacement | $50–150m, 12–24m |

What is included in the product

Tailored exclusively for Keurig Dr Pepper, this Porter's Five Forces overview uncovers competitive pressures, supplier and buyer influence, substitution risks, and entry barriers shaping its pricing power and profitability.

A concise Porter's Five Forces snapshot for Keurig Dr Pepper—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Retailer Concentration and Leverage

Major retailers like Walmart, Target, and Costco together represented roughly 35–40% of Keurig Dr Pepper’s net sales in 2024, giving them strong leverage to push for lower wholesale prices, steep slotting fees, and exclusive promotions.

Those buyers’ scale lets them secure promotional funding worth millions; a 10% reduction in shelf space at a top account can cut category sales by double digits within weeks, directly hitting quarterly revenue.

Low Consumer Switching Costs

Low consumer switching costs mean buyers can swap sodas or coffee pods instantly; private-label pods now hold about 18% US pod market share (2024 IRI data), and supermarket own-label sodas grew 4.2% (2023 Nielsen).

That ease forces Keurig Dr Pepper (KDP) to spend: KDP’s 2024 selling, general & administrative expenses were $1.8B, with heavy marketing and loyalty investment to defend share.

Price Sensitivity in Inflationary Environments

By end-2025, CPI-driven inflation near 3.4% and U.S. household real income stagnation raised CPG price sensitivity; Keurig Dr Pepper (KDP) risk: NielsenIQ showed private-label share rose ~1.8 points in beverage categories in 2024–25. If KDP raises prices to cover input-cost rises (reported COGS up ~6% YoY in 2024), price elasticity may push consumers to value brands, constraining margin preservation and threatening share.

Growth of Private Label Brands

- Private-label beverage share ~17% (US, 2024)

- 42% of shoppers perceive parity (NielsenIQ, 2024)

- Better shelf placement and promos lower KDP volumes

Digital and E-commerce Influence

Online shopping and subscription growth lets buyers compare Keurig Dr Pepper prices across retailers in real time; US e-commerce beverage sales rose ~12% in 2024 to $18.6B, increasing price sensitivity.

Platforms like Amazon offer wide choice and reviews, cutting through brand marketing—Keurig Dr Pepper’s 2024 e-commerce channel sales exceeded $1.2B, still vulnerable to comparison shopping.

Digital transparency commoditizes beverages as buyers chase value, raising churn for premium SKUs and pressuring margins.

- 2024 US e-commerce beverages $18.6B

- KDP e‑commerce sales >$1.2B (2024)

- Subscription models increase repeat-buy leverage

Retailer Power and Private‑Label Pressure Force KDP into $1.8B Defense Mode

Large retailers (Walmart, Target, Costco) drove ~35–40% of KDP net sales in 2024, giving strong leverage to demand lower prices and promotions; private‑label beverage share was ~17% (US, 2024) and 42% of shoppers saw parity with national brands (NielsenIQ, 2024), forcing KDP to spend ~$1.8B on SG&A in 2024 to defend share; e‑commerce transparency (US beverages $18.6B, KDP e‑commerce >$1.2B) raises price sensitivity.

| Metric | Value |

|---|---|

| Retailer share of KDP sales (2024) | 35–40% |

| Private‑label beverage share (US, 2024) | ~17% |

| Shoppers seeing parity (NielsenIQ, 2024) | 42% |

| KDP SG&A (2024) | $1.8B |

| US e‑commerce beverages (2024) | $18.6B |

| KDP e‑commerce sales (2024) | >$1.2B |

Preview the Actual Deliverable

Keurig Dr Pepper Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Keurig Dr Pepper you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, ready for download and use the moment you buy.

No mockups or samples: what you see is the final, professionally written analysis file available instantly after payment.