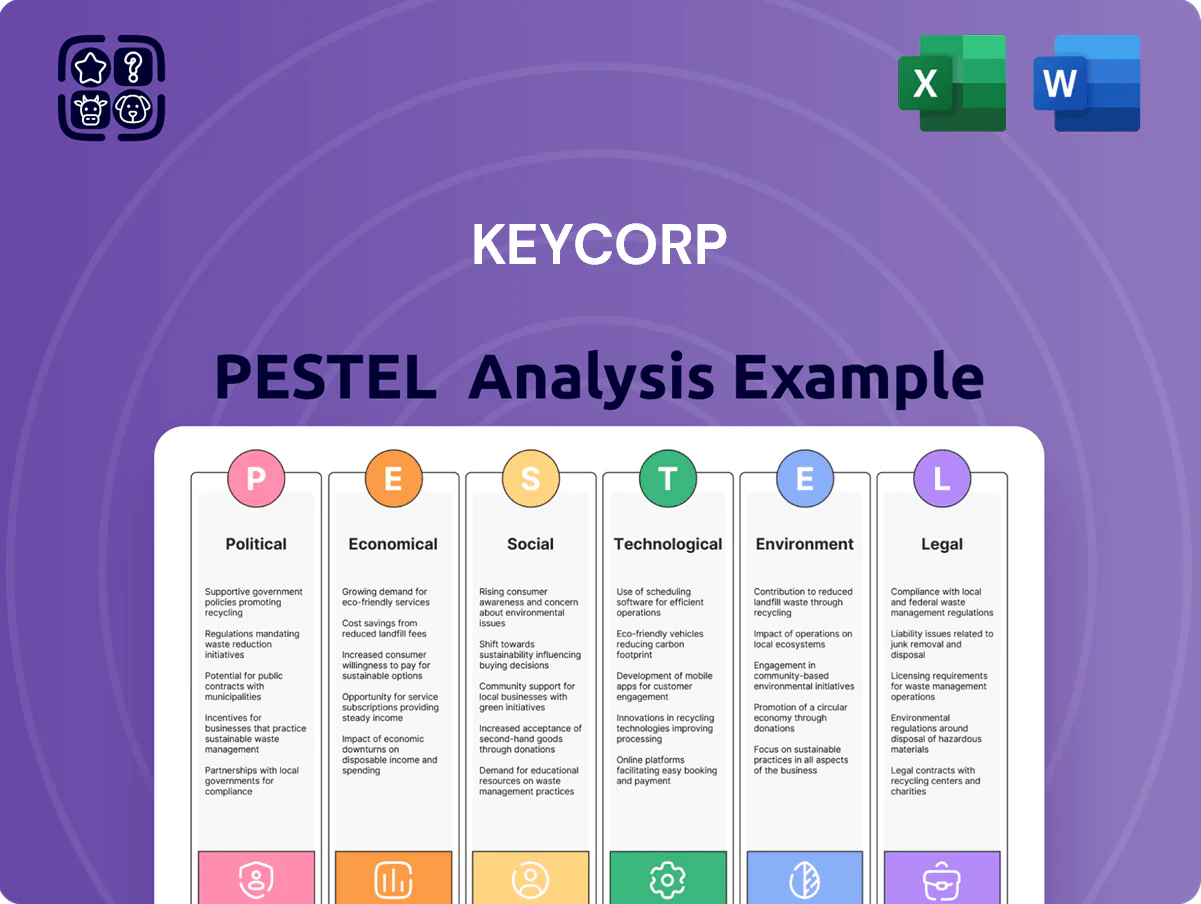

KeyCorp PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping KeyCorp’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need clarity fast. Purchase the full PESTLE analysis to access detailed risk assessments, regulatory implications, and actionable recommendations you can use immediately.

Political factors

Post-Election Regulatory Shifts

The 2024 federal elections altered agency leadership, with new appointees at the CFPB and OCC signaling potential changes to bank capital guidance that could increase CET1 expectations by 25–75bps for regional banks like KeyCorp in 2025.

Federal Reserve Independence and Influence

Political pressure on Fed rate guidance remains material for regional banks like KeyCorp, as a 25 bps hike or cut shifts net interest margin projections; KeyCorp reported NIM of 2.35% in Q4 2025, so wholesale shifts driven by legislative debates over the Fed’s dual mandate have increased quarterly NIM volatility by ~40% year-over-year. KeyCorp closely monitors Fed communications and potential mandate revisions given their direct effect on cost of capital and loan repricing.

Geopolitical Stability and Trade Policy

Ongoing international conflicts and shifts in U.S. trade policy are pressuring KeyCorp’s institutional bank clients; 2024 US tariff adjustments and supply-chain disruptions correlated with a 12% rise in nonfinancial corporate delinquencies in mid-market sectors, raising potential credit risk for KeyCorp.

Tariffs and restrictions can increase input costs and inventory financing needs for mid-market corporates, which could elevate loan loss provisions—KeyCorp reported a 0.95% net charge-off rate in 2024 vs 0.78% in 2022 for commercial portfolios.

Global political instability drives flight-to-quality flows: Treasury inflows and higher deposit balances were seen industry-wide in 2024, tightening investment banking deal pipelines and affecting KeyCorp’s fee income from cross-border M&A and trade finance.

State-Level Legislative Divergence

Operating across 39 states, KeyCorp must navigate a patchwork of state laws; in 2024 compliance costs for regional banks rose ~6% as state-specific rules proliferated.

Divergent consumer protection and financial privacy statutes—varying on data breach penalties up to $500 per consumer in some states—heighten legal risk and monitoring burden.

Political shifts in Ohio and New York can trigger state-funded infrastructure spending (Ohio $2.5B in 2024) or tax incentive changes affecting loan demand and corporate deposits.

- 39 states footprint

- +6% compliance cost trend (2024)

- Data breach fines up to $500/consumer

- Ohio $2.5B infrastructure (2024)

Government Fiscal Policy and Spending

Rising federal deficit spending and recent infrastructure packages—notably the 2021 Bipartisan Infrastructure Law ($1.2 trillion) and the 2022 CHIPS/Science Act—have boosted demand for commercial lending and public finance; KeyCorp reported increased municipal underwriting activity, with 2024 municipal bond issuance rising ~10% year-over-year to $546 billion nationally.

KeyCorp has targeted financing for domestic manufacturing and energy transition projects, capturing deals in clean energy tax-credit-backed financings; however, U.S. federal debt surpassed $34.5 trillion in 2025, raising risks of future tax increases or subsidy adjustments that could pressure corporate margins.

- Infrastructure and fiscal packages raise demand for public finance and commercial loans

- KeyCorp active in manufacturing and energy-transition financings

- U.S. federal debt > $34.5T (2025) implies potential future tax changes

- Tax or subsidy shifts could dent corporate profitability and loan performance

KeyCorp faces rising credit, compliance and capital pressure amid policy and global risks

Political shifts (CFPB/OCC leadership, Fed guidance) raise capital and NIM volatility for KeyCorp; trade policy and global conflicts increased mid-market delinquencies ~12% (2024) and commercial net charge-offs rose to 0.95% (2024). State-by-state rules (39-state footprint) lifted compliance costs ~6% (2024); federal debt > $34.5T (2025) implies fiscal policy risk.

| Metric | Value |

|---|---|

| CET1 pressure | +25–75bps |

| NIM Q4 2025 | 2.35% |

| Delinquencies mid-market | +12% (2024) |

| Net charge-off (commercial) | 0.95% (2024) |

| Compliance cost trend | +6% (2024) |

| Federal debt | > $34.5T (2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect KeyCorp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to highlight risks and opportunities.

A concise, visually segmented PESTLE summary for KeyCorp that distills regulatory, economic, social, technological, environmental, and political factors into an easily shareable slide or handout, enabling fast alignment and clearer risk discussions in planning sessions.

Economic factors

Interest Rate Normalization Trends

By end-2025 the Federal Funds Rate—projected median ~5.25% by FOMC dot plots in 2024–25—remains KeyCorp’s chief profitability driver, as net interest margin expanded to ~3.10% in 2024; a stabilizing rate environment eases management of the repricing gap between assets and liabilities.

Higher loan yields boost income but KeyCorp faces rising deposit betas—average cost of interest-bearing liabilities climbed to ~1.90% in 2024—forcing tradeoffs between yield pickup and deposit retention costs.

Inflationary Pressures and Consumer Spending

Persistent inflation affects KeyCorp retail customers’ purchasing power; US CPI eased to 3.4% year-over-year in 2024 (Dec), but elevated food and energy costs pushed credit card balances up—consumer credit rose $53.5B in Q4 2024—raising delinquency risk for KeyCorp’s unsecured lending book.

Regional Economic Performance Disparity

KeyCorp’s footprint is concentrated in Northeast and Midwest corridors where 2025 GDP growth lagged the US average at about 1.6% vs national 2.1%, creating regional economic performance disparity.

Manufacturing-heavy Ohio and Michigan and tech clusters in parts of Pennsylvania affect commercial loan demand and NPLs; Midwest manufacturing output rose 2.8% YoY in 2024, influencing credit quality.

Management must allocate capital dynamically toward regions with stronger employment—e.g., Cleveland metro unemployment fell to 3.9% in 2025 vs national 4.1%—and higher industrial output to optimize loan growth and risk-adjusted returns.

Capital Market Volatility and Fee Income

KeyCorp’s investment management and trust income closely track equity and bond market performance; 2024 U.S. equity volatility (VIX average ~17) and 10-year Treasury yield shifts (from 3.9% in Jan 2024 to ~4.2% mid-2024) materially influenced fee income streams.

Market volatility discouraged some IPOs and debt issuances—U.S. IPO deal value fell ~30% in 2024 vs 2021 peak—reducing investment banking fees for regional banks like KeyCorp.

Stable GDP growth (2.4% real GDP 2024) and rising household financial assets (U.S. household net worth reached ~$160 trillion in 2024) supported higher AUM and recurring wealth-management revenue for KeyCorp.

- VIX avg ~17 (2024)

- 10y Treasury ~4.2% mid-2024

- U.S. IPO value down ~30% vs 2021

- U.S. real GDP ~2.4% (2024)

- Household net worth ~$160T (2024)

Labor Market Dynamics and Wage Growth

Tight U.S. labor markets pushed average private-sector wage growth to about 4.1% YoY in 2025, raising KeyCorp’s compensation costs for skilled bankers and technologists and pressuring margins.

Simultaneously, regional employment in KeyCorp’s Midwest footprint remained above national unemployment (3.6% vs 3.8% in 2025), lowering retail and SMB loan defaults and supporting credit quality.

Rising wages increased household direct deposits—aggregate deposit growth for regional banks averaged ~3.5% YoY in 2025—enhancing KeyCorp’s liquidity and low-cost funding.

- Higher wages = increased personnel expense, margin pressure

- Stronger employment = lower default risk on consumer/SMB loans

- Wage-driven deposit growth (~3.5% YoY) = improved liquidity

KeyCorp: Higher Fed Rates Boost NIM to ~3.1% as Deposit Costs and Regional GDP Bite

Higher Fed rates (FFR ~5.25% by end-2025) lifted KeyCorp NIM to ~3.10% in 2024 while deposit beta rose (cost of interest-bearing liabilities ~1.90%); regional GDP (Midwest ~1.6% vs US 2.1% 2025) and wage growth (~4.1% YoY 2025) shaped loan demand, credit quality, and costs; market volatility (VIX ~17, 10y ~4.2% mid-2024) affected fee income.

| Metric | Value |

|---|---|

| NIM (2024) | ~3.10% |

| FFR (end-2025) | ~5.25% |

| Deposit cost (2024) | ~1.90% |

| Midwest GDP (2025) | ~1.6% |

| Wage growth (2025) | ~4.1% |

| VIX (2024 avg) | ~17 |

Full Version Awaits

KeyCorp PESTLE Analysis

The preview shown here is the exact KeyCorp PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible now are what you’ll download immediately after buying. Everything displayed is part of the final product.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping KeyCorp’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need clarity fast. Purchase the full PESTLE analysis to access detailed risk assessments, regulatory implications, and actionable recommendations you can use immediately.

Political factors

Post-Election Regulatory Shifts

The 2024 federal elections altered agency leadership, with new appointees at the CFPB and OCC signaling potential changes to bank capital guidance that could increase CET1 expectations by 25–75bps for regional banks like KeyCorp in 2025.

Federal Reserve Independence and Influence

Political pressure on Fed rate guidance remains material for regional banks like KeyCorp, as a 25 bps hike or cut shifts net interest margin projections; KeyCorp reported NIM of 2.35% in Q4 2025, so wholesale shifts driven by legislative debates over the Fed’s dual mandate have increased quarterly NIM volatility by ~40% year-over-year. KeyCorp closely monitors Fed communications and potential mandate revisions given their direct effect on cost of capital and loan repricing.

Geopolitical Stability and Trade Policy

Ongoing international conflicts and shifts in U.S. trade policy are pressuring KeyCorp’s institutional bank clients; 2024 US tariff adjustments and supply-chain disruptions correlated with a 12% rise in nonfinancial corporate delinquencies in mid-market sectors, raising potential credit risk for KeyCorp.

Tariffs and restrictions can increase input costs and inventory financing needs for mid-market corporates, which could elevate loan loss provisions—KeyCorp reported a 0.95% net charge-off rate in 2024 vs 0.78% in 2022 for commercial portfolios.

Global political instability drives flight-to-quality flows: Treasury inflows and higher deposit balances were seen industry-wide in 2024, tightening investment banking deal pipelines and affecting KeyCorp’s fee income from cross-border M&A and trade finance.

State-Level Legislative Divergence

Operating across 39 states, KeyCorp must navigate a patchwork of state laws; in 2024 compliance costs for regional banks rose ~6% as state-specific rules proliferated.

Divergent consumer protection and financial privacy statutes—varying on data breach penalties up to $500 per consumer in some states—heighten legal risk and monitoring burden.

Political shifts in Ohio and New York can trigger state-funded infrastructure spending (Ohio $2.5B in 2024) or tax incentive changes affecting loan demand and corporate deposits.

- 39 states footprint

- +6% compliance cost trend (2024)

- Data breach fines up to $500/consumer

- Ohio $2.5B infrastructure (2024)

Government Fiscal Policy and Spending

Rising federal deficit spending and recent infrastructure packages—notably the 2021 Bipartisan Infrastructure Law ($1.2 trillion) and the 2022 CHIPS/Science Act—have boosted demand for commercial lending and public finance; KeyCorp reported increased municipal underwriting activity, with 2024 municipal bond issuance rising ~10% year-over-year to $546 billion nationally.

KeyCorp has targeted financing for domestic manufacturing and energy transition projects, capturing deals in clean energy tax-credit-backed financings; however, U.S. federal debt surpassed $34.5 trillion in 2025, raising risks of future tax increases or subsidy adjustments that could pressure corporate margins.

- Infrastructure and fiscal packages raise demand for public finance and commercial loans

- KeyCorp active in manufacturing and energy-transition financings

- U.S. federal debt > $34.5T (2025) implies potential future tax changes

- Tax or subsidy shifts could dent corporate profitability and loan performance

KeyCorp faces rising credit, compliance and capital pressure amid policy and global risks

Political shifts (CFPB/OCC leadership, Fed guidance) raise capital and NIM volatility for KeyCorp; trade policy and global conflicts increased mid-market delinquencies ~12% (2024) and commercial net charge-offs rose to 0.95% (2024). State-by-state rules (39-state footprint) lifted compliance costs ~6% (2024); federal debt > $34.5T (2025) implies fiscal policy risk.

| Metric | Value |

|---|---|

| CET1 pressure | +25–75bps |

| NIM Q4 2025 | 2.35% |

| Delinquencies mid-market | +12% (2024) |

| Net charge-off (commercial) | 0.95% (2024) |

| Compliance cost trend | +6% (2024) |

| Federal debt | > $34.5T (2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect KeyCorp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to highlight risks and opportunities.

A concise, visually segmented PESTLE summary for KeyCorp that distills regulatory, economic, social, technological, environmental, and political factors into an easily shareable slide or handout, enabling fast alignment and clearer risk discussions in planning sessions.

Economic factors

Interest Rate Normalization Trends

By end-2025 the Federal Funds Rate—projected median ~5.25% by FOMC dot plots in 2024–25—remains KeyCorp’s chief profitability driver, as net interest margin expanded to ~3.10% in 2024; a stabilizing rate environment eases management of the repricing gap between assets and liabilities.

Higher loan yields boost income but KeyCorp faces rising deposit betas—average cost of interest-bearing liabilities climbed to ~1.90% in 2024—forcing tradeoffs between yield pickup and deposit retention costs.

Inflationary Pressures and Consumer Spending

Persistent inflation affects KeyCorp retail customers’ purchasing power; US CPI eased to 3.4% year-over-year in 2024 (Dec), but elevated food and energy costs pushed credit card balances up—consumer credit rose $53.5B in Q4 2024—raising delinquency risk for KeyCorp’s unsecured lending book.

Regional Economic Performance Disparity

KeyCorp’s footprint is concentrated in Northeast and Midwest corridors where 2025 GDP growth lagged the US average at about 1.6% vs national 2.1%, creating regional economic performance disparity.

Manufacturing-heavy Ohio and Michigan and tech clusters in parts of Pennsylvania affect commercial loan demand and NPLs; Midwest manufacturing output rose 2.8% YoY in 2024, influencing credit quality.

Management must allocate capital dynamically toward regions with stronger employment—e.g., Cleveland metro unemployment fell to 3.9% in 2025 vs national 4.1%—and higher industrial output to optimize loan growth and risk-adjusted returns.

Capital Market Volatility and Fee Income

KeyCorp’s investment management and trust income closely track equity and bond market performance; 2024 U.S. equity volatility (VIX average ~17) and 10-year Treasury yield shifts (from 3.9% in Jan 2024 to ~4.2% mid-2024) materially influenced fee income streams.

Market volatility discouraged some IPOs and debt issuances—U.S. IPO deal value fell ~30% in 2024 vs 2021 peak—reducing investment banking fees for regional banks like KeyCorp.

Stable GDP growth (2.4% real GDP 2024) and rising household financial assets (U.S. household net worth reached ~$160 trillion in 2024) supported higher AUM and recurring wealth-management revenue for KeyCorp.

- VIX avg ~17 (2024)

- 10y Treasury ~4.2% mid-2024

- U.S. IPO value down ~30% vs 2021

- U.S. real GDP ~2.4% (2024)

- Household net worth ~$160T (2024)

Labor Market Dynamics and Wage Growth

Tight U.S. labor markets pushed average private-sector wage growth to about 4.1% YoY in 2025, raising KeyCorp’s compensation costs for skilled bankers and technologists and pressuring margins.

Simultaneously, regional employment in KeyCorp’s Midwest footprint remained above national unemployment (3.6% vs 3.8% in 2025), lowering retail and SMB loan defaults and supporting credit quality.

Rising wages increased household direct deposits—aggregate deposit growth for regional banks averaged ~3.5% YoY in 2025—enhancing KeyCorp’s liquidity and low-cost funding.

- Higher wages = increased personnel expense, margin pressure

- Stronger employment = lower default risk on consumer/SMB loans

- Wage-driven deposit growth (~3.5% YoY) = improved liquidity

KeyCorp: Higher Fed Rates Boost NIM to ~3.1% as Deposit Costs and Regional GDP Bite

Higher Fed rates (FFR ~5.25% by end-2025) lifted KeyCorp NIM to ~3.10% in 2024 while deposit beta rose (cost of interest-bearing liabilities ~1.90%); regional GDP (Midwest ~1.6% vs US 2.1% 2025) and wage growth (~4.1% YoY 2025) shaped loan demand, credit quality, and costs; market volatility (VIX ~17, 10y ~4.2% mid-2024) affected fee income.

| Metric | Value |

|---|---|

| NIM (2024) | ~3.10% |

| FFR (end-2025) | ~5.25% |

| Deposit cost (2024) | ~1.90% |

| Midwest GDP (2025) | ~1.6% |

| Wage growth (2025) | ~4.1% |

| VIX (2024 avg) | ~17 |

Full Version Awaits

KeyCorp PESTLE Analysis

The preview shown here is the exact KeyCorp PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real file with no placeholders or teasers, delivered exactly as shown. The layout, content, and structure visible now are what you’ll download immediately after buying. Everything displayed is part of the final product.