Key Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

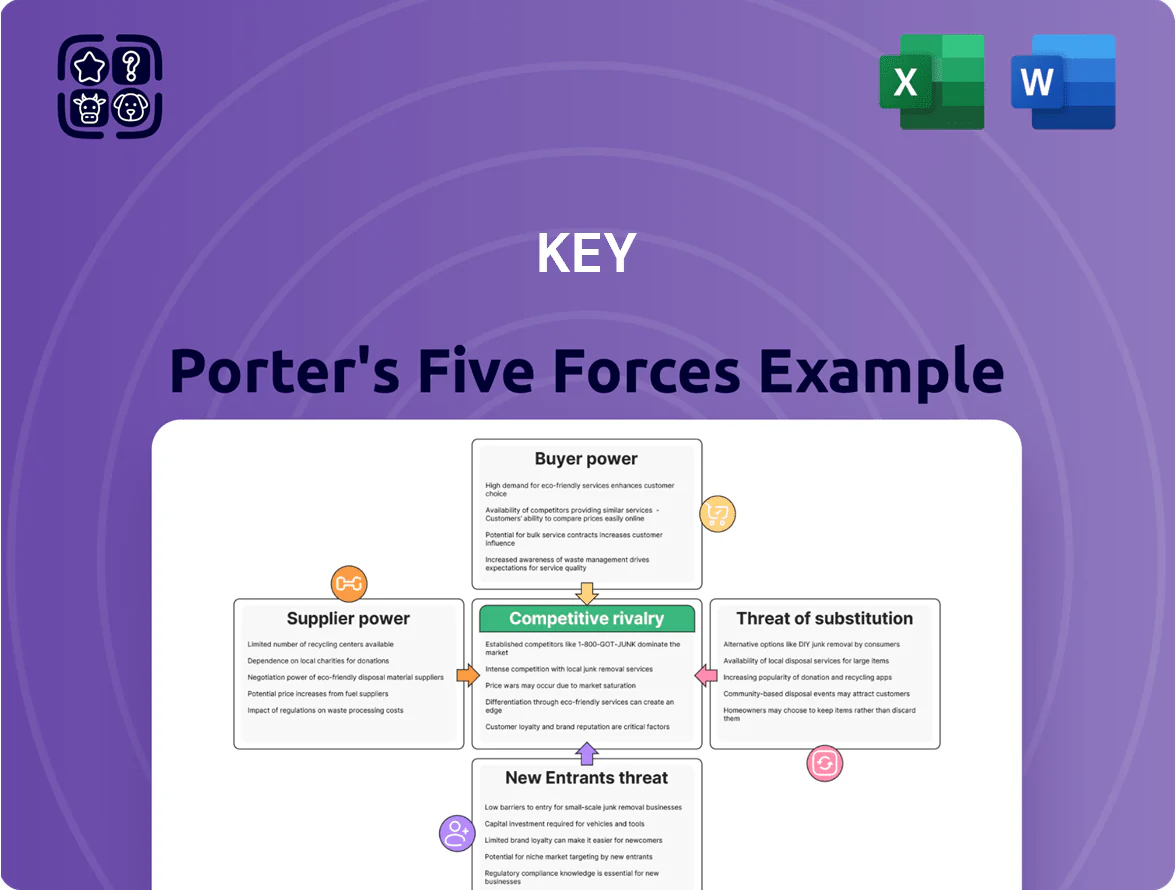

Key’s Porter's Five Forces snapshot highlights supplier and buyer power, rivalry intensity, and the real threat of new entrants and substitutes—revealing where competitive pressure concentrates and which levers matter most for strategy.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

The market for high-spec workover rigs and specialized components is concentrated among a few global makers (eg, NOV, Parker Drilling, GEODynamics), giving suppliers strong bargaining power over Key Energy Services because their proprietary designs and certified parts are needed to keep a modern fleet operational; as of Q3 2025, supplier concentration drove OEM pricing up ~8–12% year-over-year and industry lead times stretched to 20–36 weeks, and any manufacturer consolidation by late 2025 would further reduce Key’s ability to negotiate on price or delivery.

Skilled Labor and Technical Personnel

The shortage of experienced rig managers, derrickhands, and specialized technicians gives suppliers of skilled labor strong bargaining power, forcing Key Energy Services to offer competitive pay and benefits to retain staff and maintain safety.

Labor costs account for roughly 25–35% of operating expenses in well-intervention services; wage inflation of 6–10% in 2024–2025 raised crew costs materially.

This dependency on niche skills makes Key Energy vulnerable to further wage pressure and downtime risks if retention falters.

Raw Material and Steel Volatility

Suppliers of steel and tubular goods are critical for rigs and downhole tools, and global trade shifts plus industrial demand swings drove steel prices up ~18% from 2020–2024, creating pass-through cost risk for service companies.

Key Energy Services needs high-grade steel with few substitutes, so supplier concentration and limited switching power give suppliers leverage in pricing cycles, risking margin pressure if raw-material inflation exceeds 5–7% annually.

Software and Digital Integration Providers

As oil and gas shifts to data-driven well optimization, dependence on third-party fleet-management and predictive-maintenance software has risen; global oilfield software market hit about $9.2B in 2024, boosting supplier leverage.

Subscription pricing and proprietary algorithms create high switching costs—clients face migration costs often exceeding 15–25% of annual SaaS spend—giving vendors pricing power.

These providers tie integration into operators’ KPIs; missed updates or vendor lock can cut uptime and efficiency by several percentage points, so supplier influence is strategic.

- 2024 market: $9.2B oilfield software

- Switching cost: 15–25% of annual SaaS spend

- SaaS models drive recurring margins ~60–70%

- Operational impact: several % uptime/efficiency

Specialized Insurance and Risk Underwriters

Specialized insurance underwriters dominate onshore well intervention risk pools because plugging and abandonment (P&A) claims average $3.2m per incident in recent US Gulf Coast cases, so operators need comprehensive liability coverage.

Only about 8–12 underwriters worldwide focus on oilfield services, letting them set premiums (up 18%–30% since 2020) and strict exclusions.

With environmental rules tightening into 2025—eg. EPA and state-level P&A standards raising remediation obligations—insurers can demand higher compliance benchmarks to grant coverage.

- Average P&A claim: $3.2m

- Underwriters focusing on oilfield services: 8–12

- Premium increases since 2020: 18%–30%

- Stricter 2025 compliance raises insurability bar

Suppliers Squeeze Margins: Prices, Lead Times, Wages and Premiums Surge

Suppliers hold strong power: few OEMs (NOV, Parker, GEODynamics) pushed rig-part prices +8–12% YoY and lead times to 20–36 weeks by Q3 2025; skilled labor shortages raised crew wages 6–10% in 2024–25 (labor = 25–35% of Opex); steel/tubulars up ~18% (2020–24); oilfield software market $9.2B (2024) with 15–25% switching costs; P&A claims ~$3.2m, 8–12 specialist underwriters, premiums +18–30%.

| Metric | Value |

|---|---|

| OEM price change | +8–12% YoY (Q3 2025) |

| Lead times | 20–36 weeks |

| Labor wage inflation | 6–10% (2024–25) |

| Steel price change | +18% (2020–24) |

| Oilfield software | $9.2B (2024) |

| Switching cost (SaaS) | 15–25% annual spend |

| P&A claim avg | $3.2m |

| Underwriters | 8–12 |

What is included in the product

Tailored Porter’s Five Forces analysis for Key, uncovering competitive drivers, supplier and buyer power, threat of substitutes and entrants, and strategic vulnerabilities that shape pricing, margins, and market positioning.

Quickly visualize competitive pressure across all five forces with an editable radar chart—ideal for board-ready slides and rapid scenario comparisons.

Customers Bargaining Power

Concentration of Major E&P Operators

The customer base for Key Energy Services has grown more concentrated as major exploration and production mergers cut the number of buyers; by Q4 2025 the top 5 E&P clients account for roughly 48% of onshore drilling spend in the US, boosting buyer clout. These super-majors and large independents can demand volume discounts and longer payment terms, pressuring dayrates and margins. Losing one top client could reduce annual revenue by an estimated 12–18%, a material hit to EBITDA. Procurement consolidation raises switching costs for Key Energy and heightens contract risk.

Low Switching Costs for Standard Services

While specialized well intervention needs high expertise, many routine workover and maintenance services are treated as commodities, so operators view them as interchangeable and choose on price or availability. Customers can switch service providers with minimal downtime—industry surveys in 2024 showed 62% of operators changed routine service vendors within 12 months. That low switching cost forces Key Energy Services to compete sharply on pricing and maintain service uptime above 98% to protect share. Losing a 5% price gap can cut contract renewals by ~20% over a year.

Internalization of Service Capabilities

Large oil majors like Saudi Aramco and ExxonMobil can internalize well services; Aramco’s 2024 capital budget hit $90bn, showing capacity to buy rigs or build divisions, capping third-party margins.

If hourly rates climb above in-house breakeven—roughly $150–200/hr for routine services—clients will integrate, especially on multi-year projects where savings compound.

Focus on Capital Discipline

Stringent ESG and Safety Requirements

Customers now use ESG scores as primary selection criteria; by 2024, 62% of US oil & gas majors required supplier greenhouse gas (GHG) reduction plans, pushing Key Energy Services to absorb compliance costs.

Major operators demand strict safety protocols and emissions targets, with penalties and contract clauses shifting regulatory risk and remediation expenses onto Key, reducing EBITDA margins—industry reports show supplier compliance costs rose ~5–8% in 2023–24.

- 62% of majors require GHG plans

- Supplier compliance costs +5–8% (2023–24)

- Penalties shift environmental risk to Key

- Downward pressure on EBITDA margins

Customers Hold Leverage: Top-5 Drive 48% Spend — Churn, Compliance & Price Pressure

Customers hold high bargaining power: top 5 E&P clients ~48% of onshore spend (Q4 2025), losing one client cuts revenue ~12–18%, 62% of operators switched routine vendors within 12 months (2024), supplier compliance costs +5–8% (2023–24), customers demand <10% capex payback and >5% net uplift; in-house breakeven ~$150–200/hr forces price pressure.

| Metric | Value |

|---|---|

| Top-5 share (Q4 2025) | 48% |

| Revenue loss if one client exits | 12–18% |

| Operator vendor churn (2024) | 62% |

| Supplier compliance cost rise (2023–24) | 5–8% |

| In-house breakeven | $150–200/hr |

Preview Before You Purchase

Key Porter's Five Forces Analysis

This preview shows the exact Key Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or samples. The document displayed here is the final deliverable and will be available for instant download upon payment. It contains clear assessments of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitution risk tailored for decision-makers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Key’s Porter's Five Forces snapshot highlights supplier and buyer power, rivalry intensity, and the real threat of new entrants and substitutes—revealing where competitive pressure concentrates and which levers matter most for strategy.

Suppliers Bargaining Power

Specialized Equipment Manufacturers

The market for high-spec workover rigs and specialized components is concentrated among a few global makers (eg, NOV, Parker Drilling, GEODynamics), giving suppliers strong bargaining power over Key Energy Services because their proprietary designs and certified parts are needed to keep a modern fleet operational; as of Q3 2025, supplier concentration drove OEM pricing up ~8–12% year-over-year and industry lead times stretched to 20–36 weeks, and any manufacturer consolidation by late 2025 would further reduce Key’s ability to negotiate on price or delivery.

Skilled Labor and Technical Personnel

The shortage of experienced rig managers, derrickhands, and specialized technicians gives suppliers of skilled labor strong bargaining power, forcing Key Energy Services to offer competitive pay and benefits to retain staff and maintain safety.

Labor costs account for roughly 25–35% of operating expenses in well-intervention services; wage inflation of 6–10% in 2024–2025 raised crew costs materially.

This dependency on niche skills makes Key Energy vulnerable to further wage pressure and downtime risks if retention falters.

Raw Material and Steel Volatility

Suppliers of steel and tubular goods are critical for rigs and downhole tools, and global trade shifts plus industrial demand swings drove steel prices up ~18% from 2020–2024, creating pass-through cost risk for service companies.

Key Energy Services needs high-grade steel with few substitutes, so supplier concentration and limited switching power give suppliers leverage in pricing cycles, risking margin pressure if raw-material inflation exceeds 5–7% annually.

Software and Digital Integration Providers

As oil and gas shifts to data-driven well optimization, dependence on third-party fleet-management and predictive-maintenance software has risen; global oilfield software market hit about $9.2B in 2024, boosting supplier leverage.

Subscription pricing and proprietary algorithms create high switching costs—clients face migration costs often exceeding 15–25% of annual SaaS spend—giving vendors pricing power.

These providers tie integration into operators’ KPIs; missed updates or vendor lock can cut uptime and efficiency by several percentage points, so supplier influence is strategic.

- 2024 market: $9.2B oilfield software

- Switching cost: 15–25% of annual SaaS spend

- SaaS models drive recurring margins ~60–70%

- Operational impact: several % uptime/efficiency

Specialized Insurance and Risk Underwriters

Specialized insurance underwriters dominate onshore well intervention risk pools because plugging and abandonment (P&A) claims average $3.2m per incident in recent US Gulf Coast cases, so operators need comprehensive liability coverage.

Only about 8–12 underwriters worldwide focus on oilfield services, letting them set premiums (up 18%–30% since 2020) and strict exclusions.

With environmental rules tightening into 2025—eg. EPA and state-level P&A standards raising remediation obligations—insurers can demand higher compliance benchmarks to grant coverage.

- Average P&A claim: $3.2m

- Underwriters focusing on oilfield services: 8–12

- Premium increases since 2020: 18%–30%

- Stricter 2025 compliance raises insurability bar

Suppliers Squeeze Margins: Prices, Lead Times, Wages and Premiums Surge

Suppliers hold strong power: few OEMs (NOV, Parker, GEODynamics) pushed rig-part prices +8–12% YoY and lead times to 20–36 weeks by Q3 2025; skilled labor shortages raised crew wages 6–10% in 2024–25 (labor = 25–35% of Opex); steel/tubulars up ~18% (2020–24); oilfield software market $9.2B (2024) with 15–25% switching costs; P&A claims ~$3.2m, 8–12 specialist underwriters, premiums +18–30%.

| Metric | Value |

|---|---|

| OEM price change | +8–12% YoY (Q3 2025) |

| Lead times | 20–36 weeks |

| Labor wage inflation | 6–10% (2024–25) |

| Steel price change | +18% (2020–24) |

| Oilfield software | $9.2B (2024) |

| Switching cost (SaaS) | 15–25% annual spend |

| P&A claim avg | $3.2m |

| Underwriters | 8–12 |

What is included in the product

Tailored Porter’s Five Forces analysis for Key, uncovering competitive drivers, supplier and buyer power, threat of substitutes and entrants, and strategic vulnerabilities that shape pricing, margins, and market positioning.

Quickly visualize competitive pressure across all five forces with an editable radar chart—ideal for board-ready slides and rapid scenario comparisons.

Customers Bargaining Power

Concentration of Major E&P Operators

The customer base for Key Energy Services has grown more concentrated as major exploration and production mergers cut the number of buyers; by Q4 2025 the top 5 E&P clients account for roughly 48% of onshore drilling spend in the US, boosting buyer clout. These super-majors and large independents can demand volume discounts and longer payment terms, pressuring dayrates and margins. Losing one top client could reduce annual revenue by an estimated 12–18%, a material hit to EBITDA. Procurement consolidation raises switching costs for Key Energy and heightens contract risk.

Low Switching Costs for Standard Services

While specialized well intervention needs high expertise, many routine workover and maintenance services are treated as commodities, so operators view them as interchangeable and choose on price or availability. Customers can switch service providers with minimal downtime—industry surveys in 2024 showed 62% of operators changed routine service vendors within 12 months. That low switching cost forces Key Energy Services to compete sharply on pricing and maintain service uptime above 98% to protect share. Losing a 5% price gap can cut contract renewals by ~20% over a year.

Internalization of Service Capabilities

Large oil majors like Saudi Aramco and ExxonMobil can internalize well services; Aramco’s 2024 capital budget hit $90bn, showing capacity to buy rigs or build divisions, capping third-party margins.

If hourly rates climb above in-house breakeven—roughly $150–200/hr for routine services—clients will integrate, especially on multi-year projects where savings compound.

Focus on Capital Discipline

Stringent ESG and Safety Requirements

Customers now use ESG scores as primary selection criteria; by 2024, 62% of US oil & gas majors required supplier greenhouse gas (GHG) reduction plans, pushing Key Energy Services to absorb compliance costs.

Major operators demand strict safety protocols and emissions targets, with penalties and contract clauses shifting regulatory risk and remediation expenses onto Key, reducing EBITDA margins—industry reports show supplier compliance costs rose ~5–8% in 2023–24.

- 62% of majors require GHG plans

- Supplier compliance costs +5–8% (2023–24)

- Penalties shift environmental risk to Key

- Downward pressure on EBITDA margins

Customers Hold Leverage: Top-5 Drive 48% Spend — Churn, Compliance & Price Pressure

Customers hold high bargaining power: top 5 E&P clients ~48% of onshore spend (Q4 2025), losing one client cuts revenue ~12–18%, 62% of operators switched routine vendors within 12 months (2024), supplier compliance costs +5–8% (2023–24), customers demand <10% capex payback and >5% net uplift; in-house breakeven ~$150–200/hr forces price pressure.

| Metric | Value |

|---|---|

| Top-5 share (Q4 2025) | 48% |

| Revenue loss if one client exits | 12–18% |

| Operator vendor churn (2024) | 62% |

| Supplier compliance cost rise (2023–24) | 5–8% |

| In-house breakeven | $150–200/hr |

Preview Before You Purchase

Key Porter's Five Forces Analysis

This preview shows the exact Key Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or samples. The document displayed here is the final deliverable and will be available for instant download upon payment. It contains clear assessments of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitution risk tailored for decision-makers.