Keyrus PESTLE Analysis

Skip the Research. Get the Strategy.

Our targeted PESTLE Analysis for Keyrus reveals how political, economic, social, technological, legal, and environmental forces are reshaping its market position—giving you concise, actionable insights to inform strategy and investment decisions; purchase the full report for a complete, editable breakdown and immediate download.

Political factors

Geopolitical stability in core markets

Keyrus’s operations across Europe, the Americas and the Middle East make revenue sensitive to regional political shifts; in 2024 roughly 62% of group revenue derived from the Eurozone and Western Europe, heightening exposure to EU policy and stability.

Stability in the Eurozone is critical for long-term consulting contracts with large enterprises and governments; Euro area real GDP growth slowed to 0.6% in 2024, which could pressure project pipelines.

Escalation of geopolitical tensions could disrupt service delivery or delay projects in territories where Keyrus has offices—the firm maintained physical presence in over 20 countries in 2024, increasing operational risk.

Government digital transformation spending

Public sector modernization drives a steady pipeline for data intelligence firms; global government digital transformation spending reached about $1.2 trillion in 2024 and OECD reports show a 12–20% budget increase for sovereign cloud/digital sovereignty projects by end-2025 in several EU countries. Keyrus should align its roadmap to national agendas to target high-value contracts that demand localized data handling and compliance expertise, where contract sizes often exceed €5–20m.

Data sovereignty and regional policies

Political moves toward data localization force Keyrus to adjust implementation strategies for multinationals; over 70 countries had data residency laws by 2024, up from ~50 in 2018, affecting cloud architectures and raising compliance costs by an estimated 10–15% per project. Governments now mandate in-country processing for sectors like finance and health, so Keyrus must design regional data meshes and local hosting to preserve trust and avoid fines that can reach 2–4% of global turnover under some regimes.

International trade relations and tech exports

International trade agreements and diplomatic ties shape Keyrus’s ability to deploy consultants and export digital solutions; in 2024 cross-border services accounted for about 38% of global IT consulting revenue, affecting project routing and margins.

Stricter work-visa rules or tariffs raise labor mobility costs—OECD reported a 12% rise in compliance costs for cross-border services in 2023—forcing reallocation of onshore/offshore staffing.

Continuous monitoring of trade policy shifts is essential to adapt Keyrus’s global delivery model and optimize resource allocation to protect a reported 15% international revenue share growth target for 2025.

- Trade agreements determine market access and consultant mobility

- Visa/tariff changes increase delivery costs and staffing complexity

- Monitor policies to rebalance onshore/offshore capacity and meet 2025 targets

Public sector AI adoption frameworks

As of late 2025, over 40 countries have enacted public sector AI frameworks tightening requirements on fairness, explainability and data provenance; Keyrus must certify compliance with these standards to qualify for state contracts worth an estimated €6–12bn annually in EU digital transformation tenders.

Noncompliance risks exclusion from major procurements—e.g., EU/Member State procurements now mandate AI impact assessments and auditability, with penalties up to 5% of annual global revenue for vendors failing transparency rules.

- Mandatory AI impact assessments in 40+ countries by 2025

- State tenders in EU worth ~€6–12bn/year require compliance

- Penalties up to 5% of global revenue for transparency breaches

- Keyrus must ensure fairness, explainability, provenance and auditability

Keyrus faces EU-concentrated growth risk, rising compliance costs and AI regulatory exposure

Keyrus’s Eurocentric revenue mix (62% in 2024) raises exposure to EU policy and slower Eurozone growth (0.6% in 2024); geopolitical tensions across 20+ countries and rising data localization (70+ countries by 2024) increase compliance costs (~10–15%) and operational risk, while public sector digital/A I tenders (~€6–12bn/yr) demand strict compliance (40+ countries with AI rules by 2025; fines up to 5% revenue).

| Metric | Value |

|---|---|

| 2024 Eurozone share | 62% |

| Euro area GDP growth 2024 | 0.6% |

| Countries with data residency (2024) | 70+ |

| Compliance cost increase | 10–15% |

| AI frameworks by 2025 | 40+ |

| EU digital tenders/year | €6–12bn |

| Max penalties for AI noncompliance | ~5% global revenue |

What is included in the product

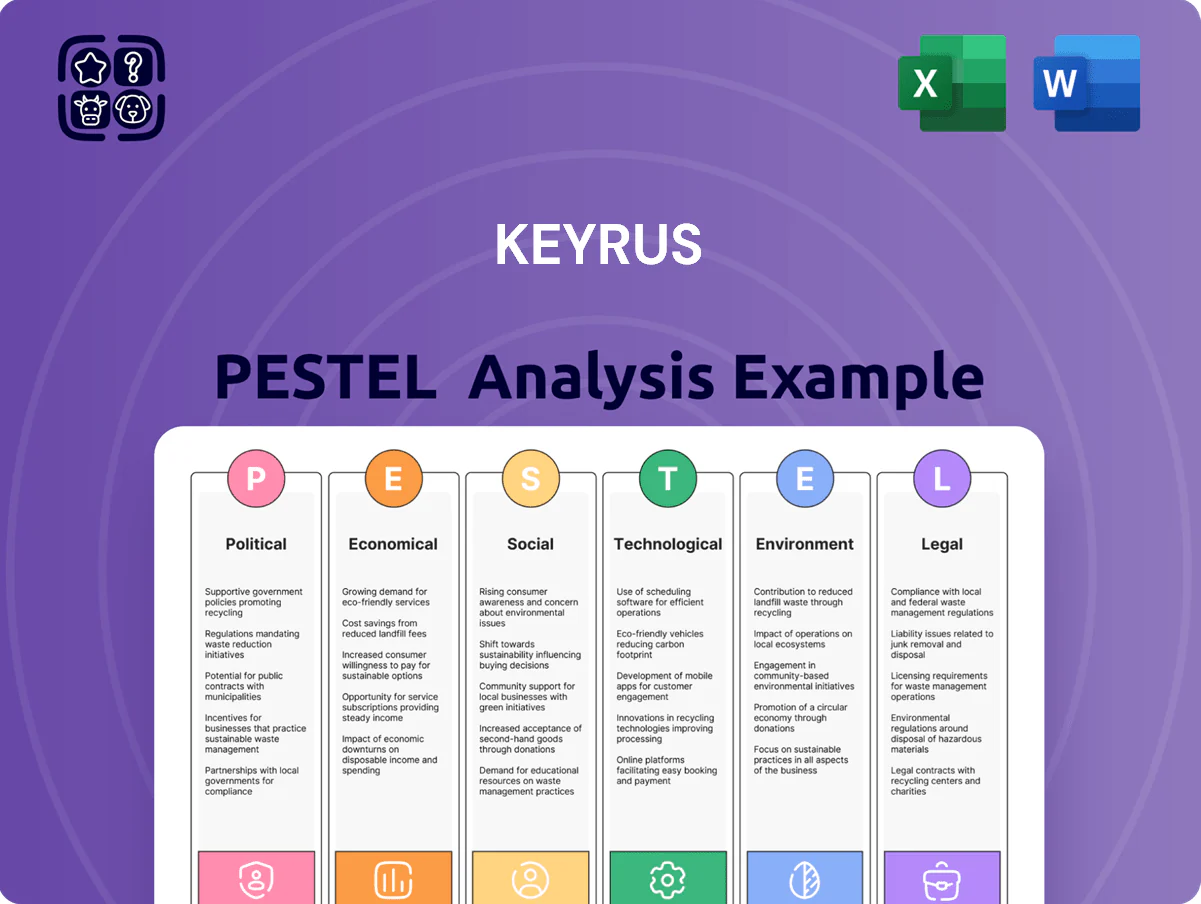

Explores how external macro-environmental factors uniquely affect Keyrus across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify strategic threats and opportunities.

Provides a concise, visually segmented PESTLE summary of Keyrus that’s easy to drop into presentations, share across teams, and adapt with notes for regional or business-line specifics, streamlining external risk discussions and strategic planning.

Economic factors

Inflationary pressures on consulting fees

Rising global inflation—CPI averaging 6.8% in 2024 and projected ~4.2% in 2025 in OECD economies—has pushed consulting rates up 6–9% as firms protect margins; Keyrus faces similar upward pricing pressure. Clients report 72% greater price sensitivity, demanding clear ROI metrics per digital project, pressuring Keyrus to justify fees with measurable KPIs. Balancing competitive pricing against 8–12% higher tech and talent costs is critical.

Global currency exchange volatility

As an international firm reporting in Euros but operating in Dollars, Brazilian Reals and other currencies, Keyrus faces material FX risk: EUR weakened ~4% vs USD in 2024 and BRL swung ~12% vs EUR in 2023–24, which can compress consolidated revenue and inflate local operating costs.

A 10% adverse move in major currencies could change reported EBITDA by low- to mid-single digits, so disciplined hedging and rolling FX forecasts are critical.

Corporate budget shifts toward automation

Economic uncertainty has pushed 62% of CIOs (Gartner 2024) to prioritize cost-optimization and automation over broad innovation, creating demand for Keyrus services that drive efficiency; positioning its BI and data-science suites as ROI-focused automation tools can capture this shift. The 2025 McKinsey estimate that automation could cut operational costs by up to 20% reinforces the case for Keyrus to market solutions that enable doing more with fewer staff.

Tech talent acquisition costs

The market for data scientists and digital transformation experts remains tight; global median data scientist salaries rose ~12% in 2024, with US medians around $120k–$140k, pushing recruitment costs higher for Keyrus.

Keyrus must boost retention and employer branding—benchmarks show retention programs can reduce turnover costs by 20–30%—or face margin pressure from rising compensation and hiring fees.

High tech turnover (industry annual attrition ~18–25% in 2024) threatens project continuity and quality, requiring contingency staffing and higher training spend.

- Salary inflation: +12% (2024) for data scientists; US median $120k–$140k

- Attrition: industry 18–25% (2024)

- Retention programs can cut turnover costs 20–30%

- Higher recruiting/training costs compress margins if not offset by pricing

Interest rate impact on digital investment

Higher rates through 2023–2024 pushed corporate capex cuts—global capex fell 2.1% in 2024—causing Keyrus clients to tighten digital investment, with many projects delayed or downsized.

With policy rates peaking (e.g., US Fed funds ~5.25% end-2024) and stabilizing by late 2025, procurement now requires stronger ROI proofs, lengthening Keyrus’s sales cycles by an estimated 20–30%.

Keyrus should shift to modular, lower-entry offerings and flexible pricing to match clients’ risk aversion and constrained budgets.

- Capex down 2.1% (2024)

- Sales-cycle length +20–30%

- Fed funds ~5.25% (end-2024)

- Recommend modular services, flexible pricing

Inflation, wage pressure and FX squeeze margins—ROI‑driven consulting amid longer sales cycles

Inflationary pressure (OECD CPI 6.8% in 2024; projected ~4.2% in 2025) raises consulting rates 6–9% while client price sensitivity (+72%) forces ROI‑driven proposals; salary inflation for data scientists +12% (2024; US median $120k–$140k) and attrition 18–25% compress margins; FX volatility (EUR −4% vs USD in 2024; BRL ±12% 2023–24) risks low‑mid single‑digit EBITDA swings; capex −2.1% (2024) lengthens sales cycles 20–30%.

| Metric | 2024/2025 |

|---|---|

| OECD CPI | 6.8% (2024); ~4.2% (2025) |

| Consulting rate rise | 6–9% |

| Data scientist salary | +12%; US $120k–$140k |

| Attrition | 18–25% |

| FX moves | EUR −4% vs USD (2024); BRL ±12% |

| Capex | −2.1% (2024) |

| Sales cycle | +20–30% |

What You See Is What You Get

Keyrus PESTLE Analysis

The preview shown here is the exact Keyrus PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Our targeted PESTLE Analysis for Keyrus reveals how political, economic, social, technological, legal, and environmental forces are reshaping its market position—giving you concise, actionable insights to inform strategy and investment decisions; purchase the full report for a complete, editable breakdown and immediate download.

Political factors

Geopolitical stability in core markets

Keyrus’s operations across Europe, the Americas and the Middle East make revenue sensitive to regional political shifts; in 2024 roughly 62% of group revenue derived from the Eurozone and Western Europe, heightening exposure to EU policy and stability.

Stability in the Eurozone is critical for long-term consulting contracts with large enterprises and governments; Euro area real GDP growth slowed to 0.6% in 2024, which could pressure project pipelines.

Escalation of geopolitical tensions could disrupt service delivery or delay projects in territories where Keyrus has offices—the firm maintained physical presence in over 20 countries in 2024, increasing operational risk.

Government digital transformation spending

Public sector modernization drives a steady pipeline for data intelligence firms; global government digital transformation spending reached about $1.2 trillion in 2024 and OECD reports show a 12–20% budget increase for sovereign cloud/digital sovereignty projects by end-2025 in several EU countries. Keyrus should align its roadmap to national agendas to target high-value contracts that demand localized data handling and compliance expertise, where contract sizes often exceed €5–20m.

Data sovereignty and regional policies

Political moves toward data localization force Keyrus to adjust implementation strategies for multinationals; over 70 countries had data residency laws by 2024, up from ~50 in 2018, affecting cloud architectures and raising compliance costs by an estimated 10–15% per project. Governments now mandate in-country processing for sectors like finance and health, so Keyrus must design regional data meshes and local hosting to preserve trust and avoid fines that can reach 2–4% of global turnover under some regimes.

International trade relations and tech exports

International trade agreements and diplomatic ties shape Keyrus’s ability to deploy consultants and export digital solutions; in 2024 cross-border services accounted for about 38% of global IT consulting revenue, affecting project routing and margins.

Stricter work-visa rules or tariffs raise labor mobility costs—OECD reported a 12% rise in compliance costs for cross-border services in 2023—forcing reallocation of onshore/offshore staffing.

Continuous monitoring of trade policy shifts is essential to adapt Keyrus’s global delivery model and optimize resource allocation to protect a reported 15% international revenue share growth target for 2025.

- Trade agreements determine market access and consultant mobility

- Visa/tariff changes increase delivery costs and staffing complexity

- Monitor policies to rebalance onshore/offshore capacity and meet 2025 targets

Public sector AI adoption frameworks

As of late 2025, over 40 countries have enacted public sector AI frameworks tightening requirements on fairness, explainability and data provenance; Keyrus must certify compliance with these standards to qualify for state contracts worth an estimated €6–12bn annually in EU digital transformation tenders.

Noncompliance risks exclusion from major procurements—e.g., EU/Member State procurements now mandate AI impact assessments and auditability, with penalties up to 5% of annual global revenue for vendors failing transparency rules.

- Mandatory AI impact assessments in 40+ countries by 2025

- State tenders in EU worth ~€6–12bn/year require compliance

- Penalties up to 5% of global revenue for transparency breaches

- Keyrus must ensure fairness, explainability, provenance and auditability

Keyrus faces EU-concentrated growth risk, rising compliance costs and AI regulatory exposure

Keyrus’s Eurocentric revenue mix (62% in 2024) raises exposure to EU policy and slower Eurozone growth (0.6% in 2024); geopolitical tensions across 20+ countries and rising data localization (70+ countries by 2024) increase compliance costs (~10–15%) and operational risk, while public sector digital/A I tenders (~€6–12bn/yr) demand strict compliance (40+ countries with AI rules by 2025; fines up to 5% revenue).

| Metric | Value |

|---|---|

| 2024 Eurozone share | 62% |

| Euro area GDP growth 2024 | 0.6% |

| Countries with data residency (2024) | 70+ |

| Compliance cost increase | 10–15% |

| AI frameworks by 2025 | 40+ |

| EU digital tenders/year | €6–12bn |

| Max penalties for AI noncompliance | ~5% global revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Keyrus across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to identify strategic threats and opportunities.

Provides a concise, visually segmented PESTLE summary of Keyrus that’s easy to drop into presentations, share across teams, and adapt with notes for regional or business-line specifics, streamlining external risk discussions and strategic planning.

Economic factors

Inflationary pressures on consulting fees

Rising global inflation—CPI averaging 6.8% in 2024 and projected ~4.2% in 2025 in OECD economies—has pushed consulting rates up 6–9% as firms protect margins; Keyrus faces similar upward pricing pressure. Clients report 72% greater price sensitivity, demanding clear ROI metrics per digital project, pressuring Keyrus to justify fees with measurable KPIs. Balancing competitive pricing against 8–12% higher tech and talent costs is critical.

Global currency exchange volatility

As an international firm reporting in Euros but operating in Dollars, Brazilian Reals and other currencies, Keyrus faces material FX risk: EUR weakened ~4% vs USD in 2024 and BRL swung ~12% vs EUR in 2023–24, which can compress consolidated revenue and inflate local operating costs.

A 10% adverse move in major currencies could change reported EBITDA by low- to mid-single digits, so disciplined hedging and rolling FX forecasts are critical.

Corporate budget shifts toward automation

Economic uncertainty has pushed 62% of CIOs (Gartner 2024) to prioritize cost-optimization and automation over broad innovation, creating demand for Keyrus services that drive efficiency; positioning its BI and data-science suites as ROI-focused automation tools can capture this shift. The 2025 McKinsey estimate that automation could cut operational costs by up to 20% reinforces the case for Keyrus to market solutions that enable doing more with fewer staff.

Tech talent acquisition costs

The market for data scientists and digital transformation experts remains tight; global median data scientist salaries rose ~12% in 2024, with US medians around $120k–$140k, pushing recruitment costs higher for Keyrus.

Keyrus must boost retention and employer branding—benchmarks show retention programs can reduce turnover costs by 20–30%—or face margin pressure from rising compensation and hiring fees.

High tech turnover (industry annual attrition ~18–25% in 2024) threatens project continuity and quality, requiring contingency staffing and higher training spend.

- Salary inflation: +12% (2024) for data scientists; US median $120k–$140k

- Attrition: industry 18–25% (2024)

- Retention programs can cut turnover costs 20–30%

- Higher recruiting/training costs compress margins if not offset by pricing

Interest rate impact on digital investment

Higher rates through 2023–2024 pushed corporate capex cuts—global capex fell 2.1% in 2024—causing Keyrus clients to tighten digital investment, with many projects delayed or downsized.

With policy rates peaking (e.g., US Fed funds ~5.25% end-2024) and stabilizing by late 2025, procurement now requires stronger ROI proofs, lengthening Keyrus’s sales cycles by an estimated 20–30%.

Keyrus should shift to modular, lower-entry offerings and flexible pricing to match clients’ risk aversion and constrained budgets.

- Capex down 2.1% (2024)

- Sales-cycle length +20–30%

- Fed funds ~5.25% (end-2024)

- Recommend modular services, flexible pricing

Inflation, wage pressure and FX squeeze margins—ROI‑driven consulting amid longer sales cycles

Inflationary pressure (OECD CPI 6.8% in 2024; projected ~4.2% in 2025) raises consulting rates 6–9% while client price sensitivity (+72%) forces ROI‑driven proposals; salary inflation for data scientists +12% (2024; US median $120k–$140k) and attrition 18–25% compress margins; FX volatility (EUR −4% vs USD in 2024; BRL ±12% 2023–24) risks low‑mid single‑digit EBITDA swings; capex −2.1% (2024) lengthens sales cycles 20–30%.

| Metric | 2024/2025 |

|---|---|

| OECD CPI | 6.8% (2024); ~4.2% (2025) |

| Consulting rate rise | 6–9% |

| Data scientist salary | +12%; US $120k–$140k |

| Attrition | 18–25% |

| FX moves | EUR −4% vs USD (2024); BRL ±12% |

| Capex | −2.1% (2024) |

| Sales cycle | +20–30% |

What You See Is What You Get

Keyrus PESTLE Analysis

The preview shown here is the exact Keyrus PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.