Kforce Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

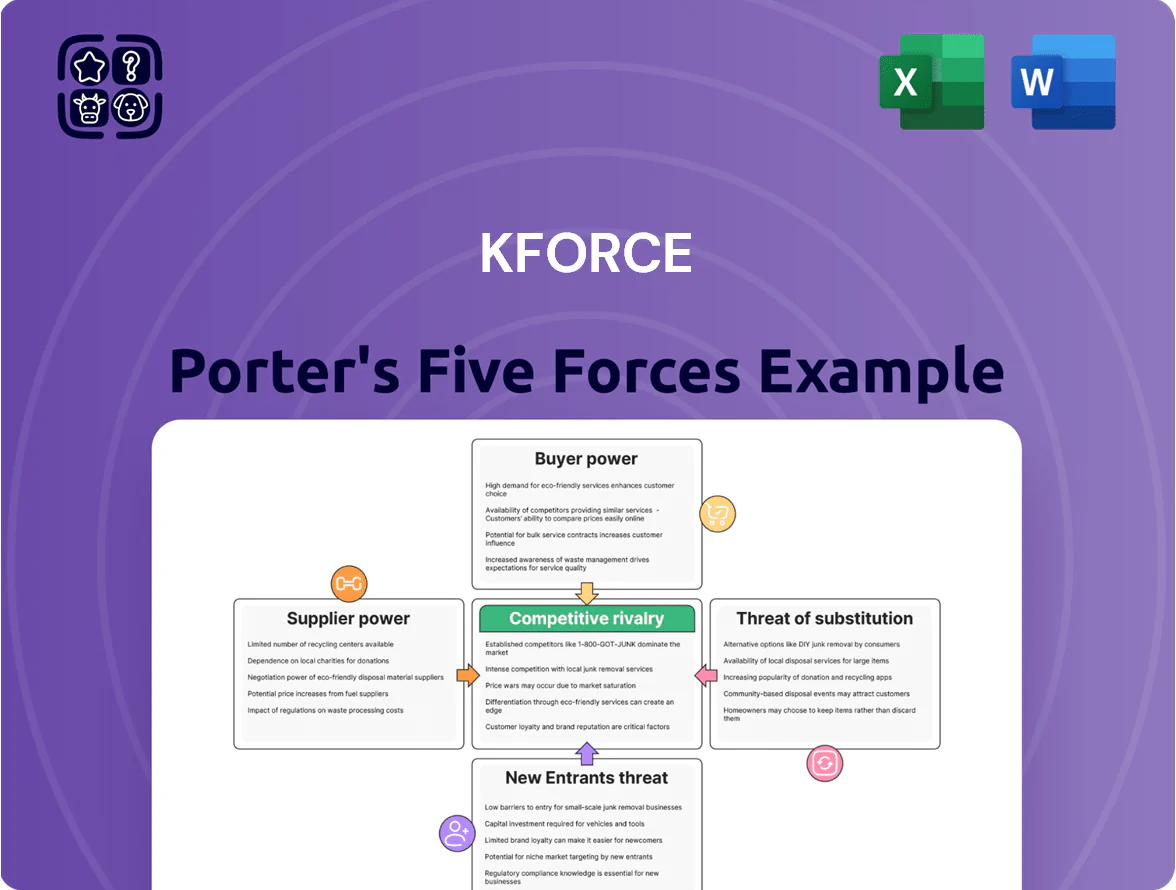

Kforce operates in a talent-driven staffing market where buyer power, supplier constraints, and competitive rivalry shape margin pressure and growth potential; regulatory shifts and technology adoption add external volatility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kforce’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report—force-by-force ratings, visuals, and actionable insights—to inform investment or strategic decisions with confidence.

Suppliers Bargaining Power

Scarcity of specialized technology talent

The primary suppliers for Kforce are skilled tech and finance professionals; by late 2025 a US shortfall of 1.4 million software developers raised their bargaining power, enabling demands for 15–30% higher pay and hybrid work, per CompTIA and Dice reports.

Influence of educational and certification bodies

Dependency on recruitment technology vendors

Kforce relies on job boards, applicant tracking systems, and AI sourcing tools; top providers like LinkedIn and iCIMS can set prices and control analytics access, giving them bargaining leverage.

A 2024 survey showed 62% of staffing firms cite platform fees as a major cost; a 10% license increase could cut Kforce’s gross margin by ~0.6 percentage points given 2024 tech spend of ~$40M.

Geographic concentration of talent hubs

Suppliers of labor cluster in urban tech hubs like Austin and Seattle, causing localized wage inflation—US tech wages rose ~6.5% in 2024 in those metros versus 3.2% national tech wage growth (BLS, 2024).

Kforce must manage regional labor laws and cost-of-living pay adjustments—median rent in San Francisco was $3,200/mo in 2024, driving higher contractor rate expectations.

Geographic dependency forces Kforce to keep a broad recruiting network across 20+ US markets (internal 2024 data) to dilute bargaining power of local talent pools.

- Concentrated hubs raise local pay 2–3% above national averages

- 20+ markets needed to mitigate cluster risk (Kforce 2024)

- Regional laws and COLA drive contract pricing

Rise of independent contractor platforms

The rise of platforms like Upwork and Toptal (Upwork reported $1.1B revenue in 2024; Toptal 2024 network ~200k experts) lets skilled pros reach clients directly, boosting individual suppliers' leverage against agencies.

More contractors choose self-employment—US freelance income hit $1.3T in 2023—so Kforce must offer career coaching, exclusive enterprise roles, and faster placements to retain talent.

Talent squeeze, rising certs and platforms boost supplier power over Kforce

Suppliers (skilled tech/finance talent, certifying institutions, platforms) hold moderate-to-high bargaining power for Kforce due to a 1.4M US developer shortfall (2025), 23% YoY rise in cybersecurity cert holders (410k in 2024), 6.5% metro tech wage growth (2024), and platform shifts (Upwork $1.1B 2024) that raise pay and speed demands.

| Metric | Value |

|---|---|

| Dev shortfall (U.S.) | 1.4M (2025) |

| Cyber certs | 410k, +23% YoY (2024) |

| Metro tech wage growth | 6.5% (2024) |

| Upwork revenue | $1.1B (2024) |

What is included in the product

Uncovers Kforce’s competitive pressures by detailing rivalry, supplier and buyer power, threat of entrants and substitutes, and regulatory or technological disruptors to assess pricing leverage, market share risks, and strategic defenses.

Condenses Kforce's competitive landscape into a one-sheet Porter's Five Forces snapshot—ideal for quick strategy pivots and investor briefings.

Customers Bargaining Power

Concentration of large enterprise clients

A significant share of Kforce’s 2024 revenue—about 45% of total net services revenue—comes from Fortune 500 firms and large financial institutions, giving those buyers strong leverage.

These high-volume clients routinely push for volume discounts, extended payment terms and strict SLAs, compressing Kforce’s gross margins (Q4 2024 gross margin 16.8%).

Loss of one major account can cut revenue materially; a single top-10 client represented roughly 7% of 2024 revenue, forcing price concessions to retain business.

Low switching costs for staffing services

Clients can switch staffing agencies easily or use several at once, and US staffing turnover averages 22% annually in 2024, increasing buyer mobility.

There are minimal financial penalties to stop using Kforce—placement fees are paid per hire—so clients often move to competitors for next projects or permanent hires.

This low switching cost forces Kforce to maintain high-quality candidates and service; Kforce reported 2024 gross margin pressure as client churn rose 3.1 percentage points year-over-year.

Utilization of Managed Service Providers

Many large clients route contingent labor through MSPs and VMS, which in 2024 managed roughly 70% of enterprise contingent spend, reducing direct Kforce-client contact and standardizing markups to 15–25%, so services trend toward commodity status.

These intermediaries enforce rate cards and SLAs, pushing procurement decisions toward lowest cost; Kforce must compete on price within narrow margins rather than on bespoke relationship value, pressuring gross margins (Kforce GAAP gross margin was 35.0% in FY2024).

Internal talent acquisition capabilities

Advancements in AI recruitment let clients cut agency spend: 2024 HR tech investments rose 18% and 42% of firms used AI sourcing, reducing reliance on firms like Kforce.

As companies source via social media and internal databases, Kforce must sell access to niche, hard-to-find talent and offer outcome-based fees to retain clients.

- 2024 HR tech spend +18%

- 42% firms use AI sourcing (2024)

- Kforce focus: niche talent, outcome pricing

Economic sensitivity of hiring budgets

Corporate clients scale hiring budgets with macro shifts and cash flow; in 2023–2024 tech and financial clients cut freelance spend ~12–18%, hitting staffing firms’ margins.

In downturns clients freeze roles or shift to lower-cost offshore labor, which reduces Kforce’s pricing leverage despite its US-based flexible staffing model.

Kforce can offer temp-to-perm and managed services, but final headcount decisions rest with customers, so revenue is cyclical and sensitive to unemployment and client capex.

- 2023–24 client hiring cuts ~12–18%

- Offshoring lowers bill rates 15–30% vs US talent

- Kforce strengths: flexible staffing, managed services

- Key risk: client-controlled headcount, cyclical revenue

Large clients squeeze margins as AI/MSP-driven commoditization pressures pricing

Large enterprise clients (≈45% of 2024 net services revenue) have strong leverage, forcing discounts, longer payment terms and strict SLAs, which compressed Q4 2024 gross margin to 16.8% and FY2024 GAAP gross margin to 35.0%; top-10 client ≈7% of revenue. Low switching costs, MSP/VMS use (~70% of contingent spend) and rising AI sourcing (42% firms, HR tech spend +18% in 2024) push pricing toward commodity.

| Metric | 2023–24 |

|---|---|

| Share from large clients | ≈45% |

| Top-10 client | ≈7% |

| Q4 gross margin | 16.8% |

| FY2024 GAAP gross margin | 35.0% |

| MSP/VMS managed spend | ≈70% |

| Firms using AI sourcing | 42% |

| HR tech spend change | +18% |

Preview the Actual Deliverable

Kforce Porter's Five Forces Analysis

This preview shows the exact Kforce Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kforce operates in a talent-driven staffing market where buyer power, supplier constraints, and competitive rivalry shape margin pressure and growth potential; regulatory shifts and technology adoption add external volatility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kforce’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report—force-by-force ratings, visuals, and actionable insights—to inform investment or strategic decisions with confidence.

Suppliers Bargaining Power

Scarcity of specialized technology talent

The primary suppliers for Kforce are skilled tech and finance professionals; by late 2025 a US shortfall of 1.4 million software developers raised their bargaining power, enabling demands for 15–30% higher pay and hybrid work, per CompTIA and Dice reports.

Influence of educational and certification bodies

Dependency on recruitment technology vendors

Kforce relies on job boards, applicant tracking systems, and AI sourcing tools; top providers like LinkedIn and iCIMS can set prices and control analytics access, giving them bargaining leverage.

A 2024 survey showed 62% of staffing firms cite platform fees as a major cost; a 10% license increase could cut Kforce’s gross margin by ~0.6 percentage points given 2024 tech spend of ~$40M.

Geographic concentration of talent hubs

Suppliers of labor cluster in urban tech hubs like Austin and Seattle, causing localized wage inflation—US tech wages rose ~6.5% in 2024 in those metros versus 3.2% national tech wage growth (BLS, 2024).

Kforce must manage regional labor laws and cost-of-living pay adjustments—median rent in San Francisco was $3,200/mo in 2024, driving higher contractor rate expectations.

Geographic dependency forces Kforce to keep a broad recruiting network across 20+ US markets (internal 2024 data) to dilute bargaining power of local talent pools.

- Concentrated hubs raise local pay 2–3% above national averages

- 20+ markets needed to mitigate cluster risk (Kforce 2024)

- Regional laws and COLA drive contract pricing

Rise of independent contractor platforms

The rise of platforms like Upwork and Toptal (Upwork reported $1.1B revenue in 2024; Toptal 2024 network ~200k experts) lets skilled pros reach clients directly, boosting individual suppliers' leverage against agencies.

More contractors choose self-employment—US freelance income hit $1.3T in 2023—so Kforce must offer career coaching, exclusive enterprise roles, and faster placements to retain talent.

Talent squeeze, rising certs and platforms boost supplier power over Kforce

Suppliers (skilled tech/finance talent, certifying institutions, platforms) hold moderate-to-high bargaining power for Kforce due to a 1.4M US developer shortfall (2025), 23% YoY rise in cybersecurity cert holders (410k in 2024), 6.5% metro tech wage growth (2024), and platform shifts (Upwork $1.1B 2024) that raise pay and speed demands.

| Metric | Value |

|---|---|

| Dev shortfall (U.S.) | 1.4M (2025) |

| Cyber certs | 410k, +23% YoY (2024) |

| Metro tech wage growth | 6.5% (2024) |

| Upwork revenue | $1.1B (2024) |

What is included in the product

Uncovers Kforce’s competitive pressures by detailing rivalry, supplier and buyer power, threat of entrants and substitutes, and regulatory or technological disruptors to assess pricing leverage, market share risks, and strategic defenses.

Condenses Kforce's competitive landscape into a one-sheet Porter's Five Forces snapshot—ideal for quick strategy pivots and investor briefings.

Customers Bargaining Power

Concentration of large enterprise clients

A significant share of Kforce’s 2024 revenue—about 45% of total net services revenue—comes from Fortune 500 firms and large financial institutions, giving those buyers strong leverage.

These high-volume clients routinely push for volume discounts, extended payment terms and strict SLAs, compressing Kforce’s gross margins (Q4 2024 gross margin 16.8%).

Loss of one major account can cut revenue materially; a single top-10 client represented roughly 7% of 2024 revenue, forcing price concessions to retain business.

Low switching costs for staffing services

Clients can switch staffing agencies easily or use several at once, and US staffing turnover averages 22% annually in 2024, increasing buyer mobility.

There are minimal financial penalties to stop using Kforce—placement fees are paid per hire—so clients often move to competitors for next projects or permanent hires.

This low switching cost forces Kforce to maintain high-quality candidates and service; Kforce reported 2024 gross margin pressure as client churn rose 3.1 percentage points year-over-year.

Utilization of Managed Service Providers

Many large clients route contingent labor through MSPs and VMS, which in 2024 managed roughly 70% of enterprise contingent spend, reducing direct Kforce-client contact and standardizing markups to 15–25%, so services trend toward commodity status.

These intermediaries enforce rate cards and SLAs, pushing procurement decisions toward lowest cost; Kforce must compete on price within narrow margins rather than on bespoke relationship value, pressuring gross margins (Kforce GAAP gross margin was 35.0% in FY2024).

Internal talent acquisition capabilities

Advancements in AI recruitment let clients cut agency spend: 2024 HR tech investments rose 18% and 42% of firms used AI sourcing, reducing reliance on firms like Kforce.

As companies source via social media and internal databases, Kforce must sell access to niche, hard-to-find talent and offer outcome-based fees to retain clients.

- 2024 HR tech spend +18%

- 42% firms use AI sourcing (2024)

- Kforce focus: niche talent, outcome pricing

Economic sensitivity of hiring budgets

Corporate clients scale hiring budgets with macro shifts and cash flow; in 2023–2024 tech and financial clients cut freelance spend ~12–18%, hitting staffing firms’ margins.

In downturns clients freeze roles or shift to lower-cost offshore labor, which reduces Kforce’s pricing leverage despite its US-based flexible staffing model.

Kforce can offer temp-to-perm and managed services, but final headcount decisions rest with customers, so revenue is cyclical and sensitive to unemployment and client capex.

- 2023–24 client hiring cuts ~12–18%

- Offshoring lowers bill rates 15–30% vs US talent

- Kforce strengths: flexible staffing, managed services

- Key risk: client-controlled headcount, cyclical revenue

Large clients squeeze margins as AI/MSP-driven commoditization pressures pricing

Large enterprise clients (≈45% of 2024 net services revenue) have strong leverage, forcing discounts, longer payment terms and strict SLAs, which compressed Q4 2024 gross margin to 16.8% and FY2024 GAAP gross margin to 35.0%; top-10 client ≈7% of revenue. Low switching costs, MSP/VMS use (~70% of contingent spend) and rising AI sourcing (42% firms, HR tech spend +18% in 2024) push pricing toward commodity.

| Metric | 2023–24 |

|---|---|

| Share from large clients | ≈45% |

| Top-10 client | ≈7% |

| Q4 gross margin | 16.8% |

| FY2024 GAAP gross margin | 35.0% |

| MSP/VMS managed spend | ≈70% |

| Firms using AI sourcing | 42% |

| HR tech spend change | +18% |

Preview the Actual Deliverable

Kforce Porter's Five Forces Analysis

This preview shows the exact Kforce Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; fully formatted, professionally written, and ready for download and use the moment you buy.