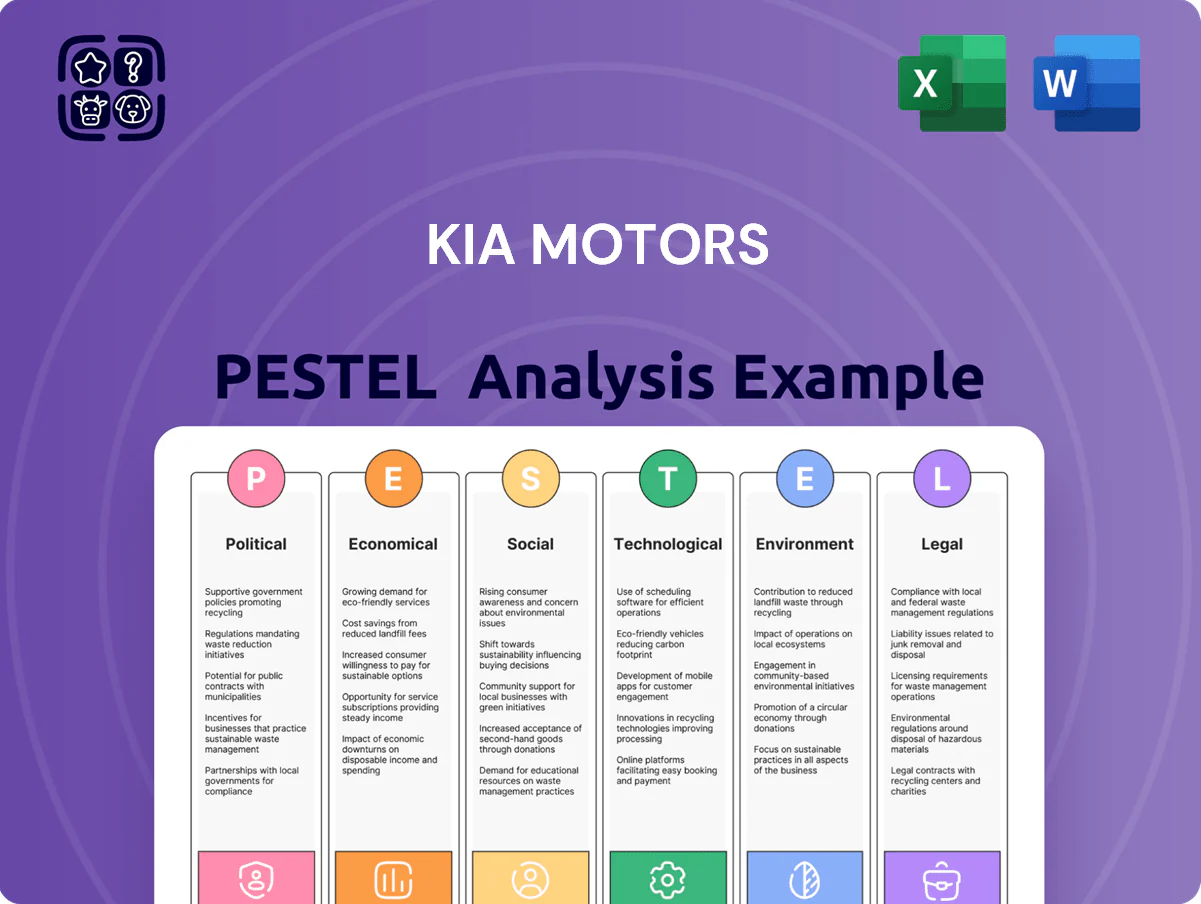

Kia Motors PESTLE Analysis

Your Competitive Advantage Starts with This Report

Stay ahead with our targeted PESTLE Analysis of Kia Motors—uncover how regulatory shifts, economic cycles, and tech disruption will shape its strategy and valuation; use these insights to refine investments or corporate plans. Buy the full report for a complete, actionable breakdown in editable formats and get instant clarity for decision-making.

Political factors

Global Trade Protectionism and Tariffs

The rise of protectionism in key markets like the US and EU threatens Kia’s export model; US tariffs and EU anti-subsidy probes could raise costs after 2024–25, with potential duties adding 5–15% to unit prices. Local content rules and the US Inflation Reduction Act incentives force Kia to accelerate local production—Kia invested $3.1bn in U.S. plants through 2025—to preserve price competitiveness and avoid penalties.

South Korean Geopolitical Stability

As a South Korean corporation, Kia faces exposure to Korean Peninsula tensions that can sway investor sentiment and credit metrics; Moody’s in 2025 noted geopolitical risk as a key sovereign pressure point for Korea’s Aa2 rating. Any escalation could disrupt Kia’s domestic plants and Korea’s integrated auto supply chain, which accounted for roughly 40% of Kia’s global parts sourcing in 2024. Management must keep contingency plans and inventory buffers to mitigate North Korean volatility and alliance-driven security risks.

EV Incentive Policies and Subsidies

Government EV incentives remain central to Kia's Plan S, with global subsidies totaling roughly $375 billion cumulatively by 2024 supporting EV adoption; however, political cycles risk sudden changes—e.g., US federal EV tax credit revisions in 2023 and varying EU national schemes reduced some consumer benefits in 2024. Kia tracks legislative shifts to reallocate marketing and adjust 2025 regional sales targets for EV6 and EV9, protecting margins and deployment of €2.5 billion charging investments.

Supply Chain Regionalization Requirements

Political pressure to de-risk supply chains from China has pushed Kia to diversify sourcing of critical minerals and semiconductors, prompting announced investments of about $5.6 billion (2024–2026) in regional manufacturing and supply hubs across Korea, Europe and North America.

Growing mandates require high-tech automotive components be produced within friendly trade blocs; tariffs and local-content rules raise Kia’s localization capex and increase per-vehicle BOM costs by an estimated 3–5%.

To secure battery materials, Kia is investing in regional lithium/nickel partnerships and logistics, targeting a 40% reduction in China-dependent procurement by 2026 to ensure uninterrupted access.

- Capex committed: ~$5.6bn (2024–2026)

- Projected BOM cost rise: 3–5%

- Target China-dependence cut: 40% by 2026

Diplomatic Relations with Major Markets

Diplomatic ties shape Kia’s sales: in 2024 China accounted for about 14% of Hyundai Motor Group’s global volume while Russia dropped below 1% after 2022 sanctions, showing sensitivity to South Korea’s foreign policy.

Geopolitical alignment can trigger boycotts or tariffs—China’s informal consumer actions in 2017 cut Korean car sales sharply—raising regulatory risk to market share.

Kia needs neutral, proactive corporate diplomacy to safeguard ~3.9 million unit global sales (2024) and long-term expansion.

- China ~14% of group volume (2024)

- Russia <1% post-2022 sanctions

- Global sales ~3.9M units (2024)

- Corporate diplomacy reduces boycott/regulatory risk

Kia ramps $5.6B de-risking, U.S. $3.1B push as localization lifts BOM 3–5%

Political risks—protectionism, local-content rules and shifting EV incentives—raise Kia’s localization capex and per-vehicle BOM by ~3–5%; Korea geopolitical tension affects supply chains (40% parts sourcing 2024) and investor sentiment; Kia committed ~$5.6bn (2024–26) to de-risk China dependence, targeting 40% reduction by 2026 while U.S. investment reached $3.1bn through 2025.

| Metric | Value |

|---|---|

| Capex committed (2024–26) | $5.6bn |

| US investment through 2025 | $3.1bn |

| Parts from Korea (2024) | 40% |

| Target China dependence cut by 2026 | 40% |

| Estimated BOM cost rise | 3–5% |

What is included in the product

Explores how macro-environmental forces uniquely affect Kia Motors across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Kia Motors that’s easy to drop into presentations, share across teams, and customize with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Fluctuations and Financing Costs

High global interest rates through 2025—with US Fed funds at 5.25–5.50% and ECB rates near 3.75%—have raised consumer auto loan costs, contributing to a 2024 global light-vehicle sales decline of ~3% and pressuring Kia's volumes.

Higher corporate borrowing widened Kia Corp.'s blended effective interest cost, increasing capital expenditure for EV line conversions; Kia planned KRW 20.7 trillion capex for 2024–2025, stressing financing needs.

Kia Finance must offer competitive APRs and promotions to sustain demand; in 2024 Kia used targeted low-rate financing and incentives to support retail sales and offset restrictive monetary policy impacts.

Raw Material Price Volatility for Batteries

The economic viability of Kia’s EV portfolio is highly sensitive to lithium, nickel and cobalt prices; lithium carbonate averaged about $40,000/ton in 2025 vs peaks >$80,000 in 2022, while nickel and cobalt remain 20–35% volatile year-over-year, pressuring margins and MSRP strategies.

Although prices have stabilized from 2022 peaks, underlying volatility persists and can erode gross margins by an estimated 3–6 percentage points on battery costs under downside scenarios.

Kia is mitigating risk through multiyear supply contracts covering roughly 60–70% of near-term needs and by participating in direct mining investments and offtake agreements to cap exposure to sudden commodity spikes.

Currency Exchange Rate Risks

As a global exporter, Kia's revenue and margins are sensitive to KRW/USD and KRW/EUR moves; a 10% appreciation of the won versus the dollar could cut export competitiveness, while a 10% depreciation can raise import costs for parts—Kia reported net transaction exposure hedged at about $8.5bn in 2024 and uses forwards, options and swaps to stabilize prices, aiming to cap currency impact within low-single-digit percentage points of operating profit.

Global Economic Growth Deceleration

Slowing global GDP growth in 2025—IMF projected world growth at 3.0% and advanced economies at 1.6%—has dampened spending on durables, prompting Kia to shift toward lower-priced entry EVs and hybrids to attract value-driven buyers.

In response, Kia expanded affordable EV offerings and flexible financing; it also reallocates inventory from softer regions to resilient markets like Southeast Asia and the US to protect volumes.

- IMF 2025 world growth ~3.0%, advanced economies ~1.6%

- Kia increasing entry EV/hybrid mix to capture value buyers

- Inventory reallocation to resilient markets (US, SE Asia)

Rising Disposable Income in Emerging Markets

Rising middle-class incomes in India and Southeast Asia boost demand for ICE and hybrid vehicles, with India contributing about 12% of Kia’s global volumes by 2024 and passenger-vehicle sales in India rising ~7% YoY in 2023–24.

Kia must localize product development and pricing to match regional affordability—India’s per-capita GDP reached ~$2,500 in 2024—enabling the company to offset slower growth in saturated Western markets.

- India ~12% of Kia global volumes (2024)

- India PV sales +7% YoY (2023–24)

- India per-capita GDP ~$2,500 (2024)

- Growth opportunity in ICE/hybrid demand across Southeast Asia

Kia weathers weaker auto demand, KRW20.7T capex, $8.5B hedges; lithium risk trims margins

Higher global rates raised auto loan costs, contributing to ~3% 2024 light-vehicle sales decline; Kia planned KRW 20.7T capex (2024–25) and hedged ~$8.5B FX exposure. Lithium ~$40k/ton (2025), commodity volatility can cut gross margin 3–6 ppt. IMF 2025 world growth ~3.0%, advanced ~1.6%; India ~12% of Kia volumes (2024), PV sales +7% YoY.

| Metric | Value |

|---|---|

| 2024 LV sales change | -3% |

| Capex 2024–25 | KRW 20.7T |

| Hedged FX (2024) | $8.5B |

| Lithium (2025) | $40,000/ton |

| IMF world growth (2025) | 3.0% |

| India share (2024) | ~12% |

Same Document Delivered

Kia Motors PESTLE Analysis

The preview shown here is the exact Kia Motors PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it contains the same content, layout, and analysis visible now with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Stay ahead with our targeted PESTLE Analysis of Kia Motors—uncover how regulatory shifts, economic cycles, and tech disruption will shape its strategy and valuation; use these insights to refine investments or corporate plans. Buy the full report for a complete, actionable breakdown in editable formats and get instant clarity for decision-making.

Political factors

Global Trade Protectionism and Tariffs

The rise of protectionism in key markets like the US and EU threatens Kia’s export model; US tariffs and EU anti-subsidy probes could raise costs after 2024–25, with potential duties adding 5–15% to unit prices. Local content rules and the US Inflation Reduction Act incentives force Kia to accelerate local production—Kia invested $3.1bn in U.S. plants through 2025—to preserve price competitiveness and avoid penalties.

South Korean Geopolitical Stability

As a South Korean corporation, Kia faces exposure to Korean Peninsula tensions that can sway investor sentiment and credit metrics; Moody’s in 2025 noted geopolitical risk as a key sovereign pressure point for Korea’s Aa2 rating. Any escalation could disrupt Kia’s domestic plants and Korea’s integrated auto supply chain, which accounted for roughly 40% of Kia’s global parts sourcing in 2024. Management must keep contingency plans and inventory buffers to mitigate North Korean volatility and alliance-driven security risks.

EV Incentive Policies and Subsidies

Government EV incentives remain central to Kia's Plan S, with global subsidies totaling roughly $375 billion cumulatively by 2024 supporting EV adoption; however, political cycles risk sudden changes—e.g., US federal EV tax credit revisions in 2023 and varying EU national schemes reduced some consumer benefits in 2024. Kia tracks legislative shifts to reallocate marketing and adjust 2025 regional sales targets for EV6 and EV9, protecting margins and deployment of €2.5 billion charging investments.

Supply Chain Regionalization Requirements

Political pressure to de-risk supply chains from China has pushed Kia to diversify sourcing of critical minerals and semiconductors, prompting announced investments of about $5.6 billion (2024–2026) in regional manufacturing and supply hubs across Korea, Europe and North America.

Growing mandates require high-tech automotive components be produced within friendly trade blocs; tariffs and local-content rules raise Kia’s localization capex and increase per-vehicle BOM costs by an estimated 3–5%.

To secure battery materials, Kia is investing in regional lithium/nickel partnerships and logistics, targeting a 40% reduction in China-dependent procurement by 2026 to ensure uninterrupted access.

- Capex committed: ~$5.6bn (2024–2026)

- Projected BOM cost rise: 3–5%

- Target China-dependence cut: 40% by 2026

Diplomatic Relations with Major Markets

Diplomatic ties shape Kia’s sales: in 2024 China accounted for about 14% of Hyundai Motor Group’s global volume while Russia dropped below 1% after 2022 sanctions, showing sensitivity to South Korea’s foreign policy.

Geopolitical alignment can trigger boycotts or tariffs—China’s informal consumer actions in 2017 cut Korean car sales sharply—raising regulatory risk to market share.

Kia needs neutral, proactive corporate diplomacy to safeguard ~3.9 million unit global sales (2024) and long-term expansion.

- China ~14% of group volume (2024)

- Russia <1% post-2022 sanctions

- Global sales ~3.9M units (2024)

- Corporate diplomacy reduces boycott/regulatory risk

Kia ramps $5.6B de-risking, U.S. $3.1B push as localization lifts BOM 3–5%

Political risks—protectionism, local-content rules and shifting EV incentives—raise Kia’s localization capex and per-vehicle BOM by ~3–5%; Korea geopolitical tension affects supply chains (40% parts sourcing 2024) and investor sentiment; Kia committed ~$5.6bn (2024–26) to de-risk China dependence, targeting 40% reduction by 2026 while U.S. investment reached $3.1bn through 2025.

| Metric | Value |

|---|---|

| Capex committed (2024–26) | $5.6bn |

| US investment through 2025 | $3.1bn |

| Parts from Korea (2024) | 40% |

| Target China dependence cut by 2026 | 40% |

| Estimated BOM cost rise | 3–5% |

What is included in the product

Explores how macro-environmental forces uniquely affect Kia Motors across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Kia Motors that’s easy to drop into presentations, share across teams, and customize with region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Fluctuations and Financing Costs

High global interest rates through 2025—with US Fed funds at 5.25–5.50% and ECB rates near 3.75%—have raised consumer auto loan costs, contributing to a 2024 global light-vehicle sales decline of ~3% and pressuring Kia's volumes.

Higher corporate borrowing widened Kia Corp.'s blended effective interest cost, increasing capital expenditure for EV line conversions; Kia planned KRW 20.7 trillion capex for 2024–2025, stressing financing needs.

Kia Finance must offer competitive APRs and promotions to sustain demand; in 2024 Kia used targeted low-rate financing and incentives to support retail sales and offset restrictive monetary policy impacts.

Raw Material Price Volatility for Batteries

The economic viability of Kia’s EV portfolio is highly sensitive to lithium, nickel and cobalt prices; lithium carbonate averaged about $40,000/ton in 2025 vs peaks >$80,000 in 2022, while nickel and cobalt remain 20–35% volatile year-over-year, pressuring margins and MSRP strategies.

Although prices have stabilized from 2022 peaks, underlying volatility persists and can erode gross margins by an estimated 3–6 percentage points on battery costs under downside scenarios.

Kia is mitigating risk through multiyear supply contracts covering roughly 60–70% of near-term needs and by participating in direct mining investments and offtake agreements to cap exposure to sudden commodity spikes.

Currency Exchange Rate Risks

As a global exporter, Kia's revenue and margins are sensitive to KRW/USD and KRW/EUR moves; a 10% appreciation of the won versus the dollar could cut export competitiveness, while a 10% depreciation can raise import costs for parts—Kia reported net transaction exposure hedged at about $8.5bn in 2024 and uses forwards, options and swaps to stabilize prices, aiming to cap currency impact within low-single-digit percentage points of operating profit.

Global Economic Growth Deceleration

Slowing global GDP growth in 2025—IMF projected world growth at 3.0% and advanced economies at 1.6%—has dampened spending on durables, prompting Kia to shift toward lower-priced entry EVs and hybrids to attract value-driven buyers.

In response, Kia expanded affordable EV offerings and flexible financing; it also reallocates inventory from softer regions to resilient markets like Southeast Asia and the US to protect volumes.

- IMF 2025 world growth ~3.0%, advanced economies ~1.6%

- Kia increasing entry EV/hybrid mix to capture value buyers

- Inventory reallocation to resilient markets (US, SE Asia)

Rising Disposable Income in Emerging Markets

Rising middle-class incomes in India and Southeast Asia boost demand for ICE and hybrid vehicles, with India contributing about 12% of Kia’s global volumes by 2024 and passenger-vehicle sales in India rising ~7% YoY in 2023–24.

Kia must localize product development and pricing to match regional affordability—India’s per-capita GDP reached ~$2,500 in 2024—enabling the company to offset slower growth in saturated Western markets.

- India ~12% of Kia global volumes (2024)

- India PV sales +7% YoY (2023–24)

- India per-capita GDP ~$2,500 (2024)

- Growth opportunity in ICE/hybrid demand across Southeast Asia

Kia weathers weaker auto demand, KRW20.7T capex, $8.5B hedges; lithium risk trims margins

Higher global rates raised auto loan costs, contributing to ~3% 2024 light-vehicle sales decline; Kia planned KRW 20.7T capex (2024–25) and hedged ~$8.5B FX exposure. Lithium ~$40k/ton (2025), commodity volatility can cut gross margin 3–6 ppt. IMF 2025 world growth ~3.0%, advanced ~1.6%; India ~12% of Kia volumes (2024), PV sales +7% YoY.

| Metric | Value |

|---|---|

| 2024 LV sales change | -3% |

| Capex 2024–25 | KRW 20.7T |

| Hedged FX (2024) | $8.5B |

| Lithium (2025) | $40,000/ton |

| IMF world growth (2025) | 3.0% |

| India share (2024) | ~12% |

Same Document Delivered

Kia Motors PESTLE Analysis

The preview shown here is the exact Kia Motors PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it contains the same content, layout, and analysis visible now with no placeholders or surprises.