Kiliç Deniz PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of Kiliç Deniz—uncover how political shifts, economic trends, social dynamics, technological advances, legal constraints, and environmental pressures will shape its trajectory; this concise, expertly researched report arms investors and strategists with actionable insights. Purchase the full version to access the complete, editable analysis and make informed decisions with confidence.

Political factors

Geopolitical Trade Relations

Kiliç Deniz exports over 60% of its output to the EU and North America, so shifts in Turkey’s diplomatic ties can rapidly alter tariffs and non-tariff barriers affecting revenues; in 2024 Turkish seafood exports to the EU fell 8% amid rising trade frictions. Trade agreements or sanctions could change tariff rates on aquaculture products—affecting margins on export volumes worth hundreds of millions USD annually. Maintaining stable relations with key importers is therefore critical to protect high-volume export streams.

Government Subsidies and Support

Turkish government incentives bolster aquaculture—2024 support programs allocated roughly TRY 1.2 billion to fisheries and aquaculture, including feed subsidies, insurance premium aid and grants for tech upgrades that directly lower Kiliç Deniz’s production costs and capex needs.

A cut in agricultural subsidies or reallocation of budget (eg. if fisheries share falls from 2024’s ~3.5% of rural supports) would raise feed and insurance expenses, squeezing operational margins and slowing planned investments.

Regulatory Stability in Turkey

Operating in Turkey’s regulated aquaculture sector requires close engagement with ministries of Agriculture and Forestry; in 2024 Turkey reported 488,000 tonnes of marine aquaculture production, underscoring regulatory impact on supply chains. Political stability in these institutions supports predictable licensing and renewals for land and sea leases—critical given average lease durations of 10–20 years—while frequent administrative changes have in past years caused multi-month licensing delays, raising project IRR uncertainty.

International Food Safety Standards

- Comply with varied jurisdictional mandates (EU: 3,412 food alerts in 2024)

- Protectionism increases certification costs (~4–7% impact)

- Regulatory engagement cuts rejections by 12–18%

Regional Maritime Jurisdiction

Regional maritime jurisdiction affects Kiliç Deniz’s offshore farms, which operate amid Aegean and Eastern Mediterranean territorial disputes; UN data notes 6 active EEZ claims in the region as of 2025, constraining site expansion.

Political tensions can delay permits and raise security costs—average offshore security premiums rose ~18% for Mediterranean aquaculture in 2024—threatening asset uptime.

Close coordination with national maritime authorities and adherence to bilateral agreements is critical to secure long-term production hubs and concessional access to new sites.

- 6 overlapping EEZ claims (2025)

- 18% rise in regional offshore security premiums (2024)

- Permitting delays increase CAPEX timetable risks

Geopolitical and cost shocks threaten Turkish fisheries: EU exports down, security costs up

Political risks: 60%+ exports to EU/NA (EU exports -8% in 2024) make diplomatic shifts/tariffs material; Turkish aquaculture supports ~TRY 1.2bn in 2024 reducing costs; fisheries received ~3.5% of rural supports—cuts would raise feed/insurance costs; 6 overlapping EEZ claims (2025) and 18% rise in offshore security premiums (2024) increase permitting, CAPEX and operating risks.

| Metric | Value |

|---|---|

| Export share to EU/NA | 60%+ |

| EU export change 2024 | -8% |

| Govt support 2024 | TRY 1.2bn |

| EEZ claims (2025) | 6 |

| Offshore security ↑ (2024) | +18% |

What is included in the product

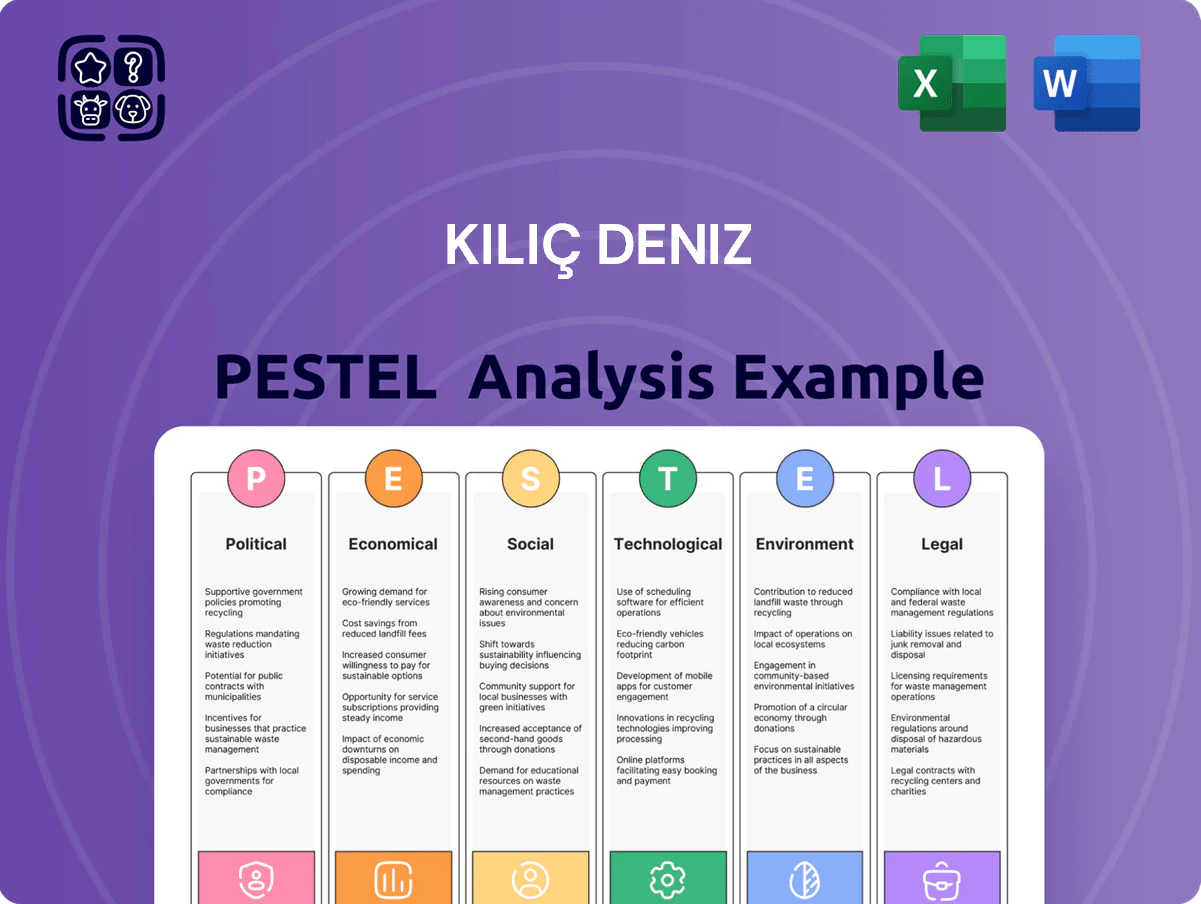

Explores how macro-environmental factors uniquely affect Kiliç Deniz across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to its region and maritime industry.

Condensed Kiliç Deniz PESTLE snapshot for quick reference in meetings or presentations, visually segmented for immediate insight and easily dropped into slides or reports.

Economic factors

Currency Fluctuations and Exchange Risk

Kılıç Deniz earns roughly 45–60% of revenue in EUR/USD while over 70% of operating costs are in TRY; with TRY falling about 35% vs USD between 2021–2024 and 18% vs EUR in 2023–2024, this mix partly hedges Lira depreciation but exposes margins to sharp swings.

Extreme FX volatility—daily USD/TRY swings exceeding 5% in crisis months—complicates cash-flow forecasting and increases cost of servicing TRY-denominated debt.

Active treasury measures—forward contracts, natural hedging via FX pricing and 2024 use of FX-linked pricing on ~40% of contracts—are essential to stabilize margins and protect balance sheet metrics like EBITDA/FX sensitivity.

Inflationary Pressures on Inputs

High Turkish inflation (year-end CPI ~64% in 2023, 2024 avg ~60%) drives up costs of fish feed, energy and labor, with feed often >50% of production costs; soybean and fishmeal price spikes in 2024 raised feed input costs by an estimated 20–35%, squeezing margins.

Global Seafood Market Demand

The economic health of major export markets like the EU and China—which accounted for ~60% of Turkish aquaculture exports in 2024—directly affects demand for premium sea bass and sea bream; GDP contractions or slower consumer spending reduce premium seafood purchases. During downturns, consumers shift to cheaper proteins, evidenced by a 2023–24 8% dip in average unit prices for Mediterranean sea bream. Monitoring indicators (GDP growth, CPI, real wages, FX) lets Kiliç Deniz adjust production and marketing to align with changing international purchasing power.

Interest Rates and Access to Capital

Expansion projects like processing plant upgrades and hatchery capacity increases need heavy debt-funded investment; Turkey's policy rate was 45% in March 2024 and 35% by Dec 2025, raising borrowing costs and risking slower growth for Kiliç Deniz.

Access to international credit and concessional loans—e.g., EBRD, IFC lines or Eurobond markets—remains critical to secure lower rates and sustain competitiveness in this capital-intensive sector.

- High domestic rates (45% in Mar 2024; 35% by Dec 2025) raise financing costs

- Debt-financed expansions sensitive to interest-rate fluctuations

- International/DFI financing can materially lower effective cost of capital

Logistics and Energy Costs

The cost of transporting fresh and frozen seafood to international markets is highly sensitive to fuel and freight rates; bunker fuel rose ~22% in 2024 vs 2023, pushing container rates up ~18% on key Asia-Europe routes.

Higher energy prices increase hatchery production costs (electricity, diesel) and risk cold-chain breaches—cold storage energy can represent 10–15% of processing costs.

Kiliç Deniz prioritizes SCM optimization and energy-saving tech (LED, heat recovery, solar) to hedge rising commodity prices and has targeted a 7–10% reduction in energy intensity by 2026.

- Fuel/freight volatility: bunker +22% (2024)

- Container rates: +18% (Asia-Europe)

- Cold storage = 10–15% processing costs

- Energy-intensity target: −7–10% by 2026

TRY inflation, FX mix and surging input costs squeeze margins—foreign funding vital

FX-heavy revenue (45–60% EUR/USD) vs >70% TRY costs, TRY depreciation (≈35% vs USD 2021–24; ≈18% vs EUR 2023–24) and 2023 CPI ~64% (2024 avg ~60%) squeeze margins; 2024 feed input rises +20–35%, bunker +22% and container rates +18% raise logistics; policy rates 45% Mar‑2024 → 35% Dec‑2025 increase financing costs; DFI/foreign credit critical to lower WACC.

| Metric | Value |

|---|---|

| Revenue FX share | 45–60% EUR/USD |

| Cost in TRY | >70% |

| TRY move | −35% vs USD (2021–24); −18% vs EUR (2023–24) |

| CPI | ~64% (2023); ~60% (2024 avg) |

| Feed cost rise | +20–35% (2024) |

| Policy rate | 45% Mar‑2024 → 35% Dec‑2025 |

| Bunker/container | +22% / +18% (2024) |

Preview the Actual Deliverable

Kiliç Deniz PESTLE Analysis

The preview shown here is the exact Kiliç Deniz PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with complete political, economic, social, technological, legal, and environmental insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our targeted PESTLE Analysis of Kiliç Deniz—uncover how political shifts, economic trends, social dynamics, technological advances, legal constraints, and environmental pressures will shape its trajectory; this concise, expertly researched report arms investors and strategists with actionable insights. Purchase the full version to access the complete, editable analysis and make informed decisions with confidence.

Political factors

Geopolitical Trade Relations

Kiliç Deniz exports over 60% of its output to the EU and North America, so shifts in Turkey’s diplomatic ties can rapidly alter tariffs and non-tariff barriers affecting revenues; in 2024 Turkish seafood exports to the EU fell 8% amid rising trade frictions. Trade agreements or sanctions could change tariff rates on aquaculture products—affecting margins on export volumes worth hundreds of millions USD annually. Maintaining stable relations with key importers is therefore critical to protect high-volume export streams.

Government Subsidies and Support

Turkish government incentives bolster aquaculture—2024 support programs allocated roughly TRY 1.2 billion to fisheries and aquaculture, including feed subsidies, insurance premium aid and grants for tech upgrades that directly lower Kiliç Deniz’s production costs and capex needs.

A cut in agricultural subsidies or reallocation of budget (eg. if fisheries share falls from 2024’s ~3.5% of rural supports) would raise feed and insurance expenses, squeezing operational margins and slowing planned investments.

Regulatory Stability in Turkey

Operating in Turkey’s regulated aquaculture sector requires close engagement with ministries of Agriculture and Forestry; in 2024 Turkey reported 488,000 tonnes of marine aquaculture production, underscoring regulatory impact on supply chains. Political stability in these institutions supports predictable licensing and renewals for land and sea leases—critical given average lease durations of 10–20 years—while frequent administrative changes have in past years caused multi-month licensing delays, raising project IRR uncertainty.

International Food Safety Standards

- Comply with varied jurisdictional mandates (EU: 3,412 food alerts in 2024)

- Protectionism increases certification costs (~4–7% impact)

- Regulatory engagement cuts rejections by 12–18%

Regional Maritime Jurisdiction

Regional maritime jurisdiction affects Kiliç Deniz’s offshore farms, which operate amid Aegean and Eastern Mediterranean territorial disputes; UN data notes 6 active EEZ claims in the region as of 2025, constraining site expansion.

Political tensions can delay permits and raise security costs—average offshore security premiums rose ~18% for Mediterranean aquaculture in 2024—threatening asset uptime.

Close coordination with national maritime authorities and adherence to bilateral agreements is critical to secure long-term production hubs and concessional access to new sites.

- 6 overlapping EEZ claims (2025)

- 18% rise in regional offshore security premiums (2024)

- Permitting delays increase CAPEX timetable risks

Geopolitical and cost shocks threaten Turkish fisheries: EU exports down, security costs up

Political risks: 60%+ exports to EU/NA (EU exports -8% in 2024) make diplomatic shifts/tariffs material; Turkish aquaculture supports ~TRY 1.2bn in 2024 reducing costs; fisheries received ~3.5% of rural supports—cuts would raise feed/insurance costs; 6 overlapping EEZ claims (2025) and 18% rise in offshore security premiums (2024) increase permitting, CAPEX and operating risks.

| Metric | Value |

|---|---|

| Export share to EU/NA | 60%+ |

| EU export change 2024 | -8% |

| Govt support 2024 | TRY 1.2bn |

| EEZ claims (2025) | 6 |

| Offshore security ↑ (2024) | +18% |

What is included in the product

Explores how macro-environmental factors uniquely affect Kiliç Deniz across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tailored to its region and maritime industry.

Condensed Kiliç Deniz PESTLE snapshot for quick reference in meetings or presentations, visually segmented for immediate insight and easily dropped into slides or reports.

Economic factors

Currency Fluctuations and Exchange Risk

Kılıç Deniz earns roughly 45–60% of revenue in EUR/USD while over 70% of operating costs are in TRY; with TRY falling about 35% vs USD between 2021–2024 and 18% vs EUR in 2023–2024, this mix partly hedges Lira depreciation but exposes margins to sharp swings.

Extreme FX volatility—daily USD/TRY swings exceeding 5% in crisis months—complicates cash-flow forecasting and increases cost of servicing TRY-denominated debt.

Active treasury measures—forward contracts, natural hedging via FX pricing and 2024 use of FX-linked pricing on ~40% of contracts—are essential to stabilize margins and protect balance sheet metrics like EBITDA/FX sensitivity.

Inflationary Pressures on Inputs

High Turkish inflation (year-end CPI ~64% in 2023, 2024 avg ~60%) drives up costs of fish feed, energy and labor, with feed often >50% of production costs; soybean and fishmeal price spikes in 2024 raised feed input costs by an estimated 20–35%, squeezing margins.

Global Seafood Market Demand

The economic health of major export markets like the EU and China—which accounted for ~60% of Turkish aquaculture exports in 2024—directly affects demand for premium sea bass and sea bream; GDP contractions or slower consumer spending reduce premium seafood purchases. During downturns, consumers shift to cheaper proteins, evidenced by a 2023–24 8% dip in average unit prices for Mediterranean sea bream. Monitoring indicators (GDP growth, CPI, real wages, FX) lets Kiliç Deniz adjust production and marketing to align with changing international purchasing power.

Interest Rates and Access to Capital

Expansion projects like processing plant upgrades and hatchery capacity increases need heavy debt-funded investment; Turkey's policy rate was 45% in March 2024 and 35% by Dec 2025, raising borrowing costs and risking slower growth for Kiliç Deniz.

Access to international credit and concessional loans—e.g., EBRD, IFC lines or Eurobond markets—remains critical to secure lower rates and sustain competitiveness in this capital-intensive sector.

- High domestic rates (45% in Mar 2024; 35% by Dec 2025) raise financing costs

- Debt-financed expansions sensitive to interest-rate fluctuations

- International/DFI financing can materially lower effective cost of capital

Logistics and Energy Costs

The cost of transporting fresh and frozen seafood to international markets is highly sensitive to fuel and freight rates; bunker fuel rose ~22% in 2024 vs 2023, pushing container rates up ~18% on key Asia-Europe routes.

Higher energy prices increase hatchery production costs (electricity, diesel) and risk cold-chain breaches—cold storage energy can represent 10–15% of processing costs.

Kiliç Deniz prioritizes SCM optimization and energy-saving tech (LED, heat recovery, solar) to hedge rising commodity prices and has targeted a 7–10% reduction in energy intensity by 2026.

- Fuel/freight volatility: bunker +22% (2024)

- Container rates: +18% (Asia-Europe)

- Cold storage = 10–15% processing costs

- Energy-intensity target: −7–10% by 2026

TRY inflation, FX mix and surging input costs squeeze margins—foreign funding vital

FX-heavy revenue (45–60% EUR/USD) vs >70% TRY costs, TRY depreciation (≈35% vs USD 2021–24; ≈18% vs EUR 2023–24) and 2023 CPI ~64% (2024 avg ~60%) squeeze margins; 2024 feed input rises +20–35%, bunker +22% and container rates +18% raise logistics; policy rates 45% Mar‑2024 → 35% Dec‑2025 increase financing costs; DFI/foreign credit critical to lower WACC.

| Metric | Value |

|---|---|

| Revenue FX share | 45–60% EUR/USD |

| Cost in TRY | >70% |

| TRY move | −35% vs USD (2021–24); −18% vs EUR (2023–24) |

| CPI | ~64% (2023); ~60% (2024 avg) |

| Feed cost rise | +20–35% (2024) |

| Policy rate | 45% Mar‑2024 → 35% Dec‑2025 |

| Bunker/container | +22% / +18% (2024) |

Preview the Actual Deliverable

Kiliç Deniz PESTLE Analysis

The preview shown here is the exact Kiliç Deniz PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with complete political, economic, social, technological, legal, and environmental insights.