Kimberly-Clark PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological change are reshaping Kimberly‑Clark’s competitive landscape—our concise PESTLE highlights risks and opportunities you can act on today; purchase the full analysis for a complete, ready-to-use strategic briefing.

Political factors

Global Trade Policy and Tariff Fluctuations

As of late 2025, Kimberly-Clark remains highly sensitive to shifting trade agreements and protectionist measures in markets like China and the EU; tariffs rose on average 8–12% for pulp and specialty polymers in 2024–25, pressuring margins. Increased import duties on wood pulp and polymers raised COGS by an estimated $120–180 million in 2025, forcing supply-chain rerouting. K-C must continuously adapt sourcing to preserve global pricing competitiveness.

Geopolitical Stability in Emerging Markets

Kimberly-Clark’s expansion in Latin America and Southeast Asia exposes it to localized political volatility; in 2024 these regions accounted for about 28% of net sales, heightening governance risk. Political unrest or sudden leadership changes can prompt currency devaluations—LATAM FX swung up to 18% vs USD in 2023—causing supply-chain and operational disruptions that compress margins. Strategic planners therefore emphasize regional diversification and local JVs; in 2024 the company increased local sourcing to 42% in key markets to hedge unpredictability.

Public Health Policy and Government Procurement

Corporate Taxation and International Tax Reform

- OECD/G20 Pillar Two: 15% global minimum tax

- Kimberly-Clark 2024 effective tax rate: ~18.6%

- 1% ETR rise ≈ $19M hit to 2024 adjusted net income

- R&D/manufacturing incentives affect investment location decisions

Regulatory Lobbying and Industry Standards

Kimberly-Clark spends millions on government relations to shape safety and manufacturing standards, reporting $40M in public policy and compliance-related expenses in 2024 and active participation in ASTM and ISO committees to influence product safety norms.

With global moves toward stricter consumer protection—EU’s 2023 Product Safety Regulation and U.S. state-level chemical disclosure laws—Kimberly-Clark maintains proactive legislative engagement to avoid abrupt compliance costs that could affect its 2024 operating margin of 11.2%.

This lobbying ensures corporate interests are represented while aligning with rising political expectations on corporate responsibility and sustainability reporting tied to investor scrutiny and ESG-linked credit terms.

- 2024 public policy spend: ~$40M

- 2024 operating margin: 11.2%

- Active in ASTM/ISO safety committees

- Key risks: EU product safety rules, U.S. chemical disclosure laws

Kimberly‑Clark faces tariff, FX and tax shocks risking $120–180M COGS hit and margin pressure

Political risks for Kimberly-Clark include rising trade tariffs (pulp/polymer duties +8–12% in 2024–25; COGS impact $120–180M in 2025), regional volatility (LATAM/SEA ~28% of sales; FX swings up to 18% in 2023), tax shifts (2024 ETR ~18.6%; OECD Pillar Two 15%) and regulatory/lobbying costs (~$40M public policy spend 2024) affecting margins and investment siting.

| Metric | Value |

|---|---|

| Tariff rise (2024–25) | +8–12% |

| COGS impact (2025) | $120–180M |

| LATAM/SEA share of sales (2024) | ~28% |

| FX swing (2023) | up to 18% |

| Effective tax rate (2024) | ~18.6% |

| Public policy spend (2024) | ~$40M |

What is included in the product

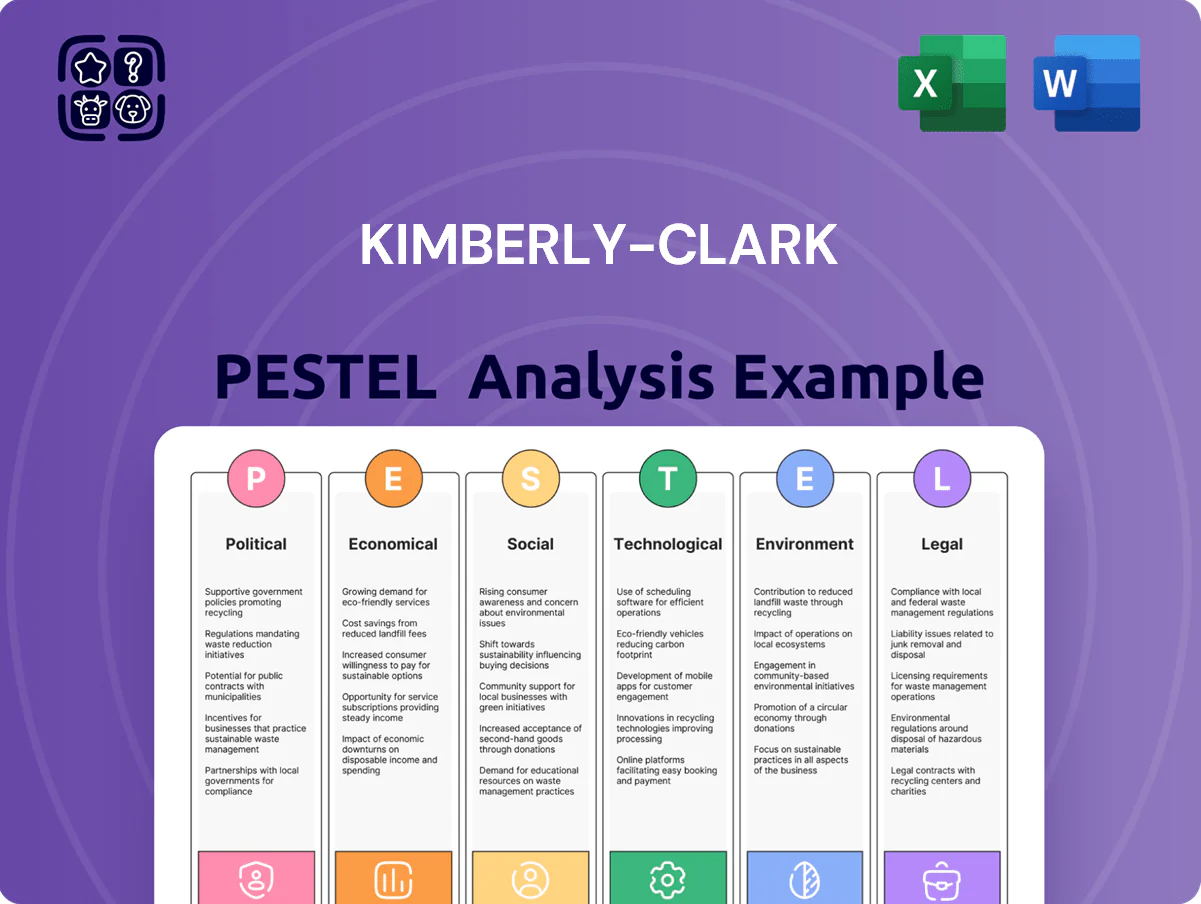

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Kimberly‑Clark, providing data-backed trends, region‑specific examples, and forward-looking insights to help executives, investors, and entrepreneurs identify risks and opportunities for strategic planning and funding decisions.

Condenses Kimberly‑Clark's PESTLE into a clear, shareable snapshot for meetings or decks, visually segmented by factor to speed risk assessment and strategic alignment across teams.

Economic factors

Commodity Price Volatility and Input Costs

At the end of 2025 wood pulp, petroleum-based resins and energy costs remained volatile, with pulp up ~18% year-over-year and benchmark Brent-linked resin prices swinging ±12% in 2025, pressuring Kimberly-Clark’s gross margin (Q4 2025 adjusted gross margin down ~140 bps YoY).

The company responded with targeted price increases—around 3–5% in key markets—and $200–300 million in annualized cost savings programs announced in 2024–25 to protect margins.

Investors track these commodity moves closely since input cost variability explains a significant portion of EBITDA volatility; a 10% pulp price shock historically shifted Kimberly-Clark EBITDA by roughly 3–4%.

Global Currency Exchange Rate Risks

With roughly 60% of Kimberly-Clark’s 2025 revenue derived outside the United States, fluctuations in the US dollar materially affect reported sales and EPS; a 10% dollar appreciation cut international-translated revenue by about 6 percentage points in prior years.

Currency headwinds reduced FY2024 organic sales growth by an estimated 2.5%, complicating quarterly forecasting and dividend planning.

Kimberly-Clark uses layered hedging—forward contracts and natural hedges—to cover a portion of exposure, but persistent macro volatility in 2024–2025 keeps translation risk a core financial concern.

Consumer Spending Power and Inflationary Trends

Inflationary pressures—US CPI up 3.4% year-over-year as of Dec 2025 and global food/energy costs elevated—squeeze household budgets, prompting shifts from premium Huggies/Kleenex to private labels; Kimberly-Clark counters with value-driven innovation and tiered pricing, highlighted by 2024 cost-savings and product down-trading strategies that helped stabilize North American volumes (-0.5% in 2024 vs prior declines). Understanding post-inflation demand elasticity is critical to sustain volume growth in mature markets.

Interest Rate Environment and Cost of Capital

The higher-for-longer global interest rate backdrop in late 2025 raises Kimberly-Clark’s weighted average cost of capital, increasing annual interest expense on its roughly $6.5 billion debt stock and elevating refinancing costs for maturing bonds into 2026–2027.

Elevated rates constrain large M&A and capex flexibility, though Kimberly-Clark’s investment-grade ratings and disciplined debt management help preserve access to capital markets and keep leverage targets intact.

- Debt stock ≈ $6.5B

- Refinancing pressure into 2026–27

- Investment-grade ratings sustain market access

Economic Growth in Developing Nations

Economic expansion in developing regions is shifting consumers from traditional hygiene to modern personal-care products, supporting Kimberly-Clark’s long-term growth; emerging markets contributed about 38% of company net sales in FY2024 (~$5.1B of $13.4B total) showing scale potential.

Rising disposable incomes and a growing middle class—World Bank reports middle-income population in Asia rose to ~2.1B by 2023—enable targeted SKUs and premiumization strategies in these markets.

Slower recoveries (IMF projected 2024 GDP growth for low-income countries at 4.1%) can delay penetration and defer revenue gains versus company forecasts.

- Emerging markets ~38% of 2024 sales (~$5.1B)

- Asia middle-income ~2.1B (2023)

- IMF 2024 low-income GDP growth 4.1%—risk to timing

Commodity and FX squeeze margins; debt and rates bite as emerging markets fuel growth

Commodity-driven margin pressure (pulp +18% YoY in 2025) and FX headwinds (60% revenue ex-US; 10% USD strength ≈ -6% reported revenue) compressed margins despite 3–5% price hikes and $200–300M cost saves; higher rates raise interest expense on ~$6.5B debt while emerging markets (38% of 2024 sales ≈ $5.1B) offer growth as middle classes expand.

| Metric | Value |

|---|---|

| Pulp change (2025) | +18% YoY |

| Revenue ex-US | ~60% |

| Debt stock | ~$6.5B |

| Emerging markets share (2024) | 38% (~$5.1B) |

Preview the Actual Deliverable

Kimberly-Clark PESTLE Analysis

The preview shown here is the exact Kimberly‑Clark PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological change are reshaping Kimberly‑Clark’s competitive landscape—our concise PESTLE highlights risks and opportunities you can act on today; purchase the full analysis for a complete, ready-to-use strategic briefing.

Political factors

Global Trade Policy and Tariff Fluctuations

As of late 2025, Kimberly-Clark remains highly sensitive to shifting trade agreements and protectionist measures in markets like China and the EU; tariffs rose on average 8–12% for pulp and specialty polymers in 2024–25, pressuring margins. Increased import duties on wood pulp and polymers raised COGS by an estimated $120–180 million in 2025, forcing supply-chain rerouting. K-C must continuously adapt sourcing to preserve global pricing competitiveness.

Geopolitical Stability in Emerging Markets

Kimberly-Clark’s expansion in Latin America and Southeast Asia exposes it to localized political volatility; in 2024 these regions accounted for about 28% of net sales, heightening governance risk. Political unrest or sudden leadership changes can prompt currency devaluations—LATAM FX swung up to 18% vs USD in 2023—causing supply-chain and operational disruptions that compress margins. Strategic planners therefore emphasize regional diversification and local JVs; in 2024 the company increased local sourcing to 42% in key markets to hedge unpredictability.

Public Health Policy and Government Procurement

Corporate Taxation and International Tax Reform

- OECD/G20 Pillar Two: 15% global minimum tax

- Kimberly-Clark 2024 effective tax rate: ~18.6%

- 1% ETR rise ≈ $19M hit to 2024 adjusted net income

- R&D/manufacturing incentives affect investment location decisions

Regulatory Lobbying and Industry Standards

Kimberly-Clark spends millions on government relations to shape safety and manufacturing standards, reporting $40M in public policy and compliance-related expenses in 2024 and active participation in ASTM and ISO committees to influence product safety norms.

With global moves toward stricter consumer protection—EU’s 2023 Product Safety Regulation and U.S. state-level chemical disclosure laws—Kimberly-Clark maintains proactive legislative engagement to avoid abrupt compliance costs that could affect its 2024 operating margin of 11.2%.

This lobbying ensures corporate interests are represented while aligning with rising political expectations on corporate responsibility and sustainability reporting tied to investor scrutiny and ESG-linked credit terms.

- 2024 public policy spend: ~$40M

- 2024 operating margin: 11.2%

- Active in ASTM/ISO safety committees

- Key risks: EU product safety rules, U.S. chemical disclosure laws

Kimberly‑Clark faces tariff, FX and tax shocks risking $120–180M COGS hit and margin pressure

Political risks for Kimberly-Clark include rising trade tariffs (pulp/polymer duties +8–12% in 2024–25; COGS impact $120–180M in 2025), regional volatility (LATAM/SEA ~28% of sales; FX swings up to 18% in 2023), tax shifts (2024 ETR ~18.6%; OECD Pillar Two 15%) and regulatory/lobbying costs (~$40M public policy spend 2024) affecting margins and investment siting.

| Metric | Value |

|---|---|

| Tariff rise (2024–25) | +8–12% |

| COGS impact (2025) | $120–180M |

| LATAM/SEA share of sales (2024) | ~28% |

| FX swing (2023) | up to 18% |

| Effective tax rate (2024) | ~18.6% |

| Public policy spend (2024) | ~$40M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Kimberly‑Clark, providing data-backed trends, region‑specific examples, and forward-looking insights to help executives, investors, and entrepreneurs identify risks and opportunities for strategic planning and funding decisions.

Condenses Kimberly‑Clark's PESTLE into a clear, shareable snapshot for meetings or decks, visually segmented by factor to speed risk assessment and strategic alignment across teams.

Economic factors

Commodity Price Volatility and Input Costs

At the end of 2025 wood pulp, petroleum-based resins and energy costs remained volatile, with pulp up ~18% year-over-year and benchmark Brent-linked resin prices swinging ±12% in 2025, pressuring Kimberly-Clark’s gross margin (Q4 2025 adjusted gross margin down ~140 bps YoY).

The company responded with targeted price increases—around 3–5% in key markets—and $200–300 million in annualized cost savings programs announced in 2024–25 to protect margins.

Investors track these commodity moves closely since input cost variability explains a significant portion of EBITDA volatility; a 10% pulp price shock historically shifted Kimberly-Clark EBITDA by roughly 3–4%.

Global Currency Exchange Rate Risks

With roughly 60% of Kimberly-Clark’s 2025 revenue derived outside the United States, fluctuations in the US dollar materially affect reported sales and EPS; a 10% dollar appreciation cut international-translated revenue by about 6 percentage points in prior years.

Currency headwinds reduced FY2024 organic sales growth by an estimated 2.5%, complicating quarterly forecasting and dividend planning.

Kimberly-Clark uses layered hedging—forward contracts and natural hedges—to cover a portion of exposure, but persistent macro volatility in 2024–2025 keeps translation risk a core financial concern.

Consumer Spending Power and Inflationary Trends

Inflationary pressures—US CPI up 3.4% year-over-year as of Dec 2025 and global food/energy costs elevated—squeeze household budgets, prompting shifts from premium Huggies/Kleenex to private labels; Kimberly-Clark counters with value-driven innovation and tiered pricing, highlighted by 2024 cost-savings and product down-trading strategies that helped stabilize North American volumes (-0.5% in 2024 vs prior declines). Understanding post-inflation demand elasticity is critical to sustain volume growth in mature markets.

Interest Rate Environment and Cost of Capital

The higher-for-longer global interest rate backdrop in late 2025 raises Kimberly-Clark’s weighted average cost of capital, increasing annual interest expense on its roughly $6.5 billion debt stock and elevating refinancing costs for maturing bonds into 2026–2027.

Elevated rates constrain large M&A and capex flexibility, though Kimberly-Clark’s investment-grade ratings and disciplined debt management help preserve access to capital markets and keep leverage targets intact.

- Debt stock ≈ $6.5B

- Refinancing pressure into 2026–27

- Investment-grade ratings sustain market access

Economic Growth in Developing Nations

Economic expansion in developing regions is shifting consumers from traditional hygiene to modern personal-care products, supporting Kimberly-Clark’s long-term growth; emerging markets contributed about 38% of company net sales in FY2024 (~$5.1B of $13.4B total) showing scale potential.

Rising disposable incomes and a growing middle class—World Bank reports middle-income population in Asia rose to ~2.1B by 2023—enable targeted SKUs and premiumization strategies in these markets.

Slower recoveries (IMF projected 2024 GDP growth for low-income countries at 4.1%) can delay penetration and defer revenue gains versus company forecasts.

- Emerging markets ~38% of 2024 sales (~$5.1B)

- Asia middle-income ~2.1B (2023)

- IMF 2024 low-income GDP growth 4.1%—risk to timing

Commodity and FX squeeze margins; debt and rates bite as emerging markets fuel growth

Commodity-driven margin pressure (pulp +18% YoY in 2025) and FX headwinds (60% revenue ex-US; 10% USD strength ≈ -6% reported revenue) compressed margins despite 3–5% price hikes and $200–300M cost saves; higher rates raise interest expense on ~$6.5B debt while emerging markets (38% of 2024 sales ≈ $5.1B) offer growth as middle classes expand.

| Metric | Value |

|---|---|

| Pulp change (2025) | +18% YoY |

| Revenue ex-US | ~60% |

| Debt stock | ~$6.5B |

| Emerging markets share (2024) | 38% (~$5.1B) |

Preview the Actual Deliverable

Kimberly-Clark PESTLE Analysis

The preview shown here is the exact Kimberly‑Clark PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.