Kinepolis Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

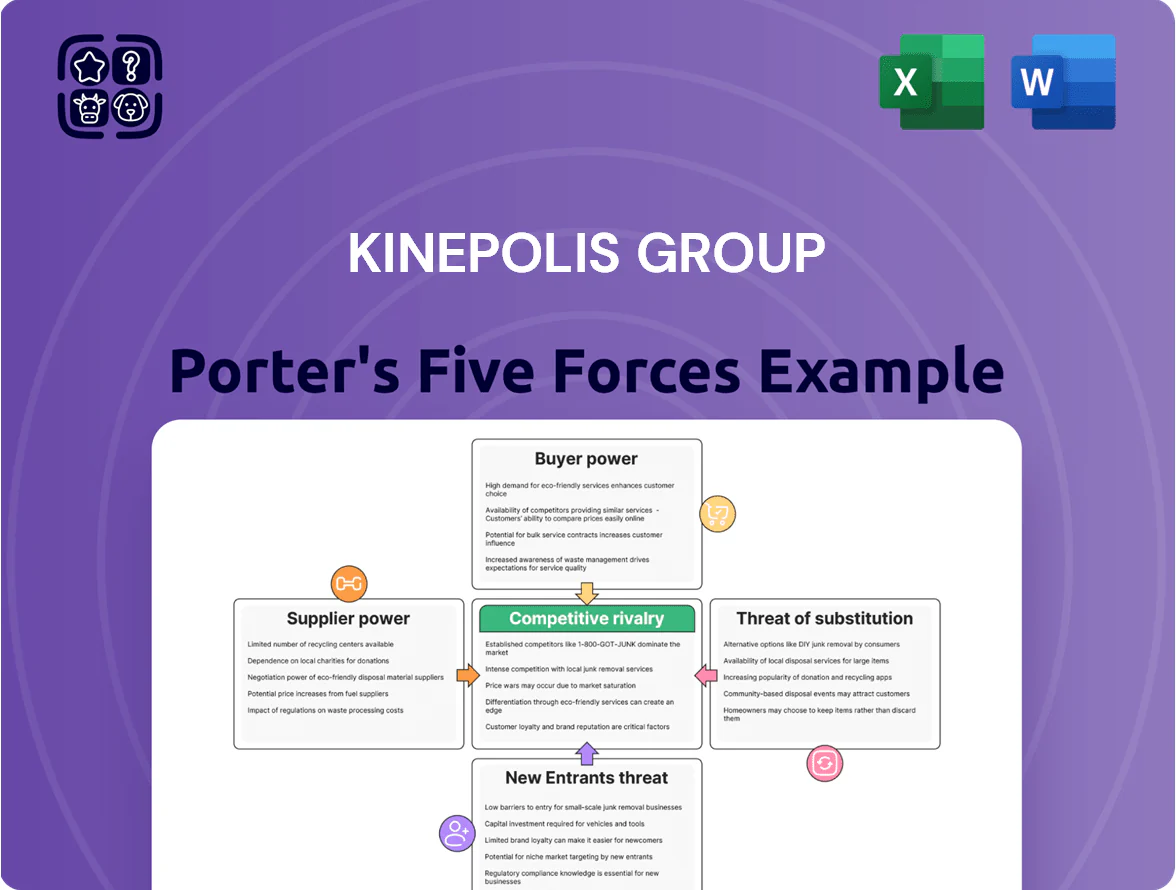

Kinepolis faces moderate buyer power, solid supplier ties, and intense rivalry from streaming and boutique cinemas, while high entry costs and unique real-estate scale limit new entrants—this snapshot highlights key pressures and tactical levers for management.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kinepolis Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Film Studios

Major Hollywood studios—Disney, Warner Bros. Discovery, Universal (NBCUniversal)—control blockbuster supply, and by end-2025 they still set licensing terms and revenue splits, often claiming 50–70% of opening-week ticket sales for wide releases; Kinepolis depends on these few suppliers for marquee titles that draw core audiences, leaving it exposed to studio scheduling, premium pricing, and windowing strategies that can swing quarterly box-office revenue by tens of millions of euros.

Exclusive Technological Partnerships

Kinepolis depends on specialist vendors for IMAX, 4DX and ScreenX systems; these vendors hold moderate supplier power since switching costs and integration time are high—typical retrofit costs can exceed €1–3m per auditorium and integration takes 6–12 months.

In 2024 Kinepolis reported premium-format revenue representing about 18% of box office income, so sustaining vendor ties is essential to preserve its €2–5 average ticket premium and justify luxury pricing.

Real Estate and Property Developers

Kinepolis owns about 60% of its estate portfolio (2024), which reduces supplier power for existing sites, but third-party developers remain critical for greenfield growth and urban infill projects.

In prime European and North American markets vacancy rates under 5% (2024) make large venues scarce, giving landlords leverage in lease terms and CAPEX pass-throughs.

Still, Kinepolis’s role as an anchor tenant—operating 100+ megaplexes across key cities—lets it secure lower rents and tenant improvement credits versus smaller chains.

Food and Beverage Vendor Consolidation

The cinema concession supply chain is concentrated: Coca-Cola and PepsiCo account for roughly 60–70% of global soft‑drink shelf share, supplying high‑margin items that drive Kinepolis Group’s F&B profitability (2024 sales mix: concessions ~30% of box‑office adj. revenue for European chains).

Strong brand loyalty limits switching to local generics without lowering satisfaction, so suppliers push pricing, minimum purchase terms, and co‑funded promotions, pressuring margins and promo budgets.

- Major suppliers: Coca‑Cola, PepsiCo — ~60–70% category share

- Concessions: ~30% of adjusted revenue for chains (2024)

- Supplier levers: pricing, promo co‑funding, purchase minima

Rising Energy and Utility Costs

Energy providers influence Kinepolis by driving utility bills, a major cost for 60+ screen megaplexes; European commercial electricity prices averaged ~€0.25/kWh in 2024, up ~15% vs 2022, raising operating leverage.

Post-2023 volatility keeps suppliers' bargaining power high since few large-scale alternatives exist; Kinepolis must hedge via long-term contracts and capex: in 2024 it reported ~€30m in energy-related capex and efficiency projects.

- Commercial electricity ~€0.25/kWh (2024)

- Prices +15% vs 2022

- Few large-scale supplier alternatives

- ~€30m energy capex (Kinepolis 2024)

Suppliers wield strong leverage: studios, concessions, tech and energy drive major cost swings

Suppliers hold moderate‑high power: studios (Disney, WBD, Universal) claim 50–70% opening grosses, risking €10–50m swings; premium tech vendors charge €1–3m/ auditorium; concessions (Coca‑Cola, PepsiCo) hold 60–70% share; energy ~€0.25/kWh (2024) pushed Kinepolis to €30m energy capex.

| Item | Metric (2024/2025) |

|---|---|

| Studio splits | 50–70% opening |

| Premium retrofit | €1–3m/auditorium |

| Concession share | 60–70% |

| Energy price | €0.25/kWh |

| Energy capex | €30m |

What is included in the product

Tailored Porter's Five Forces analysis for Kinepolis Group highlighting competitive rivalry, buyer and supplier bargaining power, entry barriers, and substitute threats, with strategic insights on disruptive forces and market positioning to guide investor and management decisions.

A concise Porter's Five Forces snapshot for Kinepolis—instantly reveals competitive pressure points and relief strategies for fast strategic decisions.

Customers Bargaining Power

Low Switching Costs for Moviegoers

Individual cinema-goers face almost zero financial switching cost—choosing a rival theater or streaming saves only ticket or concession difference—so Kinepolis must constantly upgrade service to keep loyalty; by 2025 the chain emphasizes total experience (wider recliners, premium sound, better F&B) which helped raise average per-visitor spend to about EUR 7.80 in 2024 and sustain group admissions near 30.5 million.

Price Sensitivity in Middle-Market Segments

While Kinepolis targets a premium audience, about 35% of European cinema-goers in 2024 reported ticket-price sensitivity amid 7% average food inflation, so middle-market customers push for lower prices.

Easy online price comparison raises demand for value bundles, loyalty tiers, and family discounts; Kinepolis’ 2023 loyalty program lift of ~8% in visits shows this works.

Kinepolis must match premium experience with competitive pricing—else it risks volume loss to budget chains holding ~20–25% market share in key markets.

Demand for Premium and Immersive Experiences

Modern customers demand 4K laser projection, Dolby Atmos sound, and luxury seating as standard, pushing Kinepolis to reinvest heavily—Kinepolis spent €62m on capex in 2024 to upgrade auditoria and premium offerings.

Influence of Online Reviews and Social Media

Online reviews and social media have amplified customer bargaining power; a viral post about poor cleanliness or sound at a Kinepolis site can cut weekend attendance by 5–12%, based on industry estimates where negative reviews lower visit intent by ~8% (2023–25 studies).

A single weekend of poor service at a flagship location can reduce box office and F&B receipts sharply, translating to hundreds of thousands euros in lost revenue for large multiplexes.

Kinepolis must monitor platforms, respond within 24 hours, and fix issues proactively to protect NPS and weekly admissions.

- Negative reviews can lower visit intent ~8%

- Potential weekend revenue hit 5–12%

- Respond within 24 hours to limit impact

Availability of Information and Booking Flexibility

The widespread transparency of showtimes, seats and prices on aggregators lets customers compare Kinepolis with rivals; 2024 surveys show 68% of EU moviegoers check at least two platforms before booking.

Customers expect mobile booking, instant tickets and easy cancellations; Kinepolis reported 29% of ticket sales via its app in 2024, so gaps cost revenue.

Digital control forces Kinepolis to invest in proprietary apps and CRM to own data and raise repeat visits; estimated app development and CRM scaling could require €15–30m over 3 years for a pan‑European roll‑out.

- 68% compare platforms

- 29% app sales (2024)

- €15–30m estimated digital investment

High customer leverage: 68% compare platforms — Kinepolis needs €15–30m digital push

Customers have high bargaining power: low switching costs, 68% compare platforms (2024), 29% of Kinepolis sales via app, price sensitivity ~35% of EU goers (2024), negative reviews cut visit intent ~8% and weekends revenue 5–12%; Kinepolis spent €62m capex (2024) and may need €15–30m digital spend to retain premium demand.

| Metric | Value |

|---|---|

| Platform comparison | 68% |

| App sales (Kinepolis) | 29% |

| Price-sensitive customers | 35% |

| Negative review impact | ~8% visit intent |

| 2024 capex | €62m |

| Estimated digital spend | €15–30m |

Preview the Actual Deliverable

Kinepolis Group Porter's Five Forces Analysis

This preview shows the exact Kinepolis Group Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase; no samples, no placeholders. The document covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and evidence-based conclusions. What you see is the final deliverable, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kinepolis faces moderate buyer power, solid supplier ties, and intense rivalry from streaming and boutique cinemas, while high entry costs and unique real-estate scale limit new entrants—this snapshot highlights key pressures and tactical levers for management.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kinepolis Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Film Studios

Major Hollywood studios—Disney, Warner Bros. Discovery, Universal (NBCUniversal)—control blockbuster supply, and by end-2025 they still set licensing terms and revenue splits, often claiming 50–70% of opening-week ticket sales for wide releases; Kinepolis depends on these few suppliers for marquee titles that draw core audiences, leaving it exposed to studio scheduling, premium pricing, and windowing strategies that can swing quarterly box-office revenue by tens of millions of euros.

Exclusive Technological Partnerships

Kinepolis depends on specialist vendors for IMAX, 4DX and ScreenX systems; these vendors hold moderate supplier power since switching costs and integration time are high—typical retrofit costs can exceed €1–3m per auditorium and integration takes 6–12 months.

In 2024 Kinepolis reported premium-format revenue representing about 18% of box office income, so sustaining vendor ties is essential to preserve its €2–5 average ticket premium and justify luxury pricing.

Real Estate and Property Developers

Kinepolis owns about 60% of its estate portfolio (2024), which reduces supplier power for existing sites, but third-party developers remain critical for greenfield growth and urban infill projects.

In prime European and North American markets vacancy rates under 5% (2024) make large venues scarce, giving landlords leverage in lease terms and CAPEX pass-throughs.

Still, Kinepolis’s role as an anchor tenant—operating 100+ megaplexes across key cities—lets it secure lower rents and tenant improvement credits versus smaller chains.

Food and Beverage Vendor Consolidation

The cinema concession supply chain is concentrated: Coca-Cola and PepsiCo account for roughly 60–70% of global soft‑drink shelf share, supplying high‑margin items that drive Kinepolis Group’s F&B profitability (2024 sales mix: concessions ~30% of box‑office adj. revenue for European chains).

Strong brand loyalty limits switching to local generics without lowering satisfaction, so suppliers push pricing, minimum purchase terms, and co‑funded promotions, pressuring margins and promo budgets.

- Major suppliers: Coca‑Cola, PepsiCo — ~60–70% category share

- Concessions: ~30% of adjusted revenue for chains (2024)

- Supplier levers: pricing, promo co‑funding, purchase minima

Rising Energy and Utility Costs

Energy providers influence Kinepolis by driving utility bills, a major cost for 60+ screen megaplexes; European commercial electricity prices averaged ~€0.25/kWh in 2024, up ~15% vs 2022, raising operating leverage.

Post-2023 volatility keeps suppliers' bargaining power high since few large-scale alternatives exist; Kinepolis must hedge via long-term contracts and capex: in 2024 it reported ~€30m in energy-related capex and efficiency projects.

- Commercial electricity ~€0.25/kWh (2024)

- Prices +15% vs 2022

- Few large-scale supplier alternatives

- ~€30m energy capex (Kinepolis 2024)

Suppliers wield strong leverage: studios, concessions, tech and energy drive major cost swings

Suppliers hold moderate‑high power: studios (Disney, WBD, Universal) claim 50–70% opening grosses, risking €10–50m swings; premium tech vendors charge €1–3m/ auditorium; concessions (Coca‑Cola, PepsiCo) hold 60–70% share; energy ~€0.25/kWh (2024) pushed Kinepolis to €30m energy capex.

| Item | Metric (2024/2025) |

|---|---|

| Studio splits | 50–70% opening |

| Premium retrofit | €1–3m/auditorium |

| Concession share | 60–70% |

| Energy price | €0.25/kWh |

| Energy capex | €30m |

What is included in the product

Tailored Porter's Five Forces analysis for Kinepolis Group highlighting competitive rivalry, buyer and supplier bargaining power, entry barriers, and substitute threats, with strategic insights on disruptive forces and market positioning to guide investor and management decisions.

A concise Porter's Five Forces snapshot for Kinepolis—instantly reveals competitive pressure points and relief strategies for fast strategic decisions.

Customers Bargaining Power

Low Switching Costs for Moviegoers

Individual cinema-goers face almost zero financial switching cost—choosing a rival theater or streaming saves only ticket or concession difference—so Kinepolis must constantly upgrade service to keep loyalty; by 2025 the chain emphasizes total experience (wider recliners, premium sound, better F&B) which helped raise average per-visitor spend to about EUR 7.80 in 2024 and sustain group admissions near 30.5 million.

Price Sensitivity in Middle-Market Segments

While Kinepolis targets a premium audience, about 35% of European cinema-goers in 2024 reported ticket-price sensitivity amid 7% average food inflation, so middle-market customers push for lower prices.

Easy online price comparison raises demand for value bundles, loyalty tiers, and family discounts; Kinepolis’ 2023 loyalty program lift of ~8% in visits shows this works.

Kinepolis must match premium experience with competitive pricing—else it risks volume loss to budget chains holding ~20–25% market share in key markets.

Demand for Premium and Immersive Experiences

Modern customers demand 4K laser projection, Dolby Atmos sound, and luxury seating as standard, pushing Kinepolis to reinvest heavily—Kinepolis spent €62m on capex in 2024 to upgrade auditoria and premium offerings.

Influence of Online Reviews and Social Media

Online reviews and social media have amplified customer bargaining power; a viral post about poor cleanliness or sound at a Kinepolis site can cut weekend attendance by 5–12%, based on industry estimates where negative reviews lower visit intent by ~8% (2023–25 studies).

A single weekend of poor service at a flagship location can reduce box office and F&B receipts sharply, translating to hundreds of thousands euros in lost revenue for large multiplexes.

Kinepolis must monitor platforms, respond within 24 hours, and fix issues proactively to protect NPS and weekly admissions.

- Negative reviews can lower visit intent ~8%

- Potential weekend revenue hit 5–12%

- Respond within 24 hours to limit impact

Availability of Information and Booking Flexibility

The widespread transparency of showtimes, seats and prices on aggregators lets customers compare Kinepolis with rivals; 2024 surveys show 68% of EU moviegoers check at least two platforms before booking.

Customers expect mobile booking, instant tickets and easy cancellations; Kinepolis reported 29% of ticket sales via its app in 2024, so gaps cost revenue.

Digital control forces Kinepolis to invest in proprietary apps and CRM to own data and raise repeat visits; estimated app development and CRM scaling could require €15–30m over 3 years for a pan‑European roll‑out.

- 68% compare platforms

- 29% app sales (2024)

- €15–30m estimated digital investment

High customer leverage: 68% compare platforms — Kinepolis needs €15–30m digital push

Customers have high bargaining power: low switching costs, 68% compare platforms (2024), 29% of Kinepolis sales via app, price sensitivity ~35% of EU goers (2024), negative reviews cut visit intent ~8% and weekends revenue 5–12%; Kinepolis spent €62m capex (2024) and may need €15–30m digital spend to retain premium demand.

| Metric | Value |

|---|---|

| Platform comparison | 68% |

| App sales (Kinepolis) | 29% |

| Price-sensitive customers | 35% |

| Negative review impact | ~8% visit intent |

| 2024 capex | €62m |

| Estimated digital spend | €15–30m |

Preview the Actual Deliverable

Kinepolis Group Porter's Five Forces Analysis

This preview shows the exact Kinepolis Group Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase; no samples, no placeholders. The document covers supplier and buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and evidence-based conclusions. What you see is the final deliverable, available instantly upon payment.