Kingboard Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

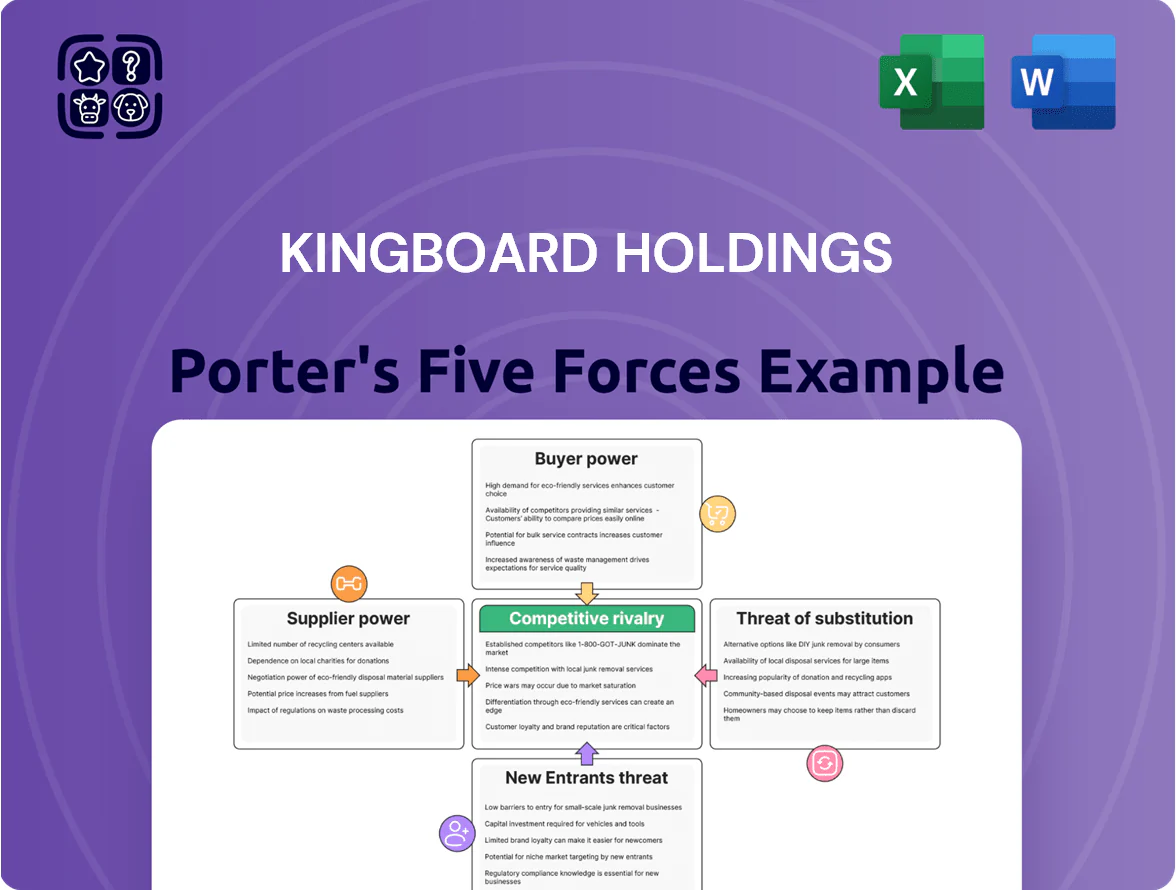

Kingboard Holdings faces moderate supplier and buyer power, intense rivalry among global chemical and laminate producers, and evolving threats from substitutes and new entrants driven by technological shifts—creating a complex strategic landscape that demands careful analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kingboard Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

Kingboard reduces supplier power by producing copper foil, glass fabric and bleached kraft paper in‑house, supplying roughly 60–70% of its PCB input needs as of FY2024, cutting external dependence. This vertical integration delivered unit cost savings estimated at 8–12% versus peers in 2024 procurement analyses. Controlling upstream output let Kingboard maintain volumes during the 2021–22 copper squeeze and limited price pass‑through in 2023–24, stabilizing gross margins.

Commodity Price Sensitivity

Despite vertical integration, Kingboard Holdings remains exposed to global crude oil and copper prices; crude rose ~15% in 2024 and LME copper averaged $8,600/ton in 2024, so feedstock and metal costs track international markets, not single suppliers.

These commodities are vital for its chemical and copper foil divisions, so a 10% move in copper prices can shift COGS materially—here’s the quick math: a $860/ton rise on 100,000 tons raises input cost by $86m.

Energy Dependency and Utility Providers

Large-scale chemical and laminate production at Kingboard Holdings consumes substantial electricity and fuel—industry estimates show electrochemical and lamination plants use 1.2–2.5 MWh per tonne and up to 10 GJ fuel per tonne—making utility suppliers strategic bottlenecks. Localized utility monopolies in China, Southeast Asia, and Brazil give providers pricing leverage; a 2024 China industrial power tariff rise of ~8% raised input costs across peers. Kingboard must secure long‑term contracts, on‑site generation, and hedges to protect margins and continuity.

Specialized Manufacturing Equipment

Specialized equipment for HDI PCBs and advanced chemicals comes from a few global vendors—ASMPT, Tokyo Electron, and Applied Materials—keeping supplier concentration high; in 2024, top 5 vendors held ~60% market share in PCB assembly tools.

Proprietary tech, exclusive spare parts, and multi-year service contracts raise total cost of ownership and create high switching costs, often tying capital expenditure cycles to supplier timelines.

This gives suppliers pricing and timing leverage over Kingboard Holdings’ CAPEX, where single-tool units run $1–5 million and downtime costs reach tens of thousands per day.

- High supplier concentration (~60% market share top vendors)

- Single-tool cost $1–5M; downtime costs ~$10k–$50k/day

- Proprietary parts + 3–5yr service contracts raise switching cost

Chemical Feedstock Access

- Suppliers control 60–80% supply

- Benzene spot ±15% → margins −120–180 bps

- 2023 chemical EBITDA margin ~11%

- Multi-year contracts reduce spot risk

Kingboard's vertical integration trims costs 8–12% but COGS still tied to oil & copper

Kingboard lowers supplier power via vertical integration (60–70% self‑supply FY2024), cutting input costs ~8–12% vs peers and buffering 2021–24 commodity shocks, but remains exposed to global oil/copper; LME copper avg $8,600/ton (2024) and crude +15% (2024) still move COGS materially; utilities and specialist equipment vendors (top5 ~60% share) create switching costs and CAPEX timing leverage.

| Metric | 2024/2023 |

|---|---|

| Self‑supply PCB inputs | 60–70% (FY2024) |

| Copper LME | $8,600/ton (2024 avg) |

| Crude oil change | +15% (2024) |

| Vertical integration saving | 8–12% vs peers (2024) |

| Chemical EBITDA margin | ~11% (2023) |

| Top OEM share (tools) | ~60% (top5, 2024) |

What is included in the product

Tailored exclusively for Kingboard Holdings, this Porter’s Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping the company’s pricing power and profitability.

Concise Porter’s Five Forces for Kingboard Holdings—instantly see supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of Electronics Giants

Low Switching Costs for Standardized Products

In generic laminates and basic multi-layer PCB markets, products are commoditized so customers switch suppliers with little friction; Kingboard faced this in 2024 when its PCB segment saw margin pressure as ASPs fell ~6% YoY in Asia.

Demand for Specialized High-End Solutions

Customers in 5G, AI, and automotive sectors demand laminates with tight thermal and dielectric specs, driving Kingboard to co-develop solutions; these end-markets represented about 38% of global laminate demand in 2024, raising customer influence. Sophisticated buyers can model BOM and capex, so they push for cost-plus or TCO pricing, limiting Kingboard’s ability to charge >5–8% innovation premiums seen in commodity lines. This technical transparency fosters collaboration but strengthens buyer bargaining power and compresses margin upside.

Impact of Industry Cyclicality

The electronics and property segments of Kingboard Holdings (HK: 148) are cyclical; global electronics demand fell ~8% in 2023 and China property investment dropped 10% year‑over‑year, directly reducing buyers’ purchase volumes and giving customers leverage.

In downturns buyers delay orders and seek 5–15% discounts to cut inventory costs, so customer bargaining power rises and compresses margins.

Kingboard needs flexible production and inventory: in 2024 it reduced operating rates by ~12% and increased short‑cycle capacity to respond quickly.

- Electronics demand volatility: −8% in 2023

- China property investment: −10% YoY (2023)

- Typical buyer discount pressure: 5–15%

- Kingboard adjusted operating rates: −12% (2024)

Information Transparency and Global Sourcing

The rise of digital supply chains gives buyers real-time visibility into global copper and resin prices (copper down 4% YTD to $8,400/t as of Dec 2025; epoxy resin spot up 6% in 2025), and OEMs leverage competitor capacity data to push margins lower.

Large procurement teams now extract live quotes and lead times, routinely pitting Kingboard Holdings’ laminates and chemicals units against Asian rivals to secure 2–5% better pricing and shorter terms.

This transparency shifts bargaining power to informed buyers, raising pressure on Kingboard’s ASPs (average selling prices) and requiring tighter cost controls and faster order fulfillment.

- Real-time price feeds (copper, resin)

- Buyers gain 2–5% price concessions

- Shorter lead times demanded

- ASPs face downward pressure

OEMs Dominate PCB Market: ASPs Down, Advanced Demand Caps Innovation Premiums

Large OEMs (Apple, Samsung, Tesla) drove ~40–55% of PCB/laminate volume in 2024, forcing single-digit margin cuts and >98% OTIF; commodity PCB ASPs fell ~6% YoY in Asia (2024). Advanced 5G/AI/auto demand = ~38% of laminate market (2024), capping innovation premiums at ~5–8%. Downturns see 5–15% buyer discounts; Kingboard cut operating rates ~12% in 2024 to stay agile.

| Metric | 2024 |

|---|---|

| Top OEM share | 40–55% |

| Commodity ASP change | -6% YoY (Asia) |

| Advanced market share | 38% |

| Buyer discount pressure | 5–15% |

| Operating rate change | -12% |

What You See Is What You Get

Kingboard Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Kingboard Holdings you’ll receive immediately after purchase—no mockups or placeholders, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Kingboard Holdings faces moderate supplier and buyer power, intense rivalry among global chemical and laminate producers, and evolving threats from substitutes and new entrants driven by technological shifts—creating a complex strategic landscape that demands careful analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kingboard Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

Kingboard reduces supplier power by producing copper foil, glass fabric and bleached kraft paper in‑house, supplying roughly 60–70% of its PCB input needs as of FY2024, cutting external dependence. This vertical integration delivered unit cost savings estimated at 8–12% versus peers in 2024 procurement analyses. Controlling upstream output let Kingboard maintain volumes during the 2021–22 copper squeeze and limited price pass‑through in 2023–24, stabilizing gross margins.

Commodity Price Sensitivity

Despite vertical integration, Kingboard Holdings remains exposed to global crude oil and copper prices; crude rose ~15% in 2024 and LME copper averaged $8,600/ton in 2024, so feedstock and metal costs track international markets, not single suppliers.

These commodities are vital for its chemical and copper foil divisions, so a 10% move in copper prices can shift COGS materially—here’s the quick math: a $860/ton rise on 100,000 tons raises input cost by $86m.

Energy Dependency and Utility Providers

Large-scale chemical and laminate production at Kingboard Holdings consumes substantial electricity and fuel—industry estimates show electrochemical and lamination plants use 1.2–2.5 MWh per tonne and up to 10 GJ fuel per tonne—making utility suppliers strategic bottlenecks. Localized utility monopolies in China, Southeast Asia, and Brazil give providers pricing leverage; a 2024 China industrial power tariff rise of ~8% raised input costs across peers. Kingboard must secure long‑term contracts, on‑site generation, and hedges to protect margins and continuity.

Specialized Manufacturing Equipment

Specialized equipment for HDI PCBs and advanced chemicals comes from a few global vendors—ASMPT, Tokyo Electron, and Applied Materials—keeping supplier concentration high; in 2024, top 5 vendors held ~60% market share in PCB assembly tools.

Proprietary tech, exclusive spare parts, and multi-year service contracts raise total cost of ownership and create high switching costs, often tying capital expenditure cycles to supplier timelines.

This gives suppliers pricing and timing leverage over Kingboard Holdings’ CAPEX, where single-tool units run $1–5 million and downtime costs reach tens of thousands per day.

- High supplier concentration (~60% market share top vendors)

- Single-tool cost $1–5M; downtime costs ~$10k–$50k/day

- Proprietary parts + 3–5yr service contracts raise switching cost

Chemical Feedstock Access

- Suppliers control 60–80% supply

- Benzene spot ±15% → margins −120–180 bps

- 2023 chemical EBITDA margin ~11%

- Multi-year contracts reduce spot risk

Kingboard's vertical integration trims costs 8–12% but COGS still tied to oil & copper

Kingboard lowers supplier power via vertical integration (60–70% self‑supply FY2024), cutting input costs ~8–12% vs peers and buffering 2021–24 commodity shocks, but remains exposed to global oil/copper; LME copper avg $8,600/ton (2024) and crude +15% (2024) still move COGS materially; utilities and specialist equipment vendors (top5 ~60% share) create switching costs and CAPEX timing leverage.

| Metric | 2024/2023 |

|---|---|

| Self‑supply PCB inputs | 60–70% (FY2024) |

| Copper LME | $8,600/ton (2024 avg) |

| Crude oil change | +15% (2024) |

| Vertical integration saving | 8–12% vs peers (2024) |

| Chemical EBITDA margin | ~11% (2023) |

| Top OEM share (tools) | ~60% (top5, 2024) |

What is included in the product

Tailored exclusively for Kingboard Holdings, this Porter’s Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping the company’s pricing power and profitability.

Concise Porter’s Five Forces for Kingboard Holdings—instantly see supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of Electronics Giants

Low Switching Costs for Standardized Products

In generic laminates and basic multi-layer PCB markets, products are commoditized so customers switch suppliers with little friction; Kingboard faced this in 2024 when its PCB segment saw margin pressure as ASPs fell ~6% YoY in Asia.

Demand for Specialized High-End Solutions

Customers in 5G, AI, and automotive sectors demand laminates with tight thermal and dielectric specs, driving Kingboard to co-develop solutions; these end-markets represented about 38% of global laminate demand in 2024, raising customer influence. Sophisticated buyers can model BOM and capex, so they push for cost-plus or TCO pricing, limiting Kingboard’s ability to charge >5–8% innovation premiums seen in commodity lines. This technical transparency fosters collaboration but strengthens buyer bargaining power and compresses margin upside.

Impact of Industry Cyclicality

The electronics and property segments of Kingboard Holdings (HK: 148) are cyclical; global electronics demand fell ~8% in 2023 and China property investment dropped 10% year‑over‑year, directly reducing buyers’ purchase volumes and giving customers leverage.

In downturns buyers delay orders and seek 5–15% discounts to cut inventory costs, so customer bargaining power rises and compresses margins.

Kingboard needs flexible production and inventory: in 2024 it reduced operating rates by ~12% and increased short‑cycle capacity to respond quickly.

- Electronics demand volatility: −8% in 2023

- China property investment: −10% YoY (2023)

- Typical buyer discount pressure: 5–15%

- Kingboard adjusted operating rates: −12% (2024)

Information Transparency and Global Sourcing

The rise of digital supply chains gives buyers real-time visibility into global copper and resin prices (copper down 4% YTD to $8,400/t as of Dec 2025; epoxy resin spot up 6% in 2025), and OEMs leverage competitor capacity data to push margins lower.

Large procurement teams now extract live quotes and lead times, routinely pitting Kingboard Holdings’ laminates and chemicals units against Asian rivals to secure 2–5% better pricing and shorter terms.

This transparency shifts bargaining power to informed buyers, raising pressure on Kingboard’s ASPs (average selling prices) and requiring tighter cost controls and faster order fulfillment.

- Real-time price feeds (copper, resin)

- Buyers gain 2–5% price concessions

- Shorter lead times demanded

- ASPs face downward pressure

OEMs Dominate PCB Market: ASPs Down, Advanced Demand Caps Innovation Premiums

Large OEMs (Apple, Samsung, Tesla) drove ~40–55% of PCB/laminate volume in 2024, forcing single-digit margin cuts and >98% OTIF; commodity PCB ASPs fell ~6% YoY in Asia (2024). Advanced 5G/AI/auto demand = ~38% of laminate market (2024), capping innovation premiums at ~5–8%. Downturns see 5–15% buyer discounts; Kingboard cut operating rates ~12% in 2024 to stay agile.

| Metric | 2024 |

|---|---|

| Top OEM share | 40–55% |

| Commodity ASP change | -6% YoY (Asia) |

| Advanced market share | 38% |

| Buyer discount pressure | 5–15% |

| Operating rate change | -12% |

What You See Is What You Get

Kingboard Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Kingboard Holdings you’ll receive immediately after purchase—no mockups or placeholders, fully formatted and ready for use.