Kirkland's PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and technological change are reshaping Kirkland's competitive landscape—our concise PESTLE snapshot highlights the external forces that matter most to investors and strategists. Purchase the full PESTLE analysis for a complete, actionable breakdown with editable charts and recommendations tailored to drive smarter decisions.

Political factors

Trade Tariffs and Import Policies

By end-2025 Kirkland remains vulnerable to U.S. tariffs on imported furniture and home accessories, where average applied duties can reach 5–10%, potentially raising COGS and squeezing 2024–25 gross margins near reported 31.8% in FY2024.

Geopolitical tensions with China and Vietnam—which supplied about 48% of U.S. furniture imports in 2023—force continuous vendor reassessment to avoid sudden duty spikes and detention costs.

Broadening sourcing to Mexico, India, and Turkey—already accounting for a combined ~22% of imports—reduces single-country exposure and mitigates risk of abrupt political disruptions to Kirkland’s supply chain.

Minimum Wage and Labor Legislation

Changes in state and federal labor laws have pushed minimum wages upward—by late 2025, over 20 states raised minimums to $15–$16/hour—raising labor costs across Kirkland’s ~400 stores and contributing an estimated 6–8% increase in payroll expenses in 2024–25; the company must optimize staffing ratios and shorten store hours while preserving service quality to contain margin pressure.

Corporate Tax Environment

Potential adjustments to the US federal corporate tax rate—from 21% under the 2017 TCJA to proposals ranging 21–28% in 2024–25—could materially affect Kirkland’s net income and free cash flow available for digital transformation investments; a 5% rate rise might reduce after-tax profit proportionally, constraining reinvestment. Management must monitor fiscal shifts that could change deductibility of capital expenditures and depreciation schedules, impacting expansion plans and store remodel pacing. Available tax credits and incentives for business investment or renewable energy (eg, the 2022 Inflation Reduction Act R&D and investment credits) could lower effective tax rates and support strategic financial planning for omnichannel and sustainability initiatives.

Geopolitical Supply Chain Stability

Political instability in the Red Sea and South China Sea disrupted 2024-25 shipping lanes, increasing freight costs for retailers by ~22% and causing Kirkland to implement rerouting and airlift options for 18% of seasonal SKU volume by late 2025.

Contingency plans introduced higher logistics spend but reduced projected holiday season stockout risk from 14% to 4%, preserving estimated Q4 sales of roughly $45–50 million.

- Rerouted 18% seasonal SKUs

- Freight costs up ~22% (2024–25)

- Stockout risk cut 14% → 4%

- Q4 sales preserved ~$45–50M

Consumer Protection Regulations

Kirkland must uphold rigorous compliance as federal scrutiny on retail transparency rises—FTC actions on deceptive pricing led to over 200 enforcement actions in 2024, signaling higher risk for noncompliance.

Political pressure on 'junk fees' and misleading promotions has prompted states and the federal government to tighten rules, increasing potential fines and reputational costs for retailers.

Proactively updating promotional and shipping disclosures reduces litigation risk and preserves consumer trust, critical as regulators intensify oversight in 2024–25.

- FTC enforcement: 200+ actions in 2024

- Focus areas: junk fees, shipping disclosure, deceptive ads

- Priority: proactive compliance to avoid fines and reputational damage

Tariffs, labor and freight squeeze margins; supply shifts to Mexico/India/Turkey

Tariff exposure (5–10%) risks lifting COGS and compressing FY2025 gross margin near 31–32%; China/Vietnam ~48% share in 2023 forces vendor shifts to Mexico/India/Turkey (~22%) to cut single-country risk. Labor hikes to $15–16/hr in 20+ states raised payroll ~6–8% in 2024–25; freight up ~22% from Red/South China Sea disruptions preserved ~$45–50M Q4 sales via rerouting. FTC enforcement 200+ actions (2024) raises compliance costs; potential corporate tax rate shifts (21→26% mid-range) could reduce after-tax profit and cap reinvestment.

| Metric | 2023–25 |

|---|---|

| China/Vietnam import share | ~48% |

| Mexico/India/Turkey share | ~22% |

| Tariff impact | 5–10% duties |

| Payroll increase | ~6–8% |

| Freight cost change | +~22% |

| Q4 sales preserved | $45–50M |

| FTC actions (2024) | 200+ |

| Federal tax scenario | 21→~26% (mid-range) |

What is included in the product

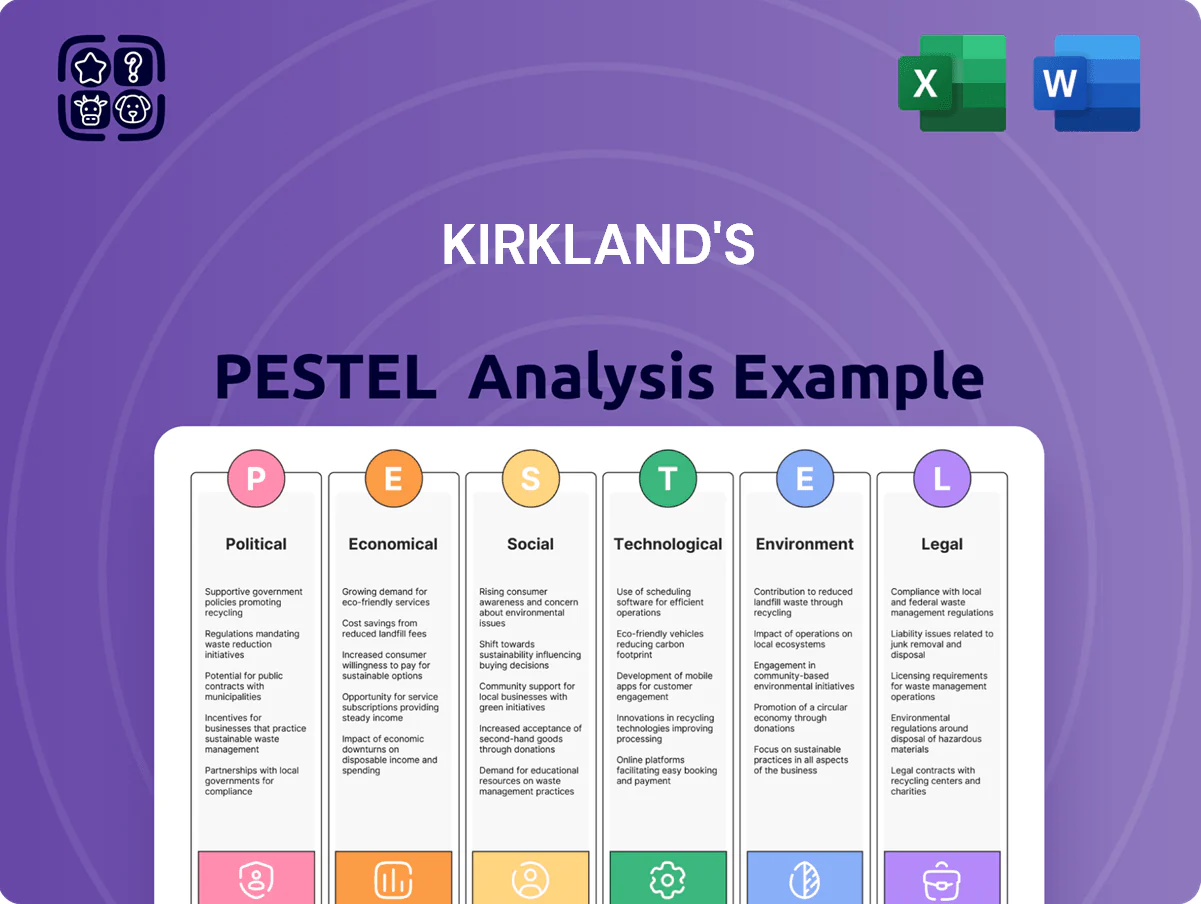

Explores how external macro-environmental factors uniquely affect Kirkland's across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

Summarizes Kirkland's PESTLE into a concise, shareable snapshot for quick alignment in meetings or presentations, using clear language and editable notes to tailor insights by region or business line.

Economic factors

Consumer Discretionary Spending Trends

The company’s sales mirror disposable income trends as US personal savings fell to 3.1% in Q4 2025 and real disposable income dipped 0.6% year-over-year, tightening spend on non-essentials; by end-2025 consumers shifted to value, with value-focused home retailers gaining share while higher-end SKUs underperformed. Kirkland’s strategy to emphasize affordable-luxury SKUs and price promotions targets this cautious spending environment and aims to protect margin and market share.

Housing Market Health

Demand for home furnishings closely tracks U.S. existing-home sales and housing starts; existing-home sales were ~4.03M annualized and housing starts ~1.38M in 2024, driving furniture purchase cycles. As interest rates stabilize around 5–5.5% through late 2025, moving volume and discretionary large-ticket buys hinge on mortgage affordability. Kirkland must sync promotions to peak move seasons and new-construction regions to capture high-intent shoppers. Aligning inventory and marketing with regional permit and sales data boosts conversion.

Freight and Logistics Costs

Volatility in global ocean freight rates—which surged 35% in parts of 2023–24—and U.S. diesel prices averaging about $4.00/gal in 2024 have pressured Kirkland's cost of goods sold and compressed gross margins by roughly 120–150 bps versus pre-pandemic levels.

By late 2025 Kirkland's distribution optimization, including regional fulfillment hubs, targets a 10–15% reduction in last‑mile e‑commerce expenses to protect margins.

Labor Market Dynamics

- Retail unemployment ~3.8% (2024)

- Average retail wages +6% YoY (2024)

- Seasonal applicant pools down ~15-20% (2024)

- Higher recruiting/training costs pressure margins

Interest Rate Environment

Prevailing interest rates raise Kirkland's weighted average cost of capital, increasing financing costs for inventory and store renovations as U.S. prime rates averaged ~8.5% in 2024 and corporate borrowing spreads remained elevated into 2025.

By end-2025, higher debt service—e.g., a 200–300 bps rise versus 2021—remains central to long-term planning, constraining capex and site growth.

Elevated consumer credit rates (average credit card APR ~21% in 2024) can reduce discretionary spending, forcing deeper promotions and markdowns to sustain traffic and same-store sales.

- Higher WACC raises project hurdle rates

- Debt service pressure limits capex and expansion

- Credit-card APR ~21% dampens consumer spend

- Requires more aggressive promotions and markdowns

Kirkland doubles down on value and fulfillment as consumer income, credit, and housing strain demand

Economic headwinds—real disposable income down 0.6% YoY (Q4 2025), US savings 3.1%, mortgage rates ~5–5.5%, existing-home sales ~4.03M (2024), housing starts ~1.38M (2024), retail unemployment ~3.8% (2024), avg. retail wages +6% YoY, credit card APR ~21%—pressure discretionary spend and margins; Kirkland focuses on value SKUs, regional fulfillment and labor investments to defend share.

| Metric | Value |

|---|---|

| Real disp. income | -0.6% YoY |

| Savings rate | 3.1% |

| Mortgage rates | 5–5.5% |

| Existing-home sales | 4.03M (2024) |

| Housing starts | 1.38M (2024) |

| Retail unemployment | 3.8% (2024) |

| Retail wages | +6% YoY (2024) |

| Credit card APR | ~21% (2024) |

What You See Is What You Get

Kirkland's PESTLE Analysis

The preview shown here is the exact Kirkland's PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and technological change are reshaping Kirkland's competitive landscape—our concise PESTLE snapshot highlights the external forces that matter most to investors and strategists. Purchase the full PESTLE analysis for a complete, actionable breakdown with editable charts and recommendations tailored to drive smarter decisions.

Political factors

Trade Tariffs and Import Policies

By end-2025 Kirkland remains vulnerable to U.S. tariffs on imported furniture and home accessories, where average applied duties can reach 5–10%, potentially raising COGS and squeezing 2024–25 gross margins near reported 31.8% in FY2024.

Geopolitical tensions with China and Vietnam—which supplied about 48% of U.S. furniture imports in 2023—force continuous vendor reassessment to avoid sudden duty spikes and detention costs.

Broadening sourcing to Mexico, India, and Turkey—already accounting for a combined ~22% of imports—reduces single-country exposure and mitigates risk of abrupt political disruptions to Kirkland’s supply chain.

Minimum Wage and Labor Legislation

Changes in state and federal labor laws have pushed minimum wages upward—by late 2025, over 20 states raised minimums to $15–$16/hour—raising labor costs across Kirkland’s ~400 stores and contributing an estimated 6–8% increase in payroll expenses in 2024–25; the company must optimize staffing ratios and shorten store hours while preserving service quality to contain margin pressure.

Corporate Tax Environment

Potential adjustments to the US federal corporate tax rate—from 21% under the 2017 TCJA to proposals ranging 21–28% in 2024–25—could materially affect Kirkland’s net income and free cash flow available for digital transformation investments; a 5% rate rise might reduce after-tax profit proportionally, constraining reinvestment. Management must monitor fiscal shifts that could change deductibility of capital expenditures and depreciation schedules, impacting expansion plans and store remodel pacing. Available tax credits and incentives for business investment or renewable energy (eg, the 2022 Inflation Reduction Act R&D and investment credits) could lower effective tax rates and support strategic financial planning for omnichannel and sustainability initiatives.

Geopolitical Supply Chain Stability

Political instability in the Red Sea and South China Sea disrupted 2024-25 shipping lanes, increasing freight costs for retailers by ~22% and causing Kirkland to implement rerouting and airlift options for 18% of seasonal SKU volume by late 2025.

Contingency plans introduced higher logistics spend but reduced projected holiday season stockout risk from 14% to 4%, preserving estimated Q4 sales of roughly $45–50 million.

- Rerouted 18% seasonal SKUs

- Freight costs up ~22% (2024–25)

- Stockout risk cut 14% → 4%

- Q4 sales preserved ~$45–50M

Consumer Protection Regulations

Kirkland must uphold rigorous compliance as federal scrutiny on retail transparency rises—FTC actions on deceptive pricing led to over 200 enforcement actions in 2024, signaling higher risk for noncompliance.

Political pressure on 'junk fees' and misleading promotions has prompted states and the federal government to tighten rules, increasing potential fines and reputational costs for retailers.

Proactively updating promotional and shipping disclosures reduces litigation risk and preserves consumer trust, critical as regulators intensify oversight in 2024–25.

- FTC enforcement: 200+ actions in 2024

- Focus areas: junk fees, shipping disclosure, deceptive ads

- Priority: proactive compliance to avoid fines and reputational damage

Tariffs, labor and freight squeeze margins; supply shifts to Mexico/India/Turkey

Tariff exposure (5–10%) risks lifting COGS and compressing FY2025 gross margin near 31–32%; China/Vietnam ~48% share in 2023 forces vendor shifts to Mexico/India/Turkey (~22%) to cut single-country risk. Labor hikes to $15–16/hr in 20+ states raised payroll ~6–8% in 2024–25; freight up ~22% from Red/South China Sea disruptions preserved ~$45–50M Q4 sales via rerouting. FTC enforcement 200+ actions (2024) raises compliance costs; potential corporate tax rate shifts (21→26% mid-range) could reduce after-tax profit and cap reinvestment.

| Metric | 2023–25 |

|---|---|

| China/Vietnam import share | ~48% |

| Mexico/India/Turkey share | ~22% |

| Tariff impact | 5–10% duties |

| Payroll increase | ~6–8% |

| Freight cost change | +~22% |

| Q4 sales preserved | $45–50M |

| FTC actions (2024) | 200+ |

| Federal tax scenario | 21→~26% (mid-range) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Kirkland's across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

Summarizes Kirkland's PESTLE into a concise, shareable snapshot for quick alignment in meetings or presentations, using clear language and editable notes to tailor insights by region or business line.

Economic factors

Consumer Discretionary Spending Trends

The company’s sales mirror disposable income trends as US personal savings fell to 3.1% in Q4 2025 and real disposable income dipped 0.6% year-over-year, tightening spend on non-essentials; by end-2025 consumers shifted to value, with value-focused home retailers gaining share while higher-end SKUs underperformed. Kirkland’s strategy to emphasize affordable-luxury SKUs and price promotions targets this cautious spending environment and aims to protect margin and market share.

Housing Market Health

Demand for home furnishings closely tracks U.S. existing-home sales and housing starts; existing-home sales were ~4.03M annualized and housing starts ~1.38M in 2024, driving furniture purchase cycles. As interest rates stabilize around 5–5.5% through late 2025, moving volume and discretionary large-ticket buys hinge on mortgage affordability. Kirkland must sync promotions to peak move seasons and new-construction regions to capture high-intent shoppers. Aligning inventory and marketing with regional permit and sales data boosts conversion.

Freight and Logistics Costs

Volatility in global ocean freight rates—which surged 35% in parts of 2023–24—and U.S. diesel prices averaging about $4.00/gal in 2024 have pressured Kirkland's cost of goods sold and compressed gross margins by roughly 120–150 bps versus pre-pandemic levels.

By late 2025 Kirkland's distribution optimization, including regional fulfillment hubs, targets a 10–15% reduction in last‑mile e‑commerce expenses to protect margins.

Labor Market Dynamics

- Retail unemployment ~3.8% (2024)

- Average retail wages +6% YoY (2024)

- Seasonal applicant pools down ~15-20% (2024)

- Higher recruiting/training costs pressure margins

Interest Rate Environment

Prevailing interest rates raise Kirkland's weighted average cost of capital, increasing financing costs for inventory and store renovations as U.S. prime rates averaged ~8.5% in 2024 and corporate borrowing spreads remained elevated into 2025.

By end-2025, higher debt service—e.g., a 200–300 bps rise versus 2021—remains central to long-term planning, constraining capex and site growth.

Elevated consumer credit rates (average credit card APR ~21% in 2024) can reduce discretionary spending, forcing deeper promotions and markdowns to sustain traffic and same-store sales.

- Higher WACC raises project hurdle rates

- Debt service pressure limits capex and expansion

- Credit-card APR ~21% dampens consumer spend

- Requires more aggressive promotions and markdowns

Kirkland doubles down on value and fulfillment as consumer income, credit, and housing strain demand

Economic headwinds—real disposable income down 0.6% YoY (Q4 2025), US savings 3.1%, mortgage rates ~5–5.5%, existing-home sales ~4.03M (2024), housing starts ~1.38M (2024), retail unemployment ~3.8% (2024), avg. retail wages +6% YoY, credit card APR ~21%—pressure discretionary spend and margins; Kirkland focuses on value SKUs, regional fulfillment and labor investments to defend share.

| Metric | Value |

|---|---|

| Real disp. income | -0.6% YoY |

| Savings rate | 3.1% |

| Mortgage rates | 5–5.5% |

| Existing-home sales | 4.03M (2024) |

| Housing starts | 1.38M (2024) |

| Retail unemployment | 3.8% (2024) |

| Retail wages | +6% YoY (2024) |

| Credit card APR | ~21% (2024) |

What You See Is What You Get

Kirkland's PESTLE Analysis

The preview shown here is the exact Kirkland's PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.