Kirkland's SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Kirkland’s strong brand recognition and niche home-decor positioning drive steady traffic, but margin pressures, online competition, and supply-chain volatility pose clear threats; our full SWOT unpacks these dynamics with revenue-impact analysis and strategic recommendations. Purchase the complete SWOT analysis for a professionally formatted Word report and editable Excel tools—ideal for investors, advisors, and strategists seeking actionable, research-backed insights.

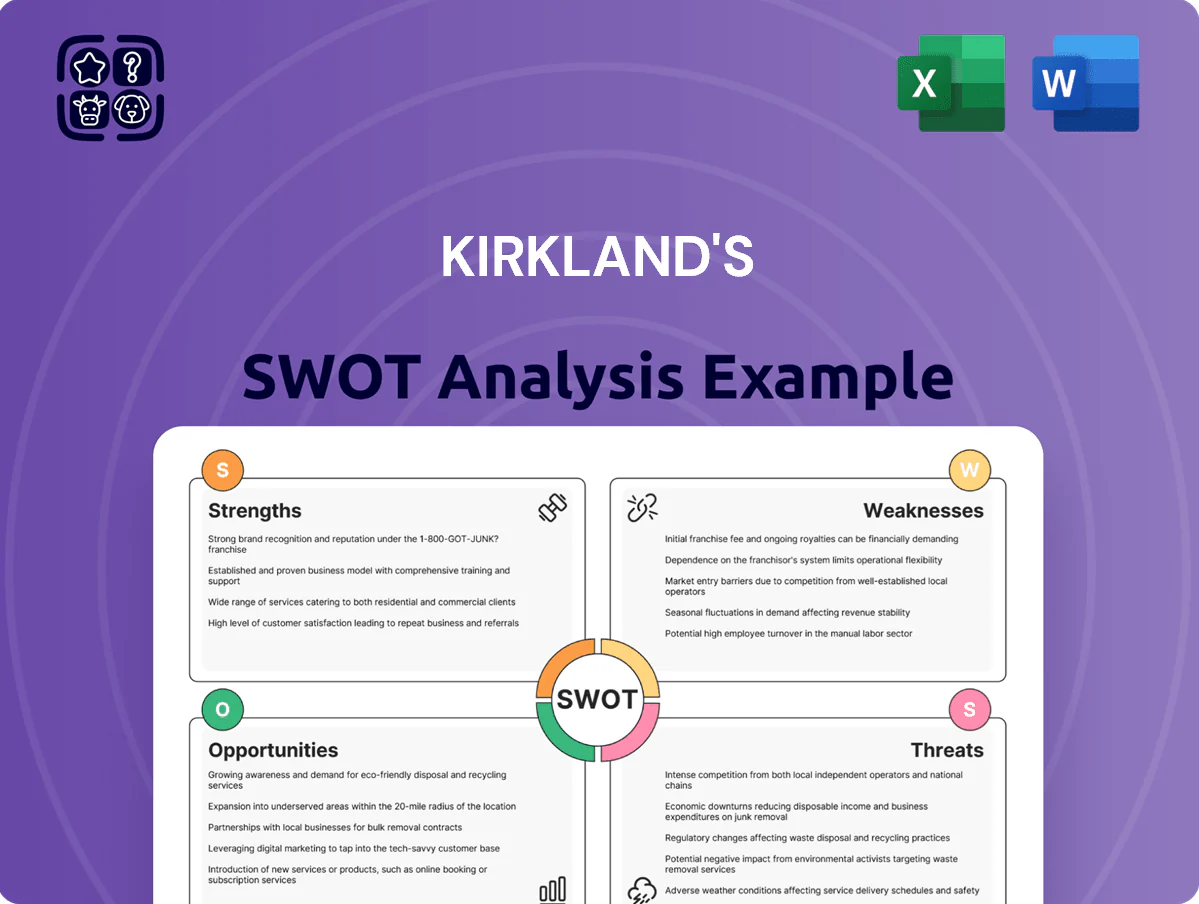

Strengths

Strategic Partnership with Beyond Inc

The 2025 partnership with Beyond Inc (formerly Overstock) boosted Kirkland's digital reach and ops: online sales rose 28% year-over-year through Q3 2025, and site traffic jumped 42%, providing access to Beyond’s 15M-customer network.

Integration of Beyond’s e-commerce stack cut average fulfillment time from 6.2 to 3.8 days and reduced shipping costs by ~12%, tying Kirkland's into a larger retail ecosystem.

Value-Oriented Brand Positioning

Kirkland’s positions itself as a value-oriented home décor brand, selling stylish pieces at accessible price points—average ticket roughly $28 in FY2024, up 4% year-over-year. This resonates with budget-conscious shoppers seeking curated aesthetics; same-store sales grew 3.5% in 2024 vs 2023, showing steady demand. Their treasure-hunt merchandising model drives consistent foot traffic, supporting 2024 store-level conversion improvements of ~120 basis points.

Strong Omnichannel Integration

Kirkland refined buy-online-pickup-in-store and ship-to-store, cutting per-order shipping costs by ~22% and lifting same-store sales conversion 6.8% by YE 2025; these services give shoppers immediate pickup and lower fulfillment spend for the retailer. By Dec 31, 2025 omnichannel drove ~34% of revenue and improved 12-month customer retention by 4.3 percentage points, making it a primary conversion engine.

Exclusive Private Label Offerings

Kirkland's proprietary private-label range makes up roughly 40% of SKUs, driving gross margins about 600 basis points above national brands and enabling tighter brand control and margin resilience versus big-box rivals.

Exclusive designs differentiate Kirkland's in décor; repeat buyers rose 12% year-over-year in FY2024, signaling stronger loyalty among home stylists and supporting pricing power.

- ~40% SKUs private label

- +600 bps margin vs national brands

- 12% repeat-buyer growth FY2024

Optimized Physical Store Footprint

- ~350 stores in 2025

- Higher store EBITDA margins

- Clustered inventory reduces logistics cost

- Better localized marketing and conversion

Kirkland’s omnichannel surge: +28% online, 34% revenue omnichannel, higher margins

Kirkland's strengthened omnichannel after a 2025 partnership with Beyond Inc, lifting online sales 28% YoY through Q3 2025 and omnichannel to ~34% of revenue by Dec 31, 2025; fulfillment time fell 6.2→3.8 days and shipping costs down ~12%. Private labels (~40% SKUs) deliver +600 bps margin vs national brands and 12% repeat-buyer growth in FY2024; ~350 stores by 2025 with higher store EBITDA.

| Metric | Value |

|---|---|

| Online sales change (Q3 2025 YoY) | +28% |

| Omnichannel revenue (Dec 31, 2025) | ~34% |

| Fulfillment time | 6.2→3.8 days |

| Private-label SKUs | ~40% |

| Margin uplift vs brands | +600 bps |

| Repeat-buyer growth (FY2024) | +12% |

| Store count (2025) | ~350 |

What is included in the product

Delivers a concise SWOT overview of Kirkland's, outlining its internal strengths and weaknesses alongside external opportunities and threats that shape the company's strategic position in the home décor retail market.

Provides a concise SWOT snapshot of Kirkland’s brand and operations for rapid strategic alignment and executive decision-making.

Weaknesses

Limited National Brand Awareness

Sensitivity to Discretionary Spending

The product mix is almost entirely discretionary home décor, so Kirkland Ltd (Kirkland’s, NASDAQ: KIRK) is highly exposed to consumer confidence swings; US consumer confidence fell to 99.6 in Dec 2024 from 107.8 a year earlier, raising downside risk. When inflation hit 3.4% in 2024, household spending shifted to essentials, and home furnishings saw category declines—Kirkland’s comparable sales dropped 8% in FY 2024, showing revenue volatility.

Historical Revenue Inconsistency

The company showed volatile comparable-store sales, swinging between -4.8% in FY2022 and +3.1% in FY2024, which seeded investor caution; by Q3 2025 management reported a 2.6% comp gain but revenue still lagged pre-pandemic levels at $436.7M YTD through Sep 2025. Turnaround moves (cost cuts, assortment resets) are underway, but the history of inconsistent results makes long-term capital allocation risky—sustained, predictable growth remains the primary hurdle.

Smaller Marketing Budget

Kirkland's 2024 marketing spend was about $22 million versus $1.5+ billion by Target’s parent (Target Corporation, 2024), so Kirkland's share of voice is limited and national reach weakens.

That gap forces reliance on organic social, email, and its loyalty program; with U.S. ad impressions dominated by mega-retailers, Kirkland's risks lower top-of-mind awareness and slower traffic growth.

- 2024 marketing spend ≈ $22M

- Target parent ad spend > $1.5B (2024)

- High dependency on organic and loyalty

- Lower national share-of-voice, weaker awareness

Operational Restructuring Overhead

- One-time restructuring spend: $55–70M

- FY2023 net loss: $18.6M

- Mid-2024 comps: -3.2%

- Risk: operational distraction, margin compression

Kirkland: $661.5M sales, shrinking comps and heavy restructuring squeeze growth

| Metric | Value |

|---|---|

| FY2024 Net Sales | $661.5M |

| FY2024 Marketing Spend | $22M |

| Estimated Ad Spend Needed (3–5%) | $20–33M |

| FY2023 Net Loss | $18.6M |

| Restructuring Costs 2024 | $55–70M |

| FY2024 Comparable Sales | -8% |

| US Consumer Confidence Dec 2024 | 99.6 |

Full Version Awaits

Kirkland's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the real file, structured and ready to use for strategic planning. Buy now to download the full, detailed report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kirkland’s strong brand recognition and niche home-decor positioning drive steady traffic, but margin pressures, online competition, and supply-chain volatility pose clear threats; our full SWOT unpacks these dynamics with revenue-impact analysis and strategic recommendations. Purchase the complete SWOT analysis for a professionally formatted Word report and editable Excel tools—ideal for investors, advisors, and strategists seeking actionable, research-backed insights.

Strengths

Strategic Partnership with Beyond Inc

The 2025 partnership with Beyond Inc (formerly Overstock) boosted Kirkland's digital reach and ops: online sales rose 28% year-over-year through Q3 2025, and site traffic jumped 42%, providing access to Beyond’s 15M-customer network.

Integration of Beyond’s e-commerce stack cut average fulfillment time from 6.2 to 3.8 days and reduced shipping costs by ~12%, tying Kirkland's into a larger retail ecosystem.

Value-Oriented Brand Positioning

Kirkland’s positions itself as a value-oriented home décor brand, selling stylish pieces at accessible price points—average ticket roughly $28 in FY2024, up 4% year-over-year. This resonates with budget-conscious shoppers seeking curated aesthetics; same-store sales grew 3.5% in 2024 vs 2023, showing steady demand. Their treasure-hunt merchandising model drives consistent foot traffic, supporting 2024 store-level conversion improvements of ~120 basis points.

Strong Omnichannel Integration

Kirkland refined buy-online-pickup-in-store and ship-to-store, cutting per-order shipping costs by ~22% and lifting same-store sales conversion 6.8% by YE 2025; these services give shoppers immediate pickup and lower fulfillment spend for the retailer. By Dec 31, 2025 omnichannel drove ~34% of revenue and improved 12-month customer retention by 4.3 percentage points, making it a primary conversion engine.

Exclusive Private Label Offerings

Kirkland's proprietary private-label range makes up roughly 40% of SKUs, driving gross margins about 600 basis points above national brands and enabling tighter brand control and margin resilience versus big-box rivals.

Exclusive designs differentiate Kirkland's in décor; repeat buyers rose 12% year-over-year in FY2024, signaling stronger loyalty among home stylists and supporting pricing power.

- ~40% SKUs private label

- +600 bps margin vs national brands

- 12% repeat-buyer growth FY2024

Optimized Physical Store Footprint

- ~350 stores in 2025

- Higher store EBITDA margins

- Clustered inventory reduces logistics cost

- Better localized marketing and conversion

Kirkland’s omnichannel surge: +28% online, 34% revenue omnichannel, higher margins

Kirkland's strengthened omnichannel after a 2025 partnership with Beyond Inc, lifting online sales 28% YoY through Q3 2025 and omnichannel to ~34% of revenue by Dec 31, 2025; fulfillment time fell 6.2→3.8 days and shipping costs down ~12%. Private labels (~40% SKUs) deliver +600 bps margin vs national brands and 12% repeat-buyer growth in FY2024; ~350 stores by 2025 with higher store EBITDA.

| Metric | Value |

|---|---|

| Online sales change (Q3 2025 YoY) | +28% |

| Omnichannel revenue (Dec 31, 2025) | ~34% |

| Fulfillment time | 6.2→3.8 days |

| Private-label SKUs | ~40% |

| Margin uplift vs brands | +600 bps |

| Repeat-buyer growth (FY2024) | +12% |

| Store count (2025) | ~350 |

What is included in the product

Delivers a concise SWOT overview of Kirkland's, outlining its internal strengths and weaknesses alongside external opportunities and threats that shape the company's strategic position in the home décor retail market.

Provides a concise SWOT snapshot of Kirkland’s brand and operations for rapid strategic alignment and executive decision-making.

Weaknesses

Limited National Brand Awareness

Sensitivity to Discretionary Spending

The product mix is almost entirely discretionary home décor, so Kirkland Ltd (Kirkland’s, NASDAQ: KIRK) is highly exposed to consumer confidence swings; US consumer confidence fell to 99.6 in Dec 2024 from 107.8 a year earlier, raising downside risk. When inflation hit 3.4% in 2024, household spending shifted to essentials, and home furnishings saw category declines—Kirkland’s comparable sales dropped 8% in FY 2024, showing revenue volatility.

Historical Revenue Inconsistency

The company showed volatile comparable-store sales, swinging between -4.8% in FY2022 and +3.1% in FY2024, which seeded investor caution; by Q3 2025 management reported a 2.6% comp gain but revenue still lagged pre-pandemic levels at $436.7M YTD through Sep 2025. Turnaround moves (cost cuts, assortment resets) are underway, but the history of inconsistent results makes long-term capital allocation risky—sustained, predictable growth remains the primary hurdle.

Smaller Marketing Budget

Kirkland's 2024 marketing spend was about $22 million versus $1.5+ billion by Target’s parent (Target Corporation, 2024), so Kirkland's share of voice is limited and national reach weakens.

That gap forces reliance on organic social, email, and its loyalty program; with U.S. ad impressions dominated by mega-retailers, Kirkland's risks lower top-of-mind awareness and slower traffic growth.

- 2024 marketing spend ≈ $22M

- Target parent ad spend > $1.5B (2024)

- High dependency on organic and loyalty

- Lower national share-of-voice, weaker awareness

Operational Restructuring Overhead

- One-time restructuring spend: $55–70M

- FY2023 net loss: $18.6M

- Mid-2024 comps: -3.2%

- Risk: operational distraction, margin compression

Kirkland: $661.5M sales, shrinking comps and heavy restructuring squeeze growth

| Metric | Value |

|---|---|

| FY2024 Net Sales | $661.5M |

| FY2024 Marketing Spend | $22M |

| Estimated Ad Spend Needed (3–5%) | $20–33M |

| FY2023 Net Loss | $18.6M |

| Restructuring Costs 2024 | $55–70M |

| FY2024 Comparable Sales | -8% |

| US Consumer Confidence Dec 2024 | 99.6 |

Full Version Awaits

Kirkland's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; once purchased, the complete, editable version is unlocked. You’re viewing a live preview of the real file, structured and ready to use for strategic planning. Buy now to download the full, detailed report.