Kistos Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

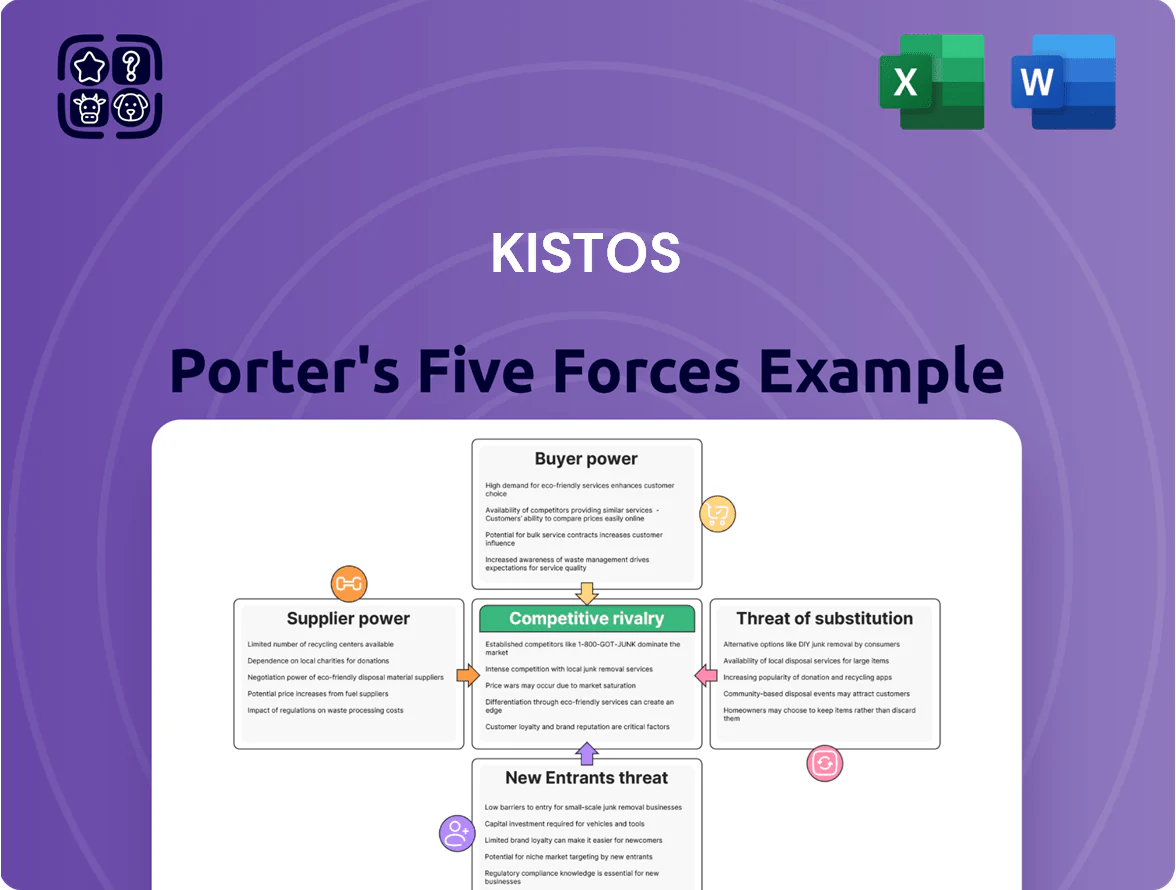

Kistos faces moderate supplier power and capital-intensive barriers that limit new entrants, while buyer bargaining and substitution risks vary by end-market—this snapshot highlights key competitive tensions and strategic levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kistos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Oilfield Service Providers

The market for high-end drilling and maintenance is concentrated: SLB (Schlumberger) and Halliburton control ~40–50% of global premium offshore service revenue, giving them pricing power over Kistos’ contracts.

Kistos depends on their rigs, subsea tech, and specialist crews, so suppliers can demand premium rates and longer lead times.

By late 2025 inflation in energy services rose ~8–12% YoY, keeping offshore maintenance demand high and furthering supplier leverage.

Limited Availability of Offshore Rigs

The North Sea supply of jack-up and semi‑submersible rigs is tight: global idle rig count fell to ~8% in Q4 2025 from 14% in 2020, while newbuild orders remain minimal, so Kistos must compete for assets.

That competition pushed North Sea dayrates up 35% year‑over‑year in 2025, forcing Kistos into higher rates and stricter multi‑year contracts.

Scarcity gives rig owners negotiation leverage, raising leasing costs and reducing contractual flexibility for Kistos’ exploration and development projects.

Regulatory and Licensing Authorities

Government bodies issuing licenses and environmental permits act as powerful suppliers for Kistos, controlling project timing and scope; delayed permits raise monthly operating losses—example: a 6-month permit delay could cost ~USD 3–5m in foregone revenues per offshore asset.

Specialized Technical Labor Shortage

The energy transition drove 12–18% of UK petroleum engineers and geoscientists toward renewables by 2023, squeezing Kistos’ talent pool and raising wage demands for offshore roles by ~15% vs 2019.

Kistos must match market pay and sign-on bonuses; scarcity boosts specialized staff and recruitment agencies' bargaining power, increasing operating cost risk and project timing exposure.

- 12–18% migration to renewables (UK, 2023)

- ~15% higher wage demands vs 2019

- Higher recruitment fees and sign-on bonuses

- Increased operating-cost and schedule risk

Midstream Infrastructure Access

- Third-party control raises tariff risk

- 2024 UK pipeline tariffs +8% (example)

- Replacement infrastructure cost: hundreds of millions+

- Limited negotiating leverage on access schedules

Suppliers Wield Pricing Power: Dayrates +35% as Top Firms Capture 40–50% Offshore Revenue

Suppliers hold strong leverage over Kistos: top service firms (SLB, Halliburton) control ~40–50% premium offshore revenue, North Sea idle rigs fell to ~8% in Q4 2025 (vs 14% in 2020) pushing 2025 dayrates +35% YoY, UK pipeline tariffs +8% in 2024, and skilled staff migration (12–18% to renewables by 2023) raised wage demands ~15% vs 2019.

| Metric | Value |

|---|---|

| Top suppliers’ market share | 40–50% |

| Idle rig count (Q4 2025) | ~8% |

| North Sea dayrates change (2025) | +35% YoY |

| UK pipeline tariffs (2024) | +8% |

| Talent migration (UK, 2023) | 12–18% |

| Wage increase vs 2019 | ~15% |

What is included in the product

Concise Porter's Five Forces assessment tailored for Kistos, revealing competitive pressures, supplier and buyer power, substitution risks, and entry barriers to inform strategy and investor decision-making.

A concise Porter's Five Forces one-sheet tailored for Kistos—quickly spot where competitive pressures bite and prioritize strategic moves.

Customers Bargaining Power

Commodity Market Price Taking

Natural gas is a globally traded commodity, so Kistos Energy has virtually no price-setting power; in 2025 UK gas referenced to the National Balancing Point (NBP) averaged about 52 p/therm (≈£52/MWh), which directly caps Kistos revenue per unit.

Revenue follows benchmarks like the Title Transfer Facility (TTF) and NBP; large utilities and industrial buyers procure at these hubs, forcing Kistos to accept prevailing rates and limiting margin control.

Wholesale Buyer Concentration

Low Switching Costs for Energy Grids

National grids and wholesale buyers can switch gas sources quickly; in 2024 UK gas imports rose 18% to 36 bcm, highlighting buyer flexibility.

Kistos’s gas is chemically identical to competitors’, so no brand loyalty—contracts hinge on price and delivery terms.

With spot LNG prices averaging $12.5/MMBtu in 2024, customers can pick lowest-cost suppliers or shorter-term, flexible contracts.

Impact of Long-Term Offtake Agreements

Long-term offtake contracts help Kistos secure financing and stabilize cash flows by fixing prices or volumes, with typical contracts covering 3–10 years and often locking in 70–90% of near-term production.

These agreements cap upside: if spot gas prices jump (e.g., EU TTF rose ~+85% in 2022 peak vs 2020), Kistos cannot fully benefit, shifting volatility risk to the producer.

Customers use long-term deals for supply security, forcing Kistos to trade off liquidity/stability versus market upside and retaining most price risk on its balance sheet.

- Secures 70–90% production

- Typical term: 3–10 years

- Limits upside during spot spikes (TTF +85% in 2022)

- Shifts price volatility risk to Kistos

Governmental Influence on Demand

- UK/EU subsidies up €10–15bn (2024)

- Buyers demand 20–40% lower carbon intensity

- Pool of long-term gas buyers shrinking

- Kistos needs efficiency + green certification

Customers squeeze Kistos: capped prices, big traders, imports, short tenors limit upside

Customers hold strong bargaining power: gas is fungible and UK NBP/TTF benchmarks capped 2025 prices (~52 p/therm ≈ £52/MWh); large traders/utilities (≈60% regional offtake in 2024) and rising UK imports (36 bcm, +18% in 2024) force Kistos onto prevailing rates, push short tenors, and demand lower carbon intensity (20–40% cuts), while 3–10yr offtakes secure 70–90% production but limit upside.

| Metric | Value |

|---|---|

| 2025 NBP avg | 52 p/therm |

| Regional offtake by majors (2024) | ≈60% |

| UK imports (2024) | 36 bcm (+18%) |

| Spot LNG avg (2024) | $12.5/MMBtu |

| Offtake terms | 3–10 yr, 70–90% prod |

Full Version Awaits

Kistos Porter's Five Forces Analysis

This preview shows the exact Kistos Porter’s Five Forces analysis document you'll receive immediately after purchase—fully formatted, comprehensive, and ready to download with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kistos faces moderate supplier power and capital-intensive barriers that limit new entrants, while buyer bargaining and substitution risks vary by end-market—this snapshot highlights key competitive tensions and strategic levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kistos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Oilfield Service Providers

The market for high-end drilling and maintenance is concentrated: SLB (Schlumberger) and Halliburton control ~40–50% of global premium offshore service revenue, giving them pricing power over Kistos’ contracts.

Kistos depends on their rigs, subsea tech, and specialist crews, so suppliers can demand premium rates and longer lead times.

By late 2025 inflation in energy services rose ~8–12% YoY, keeping offshore maintenance demand high and furthering supplier leverage.

Limited Availability of Offshore Rigs

The North Sea supply of jack-up and semi‑submersible rigs is tight: global idle rig count fell to ~8% in Q4 2025 from 14% in 2020, while newbuild orders remain minimal, so Kistos must compete for assets.

That competition pushed North Sea dayrates up 35% year‑over‑year in 2025, forcing Kistos into higher rates and stricter multi‑year contracts.

Scarcity gives rig owners negotiation leverage, raising leasing costs and reducing contractual flexibility for Kistos’ exploration and development projects.

Regulatory and Licensing Authorities

Government bodies issuing licenses and environmental permits act as powerful suppliers for Kistos, controlling project timing and scope; delayed permits raise monthly operating losses—example: a 6-month permit delay could cost ~USD 3–5m in foregone revenues per offshore asset.

Specialized Technical Labor Shortage

The energy transition drove 12–18% of UK petroleum engineers and geoscientists toward renewables by 2023, squeezing Kistos’ talent pool and raising wage demands for offshore roles by ~15% vs 2019.

Kistos must match market pay and sign-on bonuses; scarcity boosts specialized staff and recruitment agencies' bargaining power, increasing operating cost risk and project timing exposure.

- 12–18% migration to renewables (UK, 2023)

- ~15% higher wage demands vs 2019

- Higher recruitment fees and sign-on bonuses

- Increased operating-cost and schedule risk

Midstream Infrastructure Access

- Third-party control raises tariff risk

- 2024 UK pipeline tariffs +8% (example)

- Replacement infrastructure cost: hundreds of millions+

- Limited negotiating leverage on access schedules

Suppliers Wield Pricing Power: Dayrates +35% as Top Firms Capture 40–50% Offshore Revenue

Suppliers hold strong leverage over Kistos: top service firms (SLB, Halliburton) control ~40–50% premium offshore revenue, North Sea idle rigs fell to ~8% in Q4 2025 (vs 14% in 2020) pushing 2025 dayrates +35% YoY, UK pipeline tariffs +8% in 2024, and skilled staff migration (12–18% to renewables by 2023) raised wage demands ~15% vs 2019.

| Metric | Value |

|---|---|

| Top suppliers’ market share | 40–50% |

| Idle rig count (Q4 2025) | ~8% |

| North Sea dayrates change (2025) | +35% YoY |

| UK pipeline tariffs (2024) | +8% |

| Talent migration (UK, 2023) | 12–18% |

| Wage increase vs 2019 | ~15% |

What is included in the product

Concise Porter's Five Forces assessment tailored for Kistos, revealing competitive pressures, supplier and buyer power, substitution risks, and entry barriers to inform strategy and investor decision-making.

A concise Porter's Five Forces one-sheet tailored for Kistos—quickly spot where competitive pressures bite and prioritize strategic moves.

Customers Bargaining Power

Commodity Market Price Taking

Natural gas is a globally traded commodity, so Kistos Energy has virtually no price-setting power; in 2025 UK gas referenced to the National Balancing Point (NBP) averaged about 52 p/therm (≈£52/MWh), which directly caps Kistos revenue per unit.

Revenue follows benchmarks like the Title Transfer Facility (TTF) and NBP; large utilities and industrial buyers procure at these hubs, forcing Kistos to accept prevailing rates and limiting margin control.

Wholesale Buyer Concentration

Low Switching Costs for Energy Grids

National grids and wholesale buyers can switch gas sources quickly; in 2024 UK gas imports rose 18% to 36 bcm, highlighting buyer flexibility.

Kistos’s gas is chemically identical to competitors’, so no brand loyalty—contracts hinge on price and delivery terms.

With spot LNG prices averaging $12.5/MMBtu in 2024, customers can pick lowest-cost suppliers or shorter-term, flexible contracts.

Impact of Long-Term Offtake Agreements

Long-term offtake contracts help Kistos secure financing and stabilize cash flows by fixing prices or volumes, with typical contracts covering 3–10 years and often locking in 70–90% of near-term production.

These agreements cap upside: if spot gas prices jump (e.g., EU TTF rose ~+85% in 2022 peak vs 2020), Kistos cannot fully benefit, shifting volatility risk to the producer.

Customers use long-term deals for supply security, forcing Kistos to trade off liquidity/stability versus market upside and retaining most price risk on its balance sheet.

- Secures 70–90% production

- Typical term: 3–10 years

- Limits upside during spot spikes (TTF +85% in 2022)

- Shifts price volatility risk to Kistos

Governmental Influence on Demand

- UK/EU subsidies up €10–15bn (2024)

- Buyers demand 20–40% lower carbon intensity

- Pool of long-term gas buyers shrinking

- Kistos needs efficiency + green certification

Customers squeeze Kistos: capped prices, big traders, imports, short tenors limit upside

Customers hold strong bargaining power: gas is fungible and UK NBP/TTF benchmarks capped 2025 prices (~52 p/therm ≈ £52/MWh); large traders/utilities (≈60% regional offtake in 2024) and rising UK imports (36 bcm, +18% in 2024) force Kistos onto prevailing rates, push short tenors, and demand lower carbon intensity (20–40% cuts), while 3–10yr offtakes secure 70–90% production but limit upside.

| Metric | Value |

|---|---|

| 2025 NBP avg | 52 p/therm |

| Regional offtake by majors (2024) | ≈60% |

| UK imports (2024) | 36 bcm (+18%) |

| Spot LNG avg (2024) | $12.5/MMBtu |

| Offtake terms | 3–10 yr, 70–90% prod |

Full Version Awaits

Kistos Porter's Five Forces Analysis

This preview shows the exact Kistos Porter’s Five Forces analysis document you'll receive immediately after purchase—fully formatted, comprehensive, and ready to download with no placeholders or mockups.