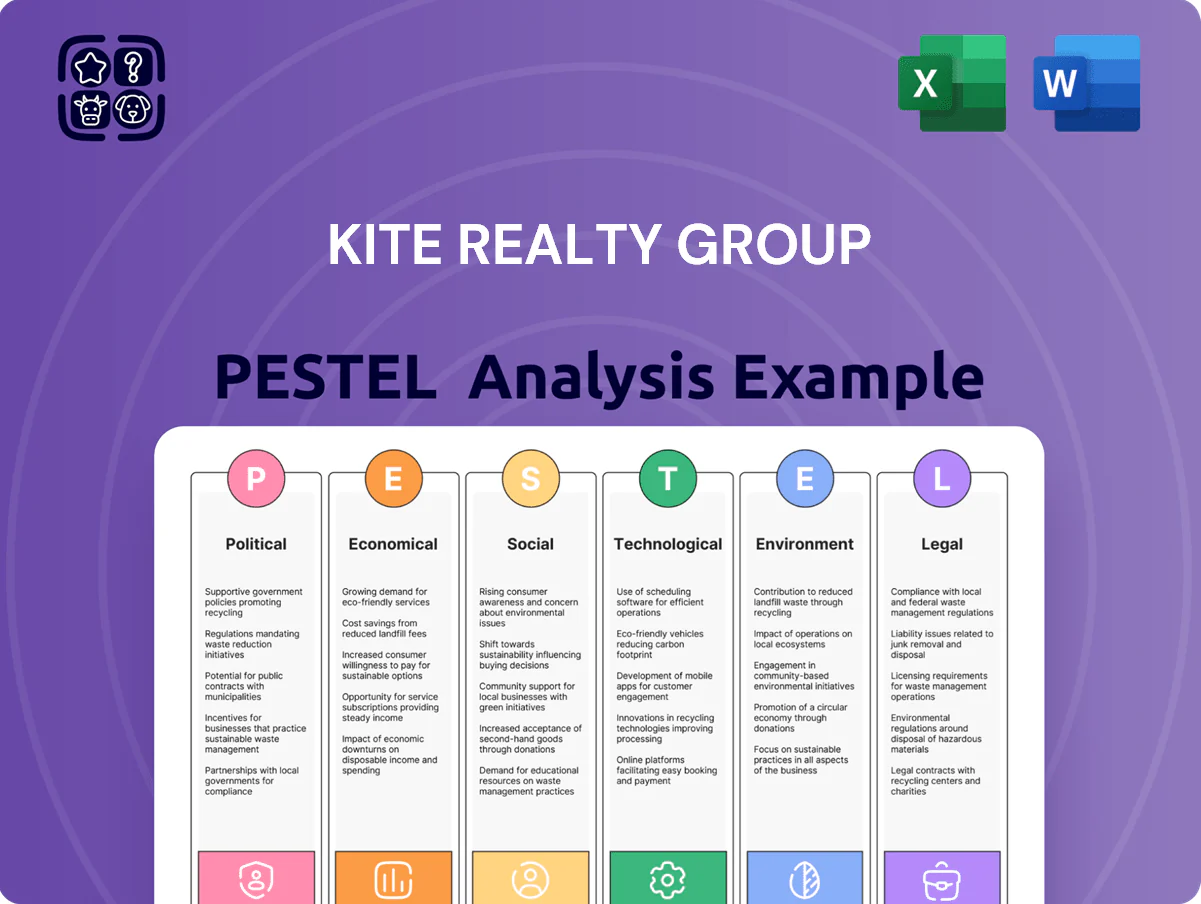

Kite Realty Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how regulatory shifts, economic cycles, and ESG trends are reshaping Kite Realty Group’s prospects with our concise PESTLE snapshot—ideal for investors and strategists who need immediate context. Purchase the full PESTLE Analysis to access a complete, actionable breakdown of political, economic, social, technological, legal, and environmental drivers tailored to Kite Realty Group.

Political factors

Federal Tax Policy and REIT Status

Federal REIT rules require Kite Realty to distribute at least 90% of taxable income, forcing a high payout ratio—KRG reported a 2024 FFO payout near 85–95% after $0.24 quarterly dividends—so changes to corporate tax rates or REIT qualification could alter its capital structure, increase retained earnings needs, or raise cost of capital; preserving REIT status avoids double taxation and supports investor confidence in its ~120 million sq ft retail portfolio.

Zoning and Land Use Regulations

Local political environments dictate feasibility of Kite Realty redevelopment and mixed-use expansions; in 2024 Kite owned 41.9 million square feet across 134 U.S. open-air centers, so zoning shifts materially affect asset densification and NOI. Changes in municipal leadership have led to zoning amendments in several Sun Belt markets in 2023–2025, speeding approvals in some jurisdictions and delaying projects elsewhere. Navigating these landscapes is essential to execute Kite’s long-term value-creation strategy in high-growth markets.

Geopolitical Stability and Trade Policy

Federal tariffs and trade policy affect Kite Realty’s renovation costs as imported steel and electronics saw price swings—U.S. tariff-driven steel prices rose ~18% in 2024, pushing construction input costs higher; lumber volatility (up 12% year-over-year in 2024) and 2023–24 supply-chain delays increased capex for mall refurbishments, tightening budgets for new developments and delaying maintenance schedules.

Government Infrastructure Spending

Federal and state investments in transportation infrastructure near Kite Realty properties—such as the $1.2 trillion Bipartisan Infrastructure Law allocations and $110B in FY2025 highway grants—can boost accessibility and raise foot traffic at key centers, increasing NOI and property valuations.

Political choices on highway expansions or transit upgrades shape retail corridor desirability; Kite monitors legislation and recent $24M state transit projects affecting several Midwestern assets to guide acquisitions.

- Infrastructure funding: $1.2T federal law; $110B FY2025 highway grants

- Targeted state projects: $24M recent Midwestern transit investments

- Strategy: acquisition focus on corridors with confirmed public capital

Public-Private Partnership Initiatives

Political support for urban revitalization often provides incentives—Kite Realty partners have accessed tax abatements and opportunity zone benefits; in 2024 municipal incentives averaged 12–18% of redevelopment project costs in major U.S. metros.

Kite may secure grants or PILOT agreements with local governments to include affordable housing or community spaces, lowering upfront capital needs and improving IRRs on mixed-use conversions.

These public-private partnerships reduce financial risk for large-scale transformations; recent redevelopment deals reported public funding covering up to 25% of eligible project costs.

- 2024 municipal incentives ≈ 12–18% of project costs

- Public funding can cover up to 25% of eligible costs

- PILOTs/tax abatements improve IRR on mixed-use projects

REIT under pressure: high FFO payouts, costly redevelopments, infrastructure tailwinds

Political factors: REIT tax rules force high payouts (KRG 2024 FFO payout ~85–95%), zoning and local politics affect redevelopment of 41.9M sq ft across 134 centers, federal infrastructure ($1.2T law; $110B FY2025) and $24M state projects boost NOI, tariffs raised 2024 construction inputs (steel +18%, lumber +12%), municipal incentives averaged 12–18% of redevelopment costs.

| Metric | Value |

|---|---|

| FFO payout | 85–95% |

| Portfolio | 41.9M sq ft, 134 centers |

| Infra funding | $1.2T/$110B |

| Steel/lumber 2024 | +18%/+12% |

| Municipal incentives | 12–18% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Kite Realty Group’s retail-focused real estate portfolio, with data-driven trends, forward-looking insights, and actionable implications to support executives, investors, and strategists in risk mitigation and opportunity identification.

Provides a concise, visually segmented PESTLE summary of Kite Realty Group that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory impacts, and market positioning for faster decision-making.

Economic factors

Interest Rate Environment

As of late 2025, Kite Realty Group faces higher cost of debt sensitivity: the 10-year U.S. Treasury rose to about 4.5% in 2025, keeping REIT borrowing costs elevated and pressuring cap rates used to value Kite’s $6.2bn portfolio (2024 book value).

Consumer Spending and Inflation

Kite Realty Group’s revenue is tightly linked to retail health and consumer disposable income in its markets; U.S. retail sales rose 4.5% year-over-year through 2025, supporting demand in many of its open-air centers. Persistent inflation—CPI at 3.4% in 2025—squeezes tenant margins, increasing rent default and weakening lease renewal leverage for some tenants. Conversely, strong consumer confidence in high-growth Sun Belt metros lifted tenant same-store sales up to mid-single digits in 2024–25, enabling favorable rent escalations and occupancy above 94% in top assets.

Labor Market Dynamics

Employment growth in Sun Belt metros—e.g., Austin, Phoenix, and Tampa saw payroll gains of 2.8–3.6% in 2024—boosts demand for retail and mixed-use housing at Kite Realty centers; regional unemployment rates averaging ~3.5% in 2024 vs. 4.0% U.S. support steady foot traffic. Tight labor markets pushed average hourly wages in leisure and hospitality up ~4% YoY in 2024, raising tenant operating costs. Kite benefits where local job growth outpaces national averages, sustaining occupancies above its portfolio median of ~95% in 2024.

Capital Market Access

The ability to raise equity or issue debt on favorable terms is essential for Kite Realty Group’s growth through acquisitions and property upgrades; as of Q4 2025 KRG’s net debt/EBITDA was ~6.2x, highlighting sensitivity to borrowing costs.

Economic volatility can limit liquidity in capital markets, forcing REITs to rely more on internal cash flow or asset dispositions; in 2024 REIT equity issuance fell ~18% YoY, tightening alternatives.

Monitoring secondary equity market health ensures KRG can fund its pipeline without excessive dilution—2025 average REIT share issuance discounts narrowed to ~6%, improving fundraising prospects.

- Net debt/EBITDA ~6.2x (Q4 2025)

- REIT equity issuance down ~18% YoY in 2024

- Average issuance discount ~6% in 2025

E-commerce Integration and Retail Resilience

The shift to omnichannel retail raises demand for physical stores as fulfillment hubs; BOPIS transactions grew 54% in 2023 and accounted for ~20% of U.S. online orders by 2024, boosting foot traffic and supporting rent growth for well-located centers.

Kite Realty’s open-air portfolio—~85% of GLA in open-air formats as of Q4 2024—offers curbside/BOPIS efficiency, improving tenant sales per sq ft and reducing vacancy risk amid retail circulation shifts.

- 54% growth in BOPIS (2023)

- BOPIS ~20% of online orders (2024)

- Kite ~85% open-air GLA (Q4 2024)

Kite: Rising costs and leverage vs. Sun Belt demand—occupancy resilience driven by open‑air exposure

Kite faces higher funding costs as 10y UST ~4.5% (2025) and net debt/EBITDA ~6.2x (Q4 2025), while CPI ~3.4% (2025) raises tenant strain; Sun Belt job growth (~2.8–3.6% in 2024) and retail sales +4.5% (2025) support occupancy >94%; BOPIS penetration ~20% (2024) favors Kite’s ~85% open-air GLA.

| Metric | Value |

|---|---|

| 10y UST (2025) | ~4.5% |

| Net debt/EBITDA (Q4 2025) | ~6.2x |

| CPI (2025) | 3.4% |

| Retail sales YoY (2025) | +4.5% |

| Sun Belt payroll growth (2024) | 2.8–3.6% |

| BOPIS share (2024) | ~20% |

| Open-air GLA (Q4 2024) | ~85% |

Preview the Actual Deliverable

Kite Realty Group PESTLE Analysis

The preview shown here is the exact Kite Realty Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview are the same file you’ll download immediately after payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how regulatory shifts, economic cycles, and ESG trends are reshaping Kite Realty Group’s prospects with our concise PESTLE snapshot—ideal for investors and strategists who need immediate context. Purchase the full PESTLE Analysis to access a complete, actionable breakdown of political, economic, social, technological, legal, and environmental drivers tailored to Kite Realty Group.

Political factors

Federal Tax Policy and REIT Status

Federal REIT rules require Kite Realty to distribute at least 90% of taxable income, forcing a high payout ratio—KRG reported a 2024 FFO payout near 85–95% after $0.24 quarterly dividends—so changes to corporate tax rates or REIT qualification could alter its capital structure, increase retained earnings needs, or raise cost of capital; preserving REIT status avoids double taxation and supports investor confidence in its ~120 million sq ft retail portfolio.

Zoning and Land Use Regulations

Local political environments dictate feasibility of Kite Realty redevelopment and mixed-use expansions; in 2024 Kite owned 41.9 million square feet across 134 U.S. open-air centers, so zoning shifts materially affect asset densification and NOI. Changes in municipal leadership have led to zoning amendments in several Sun Belt markets in 2023–2025, speeding approvals in some jurisdictions and delaying projects elsewhere. Navigating these landscapes is essential to execute Kite’s long-term value-creation strategy in high-growth markets.

Geopolitical Stability and Trade Policy

Federal tariffs and trade policy affect Kite Realty’s renovation costs as imported steel and electronics saw price swings—U.S. tariff-driven steel prices rose ~18% in 2024, pushing construction input costs higher; lumber volatility (up 12% year-over-year in 2024) and 2023–24 supply-chain delays increased capex for mall refurbishments, tightening budgets for new developments and delaying maintenance schedules.

Government Infrastructure Spending

Federal and state investments in transportation infrastructure near Kite Realty properties—such as the $1.2 trillion Bipartisan Infrastructure Law allocations and $110B in FY2025 highway grants—can boost accessibility and raise foot traffic at key centers, increasing NOI and property valuations.

Political choices on highway expansions or transit upgrades shape retail corridor desirability; Kite monitors legislation and recent $24M state transit projects affecting several Midwestern assets to guide acquisitions.

- Infrastructure funding: $1.2T federal law; $110B FY2025 highway grants

- Targeted state projects: $24M recent Midwestern transit investments

- Strategy: acquisition focus on corridors with confirmed public capital

Public-Private Partnership Initiatives

Political support for urban revitalization often provides incentives—Kite Realty partners have accessed tax abatements and opportunity zone benefits; in 2024 municipal incentives averaged 12–18% of redevelopment project costs in major U.S. metros.

Kite may secure grants or PILOT agreements with local governments to include affordable housing or community spaces, lowering upfront capital needs and improving IRRs on mixed-use conversions.

These public-private partnerships reduce financial risk for large-scale transformations; recent redevelopment deals reported public funding covering up to 25% of eligible project costs.

- 2024 municipal incentives ≈ 12–18% of project costs

- Public funding can cover up to 25% of eligible costs

- PILOTs/tax abatements improve IRR on mixed-use projects

REIT under pressure: high FFO payouts, costly redevelopments, infrastructure tailwinds

Political factors: REIT tax rules force high payouts (KRG 2024 FFO payout ~85–95%), zoning and local politics affect redevelopment of 41.9M sq ft across 134 centers, federal infrastructure ($1.2T law; $110B FY2025) and $24M state projects boost NOI, tariffs raised 2024 construction inputs (steel +18%, lumber +12%), municipal incentives averaged 12–18% of redevelopment costs.

| Metric | Value |

|---|---|

| FFO payout | 85–95% |

| Portfolio | 41.9M sq ft, 134 centers |

| Infra funding | $1.2T/$110B |

| Steel/lumber 2024 | +18%/+12% |

| Municipal incentives | 12–18% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Kite Realty Group’s retail-focused real estate portfolio, with data-driven trends, forward-looking insights, and actionable implications to support executives, investors, and strategists in risk mitigation and opportunity identification.

Provides a concise, visually segmented PESTLE summary of Kite Realty Group that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory impacts, and market positioning for faster decision-making.

Economic factors

Interest Rate Environment

As of late 2025, Kite Realty Group faces higher cost of debt sensitivity: the 10-year U.S. Treasury rose to about 4.5% in 2025, keeping REIT borrowing costs elevated and pressuring cap rates used to value Kite’s $6.2bn portfolio (2024 book value).

Consumer Spending and Inflation

Kite Realty Group’s revenue is tightly linked to retail health and consumer disposable income in its markets; U.S. retail sales rose 4.5% year-over-year through 2025, supporting demand in many of its open-air centers. Persistent inflation—CPI at 3.4% in 2025—squeezes tenant margins, increasing rent default and weakening lease renewal leverage for some tenants. Conversely, strong consumer confidence in high-growth Sun Belt metros lifted tenant same-store sales up to mid-single digits in 2024–25, enabling favorable rent escalations and occupancy above 94% in top assets.

Labor Market Dynamics

Employment growth in Sun Belt metros—e.g., Austin, Phoenix, and Tampa saw payroll gains of 2.8–3.6% in 2024—boosts demand for retail and mixed-use housing at Kite Realty centers; regional unemployment rates averaging ~3.5% in 2024 vs. 4.0% U.S. support steady foot traffic. Tight labor markets pushed average hourly wages in leisure and hospitality up ~4% YoY in 2024, raising tenant operating costs. Kite benefits where local job growth outpaces national averages, sustaining occupancies above its portfolio median of ~95% in 2024.

Capital Market Access

The ability to raise equity or issue debt on favorable terms is essential for Kite Realty Group’s growth through acquisitions and property upgrades; as of Q4 2025 KRG’s net debt/EBITDA was ~6.2x, highlighting sensitivity to borrowing costs.

Economic volatility can limit liquidity in capital markets, forcing REITs to rely more on internal cash flow or asset dispositions; in 2024 REIT equity issuance fell ~18% YoY, tightening alternatives.

Monitoring secondary equity market health ensures KRG can fund its pipeline without excessive dilution—2025 average REIT share issuance discounts narrowed to ~6%, improving fundraising prospects.

- Net debt/EBITDA ~6.2x (Q4 2025)

- REIT equity issuance down ~18% YoY in 2024

- Average issuance discount ~6% in 2025

E-commerce Integration and Retail Resilience

The shift to omnichannel retail raises demand for physical stores as fulfillment hubs; BOPIS transactions grew 54% in 2023 and accounted for ~20% of U.S. online orders by 2024, boosting foot traffic and supporting rent growth for well-located centers.

Kite Realty’s open-air portfolio—~85% of GLA in open-air formats as of Q4 2024—offers curbside/BOPIS efficiency, improving tenant sales per sq ft and reducing vacancy risk amid retail circulation shifts.

- 54% growth in BOPIS (2023)

- BOPIS ~20% of online orders (2024)

- Kite ~85% open-air GLA (Q4 2024)

Kite: Rising costs and leverage vs. Sun Belt demand—occupancy resilience driven by open‑air exposure

Kite faces higher funding costs as 10y UST ~4.5% (2025) and net debt/EBITDA ~6.2x (Q4 2025), while CPI ~3.4% (2025) raises tenant strain; Sun Belt job growth (~2.8–3.6% in 2024) and retail sales +4.5% (2025) support occupancy >94%; BOPIS penetration ~20% (2024) favors Kite’s ~85% open-air GLA.

| Metric | Value |

|---|---|

| 10y UST (2025) | ~4.5% |

| Net debt/EBITDA (Q4 2025) | ~6.2x |

| CPI (2025) | 3.4% |

| Retail sales YoY (2025) | +4.5% |

| Sun Belt payroll growth (2024) | 2.8–3.6% |

| BOPIS share (2024) | ~20% |

| Open-air GLA (Q4 2024) | ~85% |

Preview the Actual Deliverable

Kite Realty Group PESTLE Analysis

The preview shown here is the exact Kite Realty Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview are the same file you’ll download immediately after payment, with no placeholders or surprises.