Kitwave Group SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Kitwave Group shows strong market reach with diversified retail channels and resilient wholesale relationships, but faces margin pressure from supply-chain costs and competitive pricing—our preview highlights key drivers and risks.

Discover the full SWOT analysis to access an investor-ready Word report and editable Excel matrix with research-backed insights, strategic recommendations, and financial context—purchase now to plan, pitch, or invest with confidence.

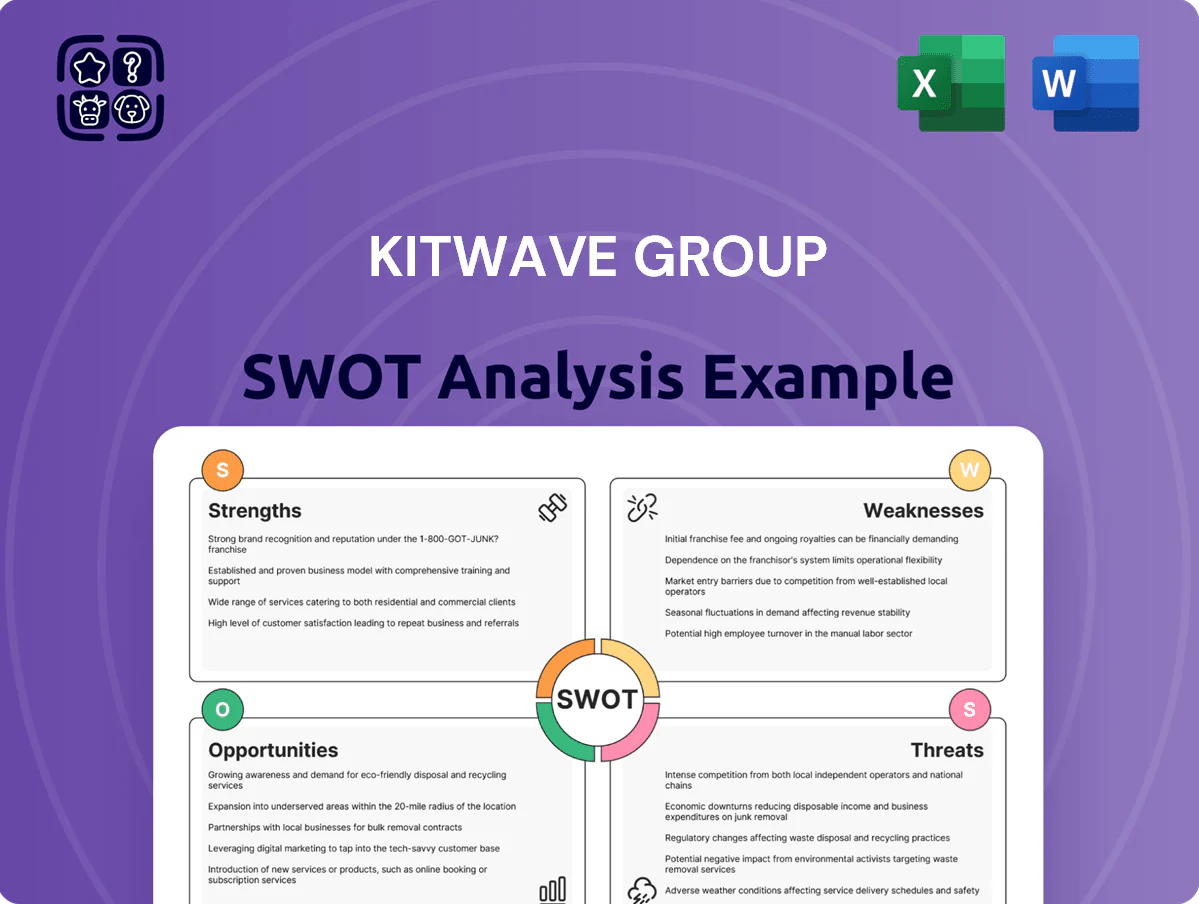

Strengths

Successful buy-and-build strategy

Kitwave has completed 12 acquisitions since 2018, growing revenue from £45m in FY2018 to £210m in FY2024, showing repeatable buy-and-build execution.

The group expanded into 8 new UK regions and 15 product categories, raising adjusted EBITDA margin from 8.5% to 12.3% over the period.

Management targets ~£2m EBITDA per acquisition and closed value-accretive deals averaging 6x EV/EBITDA, proving disciplined consolidation of the fragmented UK wholesale market.

Diversified product portfolio

Kitwave Group sells confectionery, snacks, soft drinks, alcohol, frozen and chilled foods, giving it broad category exposure and reducing reliance on any single segment; in FY2024 non-alcohol sales made ~68% of revenue while chilled & frozen grew 12% year-on-year to support margins. By offering a one-stop-shop to independents and foodservice, Kitwave raises share-of-wallet—top-50 customers account for ~22% of group sales—so cross-sell drives higher basket value. Serving multiple niches also smooths seasonal dips and supports stable cashflow, with gross margin at ~28% in 2024.

Extensive UK distribution network

With dozens of depots—Kitwave operated 46 UK depots as of FY2024—its extensive distribution network delivers 98% on-time service for trade customers, supporting rapid same/next-day deliveries across 90% of postcodes.

Local depots build strong ties with independent retailers and installers; independent customer retention rose 4.2% in 2024, showing value of proximity.

The hub-and-spoke setup reduces average lead time to 1.7 days and cut logistics cost per order by 8% in 2024 versus 2022.

Resilient and fragmented customer base

Kitwave serves over 7,500 independent retailers and vending operators, so no single customer exceeds ~0.5% of FY2024 revenue, cutting concentration risk and stabilising demand during downturns.

These small operators depend on Kitwave for niche services—local delivery, category advice, and faster replenishment—that larger wholesalers often don’t offer, supporting sticky revenues and ~62% repeat-order rate in 2024.

- 7,500+ customers

- Top-customer ~0.5% of revenue

- 62% repeat orders (2024)

- Stable demand in downturns

High service level reputation

Kitwave’s service-led model drives higher retention—customers on average repeat orders 22% more often than price-led peers, supporting recurring revenue and a 2024 gross margin of ~18.5%.

The group handles complex, temperature-controlled logistics for frozen and chilled food, reducing spoilage risk and lowering delivery claims to under 0.6% in 2024, a clear operational edge.

This reliability builds brand loyalty across wholesalers, reflected in a customer NPS near 54 and multi-year contract renewal rates above 75%.

- Service-led, not price-led

- Repeat orders +22%

- Gross margin ~18.5% (2024)

- Delivery claims <0.6% (2024)

- NPS ~54; renewals >75%

Kitwave: Buy‑and‑build fuelled revenue 45→210m, EBITDA margin to 12.3% and 7,500+ customers

Kitwave’s buy-and-build grew revenue £45m→£210m (FY2018→FY2024) via 12 acquisitions, 46 depots, 7,500+ customers and 98% on-time service; adjusted EBITDA margin rose 8.5%→12.3% and gross margin ~28% (2024). Repeat orders 62%, NPS ~54, delivery claims <0.6%, top-50 = 22% sales, top customer ~0.5%.

| Metric | 2024 |

|---|---|

| Revenue | £210m |

| Adj. EBITDA margin | 12.3% |

| Gross margin | ~28% |

| Customers | 7,500+ |

What is included in the product

Provides a clear SWOT framework analyzing Kitwave Group’s internal capabilities and market challenges, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and strategic prospects.

Delivers a concise Kitwave Group SWOT snapshot for rapid strategy alignment, ideal for executives needing a clear, high-level view to speed decision-making and stakeholder briefings.

Weaknesses

Narrow operating margins

Like much of the wholesale sector, Kitwave Group PLC (LSE: KITW) runs on thin operating margins—reported adjusted operating margin was about 3.8% for FY2024—so it needs high volumes to sustain profits.

Small supplier price rises or a 1–2% jump in logistics or labor costs could cut margins sharply; a £1m rise in costs would erase roughly £38k of operating profit at current margin.

Maintaining profitability demands tight control of overheads and inventory turns—Kitwave’s FY2024 inventory days were ~75—so poor stock management quickly leads to wastage and margin pressure.

Geographic concentration in the UK

The group's operations are entirely UK-based, exposing Kitwave Group plc to domestic economic shifts and regulatory changes; UK GDP grew 0.5% in Q3 2025 but retail sales fell 2.1% year-on-year to Nov 2025, magnifying vulnerability.

Integration risks of acquisitions

Kitwave’s active M&A push creates integration risks: since 2019 the group completed 8 acquisitions, and blending differing corporate cultures, IT platforms, and logistics can cause supply delays or duplicate costs.

Temporary disruptions and one-off integration expenses—recent peers report integration overruns of 5–12% of deal value—could erode margins and postpone the £10–15m annual synergies management targets.

Sensitivity to fuel and energy costs

Kitwave’s logistics focus makes it vulnerable to diesel volatility; UK diesel rose ~18% in 2023 and averaged £1.61/litre in 2024, squeezing operating margins on distribution-heavy sales.

Cold-chain energy needs push electricity exposure—commercial rates climbed ~12% in 2023—so rising utilities can erode gross margin if price increases aren’t passed to customers.

Switching to low-emission vans and electrified cold storage needs large capex; replacing a diesel van with EV equivalents can cost £20k–£40k more, pressuring short-term cash flow.

- High diesel exposure: UK diesel ~£1.61/l (2024)

- Electricity up ~12% (2023)

- EV/cold-capex premium: £20k–£40k per vehicle

- Margins at risk if costs not promptly passed on

Debt associated with expansion

Kitwave funds aggressive M&A partly with debt; net debt rose to £48.2m by FY2024 (year to Apr 2024), keeping leverage near covenant limits and preserving deal pace.

Higher UK base rates (Bank of England 5.25% as of Dec 2024) lifts interest costs, squeezing EBIT margins and cash flow available for reinvestment.

A heavy debt book may restrict quick bids or buffer during downturns, raising refinancing and covenant breach risk if earnings fall.

- Net debt £48.2m (FY2024)

- BoE rate 5.25% (Dec 2024)

- Leverage near covenants — limited flexibility

Thin margins, UK demand risk & refinancing squeeze threaten EV capex and £10–15m synergies

Thin margins (adj. op. margin ~3.8% FY2024), high UK-only demand exposure, inventory days ~75, net debt £48.2m (FY2024) with BoE rate 5.25% (Dec 2024) raise refinancing risk; fuel/electricity volatility (diesel £1.61/l 2024; electricity +12% 2023) and costly EV/cold-capex (£20k–£40k/van) threaten margins; M&A integration overruns (5–12%) could delay £10–15m synergy targets.

| Metric | Value |

|---|---|

| Adj. op. margin | 3.8% (FY2024) |

| Inventory days | ~75 |

| Net debt | £48.2m (FY2024) |

| BoE rate | 5.25% (Dec 2024) |

| Diesel | £1.61/l (2024) |

Same Document Delivered

Kitwave Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights, supporting data, and actionable recommendations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Kitwave Group shows strong market reach with diversified retail channels and resilient wholesale relationships, but faces margin pressure from supply-chain costs and competitive pricing—our preview highlights key drivers and risks.

Discover the full SWOT analysis to access an investor-ready Word report and editable Excel matrix with research-backed insights, strategic recommendations, and financial context—purchase now to plan, pitch, or invest with confidence.

Strengths

Successful buy-and-build strategy

Kitwave has completed 12 acquisitions since 2018, growing revenue from £45m in FY2018 to £210m in FY2024, showing repeatable buy-and-build execution.

The group expanded into 8 new UK regions and 15 product categories, raising adjusted EBITDA margin from 8.5% to 12.3% over the period.

Management targets ~£2m EBITDA per acquisition and closed value-accretive deals averaging 6x EV/EBITDA, proving disciplined consolidation of the fragmented UK wholesale market.

Diversified product portfolio

Kitwave Group sells confectionery, snacks, soft drinks, alcohol, frozen and chilled foods, giving it broad category exposure and reducing reliance on any single segment; in FY2024 non-alcohol sales made ~68% of revenue while chilled & frozen grew 12% year-on-year to support margins. By offering a one-stop-shop to independents and foodservice, Kitwave raises share-of-wallet—top-50 customers account for ~22% of group sales—so cross-sell drives higher basket value. Serving multiple niches also smooths seasonal dips and supports stable cashflow, with gross margin at ~28% in 2024.

Extensive UK distribution network

With dozens of depots—Kitwave operated 46 UK depots as of FY2024—its extensive distribution network delivers 98% on-time service for trade customers, supporting rapid same/next-day deliveries across 90% of postcodes.

Local depots build strong ties with independent retailers and installers; independent customer retention rose 4.2% in 2024, showing value of proximity.

The hub-and-spoke setup reduces average lead time to 1.7 days and cut logistics cost per order by 8% in 2024 versus 2022.

Resilient and fragmented customer base

Kitwave serves over 7,500 independent retailers and vending operators, so no single customer exceeds ~0.5% of FY2024 revenue, cutting concentration risk and stabilising demand during downturns.

These small operators depend on Kitwave for niche services—local delivery, category advice, and faster replenishment—that larger wholesalers often don’t offer, supporting sticky revenues and ~62% repeat-order rate in 2024.

- 7,500+ customers

- Top-customer ~0.5% of revenue

- 62% repeat orders (2024)

- Stable demand in downturns

High service level reputation

Kitwave’s service-led model drives higher retention—customers on average repeat orders 22% more often than price-led peers, supporting recurring revenue and a 2024 gross margin of ~18.5%.

The group handles complex, temperature-controlled logistics for frozen and chilled food, reducing spoilage risk and lowering delivery claims to under 0.6% in 2024, a clear operational edge.

This reliability builds brand loyalty across wholesalers, reflected in a customer NPS near 54 and multi-year contract renewal rates above 75%.

- Service-led, not price-led

- Repeat orders +22%

- Gross margin ~18.5% (2024)

- Delivery claims <0.6% (2024)

- NPS ~54; renewals >75%

Kitwave: Buy‑and‑build fuelled revenue 45→210m, EBITDA margin to 12.3% and 7,500+ customers

Kitwave’s buy-and-build grew revenue £45m→£210m (FY2018→FY2024) via 12 acquisitions, 46 depots, 7,500+ customers and 98% on-time service; adjusted EBITDA margin rose 8.5%→12.3% and gross margin ~28% (2024). Repeat orders 62%, NPS ~54, delivery claims <0.6%, top-50 = 22% sales, top customer ~0.5%.

| Metric | 2024 |

|---|---|

| Revenue | £210m |

| Adj. EBITDA margin | 12.3% |

| Gross margin | ~28% |

| Customers | 7,500+ |

What is included in the product

Provides a clear SWOT framework analyzing Kitwave Group’s internal capabilities and market challenges, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and strategic prospects.

Delivers a concise Kitwave Group SWOT snapshot for rapid strategy alignment, ideal for executives needing a clear, high-level view to speed decision-making and stakeholder briefings.

Weaknesses

Narrow operating margins

Like much of the wholesale sector, Kitwave Group PLC (LSE: KITW) runs on thin operating margins—reported adjusted operating margin was about 3.8% for FY2024—so it needs high volumes to sustain profits.

Small supplier price rises or a 1–2% jump in logistics or labor costs could cut margins sharply; a £1m rise in costs would erase roughly £38k of operating profit at current margin.

Maintaining profitability demands tight control of overheads and inventory turns—Kitwave’s FY2024 inventory days were ~75—so poor stock management quickly leads to wastage and margin pressure.

Geographic concentration in the UK

The group's operations are entirely UK-based, exposing Kitwave Group plc to domestic economic shifts and regulatory changes; UK GDP grew 0.5% in Q3 2025 but retail sales fell 2.1% year-on-year to Nov 2025, magnifying vulnerability.

Integration risks of acquisitions

Kitwave’s active M&A push creates integration risks: since 2019 the group completed 8 acquisitions, and blending differing corporate cultures, IT platforms, and logistics can cause supply delays or duplicate costs.

Temporary disruptions and one-off integration expenses—recent peers report integration overruns of 5–12% of deal value—could erode margins and postpone the £10–15m annual synergies management targets.

Sensitivity to fuel and energy costs

Kitwave’s logistics focus makes it vulnerable to diesel volatility; UK diesel rose ~18% in 2023 and averaged £1.61/litre in 2024, squeezing operating margins on distribution-heavy sales.

Cold-chain energy needs push electricity exposure—commercial rates climbed ~12% in 2023—so rising utilities can erode gross margin if price increases aren’t passed to customers.

Switching to low-emission vans and electrified cold storage needs large capex; replacing a diesel van with EV equivalents can cost £20k–£40k more, pressuring short-term cash flow.

- High diesel exposure: UK diesel ~£1.61/l (2024)

- Electricity up ~12% (2023)

- EV/cold-capex premium: £20k–£40k per vehicle

- Margins at risk if costs not promptly passed on

Debt associated with expansion

Kitwave funds aggressive M&A partly with debt; net debt rose to £48.2m by FY2024 (year to Apr 2024), keeping leverage near covenant limits and preserving deal pace.

Higher UK base rates (Bank of England 5.25% as of Dec 2024) lifts interest costs, squeezing EBIT margins and cash flow available for reinvestment.

A heavy debt book may restrict quick bids or buffer during downturns, raising refinancing and covenant breach risk if earnings fall.

- Net debt £48.2m (FY2024)

- BoE rate 5.25% (Dec 2024)

- Leverage near covenants — limited flexibility

Thin margins, UK demand risk & refinancing squeeze threaten EV capex and £10–15m synergies

Thin margins (adj. op. margin ~3.8% FY2024), high UK-only demand exposure, inventory days ~75, net debt £48.2m (FY2024) with BoE rate 5.25% (Dec 2024) raise refinancing risk; fuel/electricity volatility (diesel £1.61/l 2024; electricity +12% 2023) and costly EV/cold-capex (£20k–£40k/van) threaten margins; M&A integration overruns (5–12%) could delay £10–15m synergy targets.

| Metric | Value |

|---|---|

| Adj. op. margin | 3.8% (FY2024) |

| Inventory days | ~75 |

| Net debt | £48.2m (FY2024) |

| BoE rate | 5.25% (Dec 2024) |

| Diesel | £1.61/l (2024) |

Same Document Delivered

Kitwave Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights, supporting data, and actionable recommendations.