KITZ Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

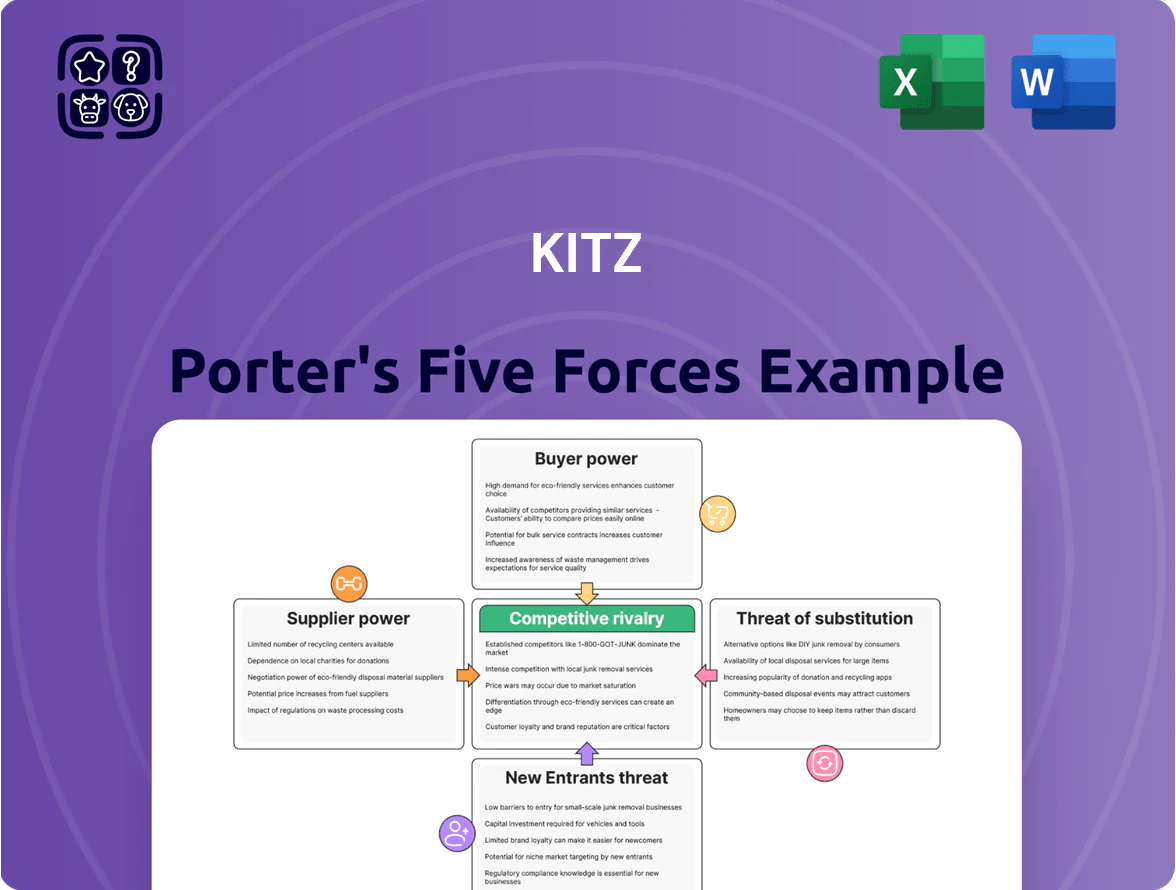

KITZ faces moderate supplier power, cost-sensitive buyers, and steady rivalry from niche valve makers, while barriers to entry and substitutes shape strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KITZ’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report for force-by-force ratings, visuals, and actionable implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Raw Material Price Volatility

The production of valves uses large volumes of copper, stainless steel, and iron, so KITZ is exposed to global commodity swings—copper rose ~35% from 2020–2024 and averaged 8% annual volatility through 2025. Suppliers of high‑grade alloys hold moderate leverage as semiconductor and hydrogen sectors demand specialty grades; such alloys saw a 12% premium in 2025. KITZ reduces supplier power via multi‑year contracts covering ~60% of purchases and its internal foundries handling ~40% of casting volume, cutting spot‑market exposure.

Energy Costs and Sustainability Requirements

Suppliers of energy-intensive inputs gained power as global carbon prices and stricter regs pushed through 2025; EU carbon permit prices averaged ~€95/ton in 2024, raising feedstock costs for KITZ. KITZ forces upstream vendors to meet strict ESG rules, shrinking the vendor pool and boosting influence of green-certified suppliers (e.g., ISO 14001, SBTi-aligned), so KITZ saw input cost increases of about 4–6% in 2024 while pursuing its 2030 decarbonization targets.

Specialized Component Scarcity

The shift to automated smart valves raises KITZ’s dependence on electronic actuators and precision sensors, components with limited second sources; suppliers for these parts hold stronger bargaining power, raising input-cost volatility. KITZ reported 18% of FY2024 capex tied to digital upgrades and cites a 30% supplier-concentration ratio for sensors in its 2024 report. KITZ offsets risk with 4–12 week inventory buffers and multi-source contracts across Japan, Taiwan, and Malaysia.

Geopolitical Influence on Sourcing

Regional export limits on critical minerals, like 2024 rare-earth export controls from China that accounted for ~60% of global supply, boost supplier leverage; KITZ faces higher costs and supply risk when these producers tighten exports.

Asia and North America impose local content rules—Canada’s 2023 Critical Minerals List incentives raised domestic sourcing by ~15%—forcing KITZ to favor compliant suppliers, narrowing options.

When geopolitical tension spikes, concentrated suppliers can demand price premiums; spot prices for copper rose 28% in H1 2024 during supply disruptions, showing leverage effects KITZ must manage.

- China ~60% rare-earth supply (2024)

- Canada domestic sourcing +15% (2023 incentives)

- Copper spot +28% H1 2024 during disruptions

Supplier Integration Trends

Supplier integration into downstream assembly is rising; global valve-component makers expanded OEM assembly by ~18% 2024–25, which could raise supplier bargaining power.

KITZ’s 2025 revenues of ¥154.2 billion and shipments to 90+ countries keep it a high-volume, prestigious partner that limits supplier price leverage.

KITZ offsets pressure via technical collaborations—joint R&D and proprietary material co-development reduced input costs by ~3.5% in 2024.

- Supplier downstream move +18% (2024–25)

- KITZ revenue ¥154.2B (2025)

- Global reach 90+ countries

- Input cost cut ~3.5% via co‑development (2024)

KITZ navigates supplier power—commodity spikes vs. 60% contracts, 40% in‑house casting

Suppliers hold moderate to high power: commodity swings (copper +35% 2020–24; 28% spike H1 2024), rare-earth concentration (China ~60% 2024), and sensor/vendor concentration (30% supplier share FY2024) raise costs and risk, while KITZ’s ¥154.2B 2025 revenue, multi‑year contracts (~60% purchases) and 40% in‑house casting reduce leverage; co‑development cut inputs ~3.5% (2024).

| Metric | Value |

|---|---|

| Copper 2020–24 | +35% |

| Rare‑earth China (2024) | ~60% |

| Sensor supplier share (2024) | 30% |

| KITZ revenue (2025) | ¥154.2B |

| Multi‑yr contracts | ~60% purchases |

| In‑house casting | 40% |

| Input cost cut (co‑dev) | ~3.5% (2024) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes, and entry barriers tailored to KITZ, highlighting disruptive forces and strategic implications for pricing, margins, and market share.

Compact Porter's Five Forces template tailored for KITZ—quickly pinpoint competitive pressures and relieve decision-making friction with an at-a-glance summary, editable pressure levels, and a ready-to-use radar chart for presentations.

Customers Bargaining Power

Consolidation of Major EPC Firms

Major EPC firms and oil & gas operators control buyer power over KITZ due to order scale—top 50 global EPCs accounted for ~45% of project spend in 2024, forcing volume discounts and tighter margins.

They demand customization and strict schedules, raising KITZ’s engineering and warranty costs and compressing EBITDA by an estimated 200–400 basis points on large contracts.

By end-2025 more buyers use digital procurement platforms; 62% of upstream buyers compare global valve pricing in real time, boosting price transparency and negotiation leverage.

Price Sensitivity in Commercial Markets

In commercial and residential construction valves are largely seen as commodities, so KITZ faces high buyer price sensitivity—industry procurement data shows specification-driven projects still award 35–45% of contracts to lower-cost regional brands in 2024.

Buyers switch quickly if the price-to-performance ratio is unclear, pressuring KITZ margins; in 2023 KITZ reported product gross margins around mid-30s% and cites competitive pricing as a key risk.

KITZ counters by promoting reliability and lower total cost of ownership (TCO); field studies indicate mean failure-related maintenance cost reductions of 20–30% over 10 years versus cheaper alternatives.

High Switching Costs in Specialized Industries

Customers in semiconductors and specialty chemicals face high switching costs because fluid control failures can halt fabs or contaminate batches, where a single downtime hour can cost semiconductor fabs up to $1–2 million (2024 estimates), so cheaper valves offer little appeal.

KITZ reduces customer bargaining power by embedding valves into process designs, signing multi-year service contracts (often 3–7 years) and capturing recurring revenue—service can represent 10–20% of lifecycle income.

Demand for Integrated Digital Solutions

- 68% of buyers prefer integrated solutions (IDC 2024)

- KITZ solution revenue +14% in 2023

- Bundling increases switching costs, lowers price pressure

Access to Global Alternatives

The transparency of global markets lets KITZ customers quickly find and vet alternative valve makers in emerging economies; 2024 import data shows Asian suppliers grew valve export share to 38% versus Japan’s 29%.

This reduced information asymmetry erodes KITZ’s legacy pricing power, so KITZ must keep innovating and hit ISO 9001/ASME quality targets to avoid churn to lower-cost rivals offering 15–30% cheaper quotes.

Failure to match cost or tech upgrades risks volume declines; KITZ reported a 4.2% domestic valve shipment drop in FY2023, showing the stakes.

- Global valve exports: Asia 38% (2024)

- Japan share: 29% (2024)

- Price gap: competitors 15–30% lower

- KITZ FY2023 domestic shipment decline: 4.2%

KITZ margins pressured by big EPCs, offsets via solutions (+14%) and lifecycle services

Large EPCs and O&G buyers wield high bargaining power—top 50 EPCs were ~45% of project spend in 2024—forcing discounts and compressing KITZ EBITDA ~200–400 bps on big jobs. Digital procurement (62% of upstream buyers, 2025) and Asian exporters rising to 38% of valve exports (2024) boost price transparency. KITZ counters with Fluidic Solutions (+14% solution revenue in 2023) and multi-year service (10–20% lifecycle income).

| Metric | Value |

|---|---|

| Top-50 EPC share (2024) | ~45% |

| Upstream digital procurement (2025) | 62% |

| Asian valve exports (2024) | 38% |

| KITZ solution rev growth (2023) | +14% |

| Service lifecycle income | 10–20% |

Full Version Awaits

KITZ Porter's Five Forces Analysis

This preview shows the exact KITZ Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KITZ faces moderate supplier power, cost-sensitive buyers, and steady rivalry from niche valve makers, while barriers to entry and substitutes shape strategic positioning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KITZ’s competitive dynamics, market pressures, and strategic advantages in detail.

Get the complete, consultant-grade report for force-by-force ratings, visuals, and actionable implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Raw Material Price Volatility

The production of valves uses large volumes of copper, stainless steel, and iron, so KITZ is exposed to global commodity swings—copper rose ~35% from 2020–2024 and averaged 8% annual volatility through 2025. Suppliers of high‑grade alloys hold moderate leverage as semiconductor and hydrogen sectors demand specialty grades; such alloys saw a 12% premium in 2025. KITZ reduces supplier power via multi‑year contracts covering ~60% of purchases and its internal foundries handling ~40% of casting volume, cutting spot‑market exposure.

Energy Costs and Sustainability Requirements

Suppliers of energy-intensive inputs gained power as global carbon prices and stricter regs pushed through 2025; EU carbon permit prices averaged ~€95/ton in 2024, raising feedstock costs for KITZ. KITZ forces upstream vendors to meet strict ESG rules, shrinking the vendor pool and boosting influence of green-certified suppliers (e.g., ISO 14001, SBTi-aligned), so KITZ saw input cost increases of about 4–6% in 2024 while pursuing its 2030 decarbonization targets.

Specialized Component Scarcity

The shift to automated smart valves raises KITZ’s dependence on electronic actuators and precision sensors, components with limited second sources; suppliers for these parts hold stronger bargaining power, raising input-cost volatility. KITZ reported 18% of FY2024 capex tied to digital upgrades and cites a 30% supplier-concentration ratio for sensors in its 2024 report. KITZ offsets risk with 4–12 week inventory buffers and multi-source contracts across Japan, Taiwan, and Malaysia.

Geopolitical Influence on Sourcing

Regional export limits on critical minerals, like 2024 rare-earth export controls from China that accounted for ~60% of global supply, boost supplier leverage; KITZ faces higher costs and supply risk when these producers tighten exports.

Asia and North America impose local content rules—Canada’s 2023 Critical Minerals List incentives raised domestic sourcing by ~15%—forcing KITZ to favor compliant suppliers, narrowing options.

When geopolitical tension spikes, concentrated suppliers can demand price premiums; spot prices for copper rose 28% in H1 2024 during supply disruptions, showing leverage effects KITZ must manage.

- China ~60% rare-earth supply (2024)

- Canada domestic sourcing +15% (2023 incentives)

- Copper spot +28% H1 2024 during disruptions

Supplier Integration Trends

Supplier integration into downstream assembly is rising; global valve-component makers expanded OEM assembly by ~18% 2024–25, which could raise supplier bargaining power.

KITZ’s 2025 revenues of ¥154.2 billion and shipments to 90+ countries keep it a high-volume, prestigious partner that limits supplier price leverage.

KITZ offsets pressure via technical collaborations—joint R&D and proprietary material co-development reduced input costs by ~3.5% in 2024.

- Supplier downstream move +18% (2024–25)

- KITZ revenue ¥154.2B (2025)

- Global reach 90+ countries

- Input cost cut ~3.5% via co‑development (2024)

KITZ navigates supplier power—commodity spikes vs. 60% contracts, 40% in‑house casting

Suppliers hold moderate to high power: commodity swings (copper +35% 2020–24; 28% spike H1 2024), rare-earth concentration (China ~60% 2024), and sensor/vendor concentration (30% supplier share FY2024) raise costs and risk, while KITZ’s ¥154.2B 2025 revenue, multi‑year contracts (~60% purchases) and 40% in‑house casting reduce leverage; co‑development cut inputs ~3.5% (2024).

| Metric | Value |

|---|---|

| Copper 2020–24 | +35% |

| Rare‑earth China (2024) | ~60% |

| Sensor supplier share (2024) | 30% |

| KITZ revenue (2025) | ¥154.2B |

| Multi‑yr contracts | ~60% purchases |

| In‑house casting | 40% |

| Input cost cut (co‑dev) | ~3.5% (2024) |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes, and entry barriers tailored to KITZ, highlighting disruptive forces and strategic implications for pricing, margins, and market share.

Compact Porter's Five Forces template tailored for KITZ—quickly pinpoint competitive pressures and relieve decision-making friction with an at-a-glance summary, editable pressure levels, and a ready-to-use radar chart for presentations.

Customers Bargaining Power

Consolidation of Major EPC Firms

Major EPC firms and oil & gas operators control buyer power over KITZ due to order scale—top 50 global EPCs accounted for ~45% of project spend in 2024, forcing volume discounts and tighter margins.

They demand customization and strict schedules, raising KITZ’s engineering and warranty costs and compressing EBITDA by an estimated 200–400 basis points on large contracts.

By end-2025 more buyers use digital procurement platforms; 62% of upstream buyers compare global valve pricing in real time, boosting price transparency and negotiation leverage.

Price Sensitivity in Commercial Markets

In commercial and residential construction valves are largely seen as commodities, so KITZ faces high buyer price sensitivity—industry procurement data shows specification-driven projects still award 35–45% of contracts to lower-cost regional brands in 2024.

Buyers switch quickly if the price-to-performance ratio is unclear, pressuring KITZ margins; in 2023 KITZ reported product gross margins around mid-30s% and cites competitive pricing as a key risk.

KITZ counters by promoting reliability and lower total cost of ownership (TCO); field studies indicate mean failure-related maintenance cost reductions of 20–30% over 10 years versus cheaper alternatives.

High Switching Costs in Specialized Industries

Customers in semiconductors and specialty chemicals face high switching costs because fluid control failures can halt fabs or contaminate batches, where a single downtime hour can cost semiconductor fabs up to $1–2 million (2024 estimates), so cheaper valves offer little appeal.

KITZ reduces customer bargaining power by embedding valves into process designs, signing multi-year service contracts (often 3–7 years) and capturing recurring revenue—service can represent 10–20% of lifecycle income.

Demand for Integrated Digital Solutions

- 68% of buyers prefer integrated solutions (IDC 2024)

- KITZ solution revenue +14% in 2023

- Bundling increases switching costs, lowers price pressure

Access to Global Alternatives

The transparency of global markets lets KITZ customers quickly find and vet alternative valve makers in emerging economies; 2024 import data shows Asian suppliers grew valve export share to 38% versus Japan’s 29%.

This reduced information asymmetry erodes KITZ’s legacy pricing power, so KITZ must keep innovating and hit ISO 9001/ASME quality targets to avoid churn to lower-cost rivals offering 15–30% cheaper quotes.

Failure to match cost or tech upgrades risks volume declines; KITZ reported a 4.2% domestic valve shipment drop in FY2023, showing the stakes.

- Global valve exports: Asia 38% (2024)

- Japan share: 29% (2024)

- Price gap: competitors 15–30% lower

- KITZ FY2023 domestic shipment decline: 4.2%

KITZ margins pressured by big EPCs, offsets via solutions (+14%) and lifecycle services

Large EPCs and O&G buyers wield high bargaining power—top 50 EPCs were ~45% of project spend in 2024—forcing discounts and compressing KITZ EBITDA ~200–400 bps on big jobs. Digital procurement (62% of upstream buyers, 2025) and Asian exporters rising to 38% of valve exports (2024) boost price transparency. KITZ counters with Fluidic Solutions (+14% solution revenue in 2023) and multi-year service (10–20% lifecycle income).

| Metric | Value |

|---|---|

| Top-50 EPC share (2024) | ~45% |

| Upstream digital procurement (2025) | 62% |

| Asian valve exports (2024) | 38% |

| KITZ solution rev growth (2023) | +14% |

| Service lifecycle income | 10–20% |

Full Version Awaits

KITZ Porter's Five Forces Analysis

This preview shows the exact KITZ Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download and use the moment you buy.