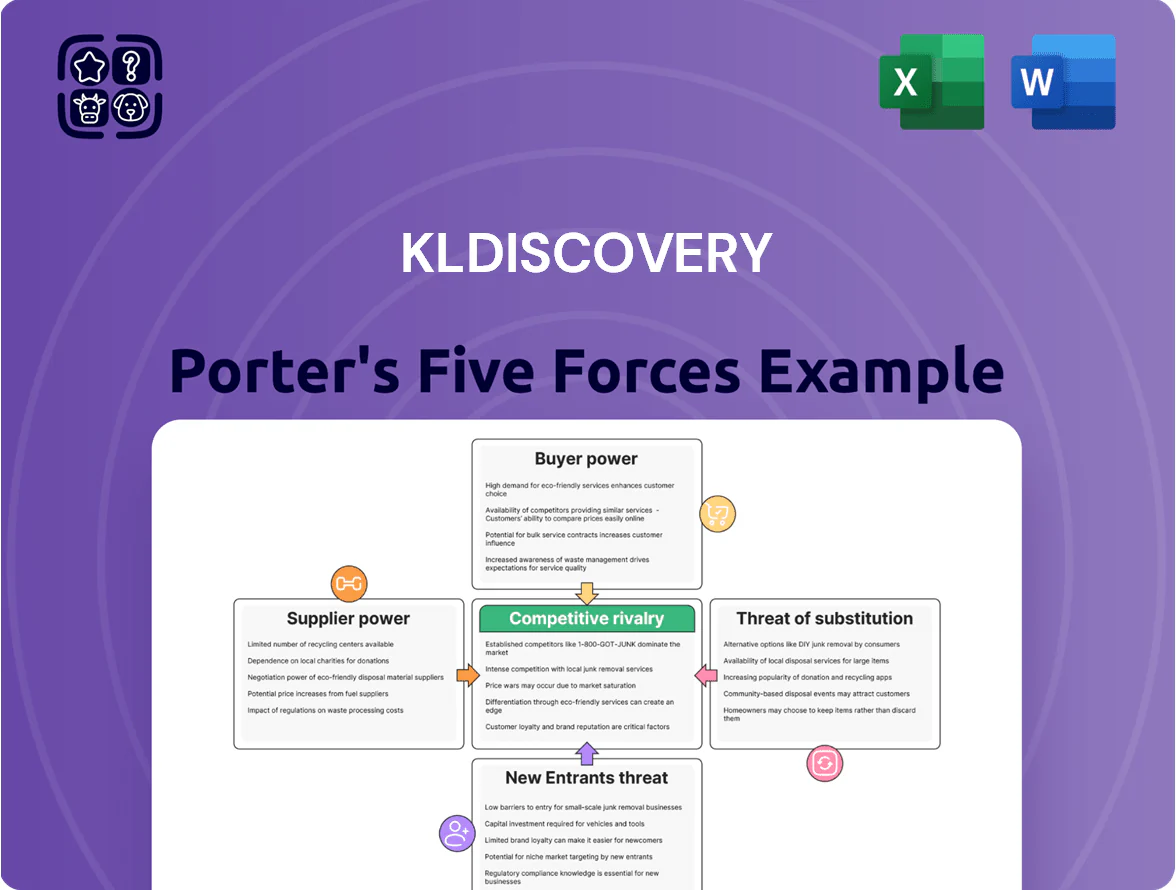

KLDiscovery Porter's Five Forces Analysis

From Overview to Strategy Blueprint

KLDiscovery faces intense competitive rivalry driven by specialized legal tech rivals and pricing pressure from larger e-discovery platforms, while moderate supplier leverage and growing client sophistication shape service demands.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KLDiscovery’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of cloud infrastructure providers

KLDiscovery depends on AWS and Microsoft Azure for core hosting; AWS had 32% and Azure 23% global IaaS/PaaS share in 2024, concentrating supplier power and raising switching costs for petabyte-scale legal archives.

Migrating terabytes of encrypted client data can cost tens of millions and months of downtime, so any 2025 price hikes or SLA changes by these providers would directly squeeze KLDiscovery’s gross margins and COGS.

Dependence on specialized forensic hardware vendors

KLDiscovery relies on niche forensic hardware makers for tools that recover damaged or encrypted media; only about 3–5 major vendors globally supply high-end imagers and write-blockers, giving suppliers strong pricing and lead-time power.

Suppliers often set 20–40% margins on specialized gear and lead times stretched to 8–16 weeks in 2024, so procurement delays can jeopardize KLDiscovery’s ability to meet court-ordered deadlines and risk client penalties.

Scarcity of elite cybersecurity and forensic talent

The pool of professionals skilled in both legal eDiscovery procedures and advanced data forensics is tiny—industry surveys in 2025 show a 22% year-over-year shortage for certified digital forensics analysts in the US. These experts form a critical supplier group and command premium pay; median total compensation for senior eDiscovery/forensics roles reached about $185,000 in 2024. Their scarcity and high mobility give individual specialists strong leverage to demand higher wages and flexible contracts, raising KLDiscovery’s labor costs and retention risk.

Licensing of third party legal review software

KLDiscovery uses proprietary Nebula and also supports Relativity to match client needs, but Relativity and similar vendors set licensing fees and push feature updates that affect project margins; Relativity held ~30% e-discovery market share in 2024 and license costs can be 10–25% of platform-related project budgets.

This dual-track model reduces full dependence on one stack but keeps KLDiscovery partially subject to external vendors’ pricing and roadmap choices, which can shift cost structure and service timelines.

- Supports Nebula plus Relativity

- Relativity ≈30% market share (2024)

- Licensing = 10–25% of platform project costs

- Partial dependence on external roadmaps and fees

Energy and utility costs for physical data centers

For KLDiscovery’s proprietary data centers, electricity and cooling are non-negotiable inputs; global energy prices rose ~15% in 2023–2024 and carbon taxes rolled out in several jurisdictions by late 2025, boosting supplier leverage.

These higher utility costs hit margins and are hard to pass through in competitive bids for long-term storage, where customers demand fixed pricing and vendors risk margin compression.

- Electricity +15% (2023–24)

- Carbon taxes implemented by late 2025

- Cooling drives ~30% of data center OPEX

- Limited pass-through in long-term contracts

Supplier Concentration Drives Costs: Cloud, Relativity, Hardware & Talent Squeeze

Suppliers exert strong leverage: AWS (32%) and Azure (23%) IaaS/PaaS share (2024) raise switching costs for petabyte archives; Relativity ~30% e-discovery share (2024) adds 10–25% licensing pressure; 3–5 major forensic hardware vendors with 20–40% margins and 8–16 week lead times; senior forensics pay median $185,000 (2024), with a 22% US shortage (2025).

| Supplier | Key Metric | 2024–25 Data |

|---|---|---|

| AWS/Azure | IaaS/PaaS share | AWS 32% / Azure 23% (2024) |

| Relativity | e-discovery share / licensing | ~30% / 10–25% project costs (2024) |

| Forensic hardware | Vendors / margins / lead time | 3–5 vendors / 20–40% margins / 8–16 weeks (2024) |

| Talent | Shortage / pay | 22% shortage (US, 2025) / $185,000 median (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for KLDiscovery that uncovers competitive drivers, assesses supplier and buyer power, evaluates entry barriers and substitutes, and highlights disruptive threats and strategic opportunities to inform investor materials and internal strategy.

KLDiscovery Porter's Five Forces condensed into a one-sheet—quickly identify litigation services' competitive pressures and make faster, data-driven decisions.

Customers Bargaining Power

Concentration of large law firm and corporate clients

A significant share of KLDiscovery’s revenue—about 35–45% in 2024 per company filings—comes from a small set of elite law firms and Fortune 500 legal departments, giving those clients strong bargaining power. Their high-volume workflows enable them to demand steep discounts and bespoke SLAs, often pushing margins down by several percentage points. When large portfolios shift at renewal or bid, KLDiscovery faces acute pricing pressure and churn risk.

Low switching costs between top tier providers

While migrating active litigation datasets is costly, clients can and do shift new matters quickly—industry surveys show 42% of corporate legal teams moved new eDiscovery work in 2024 after pricing or SLAs missed targets—because standardized workflows let legal departments run multiple top-tier vendors in parallel and pit them for price; this keeps KLDiscovery under continuous pressure to show value and hold competitive pricing to avoid churn.

Increasing price transparency and procurement involvement

Corporate legal departments now embed procurement teams that benchmark eDiscovery bids and run reverse auctions, cutting vendor margins; in 2024 procurement-driven deals accounted for an estimated 45% of enterprise eDiscovery contracts, per industry surveys.

Demand for all inclusive and subscription based pricing

By 2025 customers favor flat-fee and subscription models over per-GB pricing, shifting volume risk to providers like KLDiscovery and pressuring margins as e-discovery volumes rose ~18% CAGR 2020–24 per industry reports.

Clients now set fixed budgets and demand predictable costs, forcing KLDiscovery to improve internal efficiency—automation and cloud optimization cut processing costs 10–25% in 2024 pilots.

- Customers set pricing terms

- Providers absorb data-volume risk

- 18% CAGR data growth 2020–24

- 10–25% cost reduction via automation

Sophistication of internal corporate legal operations

Large corporations now employ legal operations teams skilled in eDiscovery workflows and platforms; by 2024, 62% of Fortune 500 firms reported formal legal ops functions, raising buyer sophistication and price pressure.

These teams unbundle services—keeping review and early case assessment in-house and outsourcing complex forensics—forcing vendors like KLDiscovery to compete on integration, automation, and per-matter pricing.

Buyers leverage benchmarks and RFPs to push for API connectivity, SLAs, and discounts; enterprises seeking cost predictability can cut vendor spend by 10–30% through in-house handling.

- Sophisticated buyers: 62% Fortune 500 with legal ops (2024)

- Unbundling: in-house review, outsource forensics

- Vendor demands: API integration, automation, strict SLAs

- Cost impact: 10–30% vendor spend reduction

Large clients squeeze margins—KLDiscovery cuts costs, automates to survive eDiscovery shift

Large clients (35–45% revenue in 2024) exert strong bargaining power, driving discounts, bespoke SLAs, and churn risk; 62% of Fortune 500 had legal ops in 2024, 42% moved new eDiscovery work after pricing/SLA misses, and buyers pushed flat-fee models as eDiscovery volumes rose ~18% CAGR 2020–24—forcing KLDiscovery to absorb volume risk and cut costs via automation (10–25% savings).

Preview the Actual Deliverable

KLDiscovery Porter's Five Forces Analysis

This preview shows the exact KLDiscovery Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the fully formatted, final file ready for download and use the moment you buy.

No mockups: this is the complete, professional analysis you’ll get instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

KLDiscovery faces intense competitive rivalry driven by specialized legal tech rivals and pricing pressure from larger e-discovery platforms, while moderate supplier leverage and growing client sophistication shape service demands.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore KLDiscovery’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of cloud infrastructure providers

KLDiscovery depends on AWS and Microsoft Azure for core hosting; AWS had 32% and Azure 23% global IaaS/PaaS share in 2024, concentrating supplier power and raising switching costs for petabyte-scale legal archives.

Migrating terabytes of encrypted client data can cost tens of millions and months of downtime, so any 2025 price hikes or SLA changes by these providers would directly squeeze KLDiscovery’s gross margins and COGS.

Dependence on specialized forensic hardware vendors

KLDiscovery relies on niche forensic hardware makers for tools that recover damaged or encrypted media; only about 3–5 major vendors globally supply high-end imagers and write-blockers, giving suppliers strong pricing and lead-time power.

Suppliers often set 20–40% margins on specialized gear and lead times stretched to 8–16 weeks in 2024, so procurement delays can jeopardize KLDiscovery’s ability to meet court-ordered deadlines and risk client penalties.

Scarcity of elite cybersecurity and forensic talent

The pool of professionals skilled in both legal eDiscovery procedures and advanced data forensics is tiny—industry surveys in 2025 show a 22% year-over-year shortage for certified digital forensics analysts in the US. These experts form a critical supplier group and command premium pay; median total compensation for senior eDiscovery/forensics roles reached about $185,000 in 2024. Their scarcity and high mobility give individual specialists strong leverage to demand higher wages and flexible contracts, raising KLDiscovery’s labor costs and retention risk.

Licensing of third party legal review software

KLDiscovery uses proprietary Nebula and also supports Relativity to match client needs, but Relativity and similar vendors set licensing fees and push feature updates that affect project margins; Relativity held ~30% e-discovery market share in 2024 and license costs can be 10–25% of platform-related project budgets.

This dual-track model reduces full dependence on one stack but keeps KLDiscovery partially subject to external vendors’ pricing and roadmap choices, which can shift cost structure and service timelines.

- Supports Nebula plus Relativity

- Relativity ≈30% market share (2024)

- Licensing = 10–25% of platform project costs

- Partial dependence on external roadmaps and fees

Energy and utility costs for physical data centers

For KLDiscovery’s proprietary data centers, electricity and cooling are non-negotiable inputs; global energy prices rose ~15% in 2023–2024 and carbon taxes rolled out in several jurisdictions by late 2025, boosting supplier leverage.

These higher utility costs hit margins and are hard to pass through in competitive bids for long-term storage, where customers demand fixed pricing and vendors risk margin compression.

- Electricity +15% (2023–24)

- Carbon taxes implemented by late 2025

- Cooling drives ~30% of data center OPEX

- Limited pass-through in long-term contracts

Supplier Concentration Drives Costs: Cloud, Relativity, Hardware & Talent Squeeze

Suppliers exert strong leverage: AWS (32%) and Azure (23%) IaaS/PaaS share (2024) raise switching costs for petabyte archives; Relativity ~30% e-discovery share (2024) adds 10–25% licensing pressure; 3–5 major forensic hardware vendors with 20–40% margins and 8–16 week lead times; senior forensics pay median $185,000 (2024), with a 22% US shortage (2025).

| Supplier | Key Metric | 2024–25 Data |

|---|---|---|

| AWS/Azure | IaaS/PaaS share | AWS 32% / Azure 23% (2024) |

| Relativity | e-discovery share / licensing | ~30% / 10–25% project costs (2024) |

| Forensic hardware | Vendors / margins / lead time | 3–5 vendors / 20–40% margins / 8–16 weeks (2024) |

| Talent | Shortage / pay | 22% shortage (US, 2025) / $185,000 median (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for KLDiscovery that uncovers competitive drivers, assesses supplier and buyer power, evaluates entry barriers and substitutes, and highlights disruptive threats and strategic opportunities to inform investor materials and internal strategy.

KLDiscovery Porter's Five Forces condensed into a one-sheet—quickly identify litigation services' competitive pressures and make faster, data-driven decisions.

Customers Bargaining Power

Concentration of large law firm and corporate clients

A significant share of KLDiscovery’s revenue—about 35–45% in 2024 per company filings—comes from a small set of elite law firms and Fortune 500 legal departments, giving those clients strong bargaining power. Their high-volume workflows enable them to demand steep discounts and bespoke SLAs, often pushing margins down by several percentage points. When large portfolios shift at renewal or bid, KLDiscovery faces acute pricing pressure and churn risk.

Low switching costs between top tier providers

While migrating active litigation datasets is costly, clients can and do shift new matters quickly—industry surveys show 42% of corporate legal teams moved new eDiscovery work in 2024 after pricing or SLAs missed targets—because standardized workflows let legal departments run multiple top-tier vendors in parallel and pit them for price; this keeps KLDiscovery under continuous pressure to show value and hold competitive pricing to avoid churn.

Increasing price transparency and procurement involvement

Corporate legal departments now embed procurement teams that benchmark eDiscovery bids and run reverse auctions, cutting vendor margins; in 2024 procurement-driven deals accounted for an estimated 45% of enterprise eDiscovery contracts, per industry surveys.

Demand for all inclusive and subscription based pricing

By 2025 customers favor flat-fee and subscription models over per-GB pricing, shifting volume risk to providers like KLDiscovery and pressuring margins as e-discovery volumes rose ~18% CAGR 2020–24 per industry reports.

Clients now set fixed budgets and demand predictable costs, forcing KLDiscovery to improve internal efficiency—automation and cloud optimization cut processing costs 10–25% in 2024 pilots.

- Customers set pricing terms

- Providers absorb data-volume risk

- 18% CAGR data growth 2020–24

- 10–25% cost reduction via automation

Sophistication of internal corporate legal operations

Large corporations now employ legal operations teams skilled in eDiscovery workflows and platforms; by 2024, 62% of Fortune 500 firms reported formal legal ops functions, raising buyer sophistication and price pressure.

These teams unbundle services—keeping review and early case assessment in-house and outsourcing complex forensics—forcing vendors like KLDiscovery to compete on integration, automation, and per-matter pricing.

Buyers leverage benchmarks and RFPs to push for API connectivity, SLAs, and discounts; enterprises seeking cost predictability can cut vendor spend by 10–30% through in-house handling.

- Sophisticated buyers: 62% Fortune 500 with legal ops (2024)

- Unbundling: in-house review, outsource forensics

- Vendor demands: API integration, automation, strict SLAs

- Cost impact: 10–30% vendor spend reduction

Large clients squeeze margins—KLDiscovery cuts costs, automates to survive eDiscovery shift

Large clients (35–45% revenue in 2024) exert strong bargaining power, driving discounts, bespoke SLAs, and churn risk; 62% of Fortune 500 had legal ops in 2024, 42% moved new eDiscovery work after pricing/SLA misses, and buyers pushed flat-fee models as eDiscovery volumes rose ~18% CAGR 2020–24—forcing KLDiscovery to absorb volume risk and cut costs via automation (10–25% savings).

Preview the Actual Deliverable

KLDiscovery Porter's Five Forces Analysis

This preview shows the exact KLDiscovery Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the fully formatted, final file ready for download and use the moment you buy.

No mockups: this is the complete, professional analysis you’ll get instantly upon payment.