Kawasaki Kisen Kaisha PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

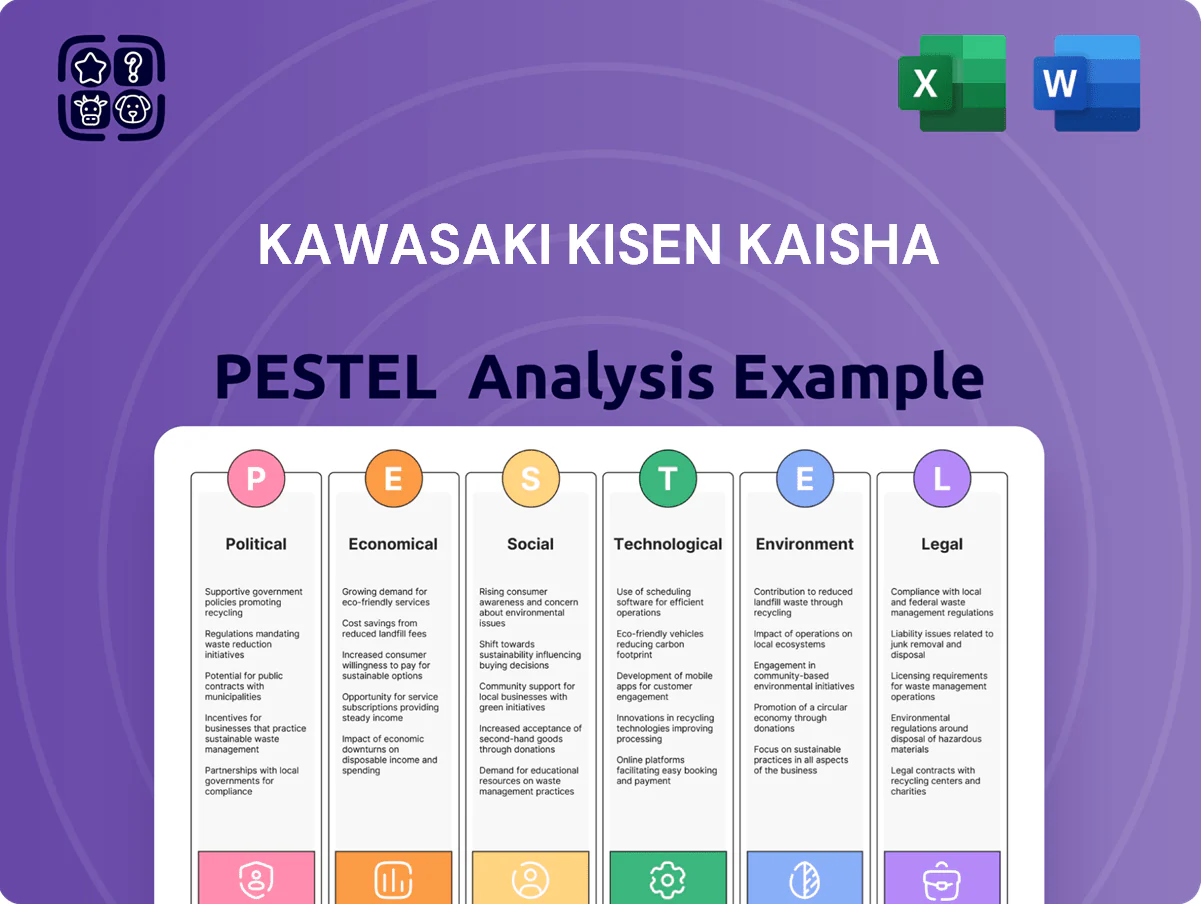

Unlock strategic clarity with our Kawasaki Kisen Kaisha PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; buy the full report for the complete, actionable breakdown and downloadable charts to support investment decisions or strategic planning.

Political factors

Geopolitical instability in trade corridors

Ongoing Middle East conflicts and South China Sea tensions have lengthened routes for K LINE, contributing to a ~7-10% rise in voyage times in 2024–25 and adding an estimated $30–45/TEU in extra fuel and rerouting costs; insurance premiums for vessels transiting high-risk corridors rose about 12% in 2025. K LINE must sustain elevated diplomatic engagement and route flexibility to contain delays and protect margins.

Trade protectionism and tariff policies

The rise of protectionist policies in the US and EU adds volatility to global trade; US tariffs rose to an average applied MFN rate of 3.5% in 2024 with several auto-sector measures raising effective duties by up to 10–25%, shrinking containerized vehicle flows.

New tariffs on autos and raw materials directly cut demand for K LINE's specialized car carriers and RO/RO services—K Line reported 2024 vehicle liftings down 6% YoY to ~1.15 million units, reflecting softer trade volumes.

Shifts in bilateral agreements and regional manufacturing relocation (nearshoring to Mexico and Southeast Asia) require K LINE to model route elasticity and adjust fleet deployment; scenario analysis should include tariff shock cases reducing volumes by 5–15% per corridor.

Japanese government maritime support

The Japanese government’s 2024 Maritime Strategy allocates ¥200 billion to fleet renewal and energy supply-chain resilience, reinforcing a pro-shipping political framework that favors domestic carriers like Kawasaki Kisen Kaisha (K LINE).

K LINE benefits from subsidies and R&D grants under the Autonomous Shipping Promotion Program, which reached ¥18.5 billion in 2025 funding for trials and technology development.

This alignment with national security and economic policies secures K LINE’s role in Japan’s merchant marine, supporting its 2024 fleet of ~430 vessels and contributing to stable long-term demand.

International sanctions and compliance

Strict enforcement of international sanctions forces K LINE to maintain rigorous legal and political screening for cargo and partners; in 2024 the company reported compliance-related costs rising to approx. JPY 14.5bn as sanction checks and vetting expanded.

Navigating global sanctions is essential to avoid fines and reputational harm that could endanger correspondent banking; shipping fines globally averaged over USD 1.2m per major breach in 2023–24.

K LINE invests heavily in compliance infrastructure, upgrading sanctions screening and AML systems to meet rapidly changing rules across jurisdictions.

- Compliance costs ~JPY 14.5bn (2024)

- Average major shipping fine ~USD 1.2m (2023–24)

- Enhanced sanctions/AML systems deployed across fleet and partners

Energy security and resource diplomacy

Kawasaki Kisen Kaisha (K LINE) transports ~10% of global LNG shipping capacity and significant crude volumes, linking it to state-led energy diplomacy; disruptions in exporters like Russia or Qatar can force route changes and surge costs—spot LNG rates spiked 300% in 2022, highlighting volatility.

Long-term charters (over 60% of fleet employment) buffer revenue but require renegotiation when political shifts alter export policies or sanctions, risking idle tonnage or early contract terminations.

- ~10% share of global LNG shipping capacity

- Over 60% fleet on long-term charters

- 2022 spot LNG rate spike ~300%

K LINE hit by geopolitical costs—voyage delays, $30–45/TEU reroutes, insurance +12%

Political risks (Middle East/South China Sea tensions, protectionism, sanctions, energy diplomacy) raised K LINE’s 2024–25 costs: voyage times +7–10%, extra fuel/reroute ~$30–45/TEU, insurance +12% (2025), compliance ~JPY14.5bn (2024); supports from Japan: ¥200bn maritime strategy, ¥18.5bn autonomous shipping funds (2025), fleet ~430 vessels, ~10% global LNG capacity.

| Metric | Value |

|---|---|

| Voyage time increase | 7–10% |

| Extra cost/TEU | $30–45 |

| Insurance rise (2025) | +12% |

| Compliance costs (2024) | JPY14.5bn |

| Japan maritime fund | ¥200bn |

| Autonomous shipping grants (2025) | ¥18.5bn |

| Fleet size (2024) | ~430 vessels |

| Global LNG share | ~10% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Kawasaki Kisen Kaisha across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategic decision-making for executives, investors, and consultants.

A concise, visually segmented Kawasaki Kisen Kaisha PESTLE summary that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning while allowing note additions for region- or business-specific context.

Economic factors

Volatility in global commodity prices

Fluctuations in iron ore, coal and grain prices drove a 12% year-on-year variance in dry bulk demand for K LINE through end-2025, with iron ore spot freight rates swinging 40% in 2025 alone. Cyclical downturns in steel and power reduced volumes, raising the company's spot-market exposure to 38% of dry-bulk liftings. K LINE offsets volatility via diversified contracts—time-charters and multi-year fixtures—covering roughly 62% of its dry-bulk capacity to 31 Dec 2025.

Currency exchange rate sensitivity

As a Yen-reporter with significant USD revenues, K Line is highly exposed to USD/JPY moves; a 10% yen depreciation in 2023 raised translated revenue by roughly JPY 50–70 billion, while dollar-denominated net debt (~USD 2.1 billion at FY2024) became costlier when USD/JPY rose above 150. Management used FX forwards, swaps and currency options covering a large portion of expected cash flows, trimming reported FX volatility despite divergent BOJ/Fed stances.

Bunker fuel and alternative energy costs

The shift from heavy fuel oil to low-sulfur fuels and LNG raised per-vessel fuel costs; scrubber-equipped ships incur capex, while 2024 global bunker average for 0.5%S was about $620/ton versus ~$420/ton for HSFO in 2020, widening operating margins pressure for K LINE.

Fuel volatility remains critical—fuel accounts for roughly 40% of voyage costs in container and bulk shipping; Brent-linked swings in 2024 saw bunker price monthly variance >25%, stressing short-term cash flows.

K LINE is cutting exposure by improving slow-steaming and hull efficiency and invested in dual-fuel LNG vessels; as of 2025 the company targets reducing fleet CO2 and fuel spend by mid-single digits annually through these measures.

Global interest rate environment

The 2025 global interest rate environment, with major central bank policy rates around 4.5–5.0% (Fed 5.25%–5.5% in late 2024; ECB ~3.75% in 2024), raises K Line's cost of capital for fleet modernization, increasing annual debt service and potentially delaying new eco-vessel orders.

K Line actively monitors monetary policy and leverages debt maturity management and hybrid financing to preserve liquidity and target investment-grade ratios.

- Higher policy rates ~4–5% raise borrowing costs and debt service.

- Potential slowdown in vessel purchases due to higher finance costs.

- Active capital-structure management to protect liquidity and ratings.

Profitability of the ONE joint venture

A significant portion of K LINE's 2024-25 net income stems from its 31.3% stake in Ocean Network Express (ONE); ONE reported a 2024 adjusted EBITDA of about USD 8.2 billion, down from 2022 peaks, directly impacting K LINE's equity earnings and dividends.

Container freight rates remain highly cyclical—Harpex index and Shanghai Containerized Freight Index fell ~45% from 2022 highs to 2024 levels—so ONE's profitability—and thus K LINE's returns—varies sharply with global demand and fleet supply.

Economic slowdowns in major markets (US, EU, China) cut container volumes; IMF 2024 growth of 3.1% vs 3.6% in 2022 implies weaker dividend flow and lower equity income for K LINE from ONE.

- K LINE owns ~31.3% of ONE; ONE 2024 adjusted EBITDA ~USD 8.2bn

- Harpex/SCFI down ~45% from 2022 to 2024

- IMF 2024 global growth 3.1% -> pressure on volumes/dividends

Macro headwinds squeeze shipping: higher spot exposure, fuel & rates spike costs

Macro cycles cut dry-bulk and container volumes—IMF 2024 growth 3.1%—driving spot exposure to 38% and 62% time-charter coverage; ONE 31.3% stake (ONE 2024 adj. EBITDA ~USD 8.2bn) amplifies income volatility. Fuel (0.5%S bunker ~$620/ton in 2024) and interest rates (policy ~4–5% in 2024–25) raised operating and financing costs, prompting LNG/efficiency investments and active FX/debt hedging.

| Metric | 2024–25 |

|---|---|

| Spot exposure | 38% |

| Time-charter cover | 62% |

| ONE stake / ONE adj. EBITDA | 31.3% / USD 8.2bn |

| Bunker 0.5%S | ~USD 620/ton |

| Policy rates range | ~4–5% |

Preview the Actual Deliverable

Kawasaki Kisen Kaisha PESTLE Analysis

The preview shown here is the exact Kawasaki Kisen Kaisha PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible are exactly what you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our Kawasaki Kisen Kaisha PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the company’s trajectory; buy the full report for the complete, actionable breakdown and downloadable charts to support investment decisions or strategic planning.

Political factors

Geopolitical instability in trade corridors

Ongoing Middle East conflicts and South China Sea tensions have lengthened routes for K LINE, contributing to a ~7-10% rise in voyage times in 2024–25 and adding an estimated $30–45/TEU in extra fuel and rerouting costs; insurance premiums for vessels transiting high-risk corridors rose about 12% in 2025. K LINE must sustain elevated diplomatic engagement and route flexibility to contain delays and protect margins.

Trade protectionism and tariff policies

The rise of protectionist policies in the US and EU adds volatility to global trade; US tariffs rose to an average applied MFN rate of 3.5% in 2024 with several auto-sector measures raising effective duties by up to 10–25%, shrinking containerized vehicle flows.

New tariffs on autos and raw materials directly cut demand for K LINE's specialized car carriers and RO/RO services—K Line reported 2024 vehicle liftings down 6% YoY to ~1.15 million units, reflecting softer trade volumes.

Shifts in bilateral agreements and regional manufacturing relocation (nearshoring to Mexico and Southeast Asia) require K LINE to model route elasticity and adjust fleet deployment; scenario analysis should include tariff shock cases reducing volumes by 5–15% per corridor.

Japanese government maritime support

The Japanese government’s 2024 Maritime Strategy allocates ¥200 billion to fleet renewal and energy supply-chain resilience, reinforcing a pro-shipping political framework that favors domestic carriers like Kawasaki Kisen Kaisha (K LINE).

K LINE benefits from subsidies and R&D grants under the Autonomous Shipping Promotion Program, which reached ¥18.5 billion in 2025 funding for trials and technology development.

This alignment with national security and economic policies secures K LINE’s role in Japan’s merchant marine, supporting its 2024 fleet of ~430 vessels and contributing to stable long-term demand.

International sanctions and compliance

Strict enforcement of international sanctions forces K LINE to maintain rigorous legal and political screening for cargo and partners; in 2024 the company reported compliance-related costs rising to approx. JPY 14.5bn as sanction checks and vetting expanded.

Navigating global sanctions is essential to avoid fines and reputational harm that could endanger correspondent banking; shipping fines globally averaged over USD 1.2m per major breach in 2023–24.

K LINE invests heavily in compliance infrastructure, upgrading sanctions screening and AML systems to meet rapidly changing rules across jurisdictions.

- Compliance costs ~JPY 14.5bn (2024)

- Average major shipping fine ~USD 1.2m (2023–24)

- Enhanced sanctions/AML systems deployed across fleet and partners

Energy security and resource diplomacy

Kawasaki Kisen Kaisha (K LINE) transports ~10% of global LNG shipping capacity and significant crude volumes, linking it to state-led energy diplomacy; disruptions in exporters like Russia or Qatar can force route changes and surge costs—spot LNG rates spiked 300% in 2022, highlighting volatility.

Long-term charters (over 60% of fleet employment) buffer revenue but require renegotiation when political shifts alter export policies or sanctions, risking idle tonnage or early contract terminations.

- ~10% share of global LNG shipping capacity

- Over 60% fleet on long-term charters

- 2022 spot LNG rate spike ~300%

K LINE hit by geopolitical costs—voyage delays, $30–45/TEU reroutes, insurance +12%

Political risks (Middle East/South China Sea tensions, protectionism, sanctions, energy diplomacy) raised K LINE’s 2024–25 costs: voyage times +7–10%, extra fuel/reroute ~$30–45/TEU, insurance +12% (2025), compliance ~JPY14.5bn (2024); supports from Japan: ¥200bn maritime strategy, ¥18.5bn autonomous shipping funds (2025), fleet ~430 vessels, ~10% global LNG capacity.

| Metric | Value |

|---|---|

| Voyage time increase | 7–10% |

| Extra cost/TEU | $30–45 |

| Insurance rise (2025) | +12% |

| Compliance costs (2024) | JPY14.5bn |

| Japan maritime fund | ¥200bn |

| Autonomous shipping grants (2025) | ¥18.5bn |

| Fleet size (2024) | ~430 vessels |

| Global LNG share | ~10% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Kawasaki Kisen Kaisha across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategic decision-making for executives, investors, and consultants.

A concise, visually segmented Kawasaki Kisen Kaisha PESTLE summary that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning while allowing note additions for region- or business-specific context.

Economic factors

Volatility in global commodity prices

Fluctuations in iron ore, coal and grain prices drove a 12% year-on-year variance in dry bulk demand for K LINE through end-2025, with iron ore spot freight rates swinging 40% in 2025 alone. Cyclical downturns in steel and power reduced volumes, raising the company's spot-market exposure to 38% of dry-bulk liftings. K LINE offsets volatility via diversified contracts—time-charters and multi-year fixtures—covering roughly 62% of its dry-bulk capacity to 31 Dec 2025.

Currency exchange rate sensitivity

As a Yen-reporter with significant USD revenues, K Line is highly exposed to USD/JPY moves; a 10% yen depreciation in 2023 raised translated revenue by roughly JPY 50–70 billion, while dollar-denominated net debt (~USD 2.1 billion at FY2024) became costlier when USD/JPY rose above 150. Management used FX forwards, swaps and currency options covering a large portion of expected cash flows, trimming reported FX volatility despite divergent BOJ/Fed stances.

Bunker fuel and alternative energy costs

The shift from heavy fuel oil to low-sulfur fuels and LNG raised per-vessel fuel costs; scrubber-equipped ships incur capex, while 2024 global bunker average for 0.5%S was about $620/ton versus ~$420/ton for HSFO in 2020, widening operating margins pressure for K LINE.

Fuel volatility remains critical—fuel accounts for roughly 40% of voyage costs in container and bulk shipping; Brent-linked swings in 2024 saw bunker price monthly variance >25%, stressing short-term cash flows.

K LINE is cutting exposure by improving slow-steaming and hull efficiency and invested in dual-fuel LNG vessels; as of 2025 the company targets reducing fleet CO2 and fuel spend by mid-single digits annually through these measures.

Global interest rate environment

The 2025 global interest rate environment, with major central bank policy rates around 4.5–5.0% (Fed 5.25%–5.5% in late 2024; ECB ~3.75% in 2024), raises K Line's cost of capital for fleet modernization, increasing annual debt service and potentially delaying new eco-vessel orders.

K Line actively monitors monetary policy and leverages debt maturity management and hybrid financing to preserve liquidity and target investment-grade ratios.

- Higher policy rates ~4–5% raise borrowing costs and debt service.

- Potential slowdown in vessel purchases due to higher finance costs.

- Active capital-structure management to protect liquidity and ratings.

Profitability of the ONE joint venture

A significant portion of K LINE's 2024-25 net income stems from its 31.3% stake in Ocean Network Express (ONE); ONE reported a 2024 adjusted EBITDA of about USD 8.2 billion, down from 2022 peaks, directly impacting K LINE's equity earnings and dividends.

Container freight rates remain highly cyclical—Harpex index and Shanghai Containerized Freight Index fell ~45% from 2022 highs to 2024 levels—so ONE's profitability—and thus K LINE's returns—varies sharply with global demand and fleet supply.

Economic slowdowns in major markets (US, EU, China) cut container volumes; IMF 2024 growth of 3.1% vs 3.6% in 2022 implies weaker dividend flow and lower equity income for K LINE from ONE.

- K LINE owns ~31.3% of ONE; ONE 2024 adjusted EBITDA ~USD 8.2bn

- Harpex/SCFI down ~45% from 2022 to 2024

- IMF 2024 global growth 3.1% -> pressure on volumes/dividends

Macro headwinds squeeze shipping: higher spot exposure, fuel & rates spike costs

Macro cycles cut dry-bulk and container volumes—IMF 2024 growth 3.1%—driving spot exposure to 38% and 62% time-charter coverage; ONE 31.3% stake (ONE 2024 adj. EBITDA ~USD 8.2bn) amplifies income volatility. Fuel (0.5%S bunker ~$620/ton in 2024) and interest rates (policy ~4–5% in 2024–25) raised operating and financing costs, prompting LNG/efficiency investments and active FX/debt hedging.

| Metric | 2024–25 |

|---|---|

| Spot exposure | 38% |

| Time-charter cover | 62% |

| ONE stake / ONE adj. EBITDA | 31.3% / USD 8.2bn |

| Bunker 0.5%S | ~USD 620/ton |

| Policy rates range | ~4–5% |

Preview the Actual Deliverable

Kawasaki Kisen Kaisha PESTLE Analysis

The preview shown here is the exact Kawasaki Kisen Kaisha PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and structure visible are exactly what you’ll download immediately after payment.