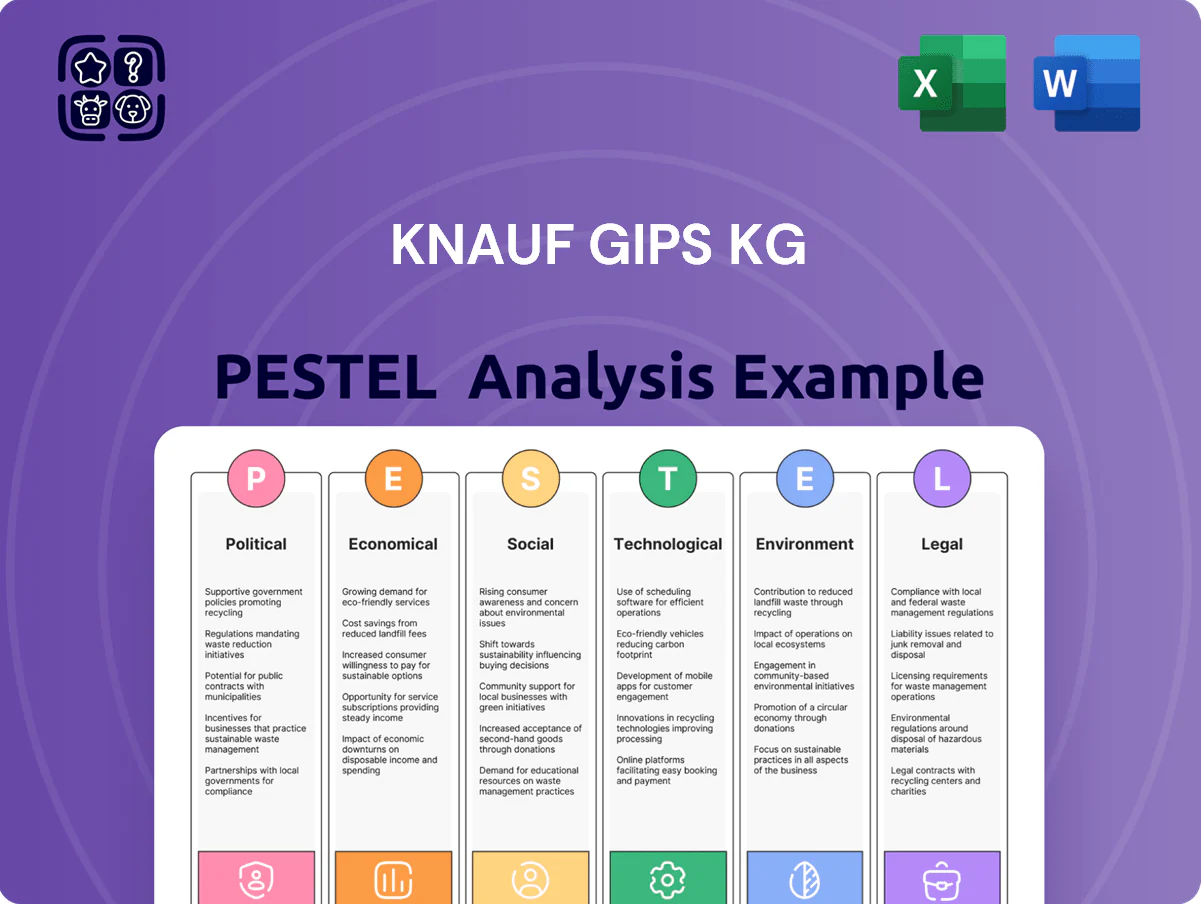

Knauf Gips KG PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Knauf Gips KG—pinpoint how political, economic, social, technological, legal, and environmental forces are reshaping its market position; buy the full report to access actionable insights, ready-to-use slides, and data-driven recommendations for investment or strategic planning.

Political factors

Geopolitical Trade Barriers and Tariffs

Knauf Gips KG’s global footprint exposes it to shifting trade policies and protectionist measures among the EU, US and China, risking tariff impacts on ~30% of its 2024 exports; recent tariffs raised import costs by up to 12% for certain mineral and chemical inputs. As of late 2025, companies have moved toward localized production—Knauf reports ~18% capacity added in APAC and North America to limit duties. Decision-makers must track bilateral agreements (e.g., EU–US, US–China dialogues) that can alter duties on construction chemicals and insulation tech, where a 5–10% tariff swing materially affects margins.

Government Infrastructure Stimulus Programs

Public spending in North America and India is set to sustain demand for large-scale construction materials through 2025; US Infrastructure Investment and Jobs Act channels roughly $550 billion to core infrastructure while India’s National Infrastructure Pipeline targets $1.4 trillion (2020–25), supporting Knauf’s commercial drylining and flooring sales.

Energy Security and Industrial Policy

The EU energy transition and national industrial policies are reshaping high-energy industries like gypsum calcination, with Europe targeting a 55% GHG reduction by 2030 under Fit for 55, pressuring Knauf to lower emissions from thermal processes that consumed ~20–30 GJ/t clinker-equivalent energy in 2024. Political mandates for industrial decarbonization raise operating costs but open access to EU funds—RRF/CEF—where grants and loans total €200+ billion for 2021–2027, enabling Knauf to invest in electric kilns and CCS pilots. National energy security drives gas price volatility—European gas prices averaged €38/MWh in 2024 vs €70/MWh in 2022—affecting feedstock costs and prompting Knauf to hedge and pursue electrification aligned with governments’ energy independence targets.

Housing Subsidy and Affordability Shifts

- 2024 affordable housing spending +7% (EU average)

- New housing starts sensitivity: ±4–6% vs subsidy/mortgage policy shifts

- Election cycles cause policy volatility affecting demand for plasterboard

- Track rent control and mortgage support legislation for construction forecasts

Standardization of International Building Codes

Political moves toward harmonized international building codes force Knauf to adapt certification and marketing for its fire-resistant and acoustic systems; EU Regulation and IMO amendments increased compliance scopes, with firesafety standards driving ~12% of product R&D spend in 2024.

Governments adopting stricter safety/performance codes require Knauf to engage regulators continuously—company reported 8 regulatory certifications gained across EU, UK and MENA in 2024 to maintain market access.

This regulatory push raises entry barriers: smaller rivals face higher certification costs while Knauf’s 2024 R&D and testing infrastructure, supported by annual revenue of ~6.2 billion EUR, provides competitive advantage.

- Stricter codes increase compliance costs but favor incumbents

- Knauf: ~12% of R&D tied to safety products (2024)

- 8 new certifications (EU/UK/MENA) in 2024

- 2024 revenue ~6.2 billion EUR supports testing/certification

Knauf weathers tariffs and capacity shifts as public infra, funds and regs reshape demand

Knauf faces tariff and trade risks impacting ~30% of 2024 exports; recent input tariffs up to 12% and ~18% capacity added in APAC/NA to mitigate duties. Public investment (US $550bn infra, India $1.4tr NIP) supports demand; EU Fit for 55 and gas price swings (€38/MWh 2024) drive decarbonization costs but unlock €200bn+ funds (2021–27). Stricter codes raised R&D compliance spend (~12%) and 8 certifications in 2024.

| Metric | 2024/2025 Value |

|---|---|

| Share exports at trade risk | ~30% |

| Input tariff impact | up to 12% |

| Capacity added (APAC/NA) | ~18% |

| US infrastructure | $550bn |

| India NIP (2020–25) | $1.4tr |

| EU funds (2021–27) | €200bn+ |

| European gas price 2024 | €38/MWh |

| R&D on safety products | ~12% |

| New certifications 2024 | 8 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Knauf Gips KG, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Knauf Gips KG that simplifies external risk assessment and market positioning for meetings, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest Rate Impact on Construction Activity

Stabilized interest rates by late 2025, with OECD policy rates averaging ~3.5% after peaking in 2023–24, underpin a cautiously improving global construction outlook. Cost of financing remains a gating factor: a 25–50 bps shift alters developer hurdle rates and can defer projects, slowing demand for drywall and plasterboard. Knauf’s revenue correlates with real estate cycles in EU, US, and MENA, where housing starts rose ~4% YTD but remain below pre-2022 peaks, making sales sensitive to central bank policy changes.

Raw Material and Commodity Price Volatility

Fluctuations in raw gypsum, paper liners and additives have materially squeezed Knauf Gips KG margins; gypsum prices rose ~18% globally in 2024 while paper pulp costs climbed ~12%, forcing pricing adjustments across European markets. Reduced synthetic gypsum from coal plant retirements shifted sourcing to costlier natural gypsum or recycled inputs, raising feedstock costs by an estimated €30–50/ton in 2024. Knauf mitigates exposure via long‑term supply contracts and vertical integration of quarry operations, lowering volatility and preserving EBITDA resilience.

Emerging Market Growth Trajectories

Rapid urbanization in Southeast Asia (urban population growth ~2% annually) and parts of Africa (urbanization rate ~3.5% annually) could lift construction demand 5–8% yearly, offering Knauf significant growth potential; capturing share hinges on local GDP stability and a rising middle class—e.g., ASEAN GDP growth ~4.5% in 2024, Sub‑Saharan Africa ~3.6% (IMF 2024). Strategic investments must weigh currency devaluation risks and inflation disparities—CPI in Nigeria ~22% (2024) vs. Germany ~3.1% (2024).

Energy Price Fluctuations in Manufacturing

The energy-intensive gypsum production makes Knauf highly sensitive to oil and gas price swings; Brent rose ~45% from $75 in Jan 2023 to ~$109/bbl in 2024, pressuring input costs and margins.

Knauf is investing in energy-efficient kilns and alternative fuels—company reports cite targets to cut specific thermal energy consumption by ~15% by 2026—to protect pricing.

Analysts monitor energy hedges and renewable power uptake; a 2024 note flagged that 30–40% grid-renewable sourcing would materially improve long-term margin resilience.

- High energy intensity → margin exposure to oil/gas prices (Brent ~$109/bbl in 2024)

- Capex on efficient kilns, target −15% thermal use by 2026

- Energy hedges and ~30–40% renewable sourcing tracked by analysts

Skilled Labor Market Constraints

The construction sector in Europe faces a chronic shortfall of skilled installers; EU reports in 2024 show a 15% gap in qualified tradespeople, raising labor costs by ~12% year-on-year and delaying projects that use Knauf’s specialized systems.

Knauf’s push for easy-to-install, high-efficiency gypsum systems directly counters rising manual labor expenses—reducing on-site installation time by up to 30% in pilot projects and protecting product demand.

- 15% skilled labor gap in EU (2024)

- Labor cost rise ~12% YoY (2023–24)

- Knauf systems cut install time ≈30% in pilots

Costs Surge as Energy, Feedstock, and Labor Drive Construction Efficiency Shift

Stabilized policy rates (~3.5% OECD 2025) temper demand; housing starts +4% YTD but below 2022 peaks. Raw gypsum +18% (2024), pulp +12% —feedstock +€30–50/ton. Brent ~€100–110/bbl (2024) raises energy costs; Knauf targets −15% thermal use by 2026. EU skilled‑labor gap 15% (2024), labor costs +12% YoY; Knauf systems cut install time ~30%.

| Metric | Value (2024/25) |

|---|---|

| OECD policy rate | ~3.5% |

| Gypsum price change | +18% |

| Pulp costs | +12% |

| Brent | ~$109/bbl |

| Labor gap EU | 15% |

What You See Is What You Get

Knauf Gips KG PESTLE Analysis

The preview shown here is the exact Knauf Gips KG PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll get upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of Knauf Gips KG—pinpoint how political, economic, social, technological, legal, and environmental forces are reshaping its market position; buy the full report to access actionable insights, ready-to-use slides, and data-driven recommendations for investment or strategic planning.

Political factors

Geopolitical Trade Barriers and Tariffs

Knauf Gips KG’s global footprint exposes it to shifting trade policies and protectionist measures among the EU, US and China, risking tariff impacts on ~30% of its 2024 exports; recent tariffs raised import costs by up to 12% for certain mineral and chemical inputs. As of late 2025, companies have moved toward localized production—Knauf reports ~18% capacity added in APAC and North America to limit duties. Decision-makers must track bilateral agreements (e.g., EU–US, US–China dialogues) that can alter duties on construction chemicals and insulation tech, where a 5–10% tariff swing materially affects margins.

Government Infrastructure Stimulus Programs

Public spending in North America and India is set to sustain demand for large-scale construction materials through 2025; US Infrastructure Investment and Jobs Act channels roughly $550 billion to core infrastructure while India’s National Infrastructure Pipeline targets $1.4 trillion (2020–25), supporting Knauf’s commercial drylining and flooring sales.

Energy Security and Industrial Policy

The EU energy transition and national industrial policies are reshaping high-energy industries like gypsum calcination, with Europe targeting a 55% GHG reduction by 2030 under Fit for 55, pressuring Knauf to lower emissions from thermal processes that consumed ~20–30 GJ/t clinker-equivalent energy in 2024. Political mandates for industrial decarbonization raise operating costs but open access to EU funds—RRF/CEF—where grants and loans total €200+ billion for 2021–2027, enabling Knauf to invest in electric kilns and CCS pilots. National energy security drives gas price volatility—European gas prices averaged €38/MWh in 2024 vs €70/MWh in 2022—affecting feedstock costs and prompting Knauf to hedge and pursue electrification aligned with governments’ energy independence targets.

Housing Subsidy and Affordability Shifts

- 2024 affordable housing spending +7% (EU average)

- New housing starts sensitivity: ±4–6% vs subsidy/mortgage policy shifts

- Election cycles cause policy volatility affecting demand for plasterboard

- Track rent control and mortgage support legislation for construction forecasts

Standardization of International Building Codes

Political moves toward harmonized international building codes force Knauf to adapt certification and marketing for its fire-resistant and acoustic systems; EU Regulation and IMO amendments increased compliance scopes, with firesafety standards driving ~12% of product R&D spend in 2024.

Governments adopting stricter safety/performance codes require Knauf to engage regulators continuously—company reported 8 regulatory certifications gained across EU, UK and MENA in 2024 to maintain market access.

This regulatory push raises entry barriers: smaller rivals face higher certification costs while Knauf’s 2024 R&D and testing infrastructure, supported by annual revenue of ~6.2 billion EUR, provides competitive advantage.

- Stricter codes increase compliance costs but favor incumbents

- Knauf: ~12% of R&D tied to safety products (2024)

- 8 new certifications (EU/UK/MENA) in 2024

- 2024 revenue ~6.2 billion EUR supports testing/certification

Knauf weathers tariffs and capacity shifts as public infra, funds and regs reshape demand

Knauf faces tariff and trade risks impacting ~30% of 2024 exports; recent input tariffs up to 12% and ~18% capacity added in APAC/NA to mitigate duties. Public investment (US $550bn infra, India $1.4tr NIP) supports demand; EU Fit for 55 and gas price swings (€38/MWh 2024) drive decarbonization costs but unlock €200bn+ funds (2021–27). Stricter codes raised R&D compliance spend (~12%) and 8 certifications in 2024.

| Metric | 2024/2025 Value |

|---|---|

| Share exports at trade risk | ~30% |

| Input tariff impact | up to 12% |

| Capacity added (APAC/NA) | ~18% |

| US infrastructure | $550bn |

| India NIP (2020–25) | $1.4tr |

| EU funds (2021–27) | €200bn+ |

| European gas price 2024 | €38/MWh |

| R&D on safety products | ~12% |

| New certifications 2024 | 8 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Knauf Gips KG, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of Knauf Gips KG that simplifies external risk assessment and market positioning for meetings, easily dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest Rate Impact on Construction Activity

Stabilized interest rates by late 2025, with OECD policy rates averaging ~3.5% after peaking in 2023–24, underpin a cautiously improving global construction outlook. Cost of financing remains a gating factor: a 25–50 bps shift alters developer hurdle rates and can defer projects, slowing demand for drywall and plasterboard. Knauf’s revenue correlates with real estate cycles in EU, US, and MENA, where housing starts rose ~4% YTD but remain below pre-2022 peaks, making sales sensitive to central bank policy changes.

Raw Material and Commodity Price Volatility

Fluctuations in raw gypsum, paper liners and additives have materially squeezed Knauf Gips KG margins; gypsum prices rose ~18% globally in 2024 while paper pulp costs climbed ~12%, forcing pricing adjustments across European markets. Reduced synthetic gypsum from coal plant retirements shifted sourcing to costlier natural gypsum or recycled inputs, raising feedstock costs by an estimated €30–50/ton in 2024. Knauf mitigates exposure via long‑term supply contracts and vertical integration of quarry operations, lowering volatility and preserving EBITDA resilience.

Emerging Market Growth Trajectories

Rapid urbanization in Southeast Asia (urban population growth ~2% annually) and parts of Africa (urbanization rate ~3.5% annually) could lift construction demand 5–8% yearly, offering Knauf significant growth potential; capturing share hinges on local GDP stability and a rising middle class—e.g., ASEAN GDP growth ~4.5% in 2024, Sub‑Saharan Africa ~3.6% (IMF 2024). Strategic investments must weigh currency devaluation risks and inflation disparities—CPI in Nigeria ~22% (2024) vs. Germany ~3.1% (2024).

Energy Price Fluctuations in Manufacturing

The energy-intensive gypsum production makes Knauf highly sensitive to oil and gas price swings; Brent rose ~45% from $75 in Jan 2023 to ~$109/bbl in 2024, pressuring input costs and margins.

Knauf is investing in energy-efficient kilns and alternative fuels—company reports cite targets to cut specific thermal energy consumption by ~15% by 2026—to protect pricing.

Analysts monitor energy hedges and renewable power uptake; a 2024 note flagged that 30–40% grid-renewable sourcing would materially improve long-term margin resilience.

- High energy intensity → margin exposure to oil/gas prices (Brent ~$109/bbl in 2024)

- Capex on efficient kilns, target −15% thermal use by 2026

- Energy hedges and ~30–40% renewable sourcing tracked by analysts

Skilled Labor Market Constraints

The construction sector in Europe faces a chronic shortfall of skilled installers; EU reports in 2024 show a 15% gap in qualified tradespeople, raising labor costs by ~12% year-on-year and delaying projects that use Knauf’s specialized systems.

Knauf’s push for easy-to-install, high-efficiency gypsum systems directly counters rising manual labor expenses—reducing on-site installation time by up to 30% in pilot projects and protecting product demand.

- 15% skilled labor gap in EU (2024)

- Labor cost rise ~12% YoY (2023–24)

- Knauf systems cut install time ≈30% in pilots

Costs Surge as Energy, Feedstock, and Labor Drive Construction Efficiency Shift

Stabilized policy rates (~3.5% OECD 2025) temper demand; housing starts +4% YTD but below 2022 peaks. Raw gypsum +18% (2024), pulp +12% —feedstock +€30–50/ton. Brent ~€100–110/bbl (2024) raises energy costs; Knauf targets −15% thermal use by 2026. EU skilled‑labor gap 15% (2024), labor costs +12% YoY; Knauf systems cut install time ~30%.

| Metric | Value (2024/25) |

|---|---|

| OECD policy rate | ~3.5% |

| Gypsum price change | +18% |

| Pulp costs | +12% |

| Brent | ~$109/bbl |

| Labor gap EU | 15% |

What You See Is What You Get

Knauf Gips KG PESTLE Analysis

The preview shown here is the exact Knauf Gips KG PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll get upon checkout.