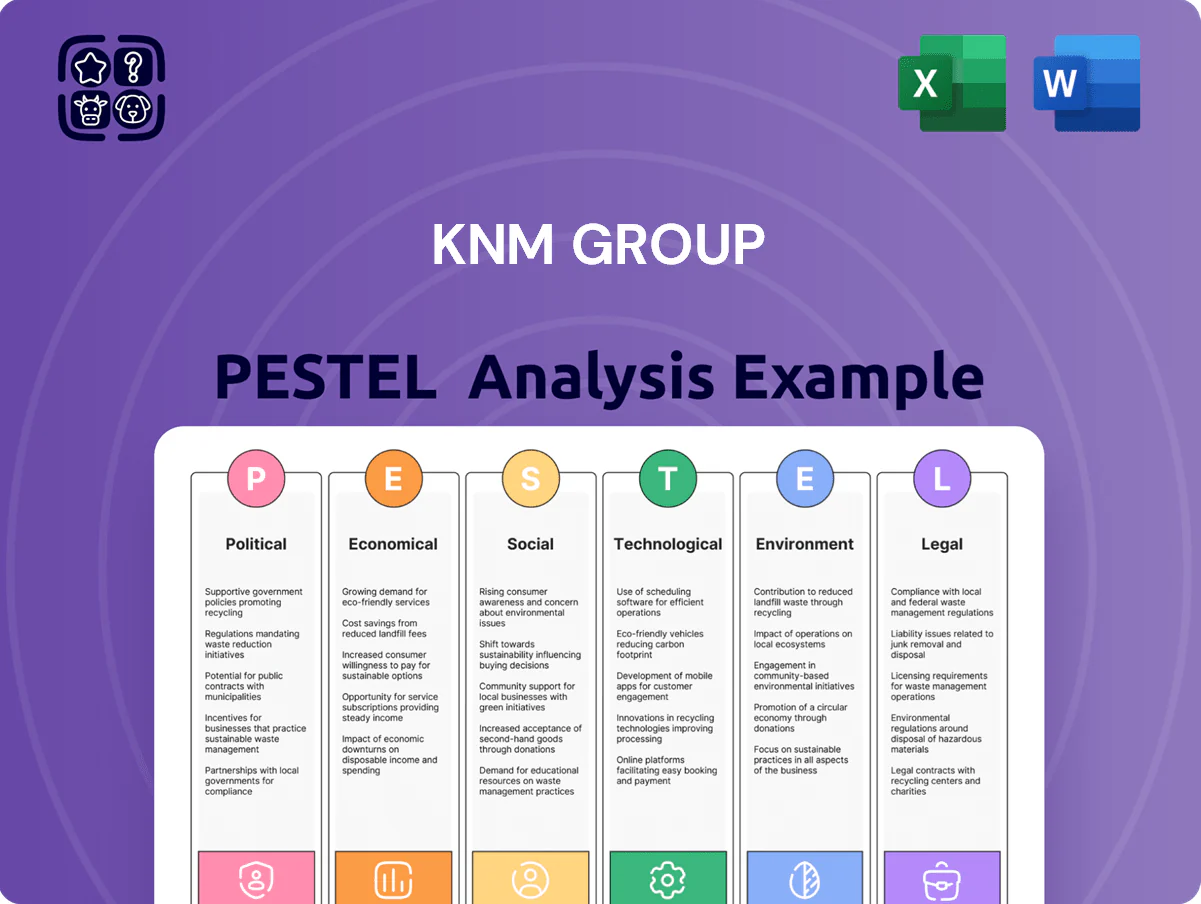

KNM Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis tailored to KNM Group—uncover how political shifts, economic pressures, and technological trends will shape its trajectory and your investment decisions; purchase the full report for a ready-to-use, deep-dive briefing that’s ideal for investors, consultants, and strategy teams.

Political factors

Internal Governance and Boardroom Stability

The ongoing power struggles among KNM Group leadership and major shareholders have left strategic direction uncertain as of late 2025, delaying approval of restructuring measures that aim to trim debt from RM1.2bn in 2024; investor confidence has fallen, with a 28% decline in share price since early 2024. These governance disruptions slow negotiations with international creditors and government agencies, making board stability essential to secure refinancing and restore market trust.

Geopolitical Energy Security Policies

Global shifts in energy sourcing, driven by conflicts in Ukraine and the Middle East, pushed EU gas import diversification and prompted a 2024 EU energy security fund of €53bn, leading nations to prioritize domestic infrastructure and resilient supply chains.

KNM Group benefits as Europe and Southeast Asia raised petrochemical and storage CAPEX—EU member states and ASEAN reported combined project pipelines exceeding $15bn in 2024—boosting demand for engineering, fabrication and modular storage solutions.

However, geopolitical volatility remains a risk: abrupt diplomatic changes have caused contract cancellations worth hundreds of millions, and KNM faces exposure to cross-border project termination and payment delays.

Malaysian Regulatory Environment

KNM remains under intense oversight by Bursa Malaysia and the Securities Commission due to its Practice Note 17 status and stressed balance sheet, with liabilities of RM1.02bn vs. cash of RM120m reported in FY2024 amplifying regulatory focus.

Government measures to bolster the local oil and gas services sector, including a 2024 MYR-focused stimulus and vendor development incentives, create demand tailwinds but mandate strict compliance with listing rules for contract eligibility.

Non-compliance risks delisting and loss of government-linked project access, while shifts in national industrial policy or localization thresholds could materially affect KNM’s ability to win RM-anchored contracts.

International Trade Barriers

As a global exporter of heavy process equipment, KNM is highly sensitive to shifts in trade agreements and tariff rates; in 2024 Malaysia's merchandise exports fell 2.1% YoY, highlighting exposure to external demand shocks.

Protectionist measures in the EU or North America, where tariffs can add 5–25% to capital goods, would raise KNM's costs and erode price competitiveness versus local suppliers.

Managing this requires continuous monitoring of WTO rulings, bilateral trade talks and export controls; in 2025 over 60% of KNM’s revenue was linked to markets with active trade policy debates.

- 2024 Malaysia exports -2.1% YoY

- Potential tariff impact 5–25% on capital goods

- 2025: >60% revenue tied to contested policy markets

Energy Transition Mandates

KNM must realign lobbying and strategy to capture hydrogen and waste-to-energy demand, markets projected to reach USD 290 billion (green hydrogen) and USD 50 billion (waste-to-energy) by 2030, respectively.

- 130+ countries with net-zero targets; 88% of GDP covered

- USD 1.2 trillion clean-energy subsidies in 2024; 175 carbon-pricing jurisdictions

- Green hydrogen market ~USD 290B by 2030; waste-to-energy ~USD 50B by 2030

KNM faces refinancing crunch amid governance turmoil as green transition reshapes demand

Political instability at KNM’s shareholder and board level has depressed investor confidence and delayed refinancing of FY2024 liabilities (RM1.02bn) amid RM120m cash; global energy security shifts and €53bn EU fund (2024) boost CAPEX demand, but protectionism (5–25% tariffs) and stricter Bursa/SC oversight heighten delisting and contract risks while net‑zero policies and USD1.2tn clean subsidies (2024) force strategic pivot to hydrogen/waste‑to‑energy.

| Metric | Value |

|---|---|

| KNM liabilities (FY2024) | RM1.02bn |

| KNM cash (FY2024) | RM120m |

| Share price change (since 2024) | -28% |

| EU energy fund (2024) | €53bn |

| Clean-energy subsidies (2024) | USD1.2tn |

| Tariff risk on capital goods | 5–25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect KNM Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented KNM Group PESTLE summary that’s easy to drop into presentations, editable for local context, and ideal for quick alignment across teams during risk and market-positioning discussions.

Economic factors

Debt Restructuring and Solvency

The successful execution of the Scheme of Arrangement and debt settlement with creditors remains the most critical economic factor for KNM at the end of 2025, with reported gross debt around RM600m in 2024 and ongoing restructuring talks targeting principal reductions and extended maturities.

High levels of legacy debt have historically constrained KNM’s cash flow and its ability to bid for large-scale EPCIC projects, contributing to negative operating cash flow in multiple recent years and depressed capital expenditure.

Achieving financial stability through agreed creditor terms is the primary prerequisite for any future growth or capital expenditure initiatives, enabling KNM to pursue new contracts and restore working capital metrics toward industry norms such as positive free cash flow and improved current ratio.

Global Interest Rate Environment

Global central banks have stabilized policy rates since 2023, but benchmark rates remain near multi-decade highs—e.g., US Fed funds ~5.25–5.50% and ECB depo ~3.75% in 2024—raising borrowing costs for capital-intensive sectors.

For KNM, elevated rates increase interest service on existing debt and push up the hurdle rate for new utility and renewable projects, reducing NPV and IRR feasibility.

Higher costs make project financing pricier; in 2024 project finance spreads widened to ~200–400bps for mid-market deals, prompting KNM to pursue equity cushions, joint ventures, and grant-linked structures.

Currency Exchange Volatility

KNM Group’s multi-jurisdictional exposure makes results highly sensitive to MYR/EUR/USD swings; a 10% depreciation of MYR vs EUR in 2024 would have altered reported EBITDA by approximately MYR 120–180m given FY2023 foreign-revenue mix. Unrealized FX swings have previously impacted valuation of assets like Borsig, where a 2023 EUR/MYR move created multi‑million ringgit valuation variances. Active hedging of contract cash flows and balance‑sheet positions is therefore essential to protect margins.

Fluctuations in Energy Prices

Fluctuations in energy prices directly affect KNM Group as clients’ CAPEX in oil and gas rises with higher Brent crude and Henry Hub prices; Brent averaged about 96 USD/bbl in 2024 and global upstream capex rose ~8% to roughly 430 billion USD in 2024, boosting demand for KNM’s process equipment and EPCC services.

Conversely, prolonged low-price periods (e.g., 2020 pandemic lows) lead to project deferrals and reduced demand for specialized heavy engineering, shrinking order pipelines and pressuring margins.

- Brent ~96 USD/bbl (2024)

- Global upstream capex ≈ 430bn USD (2024, +8%)

- High prices → stronger order book; low prices → project deferrals

Inflation and Material Costs

Persistent inflation in 2024–2025 pushed global steel prices up ~18% year-on-year and nickel/alloy premiums by ~22%, raising KNM Group’s process-equipment input costs and squeezing margins on fixed-price EPCC contracts.

Without procurement hedges and cost-escalation clauses, sudden material or logistics spikes risk eroding project profitability; KNM must enforce long-term supply agreements, indexed pricing, and pass-through mechanisms to mitigate supply-chain shocks.

- Steel +18% YoY (2024)

- Nickel/alloy premiums +22% (2024–25)

- Fixed-price EPCC exposure increases margin volatility

- Mitigation: long-term contracts, hedging, escalation clauses

KNM outlook hinges on RM600m debt overhaul; rates, FX and commodity spikes threaten margins

KNM’s 2024–25 outlook hinges on successful Scheme completion and RM600m gross debt restructuring to restore cash flow; high rates (Fed ~5.25–5.50%) raise funding costs and project hurdles; FX volatility (10% MYR/EUR swing ≈ MYR120–180m EBITDA impact) and commodity inflation (steel +18%, nickel +22% in 2024–25) elevate input costs and margin risk.

| Metric | 2024/25 |

|---|---|

| Gross debt | ~RM600m |

| Brent | ~USD96/bbl (2024) |

| Steel | +18% YoY |

| FX sensitivity | 10% MYR/EUR ≈ MYR120–180m |

Same Document Delivered

KNM Group PESTLE Analysis

The preview shown here is the exact KNM Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis tailored to KNM Group—uncover how political shifts, economic pressures, and technological trends will shape its trajectory and your investment decisions; purchase the full report for a ready-to-use, deep-dive briefing that’s ideal for investors, consultants, and strategy teams.

Political factors

Internal Governance and Boardroom Stability

The ongoing power struggles among KNM Group leadership and major shareholders have left strategic direction uncertain as of late 2025, delaying approval of restructuring measures that aim to trim debt from RM1.2bn in 2024; investor confidence has fallen, with a 28% decline in share price since early 2024. These governance disruptions slow negotiations with international creditors and government agencies, making board stability essential to secure refinancing and restore market trust.

Geopolitical Energy Security Policies

Global shifts in energy sourcing, driven by conflicts in Ukraine and the Middle East, pushed EU gas import diversification and prompted a 2024 EU energy security fund of €53bn, leading nations to prioritize domestic infrastructure and resilient supply chains.

KNM Group benefits as Europe and Southeast Asia raised petrochemical and storage CAPEX—EU member states and ASEAN reported combined project pipelines exceeding $15bn in 2024—boosting demand for engineering, fabrication and modular storage solutions.

However, geopolitical volatility remains a risk: abrupt diplomatic changes have caused contract cancellations worth hundreds of millions, and KNM faces exposure to cross-border project termination and payment delays.

Malaysian Regulatory Environment

KNM remains under intense oversight by Bursa Malaysia and the Securities Commission due to its Practice Note 17 status and stressed balance sheet, with liabilities of RM1.02bn vs. cash of RM120m reported in FY2024 amplifying regulatory focus.

Government measures to bolster the local oil and gas services sector, including a 2024 MYR-focused stimulus and vendor development incentives, create demand tailwinds but mandate strict compliance with listing rules for contract eligibility.

Non-compliance risks delisting and loss of government-linked project access, while shifts in national industrial policy or localization thresholds could materially affect KNM’s ability to win RM-anchored contracts.

International Trade Barriers

As a global exporter of heavy process equipment, KNM is highly sensitive to shifts in trade agreements and tariff rates; in 2024 Malaysia's merchandise exports fell 2.1% YoY, highlighting exposure to external demand shocks.

Protectionist measures in the EU or North America, where tariffs can add 5–25% to capital goods, would raise KNM's costs and erode price competitiveness versus local suppliers.

Managing this requires continuous monitoring of WTO rulings, bilateral trade talks and export controls; in 2025 over 60% of KNM’s revenue was linked to markets with active trade policy debates.

- 2024 Malaysia exports -2.1% YoY

- Potential tariff impact 5–25% on capital goods

- 2025: >60% revenue tied to contested policy markets

Energy Transition Mandates

KNM must realign lobbying and strategy to capture hydrogen and waste-to-energy demand, markets projected to reach USD 290 billion (green hydrogen) and USD 50 billion (waste-to-energy) by 2030, respectively.

- 130+ countries with net-zero targets; 88% of GDP covered

- USD 1.2 trillion clean-energy subsidies in 2024; 175 carbon-pricing jurisdictions

- Green hydrogen market ~USD 290B by 2030; waste-to-energy ~USD 50B by 2030

KNM faces refinancing crunch amid governance turmoil as green transition reshapes demand

Political instability at KNM’s shareholder and board level has depressed investor confidence and delayed refinancing of FY2024 liabilities (RM1.02bn) amid RM120m cash; global energy security shifts and €53bn EU fund (2024) boost CAPEX demand, but protectionism (5–25% tariffs) and stricter Bursa/SC oversight heighten delisting and contract risks while net‑zero policies and USD1.2tn clean subsidies (2024) force strategic pivot to hydrogen/waste‑to‑energy.

| Metric | Value |

|---|---|

| KNM liabilities (FY2024) | RM1.02bn |

| KNM cash (FY2024) | RM120m |

| Share price change (since 2024) | -28% |

| EU energy fund (2024) | €53bn |

| Clean-energy subsidies (2024) | USD1.2tn |

| Tariff risk on capital goods | 5–25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect KNM Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented KNM Group PESTLE summary that’s easy to drop into presentations, editable for local context, and ideal for quick alignment across teams during risk and market-positioning discussions.

Economic factors

Debt Restructuring and Solvency

The successful execution of the Scheme of Arrangement and debt settlement with creditors remains the most critical economic factor for KNM at the end of 2025, with reported gross debt around RM600m in 2024 and ongoing restructuring talks targeting principal reductions and extended maturities.

High levels of legacy debt have historically constrained KNM’s cash flow and its ability to bid for large-scale EPCIC projects, contributing to negative operating cash flow in multiple recent years and depressed capital expenditure.

Achieving financial stability through agreed creditor terms is the primary prerequisite for any future growth or capital expenditure initiatives, enabling KNM to pursue new contracts and restore working capital metrics toward industry norms such as positive free cash flow and improved current ratio.

Global Interest Rate Environment

Global central banks have stabilized policy rates since 2023, but benchmark rates remain near multi-decade highs—e.g., US Fed funds ~5.25–5.50% and ECB depo ~3.75% in 2024—raising borrowing costs for capital-intensive sectors.

For KNM, elevated rates increase interest service on existing debt and push up the hurdle rate for new utility and renewable projects, reducing NPV and IRR feasibility.

Higher costs make project financing pricier; in 2024 project finance spreads widened to ~200–400bps for mid-market deals, prompting KNM to pursue equity cushions, joint ventures, and grant-linked structures.

Currency Exchange Volatility

KNM Group’s multi-jurisdictional exposure makes results highly sensitive to MYR/EUR/USD swings; a 10% depreciation of MYR vs EUR in 2024 would have altered reported EBITDA by approximately MYR 120–180m given FY2023 foreign-revenue mix. Unrealized FX swings have previously impacted valuation of assets like Borsig, where a 2023 EUR/MYR move created multi‑million ringgit valuation variances. Active hedging of contract cash flows and balance‑sheet positions is therefore essential to protect margins.

Fluctuations in Energy Prices

Fluctuations in energy prices directly affect KNM Group as clients’ CAPEX in oil and gas rises with higher Brent crude and Henry Hub prices; Brent averaged about 96 USD/bbl in 2024 and global upstream capex rose ~8% to roughly 430 billion USD in 2024, boosting demand for KNM’s process equipment and EPCC services.

Conversely, prolonged low-price periods (e.g., 2020 pandemic lows) lead to project deferrals and reduced demand for specialized heavy engineering, shrinking order pipelines and pressuring margins.

- Brent ~96 USD/bbl (2024)

- Global upstream capex ≈ 430bn USD (2024, +8%)

- High prices → stronger order book; low prices → project deferrals

Inflation and Material Costs

Persistent inflation in 2024–2025 pushed global steel prices up ~18% year-on-year and nickel/alloy premiums by ~22%, raising KNM Group’s process-equipment input costs and squeezing margins on fixed-price EPCC contracts.

Without procurement hedges and cost-escalation clauses, sudden material or logistics spikes risk eroding project profitability; KNM must enforce long-term supply agreements, indexed pricing, and pass-through mechanisms to mitigate supply-chain shocks.

- Steel +18% YoY (2024)

- Nickel/alloy premiums +22% (2024–25)

- Fixed-price EPCC exposure increases margin volatility

- Mitigation: long-term contracts, hedging, escalation clauses

KNM outlook hinges on RM600m debt overhaul; rates, FX and commodity spikes threaten margins

KNM’s 2024–25 outlook hinges on successful Scheme completion and RM600m gross debt restructuring to restore cash flow; high rates (Fed ~5.25–5.50%) raise funding costs and project hurdles; FX volatility (10% MYR/EUR swing ≈ MYR120–180m EBITDA impact) and commodity inflation (steel +18%, nickel +22% in 2024–25) elevate input costs and margin risk.

| Metric | 2024/25 |

|---|---|

| Gross debt | ~RM600m |

| Brent | ~USD96/bbl (2024) |

| Steel | +18% YoY |

| FX sensitivity | 10% MYR/EUR ≈ MYR120–180m |

Same Document Delivered

KNM Group PESTLE Analysis

The preview shown here is the exact KNM Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.