Kobayashi Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

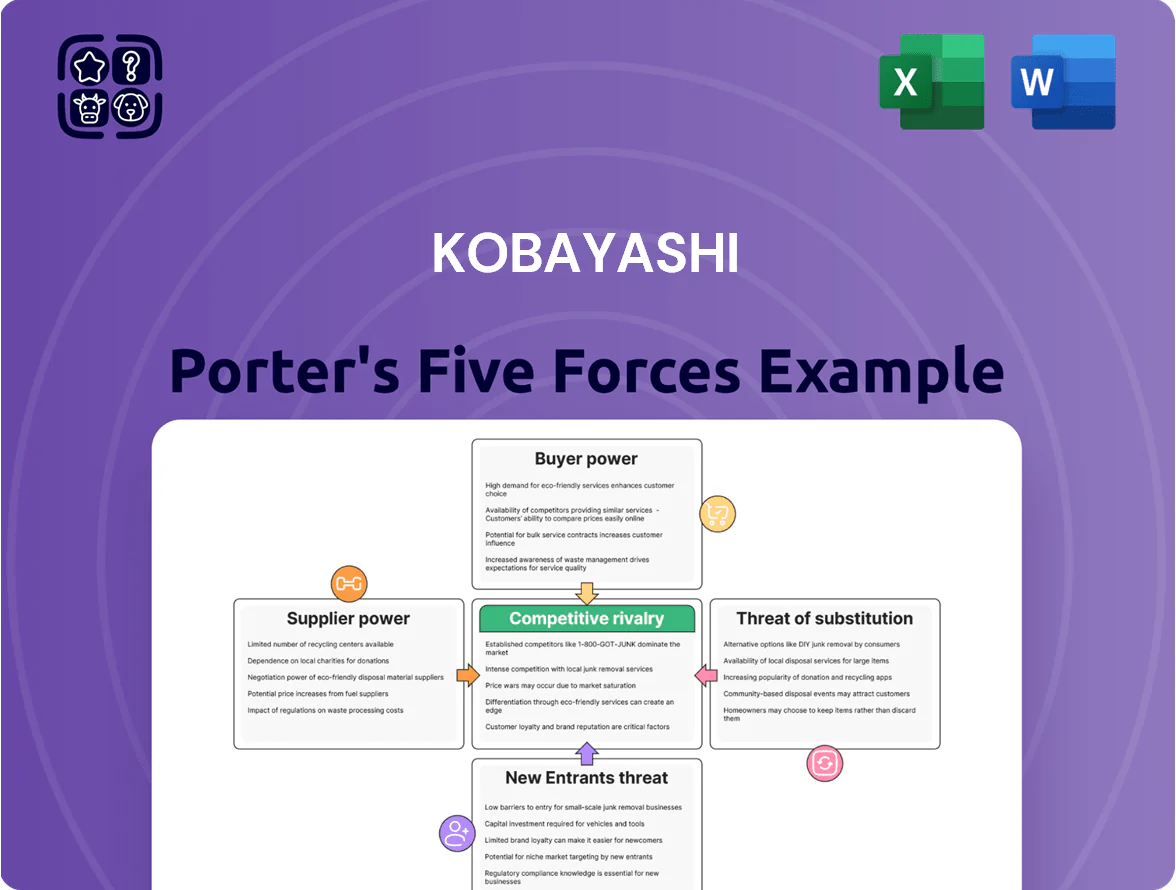

Kobayashi’s Porter’s Five Forces snapshot highlights supplier leverage, buyer sensitivity, rivalry intensity, substitute threats, and entry barriers shaping its competitive landscape—useful for quick orientation and risk spotting.

This brief preview only scratches the surface; unlock the full Porter’s Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to Kobayashi.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Kobayashi depends on chemical and natural commodities—over 40% of COGS in FY2024 were raw materials—so global price swings (e.g., 2022–24 average volatility: ~18% annually for key petrochemicals) can compress margins if suppliers pass costs on. Kobayashi keeps multiple suppliers and 3 regional procurement hubs to limit single‑source risk; maintaining 6–12 months safety stock cut production stoppages by 35% in 2024.

Specialized Ingredient Dependencies

Certain niche products need biological or chemical extracts from about 6 certified global vendors, concentrating supply and giving those suppliers price leverage; suppliers raised prices 7–12% in 2025 vs 2023 for specialty extracts.

After 2024 recalls, safety audits doubled and only ~40% of previous vendors passed new compliance, shrinking the qualified pool and strengthening suppliers’ contract terms and minimum order requirements.

Supplier Compliance and Safety Costs

By end-2025 Kobayashi enforced stricter upstream quality controls, raising suppliers’ compliance and safety costs by an estimated 8–12% per supplier; suppliers report capital outlays of $150k–$1.2M for testing and certification. These higher costs give capable, certified suppliers pricing leverage, enabling price increases of 3–7% without losing contracts. As regulators increase inspections, supplier bargaining power shifts toward those guaranteeing purity and safety.

Switching Costs for Specialized Inputs

Changing suppliers for active pharmaceutical ingredients (APIs) carries heavy regulatory hurdles—FDA or PMDA revalidation can take 6–18 months and cost $0.5–$5M per SKU—so Kobayashi faces high switching costs that deter moves to cheaper sources.

Those costs risk production delays and lost revenue (example: a 3‑month shutdown on a $20M drug line wipes ~$5M gross profit), keeping established API suppliers influential in the value chain.

- Regulatory revalidation: 6–18 months

- Requalification cost per SKU: $0.5–$5M

- 3‑month shutdown impact: ~$5M gross profit on $20M annual line

- Result: suppliers retain pricing and supply leverage

Forward Integration Risk

- Large suppliers entering finished goods (2024–25 moves)

- Risk: procurement leverage, margin pressure

- Defence: 12% domestic share, branded R&D, retail footprint

- Action: lock long-term contracts, co-branding, SKU exclusivity

Suppliers exert moderate‑high pricing power; raw materials 40%+ and costly API switches

Suppliers hold moderate‑high power: raw materials = 40%+ COGS (FY2024), petrochemical volatility ~18% pa (2022–24), niche extracts from 6 vendors saw price hikes 7–12% (2023–25), API switch costs 6–18 months and $0.5–$5M per SKU, safety compliance raised supplier costs 8–12% and allowed 3–7% price increases, but Kobayashi’s 12% Japan share limits full forward‑integration risk.

| Metric | Value |

|---|---|

| Raw materials (%COGS) | 40%+ |

| Petrochem volatility | ~18% pa |

| Niche price rise | 7–12% |

| API revalidation | 6–18 months; $0.5–$5M |

| Supplier cost raise | 8–12% |

| Brand share (Japan) | 12% |

What is included in the product

Tailored Five Forces analysis for Kobayashi that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers to protect profitability.

Kobayashi Porter's Five Forces in one sheet—instantly reveal competitive pressure hotspots and relieve strategic uncertainty for faster, evidence-based decisions.

Customers Bargaining Power

Retailer Consolidation in Japan

Japan's drugstore and convenience-store sector is concentrated: in 2024 the top 10 drugstore chains held about 62% market share and the Big Three convenience chains (7‑Eleven, Lawson, FamilyMart) ran ~55% of urban outlets, giving them huge buying power over Kobayashi.

These retailers negotiate steep trade discounts—often 5–15% deeper than smaller buyers—and demand premium shelf placement and promotional funding, squeezing Kobayashi's gross margins by several hundred basis points on key OTC lines.

Ongoing consolidation—M&A and franchise rollups reduced independent pharmacy counts by ~12% from 2018–2023—means retailers can increasingly dictate pricing, payment terms, and product assortment to manufacturers like Kobayashi.

Fragile Brand Loyalty Post Recall

Following the 2024 safety recall that cut sales 18% in Q3 2024, customer trust is fragile and price-sensitive; surveys show 42% of past buyers say they will switch brands after one safety lapse, boosting buyer bargaining power. Retail returns rose 27% and net promoter score fell 14 points, so consumers now demand clearer transparency and safety guarantees or will migrate to competitors, increasing switching risk and margin pressure.

Price Sensitivity in Hygiene Products

Consumers treat many household and hygiene items as interchangeable, driving high price elasticity; Kobayashi faced this in 2024 when 52% of Japanese shoppers cited price as the top purchase driver for toiletries (Nikkei, 2024), so price hikes risk immediate share loss to private labels. Online price transparency—price comparison apps and e-commerce listings—means shoppers can find alternatives within minutes, keeping downward pressure on margins.

Low Switching Costs for End Users

Low switching costs in OTC drugs and hygiene mean consumers can try alternatives with no financial penalty, and global FMCG data shows private-label share rose to 20% in several markets by 2024, pressuring branded players like Kobayashi.

This ease forces Kobayashi to keep innovating and spend on marketing—Japan consumer goods ad spend was ¥2.3 trillion in 2024—since no long-term contracts exist, shoppers hold pricing and loyalty power.

- Near-zero trial cost for consumers

- Private-label share ≈20% (2024)

- Japan ad spend ¥2.3T (2024)

- No long-term contracts → buyer advantage

Demand for Transparency and Efficacy

Consumers now research ingredients and clinical efficacy before buying; 72% of skincare buyers said efficacy data influences purchases in a 2024 Euromonitor survey, pushing firms to publish trials and biomarkers.

Companies must spend more on evidence-based marketing—median ad+R&D share rose to 18% of revenue for public cos in 2023—to answer buyer queries and reduce churn.

Without transparent data, brands face rapid customer loss: a 2022 McKinsey panel found 38% of consumers switched brands for better transparency within 6 months.

- 72% of buyers value efficacy data (Euromonitor 2024)

- Median ad+R&D = 18% revenue (public firms, 2023)

- 38% switched for transparency within 6 months (McKinsey 2022)

Retail consolidation squeezes Kobayashi: deep discounts, placement fees cut margins

Retail consolidation and dominant chains (top‑10 drugstores ~62% share; Big Three convenience ~55% urban outlets, 2024) give buyers strong leverage, forcing deep trade discounts (5–15%) and premium placement demands that shave several hundred bps from Kobayashi’s gross margins; low switching costs, 20% private‑label share (2024), and high price sensitivity (52% cite price for toiletries, Nikkei 2024) amplify pressure.

| Metric | Value |

|---|---|

| Top‑10 drugstore share | ~62% (2024) |

| Big Three convenience urban outlets | ~55% (2024) |

| Trade discount uplift vs small buyers | 5–15% |

| Private‑label share | ~20% (2024) |

| Toiletries: price top driver | 52% (Nikkei 2024) |

What You See Is What You Get

Kobayashi Porter's Five Forces Analysis

This preview shows the exact Kobayashi Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document is fully formatted and ready to use, including supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessments tailored to Kobayashi.

Once you buy, you’ll get instant access to this same comprehensive file for download and application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kobayashi’s Porter’s Five Forces snapshot highlights supplier leverage, buyer sensitivity, rivalry intensity, substitute threats, and entry barriers shaping its competitive landscape—useful for quick orientation and risk spotting.

This brief preview only scratches the surface; unlock the full Porter’s Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy tailored to Kobayashi.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Kobayashi depends on chemical and natural commodities—over 40% of COGS in FY2024 were raw materials—so global price swings (e.g., 2022–24 average volatility: ~18% annually for key petrochemicals) can compress margins if suppliers pass costs on. Kobayashi keeps multiple suppliers and 3 regional procurement hubs to limit single‑source risk; maintaining 6–12 months safety stock cut production stoppages by 35% in 2024.

Specialized Ingredient Dependencies

Certain niche products need biological or chemical extracts from about 6 certified global vendors, concentrating supply and giving those suppliers price leverage; suppliers raised prices 7–12% in 2025 vs 2023 for specialty extracts.

After 2024 recalls, safety audits doubled and only ~40% of previous vendors passed new compliance, shrinking the qualified pool and strengthening suppliers’ contract terms and minimum order requirements.

Supplier Compliance and Safety Costs

By end-2025 Kobayashi enforced stricter upstream quality controls, raising suppliers’ compliance and safety costs by an estimated 8–12% per supplier; suppliers report capital outlays of $150k–$1.2M for testing and certification. These higher costs give capable, certified suppliers pricing leverage, enabling price increases of 3–7% without losing contracts. As regulators increase inspections, supplier bargaining power shifts toward those guaranteeing purity and safety.

Switching Costs for Specialized Inputs

Changing suppliers for active pharmaceutical ingredients (APIs) carries heavy regulatory hurdles—FDA or PMDA revalidation can take 6–18 months and cost $0.5–$5M per SKU—so Kobayashi faces high switching costs that deter moves to cheaper sources.

Those costs risk production delays and lost revenue (example: a 3‑month shutdown on a $20M drug line wipes ~$5M gross profit), keeping established API suppliers influential in the value chain.

- Regulatory revalidation: 6–18 months

- Requalification cost per SKU: $0.5–$5M

- 3‑month shutdown impact: ~$5M gross profit on $20M annual line

- Result: suppliers retain pricing and supply leverage

Forward Integration Risk

- Large suppliers entering finished goods (2024–25 moves)

- Risk: procurement leverage, margin pressure

- Defence: 12% domestic share, branded R&D, retail footprint

- Action: lock long-term contracts, co-branding, SKU exclusivity

Suppliers exert moderate‑high pricing power; raw materials 40%+ and costly API switches

Suppliers hold moderate‑high power: raw materials = 40%+ COGS (FY2024), petrochemical volatility ~18% pa (2022–24), niche extracts from 6 vendors saw price hikes 7–12% (2023–25), API switch costs 6–18 months and $0.5–$5M per SKU, safety compliance raised supplier costs 8–12% and allowed 3–7% price increases, but Kobayashi’s 12% Japan share limits full forward‑integration risk.

| Metric | Value |

|---|---|

| Raw materials (%COGS) | 40%+ |

| Petrochem volatility | ~18% pa |

| Niche price rise | 7–12% |

| API revalidation | 6–18 months; $0.5–$5M |

| Supplier cost raise | 8–12% |

| Brand share (Japan) | 12% |

What is included in the product

Tailored Five Forces analysis for Kobayashi that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers to protect profitability.

Kobayashi Porter's Five Forces in one sheet—instantly reveal competitive pressure hotspots and relieve strategic uncertainty for faster, evidence-based decisions.

Customers Bargaining Power

Retailer Consolidation in Japan

Japan's drugstore and convenience-store sector is concentrated: in 2024 the top 10 drugstore chains held about 62% market share and the Big Three convenience chains (7‑Eleven, Lawson, FamilyMart) ran ~55% of urban outlets, giving them huge buying power over Kobayashi.

These retailers negotiate steep trade discounts—often 5–15% deeper than smaller buyers—and demand premium shelf placement and promotional funding, squeezing Kobayashi's gross margins by several hundred basis points on key OTC lines.

Ongoing consolidation—M&A and franchise rollups reduced independent pharmacy counts by ~12% from 2018–2023—means retailers can increasingly dictate pricing, payment terms, and product assortment to manufacturers like Kobayashi.

Fragile Brand Loyalty Post Recall

Following the 2024 safety recall that cut sales 18% in Q3 2024, customer trust is fragile and price-sensitive; surveys show 42% of past buyers say they will switch brands after one safety lapse, boosting buyer bargaining power. Retail returns rose 27% and net promoter score fell 14 points, so consumers now demand clearer transparency and safety guarantees or will migrate to competitors, increasing switching risk and margin pressure.

Price Sensitivity in Hygiene Products

Consumers treat many household and hygiene items as interchangeable, driving high price elasticity; Kobayashi faced this in 2024 when 52% of Japanese shoppers cited price as the top purchase driver for toiletries (Nikkei, 2024), so price hikes risk immediate share loss to private labels. Online price transparency—price comparison apps and e-commerce listings—means shoppers can find alternatives within minutes, keeping downward pressure on margins.

Low Switching Costs for End Users

Low switching costs in OTC drugs and hygiene mean consumers can try alternatives with no financial penalty, and global FMCG data shows private-label share rose to 20% in several markets by 2024, pressuring branded players like Kobayashi.

This ease forces Kobayashi to keep innovating and spend on marketing—Japan consumer goods ad spend was ¥2.3 trillion in 2024—since no long-term contracts exist, shoppers hold pricing and loyalty power.

- Near-zero trial cost for consumers

- Private-label share ≈20% (2024)

- Japan ad spend ¥2.3T (2024)

- No long-term contracts → buyer advantage

Demand for Transparency and Efficacy

Consumers now research ingredients and clinical efficacy before buying; 72% of skincare buyers said efficacy data influences purchases in a 2024 Euromonitor survey, pushing firms to publish trials and biomarkers.

Companies must spend more on evidence-based marketing—median ad+R&D share rose to 18% of revenue for public cos in 2023—to answer buyer queries and reduce churn.

Without transparent data, brands face rapid customer loss: a 2022 McKinsey panel found 38% of consumers switched brands for better transparency within 6 months.

- 72% of buyers value efficacy data (Euromonitor 2024)

- Median ad+R&D = 18% revenue (public firms, 2023)

- 38% switched for transparency within 6 months (McKinsey 2022)

Retail consolidation squeezes Kobayashi: deep discounts, placement fees cut margins

Retail consolidation and dominant chains (top‑10 drugstores ~62% share; Big Three convenience ~55% urban outlets, 2024) give buyers strong leverage, forcing deep trade discounts (5–15%) and premium placement demands that shave several hundred bps from Kobayashi’s gross margins; low switching costs, 20% private‑label share (2024), and high price sensitivity (52% cite price for toiletries, Nikkei 2024) amplify pressure.

| Metric | Value |

|---|---|

| Top‑10 drugstore share | ~62% (2024) |

| Big Three convenience urban outlets | ~55% (2024) |

| Trade discount uplift vs small buyers | 5–15% |

| Private‑label share | ~20% (2024) |

| Toiletries: price top driver | 52% (Nikkei 2024) |

What You See Is What You Get

Kobayashi Porter's Five Forces Analysis

This preview shows the exact Kobayashi Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document is fully formatted and ready to use, including supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessments tailored to Kobayashi.

Once you buy, you’ll get instant access to this same comprehensive file for download and application.