Kodak Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

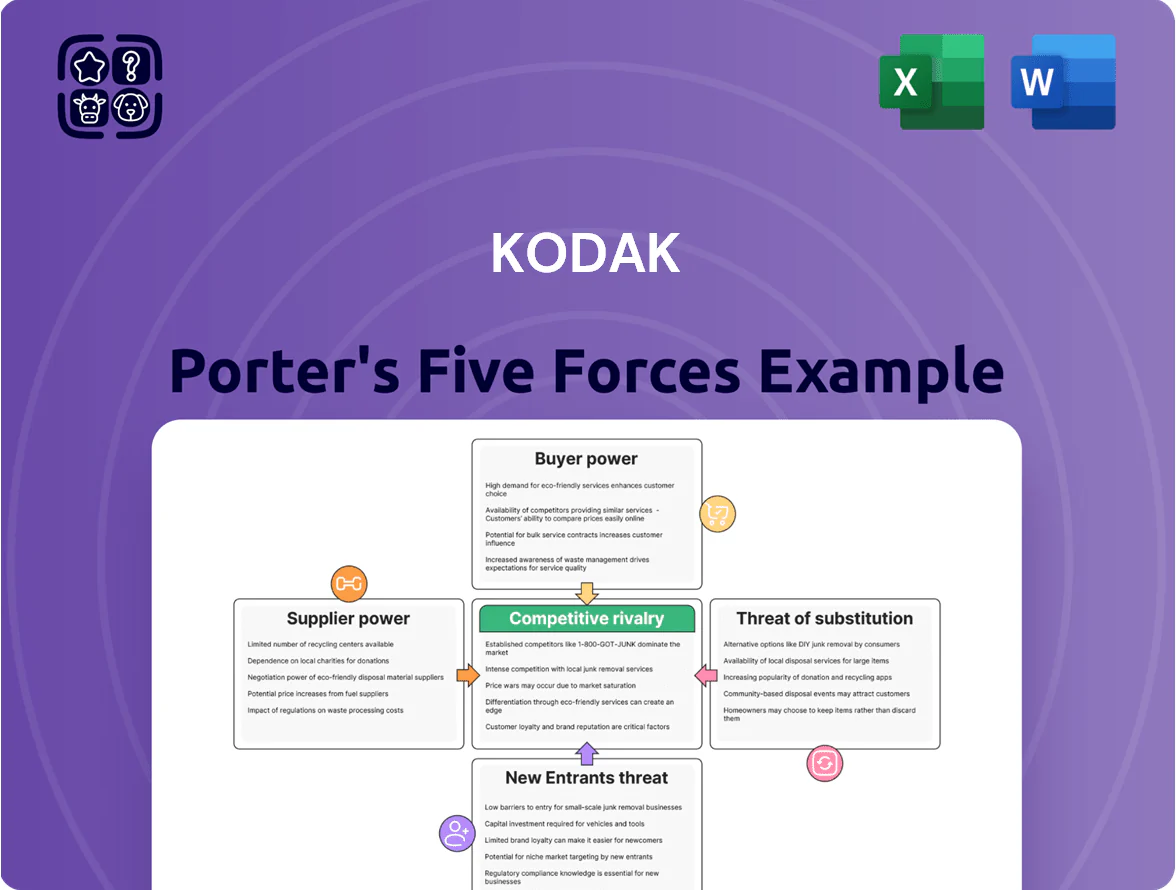

Kodak faces moderate buyer power and substitution threats as it pivots from legacy film to niche imaging and commercial print; supplier concentration and capital needs temper new entrant risk while competitive rivalry remains intense with diversified rivals. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Kodak.

Suppliers Bargaining Power

Volatility of essential raw materials

Kodak’s offset plates and specialty films depend on aluminum and silver, commodities whose prices swung 18% and 23% respectively from 2020–2025, keeping supplier power high and input costs volatile.

When aluminum or silver spikes, Kodak can’t fully pass costs to printers in a price-competitive market, squeezing gross margins—Kodak’s materials cost represented ~28% of COGS in 2024.

To blunt supplier leverage, Kodak pursues strategic sourcing and multi-year contracts; in 2023 it secured a two-year aluminum agreement covering ~60% of plate production needs.

Specialized chemical precursors

As Kodak grows its Advanced Materials and Chemicals division, it depends on a small set of global suppliers for specialized chemical precursors, giving those vendors strong pricing and delivery leverage; for example, top 5 suppliers control roughly 60% of the specialty precursor market as of 2025. This concentration raises cost and supply risk for proprietary inputs used in battery and pharmaceutical applications, where single-source components can add 10–25% to input costs. Kodak’s innovation pace is therefore partly tied to supplier reliability and cooperative IP arrangements, and any disruption could delay product launches and hit margins.

Energy and logistics costs

Kodak’s advanced-materials manufacturing is energy-heavy, so utility tariff hikes—US industrial electricity up 9.8% year-over-year in 2024—raise input costs and give suppliers pricing power over margins.

Post-2024 fuel volatility (Brent crude ranged $70–$95/barrel in 2025) increases shipping costs for heavy plates and chemicals, pushing global transport bills up ~12% for similar manufacturers.

These systemic, often non-negotiable costs force Kodak to cut waste, boost yield and shift sourcing; improving energy efficiency by 5–10% can offset a material share of margin pressure.

Technological dependence on component manufacturers

Kodak depends on third-party suppliers for sensors and semiconductors in its PROSPER and ULTRASTREAM digital print lines, giving big electronics firms bargaining power that can raise COGS or delay launches.

In 2024 global semiconductor shortages pushed component lead times to 20–28 weeks, and a 10% component cost rise would cut gross margin on these lines by ~3–4 percentage points.

- Design control: Kodak owns inkjet heads; suppliers control chips

- Lead-time risk: 20–28 weeks in 2024

- Cost exposure: 10% part-price rise → ~3–4 pp margin hit

Switching costs for proprietary inputs

Kodak’s proprietary processes use specific material grades matched to its machinery, creating supplier lock-in; switching would need months and CAPEX likely in the mid-seven figures (estimated $2–10M) to recalibrate lines.

Suppliers know this and can press harder at renewals—Kodak’s input spend was about $420M in 2024, so even a 2–5% price increase would add $8.4–21M to costs.

- Unique grades required

- Recalibration CAPEX $2–10M

- 2024 input spend $420M

- 2–5% price hike = $8.4–21M impact

Supplier concentration and commodity swings threaten Kodak margins—$8–21M shock risk

Suppliers hold high leverage over Kodak due to commodity price swings (aluminum ±18%, silver ±23% 2020–2025), concentrated specialty-precursor markets (top 5 ≈60% share in 2025), semiconductor lead-times (20–28 weeks in 2024) and energy/shipping cost rises (US industrial electricity +9.8% in 2024; transport +~12% 2025), making input-cost volatility and single-source lock-in a persistent margin risk.

| Metric | Value |

|---|---|

| Aluminum price swing (2020–2025) | ±18% |

| Silver price swing (2020–2025) | ±23% |

| Top-5 specialty precursor share (2025) | ≈60% |

| Semiconductor lead-times (2024) | 20–28 weeks |

| US industrial electricity change (2024) | +9.8% |

| Transport cost change (2025 est.) | +~12% |

| Kodak input spend (2024) | $420M |

| 2–5% supplier price shock impact | $8.4–21M |

What is included in the product

Tailored exclusively for Kodak, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping Kodak's pricing power and market resilience.

Compact Porter’s Five Forces summary tailored to Kodak—quickly spot competitive threats and opportunities to guide turnaround or licensing strategies.

Customers Bargaining Power

Consolidation of commercial printing firms

Industry consolidation through 2025 cut US commercial printers by ~28% since 2015, leaving ~4,200 firms but with top 50 customers accounting for ~42% of industry revenue; those large buyers extract volume discounts of 10–18% and push 60–90 day payment terms, squeezing Kodak’s gross margins by several percentage points.

Availability of competitive alternatives

Customers in graphic communications can choose from HP, Canon, Fujifilm and others; global print equipment shipments totaled ~9.8 million units in 2024, keeping supplier options broad and competitive.

Buyers leverage bids to pit manufacturers against each other, with enterprise deals often seeing 5–8 vendors in RFPs and price concessions of 6–12% on average in 2024.

Commodity consumables (inks, plates) show low differentiation; private-label and switch rates rose to ~28% of purchases in 2024, so price drives brand switching.

Price sensitivity in the packaging sector

Packaging customers are highly price-sensitive: carton and flexible-pack printers run on margins often below 5%, so consumable cost—inks, printheads—drives buying decisions.

They demand high-performance inkjet that lowers total cost of ownership (TCO); Kodak must innovate to cut ink use and waste or risk losing deals.

If Kodak’s presses don’t show clear ROI—e.g., >15% faster throughput or ≥10% waste cut—buyers switch to cheaper suppliers.

Low switching costs for certain consumables

Low technical barriers in offset plates and chemicals mean printers can switch brands easily; in 2024 global plate replacement volume saw price-driven churn as 12–18% of buyers switched suppliers annually in some markets.

Kodak’s SONORA solvent-free plates offer lower CO2 and waste, but if SONORA’s price premium exceeds ~10–15% buyers often revert to processed plates, capping Kodak’s pricing power.

- Low switching costs → higher customer bargaining power

- SONORA premium cap ≈ 10–15%

- 12–18% annual supplier churn in price-sensitive segments

Demand for integrated software solutions

Modern print buyers want end-to-end workflow automation, shifting bargaining power to vendors with flexible software; 72% of print firms in a 2024 Smithers survey prioritized software over new presses when upgrading.

If Kodak’s PRINERGY loses interoperability leadership, customers may switch to open-source or competitor ecosystems, risking revenue and recurring software fees.

This forces Kodak to spend heavily—Kodak reported $120m R&D in 2024—so hardware stays relevant to customers’ digital stacks.

- 72% of firms prioritize software (Smithers 2024)

- Kodak R&D $120m (2024 annual report)

- PRINERGY interoperability critical to recurring fees

- Risk: migration to open-source/competitors

Buyers wield power: Top50=42% rev, 10–18% discounts, 12–18% churn

Buyers hold strong power: top 50 account ~42% revenue, extract 10–18% discounts and 60–90 day terms; switch rates 12–18% in price-sensitive segments; SONORA premium capped ~10–15%; 72% prioritize software (Smithers 2024); Kodak R&D $120m (2024).

| Metric | Value |

|---|---|

| Top50 revenue | ~42% |

| Discounts | 10–18% |

| Switch rate | 12–18% |

| SONORA premium cap | 10–15% |

Full Version Awaits

Kodak Porter's Five Forces Analysis

This preview shows the exact Kodak Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kodak faces moderate buyer power and substitution threats as it pivots from legacy film to niche imaging and commercial print; supplier concentration and capital needs temper new entrant risk while competitive rivalry remains intense with diversified rivals. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Kodak.

Suppliers Bargaining Power

Volatility of essential raw materials

Kodak’s offset plates and specialty films depend on aluminum and silver, commodities whose prices swung 18% and 23% respectively from 2020–2025, keeping supplier power high and input costs volatile.

When aluminum or silver spikes, Kodak can’t fully pass costs to printers in a price-competitive market, squeezing gross margins—Kodak’s materials cost represented ~28% of COGS in 2024.

To blunt supplier leverage, Kodak pursues strategic sourcing and multi-year contracts; in 2023 it secured a two-year aluminum agreement covering ~60% of plate production needs.

Specialized chemical precursors

As Kodak grows its Advanced Materials and Chemicals division, it depends on a small set of global suppliers for specialized chemical precursors, giving those vendors strong pricing and delivery leverage; for example, top 5 suppliers control roughly 60% of the specialty precursor market as of 2025. This concentration raises cost and supply risk for proprietary inputs used in battery and pharmaceutical applications, where single-source components can add 10–25% to input costs. Kodak’s innovation pace is therefore partly tied to supplier reliability and cooperative IP arrangements, and any disruption could delay product launches and hit margins.

Energy and logistics costs

Kodak’s advanced-materials manufacturing is energy-heavy, so utility tariff hikes—US industrial electricity up 9.8% year-over-year in 2024—raise input costs and give suppliers pricing power over margins.

Post-2024 fuel volatility (Brent crude ranged $70–$95/barrel in 2025) increases shipping costs for heavy plates and chemicals, pushing global transport bills up ~12% for similar manufacturers.

These systemic, often non-negotiable costs force Kodak to cut waste, boost yield and shift sourcing; improving energy efficiency by 5–10% can offset a material share of margin pressure.

Technological dependence on component manufacturers

Kodak depends on third-party suppliers for sensors and semiconductors in its PROSPER and ULTRASTREAM digital print lines, giving big electronics firms bargaining power that can raise COGS or delay launches.

In 2024 global semiconductor shortages pushed component lead times to 20–28 weeks, and a 10% component cost rise would cut gross margin on these lines by ~3–4 percentage points.

- Design control: Kodak owns inkjet heads; suppliers control chips

- Lead-time risk: 20–28 weeks in 2024

- Cost exposure: 10% part-price rise → ~3–4 pp margin hit

Switching costs for proprietary inputs

Kodak’s proprietary processes use specific material grades matched to its machinery, creating supplier lock-in; switching would need months and CAPEX likely in the mid-seven figures (estimated $2–10M) to recalibrate lines.

Suppliers know this and can press harder at renewals—Kodak’s input spend was about $420M in 2024, so even a 2–5% price increase would add $8.4–21M to costs.

- Unique grades required

- Recalibration CAPEX $2–10M

- 2024 input spend $420M

- 2–5% price hike = $8.4–21M impact

Supplier concentration and commodity swings threaten Kodak margins—$8–21M shock risk

Suppliers hold high leverage over Kodak due to commodity price swings (aluminum ±18%, silver ±23% 2020–2025), concentrated specialty-precursor markets (top 5 ≈60% share in 2025), semiconductor lead-times (20–28 weeks in 2024) and energy/shipping cost rises (US industrial electricity +9.8% in 2024; transport +~12% 2025), making input-cost volatility and single-source lock-in a persistent margin risk.

| Metric | Value |

|---|---|

| Aluminum price swing (2020–2025) | ±18% |

| Silver price swing (2020–2025) | ±23% |

| Top-5 specialty precursor share (2025) | ≈60% |

| Semiconductor lead-times (2024) | 20–28 weeks |

| US industrial electricity change (2024) | +9.8% |

| Transport cost change (2025 est.) | +~12% |

| Kodak input spend (2024) | $420M |

| 2–5% supplier price shock impact | $8.4–21M |

What is included in the product

Tailored exclusively for Kodak, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping Kodak's pricing power and market resilience.

Compact Porter’s Five Forces summary tailored to Kodak—quickly spot competitive threats and opportunities to guide turnaround or licensing strategies.

Customers Bargaining Power

Consolidation of commercial printing firms

Industry consolidation through 2025 cut US commercial printers by ~28% since 2015, leaving ~4,200 firms but with top 50 customers accounting for ~42% of industry revenue; those large buyers extract volume discounts of 10–18% and push 60–90 day payment terms, squeezing Kodak’s gross margins by several percentage points.

Availability of competitive alternatives

Customers in graphic communications can choose from HP, Canon, Fujifilm and others; global print equipment shipments totaled ~9.8 million units in 2024, keeping supplier options broad and competitive.

Buyers leverage bids to pit manufacturers against each other, with enterprise deals often seeing 5–8 vendors in RFPs and price concessions of 6–12% on average in 2024.

Commodity consumables (inks, plates) show low differentiation; private-label and switch rates rose to ~28% of purchases in 2024, so price drives brand switching.

Price sensitivity in the packaging sector

Packaging customers are highly price-sensitive: carton and flexible-pack printers run on margins often below 5%, so consumable cost—inks, printheads—drives buying decisions.

They demand high-performance inkjet that lowers total cost of ownership (TCO); Kodak must innovate to cut ink use and waste or risk losing deals.

If Kodak’s presses don’t show clear ROI—e.g., >15% faster throughput or ≥10% waste cut—buyers switch to cheaper suppliers.

Low switching costs for certain consumables

Low technical barriers in offset plates and chemicals mean printers can switch brands easily; in 2024 global plate replacement volume saw price-driven churn as 12–18% of buyers switched suppliers annually in some markets.

Kodak’s SONORA solvent-free plates offer lower CO2 and waste, but if SONORA’s price premium exceeds ~10–15% buyers often revert to processed plates, capping Kodak’s pricing power.

- Low switching costs → higher customer bargaining power

- SONORA premium cap ≈ 10–15%

- 12–18% annual supplier churn in price-sensitive segments

Demand for integrated software solutions

Modern print buyers want end-to-end workflow automation, shifting bargaining power to vendors with flexible software; 72% of print firms in a 2024 Smithers survey prioritized software over new presses when upgrading.

If Kodak’s PRINERGY loses interoperability leadership, customers may switch to open-source or competitor ecosystems, risking revenue and recurring software fees.

This forces Kodak to spend heavily—Kodak reported $120m R&D in 2024—so hardware stays relevant to customers’ digital stacks.

- 72% of firms prioritize software (Smithers 2024)

- Kodak R&D $120m (2024 annual report)

- PRINERGY interoperability critical to recurring fees

- Risk: migration to open-source/competitors

Buyers wield power: Top50=42% rev, 10–18% discounts, 12–18% churn

Buyers hold strong power: top 50 account ~42% revenue, extract 10–18% discounts and 60–90 day terms; switch rates 12–18% in price-sensitive segments; SONORA premium capped ~10–15%; 72% prioritize software (Smithers 2024); Kodak R&D $120m (2024).

| Metric | Value |

|---|---|

| Top50 revenue | ~42% |

| Discounts | 10–18% |

| Switch rate | 12–18% |

| SONORA premium cap | 10–15% |

Full Version Awaits

Kodak Porter's Five Forces Analysis

This preview shows the exact Kodak Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.