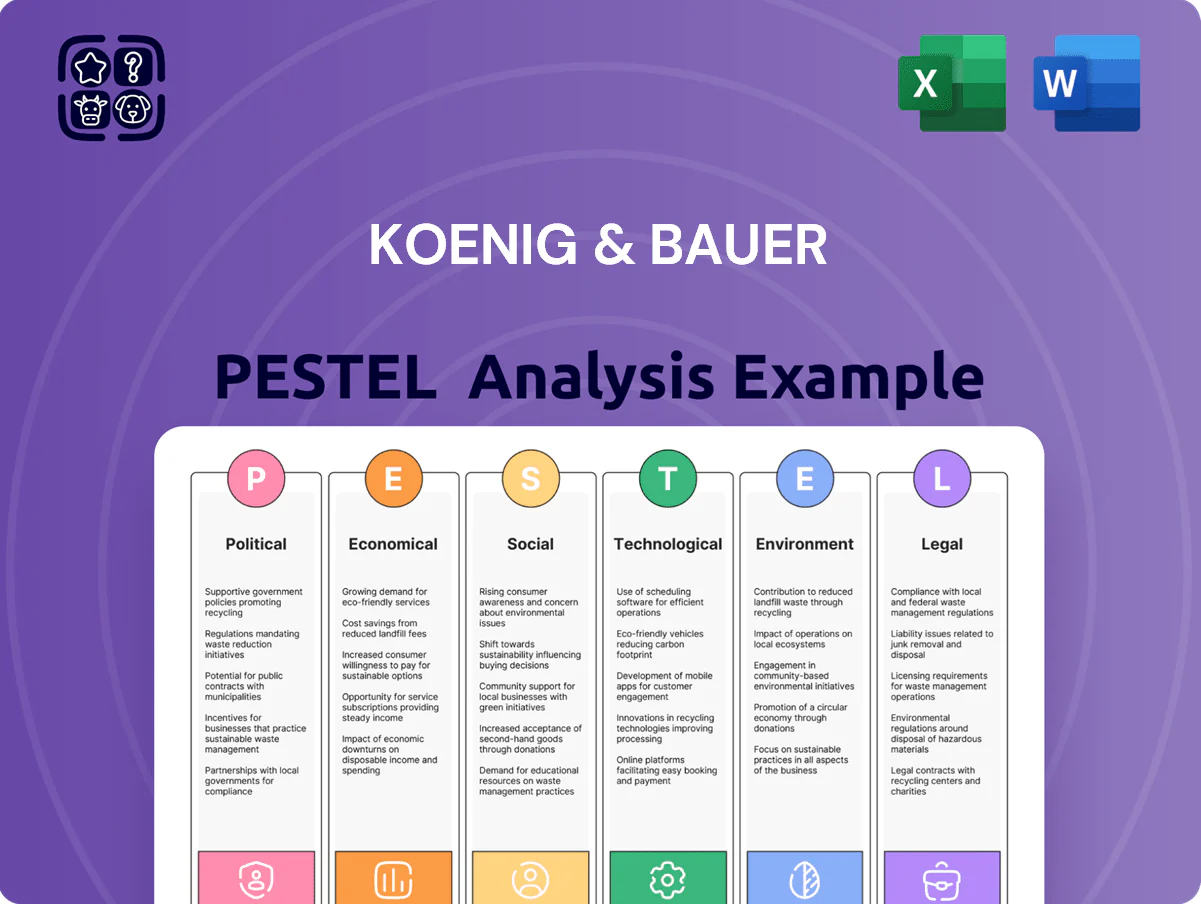

Koenig & Bauer PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic cycles, and emerging technologies are shaping Koenig & Bauer’s strategic path—our PESTLE delivers concise, actionable insights to inform investment and competitive decisions; buy the full analysis for the complete, editable report and immediate download.

Political factors

Global trade policy and tariffs

Koenig & Bauer, with exports accounting for about 75% of group sales in 2024 (€1.29bn total revenue in 2024), is highly exposed to shifts in EU-China-US trade relations; US and Chinese tariffs on machinery could erode margins and market share.

A 10% tariff on presses to China or the US would raise delivered costs materially, reducing price competitiveness versus local producers and potentially cutting unit volumes in growth markets.

Rising protectionism—EU safeguard measures or export controls on high-tech equipment—requires scenario planning, supply-chain diversification, and local assembly options to mitigate border-related risks.

Security printing and national sovereignty

As a dominant banknote printer, Koenig & Bauer is directly affected by central bank and sovereign procurement—central banks globally spent an estimated $6.5bn on banknote production in 2023, shaping orders and margins.

Political stability in emerging markets matters: Latin America, Africa and Southeast Asia accounted for ~42% of new currency issuance value in 2024, driving demand for advanced security features.

Shifts in government can alter procurement timing or force localizing production; recent moves—e.g., Nigeria and Ghana increasing domestic printing capacity in 2024—show procurement cycles and facility locations respond to political mandates.

EU industrial and digital subsidies

EU political backing for the Green Deal and digital transformation opens grant and subsidy channels—EU budget 2021–27 allocates about €200bn for single market/industrial policy and the Recovery and Resilience Facility has disbursed €800bn, offering Koenig & Bauer access to R&D and decarbonization funds.

Initiatives to modernize European manufacturing via Industry 4.0 create opportunities for the company to secure funding for automation and IoT integration, supporting capital expenditure and product development.

Dependence on these subsidies requires strict compliance with shifting EU priorities on industrial decarbonization and strategic technological autonomy, risk-managing potential funding conditionality and audit requirements.

Geopolitical instability in supply chains

- 35% rise in European industrial gas prices (2024)

- 18% increase in local supplier contracts (2024)

- 12% higher capex allocation to resilient sourcing

Export control regulations

Export controls under Germany's AWV and EU Dual-Use Regulation restrict sales of advanced press technologies to sanctioned states; in 2024 Germany issued over 5,000 export licenses with tighter scrutiny on high-tech machinery affecting Koenig & Bauer's market access.

Compliance with EU/US sanctions requires a legal framework—2023 EU fines topped €1.2bn across sectors—so lapses risk severe penalties and reputational loss for the company.

Rapid foreign-policy shifts (e.g., 2022–24 trade restrictions vs. Russia) can cut revenues from affected regions, forcing Koenig & Bauer to keep flexible sales channels and diversified geographic exposure.

- Strict AWV/EU dual-use rules limit sales to certain jurisdictions

- 2023–24 enforcement shows high fines; robust compliance mandatory

- Policy shifts can abruptly close markets—diversification required

Koenig & Bauer bets on resilience amid export, tariff and gas-price pressures

Koenig & Bauer faces trade/tariff risks (exports ~75% of €1.29bn 2024 revenue), dependence on central bank procurement (global banknote spend ~$6.5bn in 2023), and exposure to EU export controls; 2024 actions: +18% local suppliers, +12% capex to resilience, amid 35% rise in European industrial gas prices.

| Metric | 2023–24 |

|---|---|

| Revenue 2024 | €1.29bn |

| Export share | ~75% |

| Banknote market | $6.5bn (2023) |

| Local suppliers | +18% |

| Capex reallocated | +12% |

| Gas prices EU | +35% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Koenig & Bauer, with data-driven trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, easily shareable PESTLE summary for Koenig & Bauer that’s visually segmented by category, enabling quick interpretation in meetings or presentations and allowing users to add notes for their region or business line.

Economic factors

Capital expenditure cycles in packaging

The demand for Koenig & Bauer printing machinery is highly sensitive to capex cycles in global packaging and commercial printing; during the 2020–2023 downturn order intake fell, with industry capex down an estimated 12% in 2020 and only recovering by 2022–23. Economic slowdowns typically delay large-scale equipment purchases, reducing Koenig & Bauer’s near-term revenue, while a strong 2024–25 recovery—global packaging spend projected to grow ~4–6% annually—drives upgrades to high-speed, energy-efficient presses supporting higher order volumes.

Interest rate environment and financing

High interest rates raise financing costs for customers, reducing demand for Koenig & Bauer’s capital-intensive presses; ECB rates rose to 4.25% in 2024, squeezing buyer affordability. Koenig & Bauer often offers or arranges customer financing, so group order intake is sensitive to global rate moves—FY2023 order intake fell 8.7% versus 2022 amid tighter credit. As central banks cut or hike to tame inflation, K&B must adjust financing terms and risk pricing to keep sales and investor appeal.

Raw material and energy price volatility

The heavy machinery manufacturing of Koenig & Bauer is energy-intensive and depends on steel, aluminum and specialized electronics; with steel hot-rolled coil up ~15% in 2024 and aluminum LME prices averaging $2,400/ton in 2025, input cost swings squeeze margins. Fluctuations in global commodity prices forced COGS adjustments and price revisions—Q3 2024 gross margin volatility of ±180 bps reflected this. Energy market instability, with EU gas prices ranging €30–€70/MWh in 2024, raises manufacturing cost uncertainty. Predictable energy markets are therefore critical to sustain long-term profitability and plan capital-intensive production.

Currency exchange rate fluctuations

With roughly 60% of Koenig & Bauer sales generated outside the Eurozone, currency translation and transaction risks materially affect reported revenue and margins; a 10% euro appreciation in 2024 would have cut non-euro revenue competitiveness versus peers by roughly the same magnitude.

A strong euro raises German-made unit prices against Japanese and Chinese rivals—in 2023-24 export markets, price-sensitive segments saw order intake declines up to mid-single digits when EUR strength surged.

Koenig & Bauer uses active hedging (forward contracts) and expanded local sourcing/production in India and China to shield margins; localized plants accounted for about 18% of capacity by 2025, reducing transactional exposure.

- ~60% revenue outside Eurozone

- 10% EUR appreciation ≈ 10% competitiveness hit

- Order intake volatility: up to mid-single-digit declines

- Localized capacity ~18% by 2025; active forward hedging

Growth in emerging market consumption

Rising disposable incomes in Asia and Latin America—middle-class households expected to reach ~3.8 billion by 2030—boost demand for packaged goods, driving need for premium printing and labeling solutions from Koenig & Bauer; EM sales grew ~6–8% YoY in similar sectors in 2024. Koenig & Bauer’s revenue exposure to EMs is rising as it expands manufacturing and service hubs to offset flat growth in Europe/North America.

- Middle class expansion (~3.8B by 2030) increases packaged goods demand

- EM printing/labeling sales up ~6–8% YoY in 2024

- Strategic EM expansion hedges mature-market stagnation

- Revenue mix shifting toward Asia/Latin America

Koenig & Bauer hit by 2023 order slump; packaging demand and localization offer recovery

Koenig & Bauer order intake is cyclical with capex; 2020–23 saw ~12% capex drop then recovery—packaging spend set to grow ~4–6% p.a. in 2024–25. ECB rates at 4.25% in 2024 tightened financing; FY2023 orders fell 8.7%. Input costs rose (hot-rolled coil +15% in 2024; aluminum ~$2,400/t in 2025) squeezing margins; localized capacity ~18% by 2025 and ~60% revenue outside Eurozone mitigate FX and cost risks.

| Metric | Value |

|---|---|

| FY2023 order change | -8.7% |

| Packaging spend growth 2024–25 | 4–6% p.a. |

| ECB rate 2024 | 4.25% |

| Steel HRC change 2024 | +15% |

| Aluminum 2025 | $2,400/t |

| Revenue outside Eurozone | ~60% |

| Localized capacity 2025 | ~18% |

Preview Before You Purchase

Koenig & Bauer PESTLE Analysis

The preview shown here is the exact Koenig & Bauer PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, economic cycles, and emerging technologies are shaping Koenig & Bauer’s strategic path—our PESTLE delivers concise, actionable insights to inform investment and competitive decisions; buy the full analysis for the complete, editable report and immediate download.

Political factors

Global trade policy and tariffs

Koenig & Bauer, with exports accounting for about 75% of group sales in 2024 (€1.29bn total revenue in 2024), is highly exposed to shifts in EU-China-US trade relations; US and Chinese tariffs on machinery could erode margins and market share.

A 10% tariff on presses to China or the US would raise delivered costs materially, reducing price competitiveness versus local producers and potentially cutting unit volumes in growth markets.

Rising protectionism—EU safeguard measures or export controls on high-tech equipment—requires scenario planning, supply-chain diversification, and local assembly options to mitigate border-related risks.

Security printing and national sovereignty

As a dominant banknote printer, Koenig & Bauer is directly affected by central bank and sovereign procurement—central banks globally spent an estimated $6.5bn on banknote production in 2023, shaping orders and margins.

Political stability in emerging markets matters: Latin America, Africa and Southeast Asia accounted for ~42% of new currency issuance value in 2024, driving demand for advanced security features.

Shifts in government can alter procurement timing or force localizing production; recent moves—e.g., Nigeria and Ghana increasing domestic printing capacity in 2024—show procurement cycles and facility locations respond to political mandates.

EU industrial and digital subsidies

EU political backing for the Green Deal and digital transformation opens grant and subsidy channels—EU budget 2021–27 allocates about €200bn for single market/industrial policy and the Recovery and Resilience Facility has disbursed €800bn, offering Koenig & Bauer access to R&D and decarbonization funds.

Initiatives to modernize European manufacturing via Industry 4.0 create opportunities for the company to secure funding for automation and IoT integration, supporting capital expenditure and product development.

Dependence on these subsidies requires strict compliance with shifting EU priorities on industrial decarbonization and strategic technological autonomy, risk-managing potential funding conditionality and audit requirements.

Geopolitical instability in supply chains

- 35% rise in European industrial gas prices (2024)

- 18% increase in local supplier contracts (2024)

- 12% higher capex allocation to resilient sourcing

Export control regulations

Export controls under Germany's AWV and EU Dual-Use Regulation restrict sales of advanced press technologies to sanctioned states; in 2024 Germany issued over 5,000 export licenses with tighter scrutiny on high-tech machinery affecting Koenig & Bauer's market access.

Compliance with EU/US sanctions requires a legal framework—2023 EU fines topped €1.2bn across sectors—so lapses risk severe penalties and reputational loss for the company.

Rapid foreign-policy shifts (e.g., 2022–24 trade restrictions vs. Russia) can cut revenues from affected regions, forcing Koenig & Bauer to keep flexible sales channels and diversified geographic exposure.

- Strict AWV/EU dual-use rules limit sales to certain jurisdictions

- 2023–24 enforcement shows high fines; robust compliance mandatory

- Policy shifts can abruptly close markets—diversification required

Koenig & Bauer bets on resilience amid export, tariff and gas-price pressures

Koenig & Bauer faces trade/tariff risks (exports ~75% of €1.29bn 2024 revenue), dependence on central bank procurement (global banknote spend ~$6.5bn in 2023), and exposure to EU export controls; 2024 actions: +18% local suppliers, +12% capex to resilience, amid 35% rise in European industrial gas prices.

| Metric | 2023–24 |

|---|---|

| Revenue 2024 | €1.29bn |

| Export share | ~75% |

| Banknote market | $6.5bn (2023) |

| Local suppliers | +18% |

| Capex reallocated | +12% |

| Gas prices EU | +35% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Koenig & Bauer, with data-driven trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

A concise, easily shareable PESTLE summary for Koenig & Bauer that’s visually segmented by category, enabling quick interpretation in meetings or presentations and allowing users to add notes for their region or business line.

Economic factors

Capital expenditure cycles in packaging

The demand for Koenig & Bauer printing machinery is highly sensitive to capex cycles in global packaging and commercial printing; during the 2020–2023 downturn order intake fell, with industry capex down an estimated 12% in 2020 and only recovering by 2022–23. Economic slowdowns typically delay large-scale equipment purchases, reducing Koenig & Bauer’s near-term revenue, while a strong 2024–25 recovery—global packaging spend projected to grow ~4–6% annually—drives upgrades to high-speed, energy-efficient presses supporting higher order volumes.

Interest rate environment and financing

High interest rates raise financing costs for customers, reducing demand for Koenig & Bauer’s capital-intensive presses; ECB rates rose to 4.25% in 2024, squeezing buyer affordability. Koenig & Bauer often offers or arranges customer financing, so group order intake is sensitive to global rate moves—FY2023 order intake fell 8.7% versus 2022 amid tighter credit. As central banks cut or hike to tame inflation, K&B must adjust financing terms and risk pricing to keep sales and investor appeal.

Raw material and energy price volatility

The heavy machinery manufacturing of Koenig & Bauer is energy-intensive and depends on steel, aluminum and specialized electronics; with steel hot-rolled coil up ~15% in 2024 and aluminum LME prices averaging $2,400/ton in 2025, input cost swings squeeze margins. Fluctuations in global commodity prices forced COGS adjustments and price revisions—Q3 2024 gross margin volatility of ±180 bps reflected this. Energy market instability, with EU gas prices ranging €30–€70/MWh in 2024, raises manufacturing cost uncertainty. Predictable energy markets are therefore critical to sustain long-term profitability and plan capital-intensive production.

Currency exchange rate fluctuations

With roughly 60% of Koenig & Bauer sales generated outside the Eurozone, currency translation and transaction risks materially affect reported revenue and margins; a 10% euro appreciation in 2024 would have cut non-euro revenue competitiveness versus peers by roughly the same magnitude.

A strong euro raises German-made unit prices against Japanese and Chinese rivals—in 2023-24 export markets, price-sensitive segments saw order intake declines up to mid-single digits when EUR strength surged.

Koenig & Bauer uses active hedging (forward contracts) and expanded local sourcing/production in India and China to shield margins; localized plants accounted for about 18% of capacity by 2025, reducing transactional exposure.

- ~60% revenue outside Eurozone

- 10% EUR appreciation ≈ 10% competitiveness hit

- Order intake volatility: up to mid-single-digit declines

- Localized capacity ~18% by 2025; active forward hedging

Growth in emerging market consumption

Rising disposable incomes in Asia and Latin America—middle-class households expected to reach ~3.8 billion by 2030—boost demand for packaged goods, driving need for premium printing and labeling solutions from Koenig & Bauer; EM sales grew ~6–8% YoY in similar sectors in 2024. Koenig & Bauer’s revenue exposure to EMs is rising as it expands manufacturing and service hubs to offset flat growth in Europe/North America.

- Middle class expansion (~3.8B by 2030) increases packaged goods demand

- EM printing/labeling sales up ~6–8% YoY in 2024

- Strategic EM expansion hedges mature-market stagnation

- Revenue mix shifting toward Asia/Latin America

Koenig & Bauer hit by 2023 order slump; packaging demand and localization offer recovery

Koenig & Bauer order intake is cyclical with capex; 2020–23 saw ~12% capex drop then recovery—packaging spend set to grow ~4–6% p.a. in 2024–25. ECB rates at 4.25% in 2024 tightened financing; FY2023 orders fell 8.7%. Input costs rose (hot-rolled coil +15% in 2024; aluminum ~$2,400/t in 2025) squeezing margins; localized capacity ~18% by 2025 and ~60% revenue outside Eurozone mitigate FX and cost risks.

| Metric | Value |

|---|---|

| FY2023 order change | -8.7% |

| Packaging spend growth 2024–25 | 4–6% p.a. |

| ECB rate 2024 | 4.25% |

| Steel HRC change 2024 | +15% |

| Aluminum 2025 | $2,400/t |

| Revenue outside Eurozone | ~60% |

| Localized capacity 2025 | ~18% |

Preview Before You Purchase

Koenig & Bauer PESTLE Analysis

The preview shown here is the exact Koenig & Bauer PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.