Kofola Boston Consulting Group Matrix

Download Your Competitive Advantage

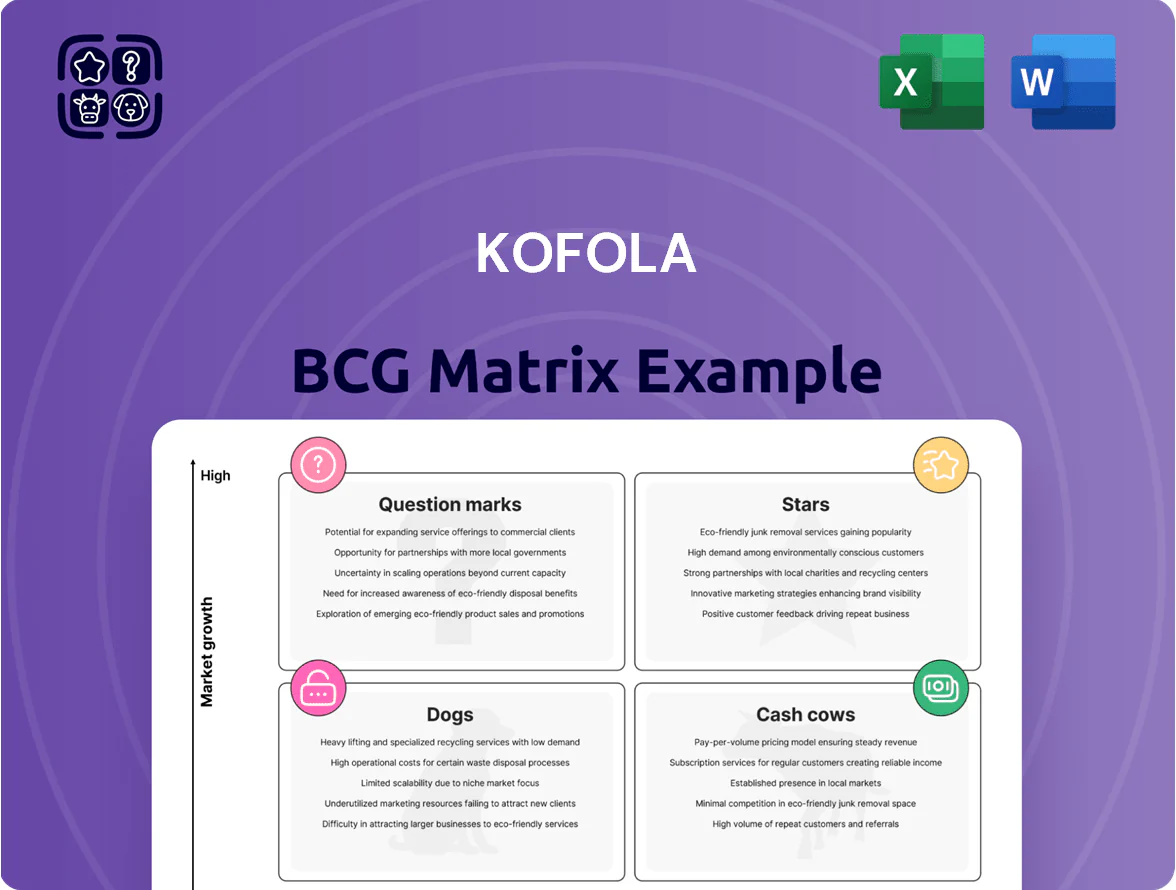

Kofola’s BCG Matrix preview highlights where its beverage brands likely sit amid shifting consumer tastes and competitive pressure—spotting potential Stars and Cash Cows as well as underperforming Dogs and risky Question Marks. Our concise snapshot frames market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files. Purchase the complete report to get actionable strategy, visual mapping, and a clear plan for resource allocation and portfolio optimization.

Stars

UGO Fresh Bars and Salateries

UGO Fresh Bars and Salateries represents Kofola’s health-conscious segment, posting double-digit CAGR and recording ~15% year-on-year growth through Q3 2025, driven by fresh juice and healthy fast-food demand in Czechia and Slovakia.

The unit holds market-leading share—estimated 28% in fresh juices and 22% in healthy fast casual across both markets—supported by 120+ outlets and €28m 2024 revenue.

Significant capex of ~€12–15m over 2026–2027 is needed to add 60 stores and finish digital delivery integration (now 35% of sales) to defend against rising local and international rivals.

Semtex Energy Drinks

In Kofola’s BCG matrix Semtex sits as a Cash Cow: energy drinks are among the fastest-growing non-alcoholic segments, with global CAGR ~7.8% to 2025 (Euromonitor 2024), and Semtex holds an estimated Czech/CEE market share ~22% in 2024 after flavor diversification and gamer/sports targeting.

Maintaining share requires continued marketing spend; Kofola’s 2024 S&A showed marketing at ~7.2% of revenue, and cutting back risks encroachment by Red Bull and Monster, which together control ~55% of global energy sales (2024 Statista).

Premium Coffee Segment

Kofola’s Premium Coffee segment, led by Cafe Reserva, is a Star in the BCG matrix: HoReCa demand grew 18% YoY in 2025 and premium coffee sales rose €12.4m (up 32%); margins are above group average at ~26%.

Functional and Vitamin Waters

Functional and vitamin waters are a Star for Kofola: category revenue grew ~28% y/y in 2024, and Kofola—using brands Rajec and Korunní—holds an estimated 22% share in Czech-Slovak functional water channels as of Q3 2025.

High promotional spend (~6–8% of net sales) is offset by rapid volume growth: retail +32% and convenience +45% in 2024, driving scale advantages and improving gross margins.

- Category growth 28% (2024)

- Kofola market share ~22% (Q3 2025)

- Retail volume +32% (2024)

- Promo spend 6–8% of sales

- Convenience +45% volume (2024)

Adriatic Region Expansion

Kofola’s Adriatic expansion, led by Radenska, is a Star: Southeast Europe volume growth (~4–6% CAGR 2021–25) outpaced Central Europe (≈1–2%), giving Kofola higher unit sales and margin leverage in 2025. Continued outperformance needs capex: planned €25–35m regional investments through 2026 to boost local production efficiency and trade marketing.

- Radenska driving share gains in Slovenia, Croatia, Serbia

- SE Europe growth ~4–6% CAGR 2021–25

- Planned capex €25–35m through 2026

- Higher volume = better fixed-cost absorption

High-growth beverage stars drive €40–50m sales; €37–50m capex fuels 60-store rollout

Stars: UGO, Premium Coffee, Functional Waters, and Adriatic Radenska show 2024–25 CAGR 18–32%, market shares 22–28%, combined 2024 revenue ~€40–50m, promo/marketing 6–8% of sales, planned capex €37–50m (2026–27) to add 60 stores, finish delivery and regional efficiency.

| Unit | 2024 rev (€m) | share (%) | growth 24–25 (%) | capex €m |

|---|---|---|---|---|

| UGO | 28 | 22–28 | ~15 | 12–15 |

| Cafe Reserva | 12.4 | — | 32 | — |

| Functional waters | ~8–10 | 22 | 28 | 5–10 |

| Radenska | — | — | 4–6 CAGR | 25–35 |

What is included in the product

Concise BCG Matrix review of Kofola’s brands: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page Kofola BCG Matrix placing each brand in a quadrant for fast strategic decisions and portfolio clarity.

Cash Cows

Kofola Original Cola

Kofola Original Cola remains the group’s primary liquidity engine, delivering roughly 2024 net sales of ~€140m in CEE markets and sustaining a 40–50% market share in Czechia and Slovakia as of Q4 2024.

With cola category growth near 0–1% annually, Kofola prioritizes cost-per-litre cuts, SKU rationalization, and 3–4% annual margin improvement over share expansion.

Cash flow from Kofola Original funds ~€20–30m annual capex and working-capital needs and underwrites R&D and marketing for question marks and star brands.

Rajec Mineral Water

Rajec Mineral Water, a household name in Slovakia and Czechia, dominates the plain bottled water segment with ~35% market share (2024 Euromonitor) and nature-focused branding that signals purity.

Plain bottled water shows low annual growth (~2% CAGR 2020–24), so Kofola cuts marketing spend and extracts steady margins; Rajec generated ~CZK 650m EBITDA for Kofola in 2024.

The brand supplies reliable cash flow—covering dividends and debt—supporting Kofola’s 2024 net debt/EBITDA of ~1.8x and EUR 0.10 per-share dividend paid in 2024.

Jupí Syrups

Jupí Syrups leads the concentrated syrup market with ~40% market share in CEE (2024 E)(Euromonitor), a category showing high household penetration (~70% of CEE households) but flat CAGR ~0–1% (2021–24).

Production uses mature lines; capex needs are low — maintenance capex ~1–2% of sales, no new plants planned in 2025 per Kofola interim report.

Gross margins ~42% in 2024; Jupí profits contributed an estimated €12–15m to cover group admin costs, supporting Kofola’s EBITDA stability.

Jupík Children Drinks

Jupík Children Drinks holds a high market share in the kids' beverage segment in Czechia and Slovakia, delivering steady revenue—estimated net sales contribution to Kofola Group around 8–10% in 2024 (Kofola consolidated revenue €360m in 2024). Stable birth rates keep market size flat, so Jupík acts as a cash cow, funding other growth bets.

Promotion stays tactical and low-cost, focused on in-store visibility and price promotions; marketing spend for the SKU family is roughly 2–3% of brand revenues, preserving margins and shelf presence without expensive market creation.

- High market share in kids' drinks

- Contributes ~8–10% of Kofola 2024 sales (€360m)

- Stable birth rates → flat market size

- Marketing spend ~2–3% of brand revenues

Vinea Herb-Based Soda

Vinea Herb-Based Soda, rooted in Slovakia’s grape-beverage tradition, holds a dominant niche share (~35% regional share) with stable annual sales ~€12–15m and 4–6% annual decline in category volume, fitting a classic cash cow profile.

The market is mature with low innovation need; marketing and distribution cost ~8% of sales, yielding predictable EBITDA margins near 22%, funding Kofola’s growth bets.

- 35% regional market share

- €12–15m annual sales

- 22% EBITDA margin

- 8% sales in marketing/distribution

- Category volume decline 4–6% yearly

Kofola 2024: Strong cash cows—€207–€212m core sales, low leverage, €0.10 dividend

Kofola cash cows (2024): Kofola Original Cola €140m sales, 40–50% CZ/SK share; Rajec water €~30m sales, ~35% share, CZK 650m EBITDA; Jupí syrups €~25m sales, 40% share, gross margin 42%; Jupík 8–10% group sales; Vinea €12–15m sales, 22% EBITDA. Net debt/EBITDA ~1.8x; dividend €0.10/sh.

| Brand | Sales 2024 | Share | EBITDA/margin |

|---|---|---|---|

| Kofola Original | €140m | 40–50% | — |

| Rajec | €30m | 35% | CZK 650m |

| Jupí | €25m | 40% | 42% GM |

| Vinea | €12–15m | 35% | 22% EBITDA |

Full Transparency, Always

Kofola BCG Matrix

The file you're previewing is the final Kofola BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Kofola’s BCG Matrix preview highlights where its beverage brands likely sit amid shifting consumer tastes and competitive pressure—spotting potential Stars and Cash Cows as well as underperforming Dogs and risky Question Marks. Our concise snapshot frames market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files. Purchase the complete report to get actionable strategy, visual mapping, and a clear plan for resource allocation and portfolio optimization.

Stars

UGO Fresh Bars and Salateries

UGO Fresh Bars and Salateries represents Kofola’s health-conscious segment, posting double-digit CAGR and recording ~15% year-on-year growth through Q3 2025, driven by fresh juice and healthy fast-food demand in Czechia and Slovakia.

The unit holds market-leading share—estimated 28% in fresh juices and 22% in healthy fast casual across both markets—supported by 120+ outlets and €28m 2024 revenue.

Significant capex of ~€12–15m over 2026–2027 is needed to add 60 stores and finish digital delivery integration (now 35% of sales) to defend against rising local and international rivals.

Semtex Energy Drinks

In Kofola’s BCG matrix Semtex sits as a Cash Cow: energy drinks are among the fastest-growing non-alcoholic segments, with global CAGR ~7.8% to 2025 (Euromonitor 2024), and Semtex holds an estimated Czech/CEE market share ~22% in 2024 after flavor diversification and gamer/sports targeting.

Maintaining share requires continued marketing spend; Kofola’s 2024 S&A showed marketing at ~7.2% of revenue, and cutting back risks encroachment by Red Bull and Monster, which together control ~55% of global energy sales (2024 Statista).

Premium Coffee Segment

Kofola’s Premium Coffee segment, led by Cafe Reserva, is a Star in the BCG matrix: HoReCa demand grew 18% YoY in 2025 and premium coffee sales rose €12.4m (up 32%); margins are above group average at ~26%.

Functional and Vitamin Waters

Functional and vitamin waters are a Star for Kofola: category revenue grew ~28% y/y in 2024, and Kofola—using brands Rajec and Korunní—holds an estimated 22% share in Czech-Slovak functional water channels as of Q3 2025.

High promotional spend (~6–8% of net sales) is offset by rapid volume growth: retail +32% and convenience +45% in 2024, driving scale advantages and improving gross margins.

- Category growth 28% (2024)

- Kofola market share ~22% (Q3 2025)

- Retail volume +32% (2024)

- Promo spend 6–8% of sales

- Convenience +45% volume (2024)

Adriatic Region Expansion

Kofola’s Adriatic expansion, led by Radenska, is a Star: Southeast Europe volume growth (~4–6% CAGR 2021–25) outpaced Central Europe (≈1–2%), giving Kofola higher unit sales and margin leverage in 2025. Continued outperformance needs capex: planned €25–35m regional investments through 2026 to boost local production efficiency and trade marketing.

- Radenska driving share gains in Slovenia, Croatia, Serbia

- SE Europe growth ~4–6% CAGR 2021–25

- Planned capex €25–35m through 2026

- Higher volume = better fixed-cost absorption

High-growth beverage stars drive €40–50m sales; €37–50m capex fuels 60-store rollout

Stars: UGO, Premium Coffee, Functional Waters, and Adriatic Radenska show 2024–25 CAGR 18–32%, market shares 22–28%, combined 2024 revenue ~€40–50m, promo/marketing 6–8% of sales, planned capex €37–50m (2026–27) to add 60 stores, finish delivery and regional efficiency.

| Unit | 2024 rev (€m) | share (%) | growth 24–25 (%) | capex €m |

|---|---|---|---|---|

| UGO | 28 | 22–28 | ~15 | 12–15 |

| Cafe Reserva | 12.4 | — | 32 | — |

| Functional waters | ~8–10 | 22 | 28 | 5–10 |

| Radenska | — | — | 4–6 CAGR | 25–35 |

What is included in the product

Concise BCG Matrix review of Kofola’s brands: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page Kofola BCG Matrix placing each brand in a quadrant for fast strategic decisions and portfolio clarity.

Cash Cows

Kofola Original Cola

Kofola Original Cola remains the group’s primary liquidity engine, delivering roughly 2024 net sales of ~€140m in CEE markets and sustaining a 40–50% market share in Czechia and Slovakia as of Q4 2024.

With cola category growth near 0–1% annually, Kofola prioritizes cost-per-litre cuts, SKU rationalization, and 3–4% annual margin improvement over share expansion.

Cash flow from Kofola Original funds ~€20–30m annual capex and working-capital needs and underwrites R&D and marketing for question marks and star brands.

Rajec Mineral Water

Rajec Mineral Water, a household name in Slovakia and Czechia, dominates the plain bottled water segment with ~35% market share (2024 Euromonitor) and nature-focused branding that signals purity.

Plain bottled water shows low annual growth (~2% CAGR 2020–24), so Kofola cuts marketing spend and extracts steady margins; Rajec generated ~CZK 650m EBITDA for Kofola in 2024.

The brand supplies reliable cash flow—covering dividends and debt—supporting Kofola’s 2024 net debt/EBITDA of ~1.8x and EUR 0.10 per-share dividend paid in 2024.

Jupí Syrups

Jupí Syrups leads the concentrated syrup market with ~40% market share in CEE (2024 E)(Euromonitor), a category showing high household penetration (~70% of CEE households) but flat CAGR ~0–1% (2021–24).

Production uses mature lines; capex needs are low — maintenance capex ~1–2% of sales, no new plants planned in 2025 per Kofola interim report.

Gross margins ~42% in 2024; Jupí profits contributed an estimated €12–15m to cover group admin costs, supporting Kofola’s EBITDA stability.

Jupík Children Drinks

Jupík Children Drinks holds a high market share in the kids' beverage segment in Czechia and Slovakia, delivering steady revenue—estimated net sales contribution to Kofola Group around 8–10% in 2024 (Kofola consolidated revenue €360m in 2024). Stable birth rates keep market size flat, so Jupík acts as a cash cow, funding other growth bets.

Promotion stays tactical and low-cost, focused on in-store visibility and price promotions; marketing spend for the SKU family is roughly 2–3% of brand revenues, preserving margins and shelf presence without expensive market creation.

- High market share in kids' drinks

- Contributes ~8–10% of Kofola 2024 sales (€360m)

- Stable birth rates → flat market size

- Marketing spend ~2–3% of brand revenues

Vinea Herb-Based Soda

Vinea Herb-Based Soda, rooted in Slovakia’s grape-beverage tradition, holds a dominant niche share (~35% regional share) with stable annual sales ~€12–15m and 4–6% annual decline in category volume, fitting a classic cash cow profile.

The market is mature with low innovation need; marketing and distribution cost ~8% of sales, yielding predictable EBITDA margins near 22%, funding Kofola’s growth bets.

- 35% regional market share

- €12–15m annual sales

- 22% EBITDA margin

- 8% sales in marketing/distribution

- Category volume decline 4–6% yearly

Kofola 2024: Strong cash cows—€207–€212m core sales, low leverage, €0.10 dividend

Kofola cash cows (2024): Kofola Original Cola €140m sales, 40–50% CZ/SK share; Rajec water €~30m sales, ~35% share, CZK 650m EBITDA; Jupí syrups €~25m sales, 40% share, gross margin 42%; Jupík 8–10% group sales; Vinea €12–15m sales, 22% EBITDA. Net debt/EBITDA ~1.8x; dividend €0.10/sh.

| Brand | Sales 2024 | Share | EBITDA/margin |

|---|---|---|---|

| Kofola Original | €140m | 40–50% | — |

| Rajec | €30m | 35% | CZK 650m |

| Jupí | €25m | 40% | 42% GM |

| Vinea | €12–15m | 35% | 22% EBITDA |

Full Transparency, Always

Kofola BCG Matrix

The file you're previewing is the final Kofola BCG Matrix you'll receive after purchase — no watermarks, no demo content, just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.