Korea Gas Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

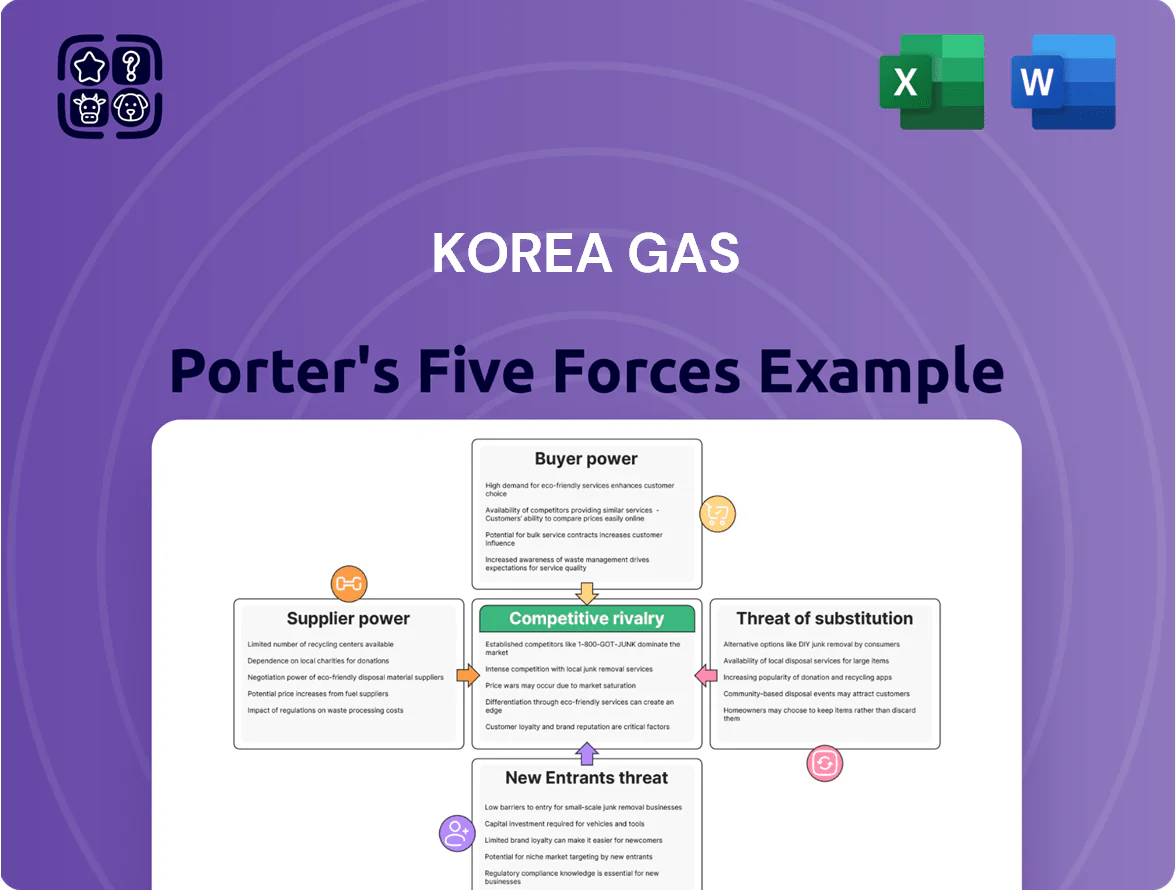

Korea Gas faces moderate supplier power and regulatory scrutiny, with steady domestic demand but rising competition from renewable substitutes narrowing margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Korea Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global LNG Producers

The global LNG market is highly concentrated: Qatar, the United States, and Australia supplied about 60% of seaborne LNG in 2024, giving these exporters strong pricing power over buyers like KOGAS.

KOGAS sources roughly 70–80% of South Korea’s gas imports from these suppliers, so it often acts as a price-taker in long-term contracts and spot purchases.

As of late 2025, few alternative large-scale suppliers exist, keeping bargaining power tilted toward exporters and pressuring KOGAS’s procurement costs.

Rigidity of Long-Term Take-or-Pay Contracts

Geopolitical Influence on Supply Routes

Geopolitical tensions in the Middle East and chokepoints like the Strait of Hormuz repeatedly threaten supply stability; disruptions in 2024 pushed spot LNG premiums up to 45% above long-term contract prices, boosting suppliers in low-risk jurisdictions. KOGAS must navigate sanctions and rerouting costs—shipping detours added ~8–12% to freight per cargo in 2024—so suppliers in stable regions gain pricing leverage. This raises supplier bargaining power and spot-market dependency for Korea Gas.

Competition for Spot Market Volumes

KOGAS competes with major Asian buyers and European importers for spot LNG to meet seasonal peaks; in 2024 spot prices averaged about 12–16 USD/MMBtu in Asia, giving suppliers leverage to favor highest bidders during cold snaps.

After 2022 Europe became a permanent LNG buyer, adding ~50–60 mtpa of demand and enabling suppliers to pit buyers against each other in shortages, raising supplier bargaining power.

- 2024 Asian spot: ~12–16 USD/MMBtu

- Europe added ~50–60 mtpa post-2022

- Suppliers win during cold snaps/high demand

Limited Upstream Integration Success

- 2024 self-sufficiency ~12%

- Imports ≈88% of supply (2024)

- High exposure to global LNG price swings

- Dependent on production schedules of majors

Suppliers Dominate LNG: Korea 88% Imports, Take-or-Pay 60–70%, Asia Spot $12–16

Suppliers hold strong bargaining power: Qatar, US, Australia supplied ~60% seaborne LNG in 2024, forcing KOGAS into price-taking; imports ≈88% of supply and self-sufficiency ~12% (2024). Long-term take-or-pay contracts cover ~60–70% of volumes, contributing ~40% of 2024 purchase liabilities. Geopolitics and Europe’s +50–60 mtpa demand post-2022 raised spot premiums (Asia 2024: ~12–16 USD/MMBtu).

| Metric | Value |

|---|---|

| Seaborne share (2024) | Qatar/US/Australia ~60% |

| Korea imports (2024) | ~88% |

| Self-sufficiency (2024) | ~12% |

| Take-or-pay coverage | ~60–70% |

| Spot Asia (2024) | ~12–16 USD/MMBtu |

What is included in the product

Tailored Porter's Five Forces for Korea Gas: evaluates supplier and buyer power, entry barriers, rivalry intensity, and substitutes, highlighting disruptive threats, pricing pressures, and strategic levers to protect market share and profitability.

A concise Korea Gas Porter’s Five Forces snapshot that pinpoints competitive pressures and regulatory risks—ready to drop into decision decks for fast, actionable insights.

Customers Bargaining Power

Government Regulation of Retail Pricing

The South Korean government caps end-user natural gas prices to curb inflation and protect households, meaning KOGAS cannot fully pass 2024–2025 LNG cost spikes onto consumers; regulation kept residential tariffs roughly 20–30% below market-adjusted levels in 2024, squeezing margins.

Industrial Fuel Switching Capabilities

Large Korean steel, petrochemical and manufacturing plants can switch between LNG, fuel oil and LPG; surveys in 2024 show ~35–45% of high-volume users have dual-fuel capability, so if KOGAS (Korea Gas Corporation) raises wholesale prices above competitors, these customers can cut LNG demand by 10–30% within quarters, giving them strong indirect bargaining power.

Power Generation Sector Sensitivity

The Korea Electric Power Corporation (KEPCO) and independent power producers (IPPs) purchase ~45% of Korea Gas (KOGAS) pipeline gas for power generation and are highly fuel-price sensitive because they bid into the marginal electricity price market; a 10% LNG price rise in 2024 raised dispatch costs by ~3.2 won/kWh, cutting margins.

Accumulation of Uncollected Receivables

- KRW 8.2T receivables by 2025

- KRW 1.1T annual subsidy-like shortfall

- Higher debt, tighter pricing room

Limited Direct Wholesale Choice

- KOGAS market share ~70% (2024)

- Spot/alternative supply ~10% of LNG demand (2024)

- City gas firms lack pipeline alternatives

KOGAS under squeeze: tariff gaps, KRW8.2T receivables and industrial demand risk

KOGAS faces strong customer pressure: regulated retail caps kept residential tariffs 20–30% below market in 2024, KRW 8.2T receivables by 2025 causing a KRW 1.1T annual shortfall, and large industrial buyers (35–45% dual-fuel capable) able to cut LNG demand 10–30% quickly; yet KOGAS retains ~70% market share and grid control, with spot imports ~10% of LNG demand (2024).

| Metric | 2024–2025 |

|---|---|

| Residential tariff gap | 20–30% below market (2024) |

| Receivables | KRW 8.2T (end‑2025) |

| Annual shortfall | KRW 1.1T |

| Dual‑fuel users | 35–45% (2024) |

| Market share | ~70% (KOGAS, 2024) |

| Spot imports | ~10% of LNG demand (2024) |

Same Document Delivered

Korea Gas Porter's Five Forces Analysis

This preview shows the exact Korea Gas Porter's Five Forces analysis you'll receive—no samples or placeholders; the full, professionally formatted document is ready for immediate download upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Korea Gas faces moderate supplier power and regulatory scrutiny, with steady domestic demand but rising competition from renewable substitutes narrowing margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Korea Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Global LNG Producers

The global LNG market is highly concentrated: Qatar, the United States, and Australia supplied about 60% of seaborne LNG in 2024, giving these exporters strong pricing power over buyers like KOGAS.

KOGAS sources roughly 70–80% of South Korea’s gas imports from these suppliers, so it often acts as a price-taker in long-term contracts and spot purchases.

As of late 2025, few alternative large-scale suppliers exist, keeping bargaining power tilted toward exporters and pressuring KOGAS’s procurement costs.

Rigidity of Long-Term Take-or-Pay Contracts

Geopolitical Influence on Supply Routes

Geopolitical tensions in the Middle East and chokepoints like the Strait of Hormuz repeatedly threaten supply stability; disruptions in 2024 pushed spot LNG premiums up to 45% above long-term contract prices, boosting suppliers in low-risk jurisdictions. KOGAS must navigate sanctions and rerouting costs—shipping detours added ~8–12% to freight per cargo in 2024—so suppliers in stable regions gain pricing leverage. This raises supplier bargaining power and spot-market dependency for Korea Gas.

Competition for Spot Market Volumes

KOGAS competes with major Asian buyers and European importers for spot LNG to meet seasonal peaks; in 2024 spot prices averaged about 12–16 USD/MMBtu in Asia, giving suppliers leverage to favor highest bidders during cold snaps.

After 2022 Europe became a permanent LNG buyer, adding ~50–60 mtpa of demand and enabling suppliers to pit buyers against each other in shortages, raising supplier bargaining power.

- 2024 Asian spot: ~12–16 USD/MMBtu

- Europe added ~50–60 mtpa post-2022

- Suppliers win during cold snaps/high demand

Limited Upstream Integration Success

- 2024 self-sufficiency ~12%

- Imports ≈88% of supply (2024)

- High exposure to global LNG price swings

- Dependent on production schedules of majors

Suppliers Dominate LNG: Korea 88% Imports, Take-or-Pay 60–70%, Asia Spot $12–16

Suppliers hold strong bargaining power: Qatar, US, Australia supplied ~60% seaborne LNG in 2024, forcing KOGAS into price-taking; imports ≈88% of supply and self-sufficiency ~12% (2024). Long-term take-or-pay contracts cover ~60–70% of volumes, contributing ~40% of 2024 purchase liabilities. Geopolitics and Europe’s +50–60 mtpa demand post-2022 raised spot premiums (Asia 2024: ~12–16 USD/MMBtu).

| Metric | Value |

|---|---|

| Seaborne share (2024) | Qatar/US/Australia ~60% |

| Korea imports (2024) | ~88% |

| Self-sufficiency (2024) | ~12% |

| Take-or-pay coverage | ~60–70% |

| Spot Asia (2024) | ~12–16 USD/MMBtu |

What is included in the product

Tailored Porter's Five Forces for Korea Gas: evaluates supplier and buyer power, entry barriers, rivalry intensity, and substitutes, highlighting disruptive threats, pricing pressures, and strategic levers to protect market share and profitability.

A concise Korea Gas Porter’s Five Forces snapshot that pinpoints competitive pressures and regulatory risks—ready to drop into decision decks for fast, actionable insights.

Customers Bargaining Power

Government Regulation of Retail Pricing

The South Korean government caps end-user natural gas prices to curb inflation and protect households, meaning KOGAS cannot fully pass 2024–2025 LNG cost spikes onto consumers; regulation kept residential tariffs roughly 20–30% below market-adjusted levels in 2024, squeezing margins.

Industrial Fuel Switching Capabilities

Large Korean steel, petrochemical and manufacturing plants can switch between LNG, fuel oil and LPG; surveys in 2024 show ~35–45% of high-volume users have dual-fuel capability, so if KOGAS (Korea Gas Corporation) raises wholesale prices above competitors, these customers can cut LNG demand by 10–30% within quarters, giving them strong indirect bargaining power.

Power Generation Sector Sensitivity

The Korea Electric Power Corporation (KEPCO) and independent power producers (IPPs) purchase ~45% of Korea Gas (KOGAS) pipeline gas for power generation and are highly fuel-price sensitive because they bid into the marginal electricity price market; a 10% LNG price rise in 2024 raised dispatch costs by ~3.2 won/kWh, cutting margins.

Accumulation of Uncollected Receivables

- KRW 8.2T receivables by 2025

- KRW 1.1T annual subsidy-like shortfall

- Higher debt, tighter pricing room

Limited Direct Wholesale Choice

- KOGAS market share ~70% (2024)

- Spot/alternative supply ~10% of LNG demand (2024)

- City gas firms lack pipeline alternatives

KOGAS under squeeze: tariff gaps, KRW8.2T receivables and industrial demand risk

KOGAS faces strong customer pressure: regulated retail caps kept residential tariffs 20–30% below market in 2024, KRW 8.2T receivables by 2025 causing a KRW 1.1T annual shortfall, and large industrial buyers (35–45% dual-fuel capable) able to cut LNG demand 10–30% quickly; yet KOGAS retains ~70% market share and grid control, with spot imports ~10% of LNG demand (2024).

| Metric | 2024–2025 |

|---|---|

| Residential tariff gap | 20–30% below market (2024) |

| Receivables | KRW 8.2T (end‑2025) |

| Annual shortfall | KRW 1.1T |

| Dual‑fuel users | 35–45% (2024) |

| Market share | ~70% (KOGAS, 2024) |

| Spot imports | ~10% of LNG demand (2024) |

Same Document Delivered

Korea Gas Porter's Five Forces Analysis

This preview shows the exact Korea Gas Porter's Five Forces analysis you'll receive—no samples or placeholders; the full, professionally formatted document is ready for immediate download upon purchase.