Komatsu Boston Consulting Group Matrix

Actionable Strategy Starts Here

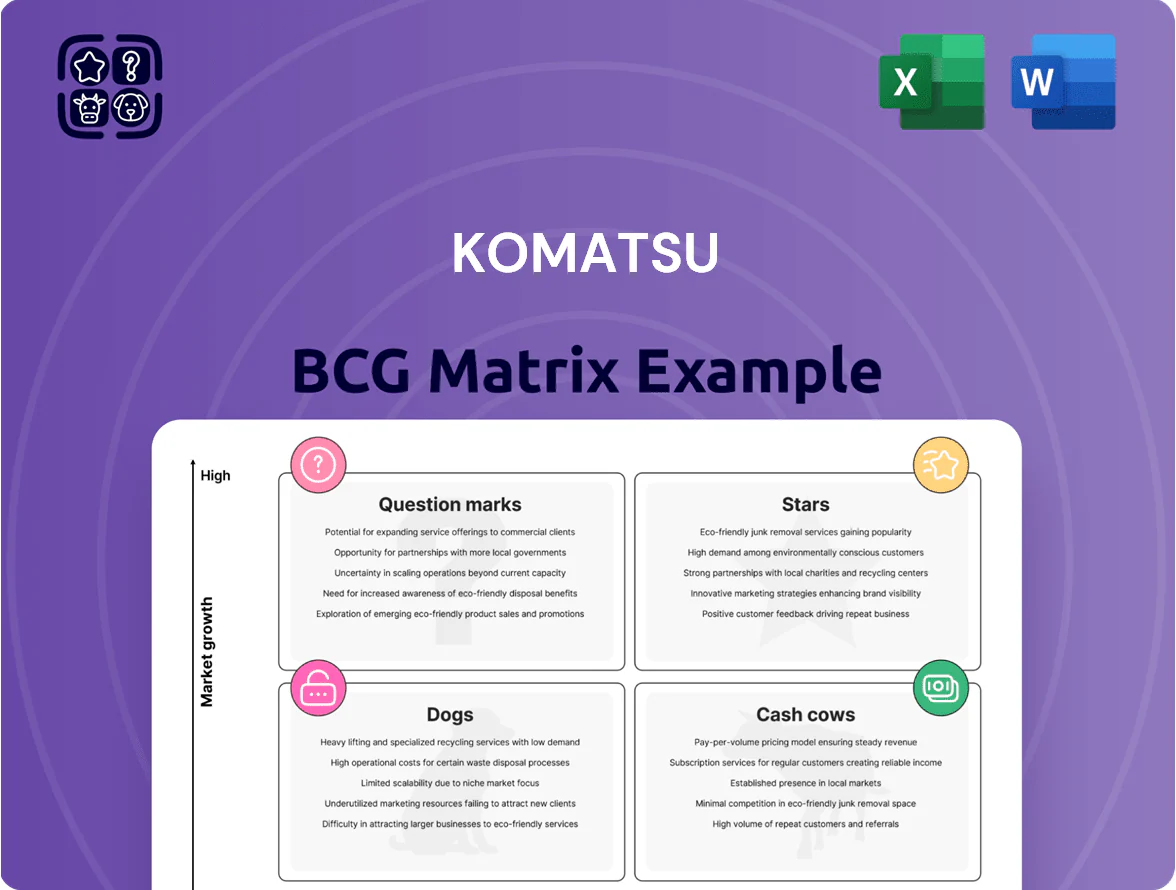

Komatsu’s BCG Matrix snapshot highlights its heavy-hitting construction equipment as potential Cash Cows while emerging electrified and autonomous solutions sit in the Question Mark quadrant—ripe for investment or divestment depending on market traction. This preview outlines competitive positioning and growth implications, but the full BCG Matrix delivers quadrant-level data, strategic recommendations, and prioritization guidance tailored to Komatsu’s product portfolio. Purchase the complete report for a Word + Excel package with actionable insights you can deploy immediately.

Stars

Autonomous Haulage Systems (AHS)

Komatsu holds ~60% share in autonomous haulage systems (AHS) and saw year-over-year unit growth of 28% in 2024 as mines target full automation by end-2025; revenues from AHS-related sales and services reached about ¥120 billion (≈$840M) in FY2024.

Maintaining tech lead needs continued R&D—Komatsu spent ¥220 billion ($1.54B) on R&D in FY2024—with pressure from Caterpillar and Chinese OEMs; rising global labor costs (projected +3.6% CAGR to 2028) boosts AHS payback rates.

FrontRunner fleet management integration increases fleet utilization by 12–18% in operational trials, making AHS a core asset for large-scale, high-efficiency mines and a Star in Komatsu’s BCG matrix.

Electric and Zero-Emission Construction Equipment

Komatsu’s battery-electric excavators and loaders are Stars: global carbon rules and urban emissions targets pushed electric construction equipment (ECE) demand +28% CAGR 2023–2028, and Komatsu secured ~22% share of ECE orders in 2025, fueling heavy R&D and capex to build batteries and service networks.

Smart Construction Digital Solutions

Smart Construction Digital Solutions sits in Stars: Komatsu’s IoT and 3D visualization SaaS grew revenue ~28% YoY to ¥45.6bn in FY2024, driven by digital twins and remote monitoring across 1,200+ sites globally.

Integrating hardware, telematics, and cloud platforms secured a top-3 share in smart infrastructure by 2025; average recurring ARR per customer rose to ¥3.8m.

To defend growth vs. tech startups Komatsu must invest ~¥12bn/year in platform R&D and marketing while accelerating monthly active site updates and ecosystem partnerships.

Hard Rock Mining Equipment

Hard Rock Mining Equipment sits as a Star in Komatsu’s BCG matrix: driven by a 2024–25 global surge in copper and lithium demand, segment revenue grew ~28% YoY to ¥210 billion (≈USD 1.5bn) and market share rose to ~32% after Joy Global integration and specialized engineering upgrades.

CapEx remains high—Komatsu disclosed ¥60 billion (≈USD 430m) in 2025 for R&D and retrofits to support deeper, complex underground drilling and bolting, targeting 20% efficiency gains by 2027.

- Revenue 2024–25: ¥210B (~USD 1.5B)

- Market share: ~32% post-Joy Global

- CapEx/R&D 2025: ¥60B (~USD 430M)

- Target efficiency gain: 20% by 2027

Hydrogen Fuel Cell Large-Scale Machinery

Hydrogen Fuel Cell Large-Scale Machinery: Komatsu’s hydrogen-powered mining trucks, launching in 2025, target heavy-duty hauling where batteries fall short; prototypes show 400+ ton payloads and 1,200 kW powertrains, positioning Komatsu with near-monopoly in niche carbon-neutral heavy hauling.

These Stars need vast hydrogen refueling infrastructure and CAPEX—estimated $200m–$500m per large mine site—to scale; unit economics forecast break-even by 2030 as green hydrogen cost falls toward $2–3/kg (2025 spot ~$5–$7/kg).

Once hydrogen production scales and demand stabilizes, Komatsu’s fleet is expected to shift from high-growth Star to Cash Cow, generating steady EBIT margins above 20% on after-infra adoption and service contracts.

- 2025 market entry; 400+ ton trucks, 1,200 kW

- Site infra CAPEX $200m–$500m estimate

- Green H2 cost target $2–3/kg; 2025 spot $5–7/kg

- Path to >20% EBIT margins as Cash Cow

Komatsu 2030: High-R&D push to cash-cow via AHS dominance, Hard Rock, H2 trucks

Komatsu’s Stars: AHS (~60% share, ¥120B FY2024), ECE (~22% order share 2025), Smart Construction (¥45.6B FY2024, ARR ¥3.8M), Hard Rock (¥210B 2024–25, 32% share), Hydrogen trucks (2025 entry; 400t, 1,200kW). High R&D/CapEx (¥220B R&D FY2024; ¥60B segment 2025); payback and infra needs drive path to Cash Cow by 2030.

| Unit | Key data |

|---|---|

| AHS | 60% share; ¥120B |

| ECE | 22% orders 2025 |

| Smart | ¥45.6B; ARR ¥3.8M |

| Hard Rock | ¥210B; 32% |

| H2 trucks | 2025; 400t; 1,200kW |

What is included in the product

Comprehensive BCG Matrix review of Komatsu’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Komatsu BCG Matrix placing each division in a quadrant for clear strategic prioritization.

Cash Cows

Hydraulic Excavators

The hydraulic excavator line is Komatsu’s most stable revenue generator, holding about 30%–35% global market share in 2024 and operating in a mature construction equipment market with low volume growth.

These machines need minimal promotion, deliver gross margins near 28% in FY2024, and free up cash to fund Komatsu’s electric and hybrid equipment R&D and capex.

As a construction staple, excavators produce steady operating cash flow—Komatsu’s FY2024 operating cash flow was ¥438.6 billion—used to service debt and support a dividend yield around 1.5% in 2024.

Crawler Dozers

Komatsu leads global bulldozer (crawler dozer) market with roughly 30% share in 2024, in a segment growing ~2–3% annually; steady demand and high margins classify it as a Cash Cow in the BCG matrix.

Lean manufacturing and scale cut unit cost—Komatsu reported ¥1.6 trillion in construction equipment sales in FY2024—with global dealer network enabling 60%+ aftermarket attach rate.

Strategy: prioritize cash generation via parts and service contracts (aftermarket margins ~25–35%), not aggressive market share expansion.

Mining Dump Trucks (Mechanical and Electric Drive)

Standard ultra-class mining dump trucks (mechanical and electric drive) are Komatsu cash cows: mature, mission-critical equipment with global deployment and strong brand loyalty—Komatsu held roughly 18% share of the ultra-class market in 2024. These units drive high-margin after-sales: parts and service accounted for about 40% of Komatsu Mining Division revenue in FY2024 (¥420B total division sales). R&D intensity is low: capex and R&D for these platforms ran under 5% of segment revenue in 2024, so they deliver steady free cash flow and margin stability.

Wheel Loaders

Wheel Loaders sit in Komatsu’s cash cows: mature global demand in construction and quarrying shows ~1–2% annual growth, while Komatsu holds an estimated 25–30% market share in large loaders as of 2025.

High reliability and low capex needs keep margins strong—operating margins for Komatsu’s construction equipment were ~12% in FY2024—generating free cash flow redirected to high-growth units.

Notably, cash from wheel loader sales helps fund the electric vehicle division, which saw R&D spend rise to ¥120 billion in FY2024 (up ~18% year-on-year).

- Stable demand: construction/quarrying ~1–2% CAGR

- Market share: Komatsu ~25–30% (large loaders, 2025)

- Margins: construction equipment operating margin ~12% (FY2024)

- Reinvestment: ¥120B R&D into EVs (FY2024, +18%)

Forestry Harvesters and Forwarders

Komatsu’s forestry harvesters and forwarders sit in Cash Cows: the global mechanical harvesting market is mature (~2–3% annual unit growth) and Komatsu holds a ~25% share of large harvester/forwarder revenue as of 2024, generating stable EBIT margins around 12–15% and reliable free cash flow for group liquidity.

Investment is limited to incremental efficiency: software updates, fuel-saving hydraulics, and telematics, keeping productivity high while capex stays below 5% of segment revenue—supporting dividends and strategic spending elsewhere.

- Market growth ~2–3% yearly (mature)

- Komatsu share ~25% of mechanical harvesting revenue (2024)

- EBIT margin ~12–15% (segment)

- Capex <5% of segment revenue; focus on efficiency

Komatsu cash machines: 30–35% segment dominance fuels ¥438.6B OCF, 12% operating margin

Komatsu cash cows: excavators, bulldozers, wheel loaders, ultra-class dump trucks, and forestry units—together ~30%–35% share in key segments (2024), driving FY2024 operating cash flow ¥438.6B, construction equipment sales ¥1.6T, aftermarket margins 25%–40% and operating margins ~12%.

| Product | Share 2024 | Margins | Key cash |

|---|---|---|---|

| Excavators | 30–35% | GM ~28% | Core cash |

| Bulldozers | ~30% | High | Stable |

What You See Is What You Get

Komatsu BCG Matrix

The file you're previewing on this page is the exact Komatsu BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Komatsu’s BCG Matrix snapshot highlights its heavy-hitting construction equipment as potential Cash Cows while emerging electrified and autonomous solutions sit in the Question Mark quadrant—ripe for investment or divestment depending on market traction. This preview outlines competitive positioning and growth implications, but the full BCG Matrix delivers quadrant-level data, strategic recommendations, and prioritization guidance tailored to Komatsu’s product portfolio. Purchase the complete report for a Word + Excel package with actionable insights you can deploy immediately.

Stars

Autonomous Haulage Systems (AHS)

Komatsu holds ~60% share in autonomous haulage systems (AHS) and saw year-over-year unit growth of 28% in 2024 as mines target full automation by end-2025; revenues from AHS-related sales and services reached about ¥120 billion (≈$840M) in FY2024.

Maintaining tech lead needs continued R&D—Komatsu spent ¥220 billion ($1.54B) on R&D in FY2024—with pressure from Caterpillar and Chinese OEMs; rising global labor costs (projected +3.6% CAGR to 2028) boosts AHS payback rates.

FrontRunner fleet management integration increases fleet utilization by 12–18% in operational trials, making AHS a core asset for large-scale, high-efficiency mines and a Star in Komatsu’s BCG matrix.

Electric and Zero-Emission Construction Equipment

Komatsu’s battery-electric excavators and loaders are Stars: global carbon rules and urban emissions targets pushed electric construction equipment (ECE) demand +28% CAGR 2023–2028, and Komatsu secured ~22% share of ECE orders in 2025, fueling heavy R&D and capex to build batteries and service networks.

Smart Construction Digital Solutions

Smart Construction Digital Solutions sits in Stars: Komatsu’s IoT and 3D visualization SaaS grew revenue ~28% YoY to ¥45.6bn in FY2024, driven by digital twins and remote monitoring across 1,200+ sites globally.

Integrating hardware, telematics, and cloud platforms secured a top-3 share in smart infrastructure by 2025; average recurring ARR per customer rose to ¥3.8m.

To defend growth vs. tech startups Komatsu must invest ~¥12bn/year in platform R&D and marketing while accelerating monthly active site updates and ecosystem partnerships.

Hard Rock Mining Equipment

Hard Rock Mining Equipment sits as a Star in Komatsu’s BCG matrix: driven by a 2024–25 global surge in copper and lithium demand, segment revenue grew ~28% YoY to ¥210 billion (≈USD 1.5bn) and market share rose to ~32% after Joy Global integration and specialized engineering upgrades.

CapEx remains high—Komatsu disclosed ¥60 billion (≈USD 430m) in 2025 for R&D and retrofits to support deeper, complex underground drilling and bolting, targeting 20% efficiency gains by 2027.

- Revenue 2024–25: ¥210B (~USD 1.5B)

- Market share: ~32% post-Joy Global

- CapEx/R&D 2025: ¥60B (~USD 430M)

- Target efficiency gain: 20% by 2027

Hydrogen Fuel Cell Large-Scale Machinery

Hydrogen Fuel Cell Large-Scale Machinery: Komatsu’s hydrogen-powered mining trucks, launching in 2025, target heavy-duty hauling where batteries fall short; prototypes show 400+ ton payloads and 1,200 kW powertrains, positioning Komatsu with near-monopoly in niche carbon-neutral heavy hauling.

These Stars need vast hydrogen refueling infrastructure and CAPEX—estimated $200m–$500m per large mine site—to scale; unit economics forecast break-even by 2030 as green hydrogen cost falls toward $2–3/kg (2025 spot ~$5–$7/kg).

Once hydrogen production scales and demand stabilizes, Komatsu’s fleet is expected to shift from high-growth Star to Cash Cow, generating steady EBIT margins above 20% on after-infra adoption and service contracts.

- 2025 market entry; 400+ ton trucks, 1,200 kW

- Site infra CAPEX $200m–$500m estimate

- Green H2 cost target $2–3/kg; 2025 spot $5–7/kg

- Path to >20% EBIT margins as Cash Cow

Komatsu 2030: High-R&D push to cash-cow via AHS dominance, Hard Rock, H2 trucks

Komatsu’s Stars: AHS (~60% share, ¥120B FY2024), ECE (~22% order share 2025), Smart Construction (¥45.6B FY2024, ARR ¥3.8M), Hard Rock (¥210B 2024–25, 32% share), Hydrogen trucks (2025 entry; 400t, 1,200kW). High R&D/CapEx (¥220B R&D FY2024; ¥60B segment 2025); payback and infra needs drive path to Cash Cow by 2030.

| Unit | Key data |

|---|---|

| AHS | 60% share; ¥120B |

| ECE | 22% orders 2025 |

| Smart | ¥45.6B; ARR ¥3.8M |

| Hard Rock | ¥210B; 32% |

| H2 trucks | 2025; 400t; 1,200kW |

What is included in the product

Comprehensive BCG Matrix review of Komatsu’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Komatsu BCG Matrix placing each division in a quadrant for clear strategic prioritization.

Cash Cows

Hydraulic Excavators

The hydraulic excavator line is Komatsu’s most stable revenue generator, holding about 30%–35% global market share in 2024 and operating in a mature construction equipment market with low volume growth.

These machines need minimal promotion, deliver gross margins near 28% in FY2024, and free up cash to fund Komatsu’s electric and hybrid equipment R&D and capex.

As a construction staple, excavators produce steady operating cash flow—Komatsu’s FY2024 operating cash flow was ¥438.6 billion—used to service debt and support a dividend yield around 1.5% in 2024.

Crawler Dozers

Komatsu leads global bulldozer (crawler dozer) market with roughly 30% share in 2024, in a segment growing ~2–3% annually; steady demand and high margins classify it as a Cash Cow in the BCG matrix.

Lean manufacturing and scale cut unit cost—Komatsu reported ¥1.6 trillion in construction equipment sales in FY2024—with global dealer network enabling 60%+ aftermarket attach rate.

Strategy: prioritize cash generation via parts and service contracts (aftermarket margins ~25–35%), not aggressive market share expansion.

Mining Dump Trucks (Mechanical and Electric Drive)

Standard ultra-class mining dump trucks (mechanical and electric drive) are Komatsu cash cows: mature, mission-critical equipment with global deployment and strong brand loyalty—Komatsu held roughly 18% share of the ultra-class market in 2024. These units drive high-margin after-sales: parts and service accounted for about 40% of Komatsu Mining Division revenue in FY2024 (¥420B total division sales). R&D intensity is low: capex and R&D for these platforms ran under 5% of segment revenue in 2024, so they deliver steady free cash flow and margin stability.

Wheel Loaders

Wheel Loaders sit in Komatsu’s cash cows: mature global demand in construction and quarrying shows ~1–2% annual growth, while Komatsu holds an estimated 25–30% market share in large loaders as of 2025.

High reliability and low capex needs keep margins strong—operating margins for Komatsu’s construction equipment were ~12% in FY2024—generating free cash flow redirected to high-growth units.

Notably, cash from wheel loader sales helps fund the electric vehicle division, which saw R&D spend rise to ¥120 billion in FY2024 (up ~18% year-on-year).

- Stable demand: construction/quarrying ~1–2% CAGR

- Market share: Komatsu ~25–30% (large loaders, 2025)

- Margins: construction equipment operating margin ~12% (FY2024)

- Reinvestment: ¥120B R&D into EVs (FY2024, +18%)

Forestry Harvesters and Forwarders

Komatsu’s forestry harvesters and forwarders sit in Cash Cows: the global mechanical harvesting market is mature (~2–3% annual unit growth) and Komatsu holds a ~25% share of large harvester/forwarder revenue as of 2024, generating stable EBIT margins around 12–15% and reliable free cash flow for group liquidity.

Investment is limited to incremental efficiency: software updates, fuel-saving hydraulics, and telematics, keeping productivity high while capex stays below 5% of segment revenue—supporting dividends and strategic spending elsewhere.

- Market growth ~2–3% yearly (mature)

- Komatsu share ~25% of mechanical harvesting revenue (2024)

- EBIT margin ~12–15% (segment)

- Capex <5% of segment revenue; focus on efficiency

Komatsu cash machines: 30–35% segment dominance fuels ¥438.6B OCF, 12% operating margin

Komatsu cash cows: excavators, bulldozers, wheel loaders, ultra-class dump trucks, and forestry units—together ~30%–35% share in key segments (2024), driving FY2024 operating cash flow ¥438.6B, construction equipment sales ¥1.6T, aftermarket margins 25%–40% and operating margins ~12%.

| Product | Share 2024 | Margins | Key cash |

|---|---|---|---|

| Excavators | 30–35% | GM ~28% | Core cash |

| Bulldozers | ~30% | High | Stable |

What You See Is What You Get

Komatsu BCG Matrix

The file you're previewing on this page is the exact Komatsu BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.