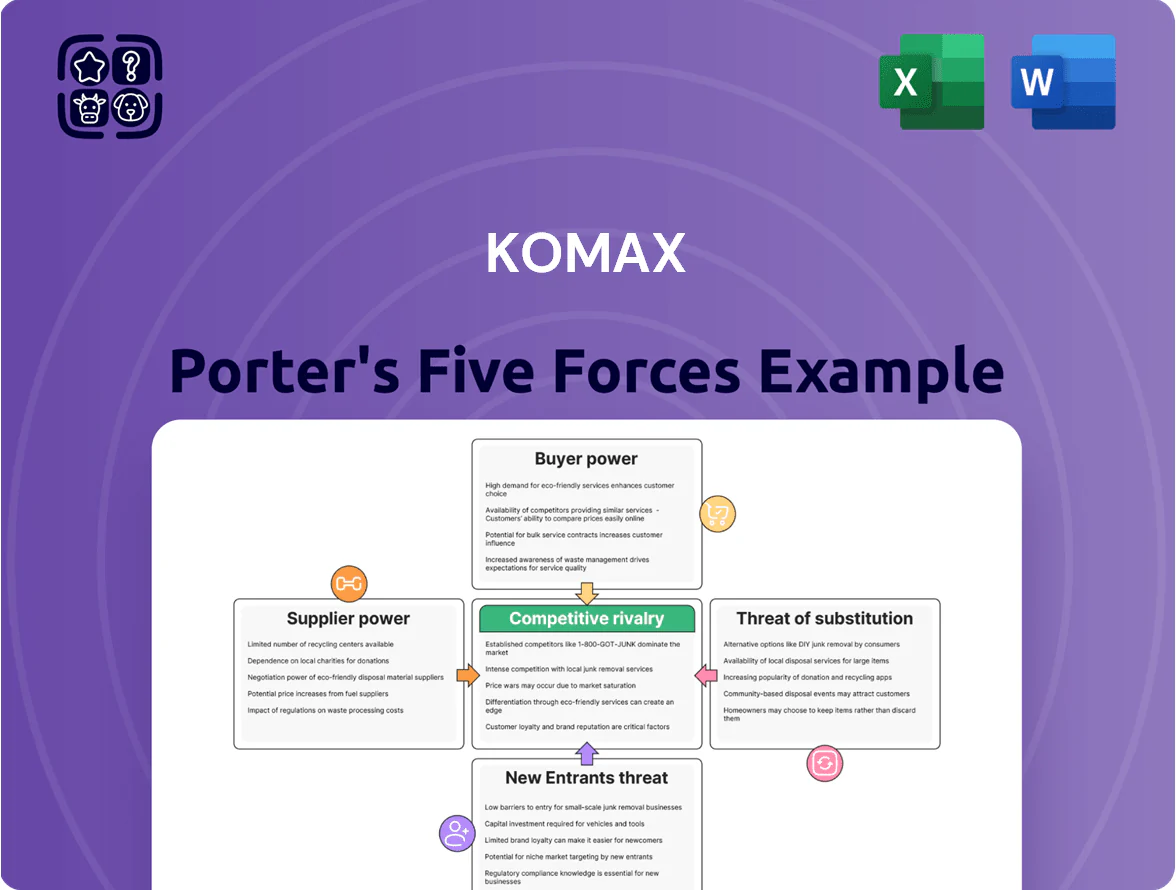

Komax Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Komax faces moderate supplier power due to specialized component needs, steady buyer power among industrial clients, and a moderate threat from new entrants given capital and technical barriers; substitutes and rivalry hinge on automation trends and regional competition. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Komax’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized electronic component dependency

Komax depends on high-precision semiconductors for its automated wire-processing machines; in 2024 about 22% of its COGS was tied to electronic modules, raising supplier importance.

Few vendors supply the specific high-end microchips Komax needs, so those suppliers can exert pricing and delivery leverage—chip lead times hit 18–24 weeks in 2023–24.

During supply shocks, price pass-through raised component costs ~6–9% for industrial OEMs; Komax’s scale limits but does not eliminate this supplier power.

Raw material price fluctuations

The production of Komax wire-processing machinery relies heavily on high-grade steel, aluminum and alloys; in 2024 steel accounted for an estimated 18–22% of BOM cost per unit, so price swings hit margins directly.

Global metal prices rose ~12% in 2023–24 (LME indices), making suppliers’ bargaining power higher during tight supply cycles and pushing Komax to pass costs or absorb margin hits.

These materials are standardized and essential, limiting Komax’s ability to negotiate below market rates when demand is strong; long-term metal contracts and hedging partially mitigate but don’t remove exposure.

Proprietary software and automation integration

As Komax shifts to software-driven automation, dependence on third-party providers rises; proprietary protocol licenses and integration complexity raise supplier power, evidenced by Komax reporting 28% of R&D spend in 2024 on software integrations. Strategic partnerships reduce disruption but create supplier lock-in—typical contract terms span 3–7 years—so switching costs and technical debt increase bargaining leverage for suppliers.

Limited number of precision tool manufacturers

The high-quality blades and crimping tools in Komax machines must meet tolerances often under 10 microns to comply with automotive safety standards; in 2024 Komax reported ~65% of revenues tied to automotive-related tooling and services, stressing precision supply needs.

Only a few specialized manufacturers—estimated 5–8 global suppliers—can deliver required quality and volume, creating supplier concentration that grants moderate bargaining power over specs and 8–12 week lead times.

- ~10 micron tolerances required

- 5–8 qualified suppliers globally

- 65% revenue exposure to automotive tooling (2024)

- Typical lead times 8–12 weeks

Supplier diversification and global sourcing

Komax keeps a global vendor network—over 200 qualified suppliers across Europe, Asia and the Americas as of 2025—to avoid concentration risk and blunt supplier bargaining power.

By sourcing regionally and running competitive bids, Komax negotiates price and lead-time concessions, protecting gross margins that faced a 120–180 bps hit in 2022 from logistics spikes.

This diversification shields Komax from regional shocks and geopolitical risk, letting procurement shift volumes quickly to secure better terms.

- 200+ qualified suppliers (2025)

- 120–180 bps margin impact from 2022 logistics shocks

- Multi-region sourcing: Europe, Asia, Americas

Supplier concentration drives higher COGS risk; Komax mitigates with 200+ suppliers

Suppliers hold moderate-to-high power: specialized chips and precision tooling concentrate with few vendors (5–8), chip lead times 18–24 weeks, tooling 8–12 weeks, and electronics/steel made up ~22% and ~20% of BOM respectively in 2024, raising cost pass-through (~6–9%) and 2022 logistics margin hit of 120–180 bps; Komax offsets via 200+ suppliers (2025) and regional sourcing.

| Metric | Value (year) |

|---|---|

| Qualified suppliers | 200+ (2025) |

| Specialized suppliers | 5–8 |

| Chip lead time | 18–24 wks (2023–24) |

| Tooling lead time | 8–12 wks (2024) |

| Electronics % of COGS | ~22% (2024) |

| Steel % of BOM | ~20% (2024) |

| Price pass-through | ~6–9% (shocks) |

| Logistics margin hit | 120–180 bps (2022) |

What is included in the product

Tailored Porter's Five Forces for Komax, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging disruptive threats to its market share.

Komax Porter's Five Forces delivers a one-sheet, slide-ready summary that quantifies competitive pressure and can be toggled for scenarios—ideal for fast, board-ready strategic decisions.

Customers Bargaining Power

Concentration of automotive Tier 1 suppliers

A significant share of Komax’s sales is concentrated in a few global Tier 1s—Aptiv, Leoni, Sumitomo—who together accounted for roughly 35–45% of automotive revenue in 2024, giving them strong bargaining power.

These buyers demand high volumes and push for price cuts and tailored features; their scale lets them shape Komax’s R&D and product roadmap to fit specific manufacturing lines.

High switching costs for integrated systems

Once Komax’s fully automated lines are installed, customers face high switching costs—estimated integration expenses plus downtime can exceed USD 500k per line and 4–12 weeks of lost output—creating strong lock-in and lowering buyer bargaining power. Deep software ties, certified operator training, and multi-year maintenance contracts (often 3–5 years) raise exit barriers, so retention stays high despite price pressure; Komax’s service revenue grew ~8% in 2024, reflecting this stickiness.

Demand for customized automation solutions

Customers in EV supply chains increasingly demand bespoke automation for complex wire harnesses; global EV production rose 40% in 2024 to ~16.5 million units, pushing customization needs.

This raises Komax’s bargaining power: few rivals match its engineering depth and 2024 R&D spend of CHF 115m, so Komax can command premium contracts.

Still, buyers demand high service levels and ongoing innovation; contract renewal depends on uptime and software updates, with SLA penalties commonly 5–10% of annual fees.

Price sensitivity in competitive end markets

Automotive and telecommunications buyers run on thin margins—global auto OEM net margins averaged ~6.2% in 2024 and telecom operators 4–7%—so capex sensitivity is high and customers push for automation to cut unit costs.

Komax’s machines are valued for quality, but buyers demand fast payback; typical target ROI windows are 12–36 months, forcing Komax to prove rapid cost-per-wire or labour savings.

Pressure to lower total cost of ownership constrains Komax’s premium pricing unless it shows measurable throughput gains and service savings within contract timelines.

Importance of global service and maintenance

Customers depend on Komax for 24/7 technical support, spare parts, and software updates to avoid costly downtime; industry data shows unplanned production stops can cost €10,000–€100,000+ per hour in automotive wiring plants (2024 estimates), so service contracts are small by comparison.

Global, reliable support gives Komax pricing power and stickiness; reported service revenue reached ~15% of Komax group sales in 2024, reinforcing that customers pay premiums for continuity.

- High downtime cost → higher willingness to pay

- Service revenue ≈15% of sales (2024)

- Global spare-parts network reduces churn

Komax: High switching costs, buyer concentration and R&D fuel premium pricing

Buyers (Aptiv, Leoni, Sumitomo) held 35–45% of Komax automotive revenue in 2024, giving strong price leverage, but high switching costs (≈USD 500k+/line, 4–12 weeks downtime) and multi-year service contracts (3–5 years) create lock-in; service revenue ≈15% of sales (2024) and Komax R&D CHF 115m (2024) support premium pricing subject to ROI targets of 12–36 months.

| Metric | 2024 |

|---|---|

| Top-tier buyer share | 35–45% |

| Switching cost per line | ≈USD 500k+ |

| Downtime | 4–12 weeks |

| Service revenue | ≈15% sales |

| R&D spend | CHF 115m |

| Buyer ROI target | 12–36 months |

Same Document Delivered

Komax Porter's Five Forces Analysis

This preview shows the exact Komax Porter’s Five Forces analysis you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Komax faces moderate supplier power due to specialized component needs, steady buyer power among industrial clients, and a moderate threat from new entrants given capital and technical barriers; substitutes and rivalry hinge on automation trends and regional competition. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Komax’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized electronic component dependency

Komax depends on high-precision semiconductors for its automated wire-processing machines; in 2024 about 22% of its COGS was tied to electronic modules, raising supplier importance.

Few vendors supply the specific high-end microchips Komax needs, so those suppliers can exert pricing and delivery leverage—chip lead times hit 18–24 weeks in 2023–24.

During supply shocks, price pass-through raised component costs ~6–9% for industrial OEMs; Komax’s scale limits but does not eliminate this supplier power.

Raw material price fluctuations

The production of Komax wire-processing machinery relies heavily on high-grade steel, aluminum and alloys; in 2024 steel accounted for an estimated 18–22% of BOM cost per unit, so price swings hit margins directly.

Global metal prices rose ~12% in 2023–24 (LME indices), making suppliers’ bargaining power higher during tight supply cycles and pushing Komax to pass costs or absorb margin hits.

These materials are standardized and essential, limiting Komax’s ability to negotiate below market rates when demand is strong; long-term metal contracts and hedging partially mitigate but don’t remove exposure.

Proprietary software and automation integration

As Komax shifts to software-driven automation, dependence on third-party providers rises; proprietary protocol licenses and integration complexity raise supplier power, evidenced by Komax reporting 28% of R&D spend in 2024 on software integrations. Strategic partnerships reduce disruption but create supplier lock-in—typical contract terms span 3–7 years—so switching costs and technical debt increase bargaining leverage for suppliers.

Limited number of precision tool manufacturers

The high-quality blades and crimping tools in Komax machines must meet tolerances often under 10 microns to comply with automotive safety standards; in 2024 Komax reported ~65% of revenues tied to automotive-related tooling and services, stressing precision supply needs.

Only a few specialized manufacturers—estimated 5–8 global suppliers—can deliver required quality and volume, creating supplier concentration that grants moderate bargaining power over specs and 8–12 week lead times.

- ~10 micron tolerances required

- 5–8 qualified suppliers globally

- 65% revenue exposure to automotive tooling (2024)

- Typical lead times 8–12 weeks

Supplier diversification and global sourcing

Komax keeps a global vendor network—over 200 qualified suppliers across Europe, Asia and the Americas as of 2025—to avoid concentration risk and blunt supplier bargaining power.

By sourcing regionally and running competitive bids, Komax negotiates price and lead-time concessions, protecting gross margins that faced a 120–180 bps hit in 2022 from logistics spikes.

This diversification shields Komax from regional shocks and geopolitical risk, letting procurement shift volumes quickly to secure better terms.

- 200+ qualified suppliers (2025)

- 120–180 bps margin impact from 2022 logistics shocks

- Multi-region sourcing: Europe, Asia, Americas

Supplier concentration drives higher COGS risk; Komax mitigates with 200+ suppliers

Suppliers hold moderate-to-high power: specialized chips and precision tooling concentrate with few vendors (5–8), chip lead times 18–24 weeks, tooling 8–12 weeks, and electronics/steel made up ~22% and ~20% of BOM respectively in 2024, raising cost pass-through (~6–9%) and 2022 logistics margin hit of 120–180 bps; Komax offsets via 200+ suppliers (2025) and regional sourcing.

| Metric | Value (year) |

|---|---|

| Qualified suppliers | 200+ (2025) |

| Specialized suppliers | 5–8 |

| Chip lead time | 18–24 wks (2023–24) |

| Tooling lead time | 8–12 wks (2024) |

| Electronics % of COGS | ~22% (2024) |

| Steel % of BOM | ~20% (2024) |

| Price pass-through | ~6–9% (shocks) |

| Logistics margin hit | 120–180 bps (2022) |

What is included in the product

Tailored Porter's Five Forces for Komax, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and emerging disruptive threats to its market share.

Komax Porter's Five Forces delivers a one-sheet, slide-ready summary that quantifies competitive pressure and can be toggled for scenarios—ideal for fast, board-ready strategic decisions.

Customers Bargaining Power

Concentration of automotive Tier 1 suppliers

A significant share of Komax’s sales is concentrated in a few global Tier 1s—Aptiv, Leoni, Sumitomo—who together accounted for roughly 35–45% of automotive revenue in 2024, giving them strong bargaining power.

These buyers demand high volumes and push for price cuts and tailored features; their scale lets them shape Komax’s R&D and product roadmap to fit specific manufacturing lines.

High switching costs for integrated systems

Once Komax’s fully automated lines are installed, customers face high switching costs—estimated integration expenses plus downtime can exceed USD 500k per line and 4–12 weeks of lost output—creating strong lock-in and lowering buyer bargaining power. Deep software ties, certified operator training, and multi-year maintenance contracts (often 3–5 years) raise exit barriers, so retention stays high despite price pressure; Komax’s service revenue grew ~8% in 2024, reflecting this stickiness.

Demand for customized automation solutions

Customers in EV supply chains increasingly demand bespoke automation for complex wire harnesses; global EV production rose 40% in 2024 to ~16.5 million units, pushing customization needs.

This raises Komax’s bargaining power: few rivals match its engineering depth and 2024 R&D spend of CHF 115m, so Komax can command premium contracts.

Still, buyers demand high service levels and ongoing innovation; contract renewal depends on uptime and software updates, with SLA penalties commonly 5–10% of annual fees.

Price sensitivity in competitive end markets

Automotive and telecommunications buyers run on thin margins—global auto OEM net margins averaged ~6.2% in 2024 and telecom operators 4–7%—so capex sensitivity is high and customers push for automation to cut unit costs.

Komax’s machines are valued for quality, but buyers demand fast payback; typical target ROI windows are 12–36 months, forcing Komax to prove rapid cost-per-wire or labour savings.

Pressure to lower total cost of ownership constrains Komax’s premium pricing unless it shows measurable throughput gains and service savings within contract timelines.

Importance of global service and maintenance

Customers depend on Komax for 24/7 technical support, spare parts, and software updates to avoid costly downtime; industry data shows unplanned production stops can cost €10,000–€100,000+ per hour in automotive wiring plants (2024 estimates), so service contracts are small by comparison.

Global, reliable support gives Komax pricing power and stickiness; reported service revenue reached ~15% of Komax group sales in 2024, reinforcing that customers pay premiums for continuity.

- High downtime cost → higher willingness to pay

- Service revenue ≈15% of sales (2024)

- Global spare-parts network reduces churn

Komax: High switching costs, buyer concentration and R&D fuel premium pricing

Buyers (Aptiv, Leoni, Sumitomo) held 35–45% of Komax automotive revenue in 2024, giving strong price leverage, but high switching costs (≈USD 500k+/line, 4–12 weeks downtime) and multi-year service contracts (3–5 years) create lock-in; service revenue ≈15% of sales (2024) and Komax R&D CHF 115m (2024) support premium pricing subject to ROI targets of 12–36 months.

| Metric | 2024 |

|---|---|

| Top-tier buyer share | 35–45% |

| Switching cost per line | ≈USD 500k+ |

| Downtime | 4–12 weeks |

| Service revenue | ≈15% sales |

| R&D spend | CHF 115m |

| Buyer ROI target | 12–36 months |

Same Document Delivered

Komax Porter's Five Forces Analysis

This preview shows the exact Komax Porter’s Five Forces analysis you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.