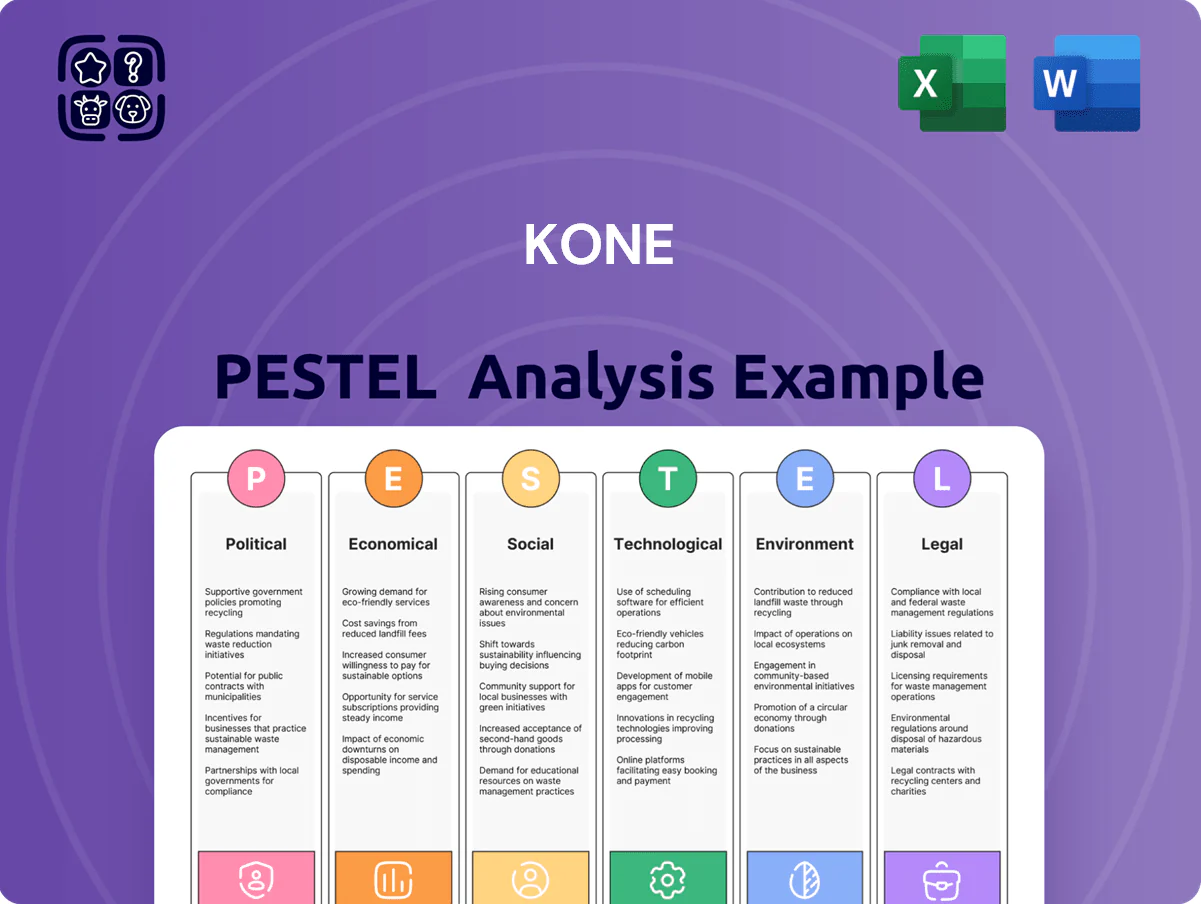

Kone PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Kone—insightfully mapping political, economic, social, technological, legal, and environmental forces that will shape its near-term strategy and long-term growth; ideal for investors, consultants, and executives seeking actionable intelligence. Purchase the full report to access the complete, editable breakdown and make faster, smarter decisions with data-driven clarity.

Political factors

Geopolitical Trade Relations

Ongoing trade tensions among China, the US and EU complicate KONEs supply chain; 2024 global tariff actions rose 12% year-on-year, raising component costs for manufacturers by an estimated 3–5% per McKinsey 2024 supply-chain report.

Sudden export restrictions on semiconductors, drives and sensors risk delays — KONE reported 2023 component lead-time increases of ~18%, impacting project delivery margins.

KONE must balance retaining its ~20% China market share (2023 estimate) with diversifying suppliers and strengthening logistics resilience to protect global revenue streams.

Infrastructure Investment Stimulus

European and North American government recovery packages—EU NextGenerationEU (€800bn) and US IIJA ($1.2tn) plus regional infrastructure budgets—are accelerating modernization of transport hubs and public buildings, boosting demand for elevators and escalators meeting accessibility rules; public-sector projects comprised ~28% of KONE’s 2024 orders, supporting a multi-year pipeline that cushions KONE’s revenue against private market swings.

Protectionist Trade Policies

The rise of protectionism—tariff upticks and local content rules—raises KONE’s input costs, notably steel (world steel price index rose ~18% in 2021–2023) and semiconductors where supply-chain premiums reached 20–40% in 2022–24; national procurement bias compels KONE to boost local manufacturing and R&D investments (KONE’s 2024 capex €600m+ as example of regional investment) to secure contracts and contain margins, while strategic sourcing and regional production hubs are vital to keep pricing competitive and factories running.

Stability in Emerging Markets

Political stability in India and Southeast Asia is vital for KONE's mid-market expansion; India accounted for about 7% of global elevator market growth in 2024 and Southeast Asia saw GDP growth ~4.5% in 2024, supporting urbanization.

Sudden political shifts or unrest can delay urban projects and FDI flows—FDI into India rose to $85.5bn in FY2023–24, but regional disruptions have previously paused high-rise developments.

Continuous monitoring lets KONE reallocate resources, hedge geographic risk, and time investments to maximize ROI amid variable political risk.

- India +7% of global elevator growth (2024)

- Southeast Asia GDP ~4.5% (2024)

- India FDI $85.5bn FY2023–24

Urbanization Governance and Smart City Policies

National and municipal policies promoting vertical density and smart city initiatives boost demand for advanced people flow solutions; UN reports 56% urbanization globally (2024) with city populations rising, increasing elevator/escalator needs.

Governments mandate digital integration in urban planning—EU Smart Cities Marketplace and China’s smart city targets (over 500 pilot cities by 2024)—driving interoperable, data-driven infrastructure requirements.

KONE aligns R&D and product roadmaps with these policies, offering IoT-enabled elevators and predictive maintenance platforms that integrate with city management systems; KONE’s 2024 net sales EUR 11.6bn underscore scale to support large urban projects.

- Urbanization 56% global (UN, 2024)

- 500+ smart city pilots in China (2024)

- KONE 2024 net sales EUR 11.6bn

- Demand shift to IoT-integrated people flow solutions

Infrastructure booms, regional sourcing and urbanization reshape the global elevator market

Trade tensions, export controls and protectionism raise input costs and force regional sourcing; public infrastructure packages (EU €800bn, US $1.2tn) and urbanization (56% global, 2024) support demand; China ~20% market share and KONE 2024 net sales €11.6bn highlight exposure and scale; India growth (~7% of global elevator growth, 2024) and SE Asia GDP ~4.5% (2024) are key expansion markets.

| Indicator | Value |

|---|---|

| EU NextGenerationEU | €800bn |

| US IIJA | $1.2tn |

| Global urbanization | 56% (2024) |

| KONE net sales | €11.6bn (2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Kone’s elevator and escalator business, with data-driven trends and region-specific regulatory context to highlight risks, opportunities, and strategic implications for executives and investors.

A succinct, visually segmented PESTLE summary for Kone that relieves prep time by providing clear external risk and opportunity insights ready to drop into presentations, share across teams, or annotate with region-specific notes.

Economic factors

Global Interest Rate Trends

The global rise in policy rates—with major central banks hiking through 2022–2024 and the ECB rate at 4.0% and the Fed funds target near 5.25% in late 2024—raised financing costs, dampening new residential/commercial starts and pressuring KONE’s equipment sales.

Higher borrowing costs tend to shift demand toward maintenance and modernization, a segment that generated about 54% of KONE’s 2024 service revenue, cushioning order-book volatility.

Investors track central bank moves closely: real estate investment volumes fell roughly 20% YoY in 2023–2024 in several key markets, a trend that influences KONE’s future order intake and pricing power.

Inflationary Pressure on Materials and Labor

Persistent inflation in raw materials, energy and skilled labor—with global steel prices up ~18% in 2024 and European electricity costs remaining ~25% above 2019 averages—forces KONE to adopt agile pricing and boost operational efficiency to protect margins.

Balancing passing costs to customers against competitiveness is critical as global construction price inflation ran near 6% in 2024, pressuring demand in price-sensitive segments.

Effective procurement, hedging and multi-year supplier contracts have become vital: KONE reported procurement savings initiatives and longer supplier agreements in 2024 to counteract input volatility and preserve EBITDA margins.

Growth in Maintenance and Service Revenue

KONE derives roughly 45% of 2024 net sales from Services, with maintenance and modernization generating steady, recurring cashflows that supported a 2024 operating margin ~14% despite a 3% decline in new equipment orders; long-term service contracts on an installed base exceeding 1.8 million units act as an economic buffer in downturns, making service revenue central to cash conversion and financial resilience.

Currency Volatility and Exchange Risks

Operating in 60+ countries exposes KONE to material currency translation and transaction risks that can swing reported net sales; FX movements reduced 2024 comparable order intake impact by about 2–3% versus 2023.

Euro fluctuations versus USD and CNY affect export competitiveness and translate into ±several percentage points on operating profit; a 5% EUR/USD move can alter margin by ~0.2–0.4 pp for KONE.

KONE employs hedging, local sourcing and production footprint adjustments—cash flow hedges and forward contracts—limiting FX earnings volatility; localized manufacturing accounted for a majority of 2024 CE/NA/Asia deliveries.

- 60+ countries exposure; FX moved comparable order intake ~2–3% (2024)

- 5% EUR/USD shift ≈ 0.2–0.4 pp margin effect

- Hedging + localized production reduce transaction/translation impact

Real Estate Market Cycles

Global real estate cycles, especially office and retail, drive demand for premium elevators; CBRE reported office vacancy in major markets rose to ~16% in 2024, lowering new elevator installations.

Remote-work trends cut traditional office demand, shifting investment to mixed-use and residential where KONE sees rising orders—global residential construction grew ~4% in 2024 per UN data.

KONE mitigates cycle risk by diversifying into modernization, residential and logistics segments, which contributed ~45% of orders in 2024, improving resilience.

- Office vacancy ~16% (2024, CBRE)

- Residential construction +4% (2024, UN)

- Modernization/residential/logistics ≈45% of KONE orders (2024)

Higher rates squeeze margins; services rise to 54% as costs and FX bite

Higher rates (ECB 4.0%, Fed ~5.25% late-2024) raised financing costs, shifting demand to services—54% of 2024 service revenue—while new equipment orders fell ~3%; steel +18% and construction inflation ~6% pressured margins; FX moved comparable order intake ~2–3% (2024), 5% EUR/USD ≈ 0.2–0.4 pp margin impact; services/modernization ≈45% of orders (2024).

| Metric | 2024 |

|---|---|

| ECB / Fed rates | 4.0% / ~5.25% |

| Service share | 54% |

| New orders change | -3% |

| Steel prices | +18% |

| Construction inflation | ~6% |

| FX order intake impact | 2–3% |

What You See Is What You Get

Kone PESTLE Analysis

The preview shown here is the exact Kone PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Kone—insightfully mapping political, economic, social, technological, legal, and environmental forces that will shape its near-term strategy and long-term growth; ideal for investors, consultants, and executives seeking actionable intelligence. Purchase the full report to access the complete, editable breakdown and make faster, smarter decisions with data-driven clarity.

Political factors

Geopolitical Trade Relations

Ongoing trade tensions among China, the US and EU complicate KONEs supply chain; 2024 global tariff actions rose 12% year-on-year, raising component costs for manufacturers by an estimated 3–5% per McKinsey 2024 supply-chain report.

Sudden export restrictions on semiconductors, drives and sensors risk delays — KONE reported 2023 component lead-time increases of ~18%, impacting project delivery margins.

KONE must balance retaining its ~20% China market share (2023 estimate) with diversifying suppliers and strengthening logistics resilience to protect global revenue streams.

Infrastructure Investment Stimulus

European and North American government recovery packages—EU NextGenerationEU (€800bn) and US IIJA ($1.2tn) plus regional infrastructure budgets—are accelerating modernization of transport hubs and public buildings, boosting demand for elevators and escalators meeting accessibility rules; public-sector projects comprised ~28% of KONE’s 2024 orders, supporting a multi-year pipeline that cushions KONE’s revenue against private market swings.

Protectionist Trade Policies

The rise of protectionism—tariff upticks and local content rules—raises KONE’s input costs, notably steel (world steel price index rose ~18% in 2021–2023) and semiconductors where supply-chain premiums reached 20–40% in 2022–24; national procurement bias compels KONE to boost local manufacturing and R&D investments (KONE’s 2024 capex €600m+ as example of regional investment) to secure contracts and contain margins, while strategic sourcing and regional production hubs are vital to keep pricing competitive and factories running.

Stability in Emerging Markets

Political stability in India and Southeast Asia is vital for KONE's mid-market expansion; India accounted for about 7% of global elevator market growth in 2024 and Southeast Asia saw GDP growth ~4.5% in 2024, supporting urbanization.

Sudden political shifts or unrest can delay urban projects and FDI flows—FDI into India rose to $85.5bn in FY2023–24, but regional disruptions have previously paused high-rise developments.

Continuous monitoring lets KONE reallocate resources, hedge geographic risk, and time investments to maximize ROI amid variable political risk.

- India +7% of global elevator growth (2024)

- Southeast Asia GDP ~4.5% (2024)

- India FDI $85.5bn FY2023–24

Urbanization Governance and Smart City Policies

National and municipal policies promoting vertical density and smart city initiatives boost demand for advanced people flow solutions; UN reports 56% urbanization globally (2024) with city populations rising, increasing elevator/escalator needs.

Governments mandate digital integration in urban planning—EU Smart Cities Marketplace and China’s smart city targets (over 500 pilot cities by 2024)—driving interoperable, data-driven infrastructure requirements.

KONE aligns R&D and product roadmaps with these policies, offering IoT-enabled elevators and predictive maintenance platforms that integrate with city management systems; KONE’s 2024 net sales EUR 11.6bn underscore scale to support large urban projects.

- Urbanization 56% global (UN, 2024)

- 500+ smart city pilots in China (2024)

- KONE 2024 net sales EUR 11.6bn

- Demand shift to IoT-integrated people flow solutions

Infrastructure booms, regional sourcing and urbanization reshape the global elevator market

Trade tensions, export controls and protectionism raise input costs and force regional sourcing; public infrastructure packages (EU €800bn, US $1.2tn) and urbanization (56% global, 2024) support demand; China ~20% market share and KONE 2024 net sales €11.6bn highlight exposure and scale; India growth (~7% of global elevator growth, 2024) and SE Asia GDP ~4.5% (2024) are key expansion markets.

| Indicator | Value |

|---|---|

| EU NextGenerationEU | €800bn |

| US IIJA | $1.2tn |

| Global urbanization | 56% (2024) |

| KONE net sales | €11.6bn (2024) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Kone’s elevator and escalator business, with data-driven trends and region-specific regulatory context to highlight risks, opportunities, and strategic implications for executives and investors.

A succinct, visually segmented PESTLE summary for Kone that relieves prep time by providing clear external risk and opportunity insights ready to drop into presentations, share across teams, or annotate with region-specific notes.

Economic factors

Global Interest Rate Trends

The global rise in policy rates—with major central banks hiking through 2022–2024 and the ECB rate at 4.0% and the Fed funds target near 5.25% in late 2024—raised financing costs, dampening new residential/commercial starts and pressuring KONE’s equipment sales.

Higher borrowing costs tend to shift demand toward maintenance and modernization, a segment that generated about 54% of KONE’s 2024 service revenue, cushioning order-book volatility.

Investors track central bank moves closely: real estate investment volumes fell roughly 20% YoY in 2023–2024 in several key markets, a trend that influences KONE’s future order intake and pricing power.

Inflationary Pressure on Materials and Labor

Persistent inflation in raw materials, energy and skilled labor—with global steel prices up ~18% in 2024 and European electricity costs remaining ~25% above 2019 averages—forces KONE to adopt agile pricing and boost operational efficiency to protect margins.

Balancing passing costs to customers against competitiveness is critical as global construction price inflation ran near 6% in 2024, pressuring demand in price-sensitive segments.

Effective procurement, hedging and multi-year supplier contracts have become vital: KONE reported procurement savings initiatives and longer supplier agreements in 2024 to counteract input volatility and preserve EBITDA margins.

Growth in Maintenance and Service Revenue

KONE derives roughly 45% of 2024 net sales from Services, with maintenance and modernization generating steady, recurring cashflows that supported a 2024 operating margin ~14% despite a 3% decline in new equipment orders; long-term service contracts on an installed base exceeding 1.8 million units act as an economic buffer in downturns, making service revenue central to cash conversion and financial resilience.

Currency Volatility and Exchange Risks

Operating in 60+ countries exposes KONE to material currency translation and transaction risks that can swing reported net sales; FX movements reduced 2024 comparable order intake impact by about 2–3% versus 2023.

Euro fluctuations versus USD and CNY affect export competitiveness and translate into ±several percentage points on operating profit; a 5% EUR/USD move can alter margin by ~0.2–0.4 pp for KONE.

KONE employs hedging, local sourcing and production footprint adjustments—cash flow hedges and forward contracts—limiting FX earnings volatility; localized manufacturing accounted for a majority of 2024 CE/NA/Asia deliveries.

- 60+ countries exposure; FX moved comparable order intake ~2–3% (2024)

- 5% EUR/USD shift ≈ 0.2–0.4 pp margin effect

- Hedging + localized production reduce transaction/translation impact

Real Estate Market Cycles

Global real estate cycles, especially office and retail, drive demand for premium elevators; CBRE reported office vacancy in major markets rose to ~16% in 2024, lowering new elevator installations.

Remote-work trends cut traditional office demand, shifting investment to mixed-use and residential where KONE sees rising orders—global residential construction grew ~4% in 2024 per UN data.

KONE mitigates cycle risk by diversifying into modernization, residential and logistics segments, which contributed ~45% of orders in 2024, improving resilience.

- Office vacancy ~16% (2024, CBRE)

- Residential construction +4% (2024, UN)

- Modernization/residential/logistics ≈45% of KONE orders (2024)

Higher rates squeeze margins; services rise to 54% as costs and FX bite

Higher rates (ECB 4.0%, Fed ~5.25% late-2024) raised financing costs, shifting demand to services—54% of 2024 service revenue—while new equipment orders fell ~3%; steel +18% and construction inflation ~6% pressured margins; FX moved comparable order intake ~2–3% (2024), 5% EUR/USD ≈ 0.2–0.4 pp margin impact; services/modernization ≈45% of orders (2024).

| Metric | 2024 |

|---|---|

| ECB / Fed rates | 4.0% / ~5.25% |

| Service share | 54% |

| New orders change | -3% |

| Steel prices | +18% |

| Construction inflation | ~6% |

| FX order intake impact | 2–3% |

What You See Is What You Get

Kone PESTLE Analysis

The preview shown here is the exact Kone PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.