Kotak Mahindra Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

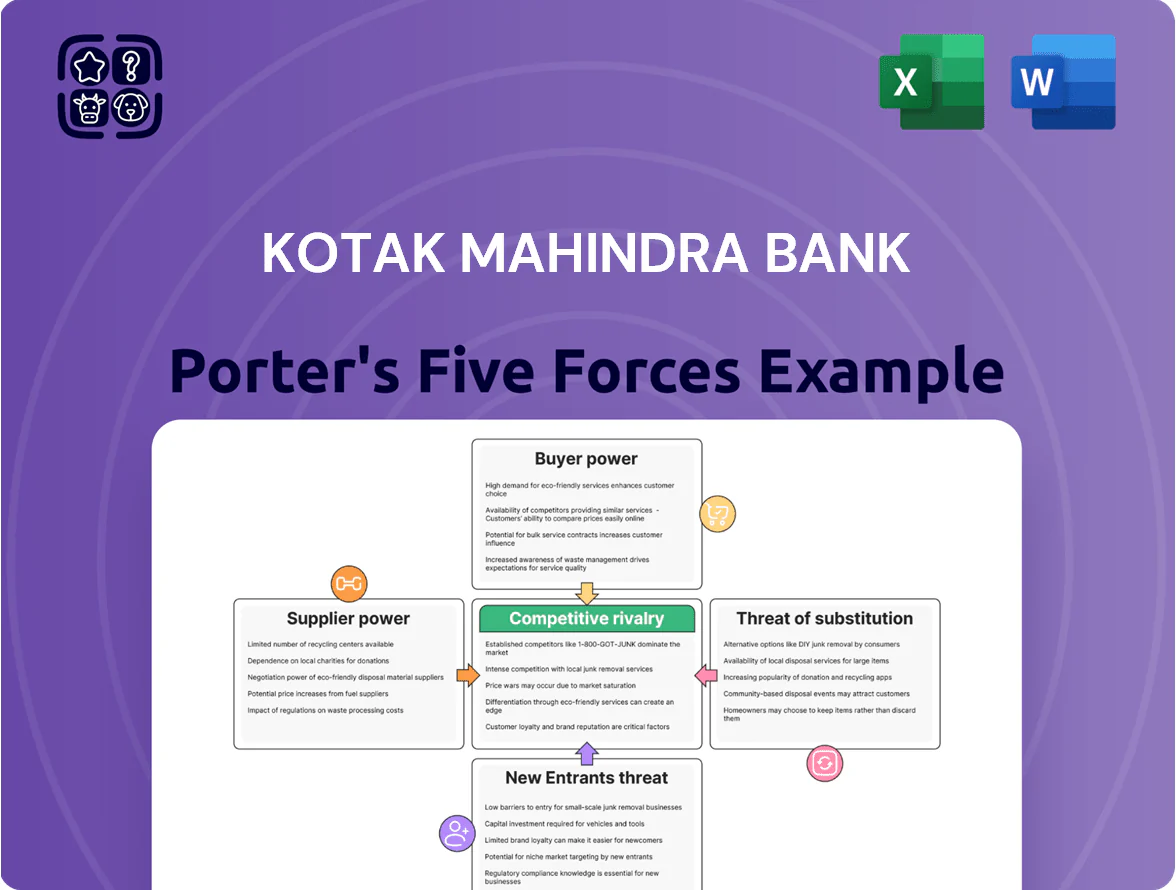

Kotak Mahindra Bank faces intense rivalry from large private and public banks, rising fintech challengers, and price-sensitive corporate and retail clients, while regulatory oversight and capital requirements temper aggressive expansion.

Supplier and buyer powers are moderate—technology vendors and large depositors can influence terms, yet strong brand and distribution scale give Kotak negotiating leverage.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kotak Mahindra Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of low-cost retail deposits

Retail depositors are Kotak Mahindra Bank’s primary suppliers of funds; by Q3 2025 the bank reported CASA (current account saving account) ratio near 44%, signaling a granular, low-cost deposit base that limits individual depositor leverage.

Kotak’s strong brand and branch/digital mix supported retail deposits of ₹2.8 lakh crore in FY2025, reducing supplier bargaining power versus wholesale funding sources.

The bank’s ability to price CASA competitively—average CASA cost below 3% in 2025—ensures steady access to low-cost capital.

Dependence on technology and fintech partners

Suppliers of core banking software, cloud infrastructure, and cybersecurity exert strong leverage over Kotak Mahindra Bank because switching costs run into tens of millions USD and integration timelines exceed 12–24 months; in 2024 Kotak reported 48% of transactions via digital channels, raising supplier importance.

Influence of the Reserve Bank of India

The Reserve Bank of India (RBI) is the dominant supplier of regulatory capital and liquidity for Kotak Mahindra Bank via tools like the repo rate (6.50% as of Dec 2025) and standing liquidity facilities; changes in CRR (4.50% in Dec 2025) and SLR (18.00% in Dec 2025) directly affect Kotak’s available funds and funding cost, forcing strict compliance and making the RBI the most powerful supplier in the bank’s ecosystem.

Human capital and skilled labor market

The limited pool of specialists in investment banking, data science, and risk gives top performers strong bargaining power; Kotak reported a 12% rise in tech hiring costs in 2024 and faces poaching from HDFC, ICICI, and fintechs like Razorpay.

Kotak must offer market-leading pay, stock incentives, and training — attrition in digital roles hit 18% bank-wide in FY2024, boosting wage inflation for front-office talent.

- 12% rise in tech hiring costs (2024)

- 18% digital-role attrition (FY2024)

- Competition: HDFC, ICICI, Razorpay

- Need: pay, equity, reskilling

Access to wholesale and international capital markets

For non-deposit funding, Kotak Mahindra Bank (Kotak) leans on institutional investors and international bond markets; supplier leverage depends on Kotak’s credit rating and global liquidity. By 2025 Kotak’s CET1 ratio ~16.5% and net worth strength let it secure tighter spreads—its $500m 2024 dollar bond printed at ~5.5%. Still, sudden global liquidity tightening can quickly raise funding costs and supplier bargaining power.

- Depends on institutional investors, intl bond markets

- CET1 ≈16.5% (2025), $500m 2024 bond at ~5.5%

- Bargaining power rises if credit rating falls

- Global liquidity shifts remain key external risk

Retail deposits cushion funding; RBI rules & tech vendors, talent squeeze raise supplier power

Retail depositors (CASA ~44% Q3 2025; retail deposits ₹2.8 lakh crore FY2025) limit supplier power for funds, while RBI policy (repo 6.50%, CRR 4.50%, SLR 18.00% Dec 2025) and core-software/cloud vendors (12–24 month switch cost) hold strong leverage; tech hiring costs +12% (2024) and 18% digital attrition raise labor supplier power.

| Item | Key metric |

|---|---|

| CASA | ~44% Q3 2025 |

| Retail deposits | ₹2.8 lakh crore FY2025 |

| Repo/CRR/SLR | 6.50% / 4.50% / 18.00% (Dec 2025) |

| Tech hiring | +12% (2024) |

| Attrition | 18% digital (FY2024) |

What is included in the product

Tailored exclusively for Kotak Mahindra Bank, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

One-sheet Porter's Five Forces for Kotak Mahindra Bank—quickly spot competitive pressures, tailor force ratings to new regulations or entrants, and paste directly into pitch decks for fast executive decisions.

Customers Bargaining Power

High price sensitivity in retail lending

Retail borrowers for home and personal loans use digital comparison platforms (e.g., BankBazaar, PaisaBazaar) and rate dashboards, raising price sensitivity; as of Dec 2025, ~64% of Indian retail loan shoppers compare rates online.

Low switching costs for digital banking users

Bargaining strength of large corporate clients

Large corporate borrowers and institutions wield strong bargaining power at Kotak Mahindra Bank because top 200 corporate clients accounted for roughly 28% of corporate loan book as of FY2025, so they demand customized credit lines, lower yields and discounted cash-management fees; Kotak reported average corporate loan yield of 7.1% in FY2025, and management notes margin pressure from bespoke pricing to retain high-value relationships.

Rising expectations for integrated financial ecosystems

Modern customers demand seamless integration of banking, insurance, and wealth management in one platform; Kotak Mahindra Bank faces pressure after Paytm Payments Bank and Zerodha-linked platforms grew active user bases by 2025 (Paytm ~100m, Zerodha ~8m clients), raising churn risk if Kotak’s super-app lags.

If Kotak fails to deliver a superior super-app experience, customers will migrate to platforms offering convenience and lower fees; retail digital transactions in India rose 22% CAGR 2019–2024, giving consumers leverage.

This shift empowers customers to demand more value-added, lower-cost services; Kotak’s Wealth Management AUM was Rs 1.2 lakh crore (FY2024), so retaining clients depends on integrated offerings and competitive pricing.

- Customers: expect banking + insurance + wealth in one app

- Migration risk: high if super-app UX or pricing lags

- Market signal: digital txn CAGR 22% (2019–2024)

- Kotak AUM FY2024: Rs 1.2 lakh crore

Impact of the Account Aggregator framework

By 2025 the Account Aggregator (AA) network in India reached over 55 million consent transactions, giving customers direct control of financial data and enabling instant sharing of credit histories with multiple lenders to shop rates.

This democratization raised borrower bargaining power vs Kotak Mahindra Bank: faster price discovery, higher rate competition, and increased demand for personalized offers—industry data show ~12–18 bps tighter spreads on unsecured loans where AA was used.

- 55m+ AA consent transactions by 2025

- Instant multi-lender credit sharing increases rate transparency

- 12–18 bps average tightening of unsecured loan spreads

- Higher demand for tailored pricing and faster decisions

Kotak must match digital pricing, UX & integrated offers to protect CASA, margins & Rs1.2Lcr AUM

Customers wield rising power: digital rate comparison (64% of loan shoppers online by Dec 2025), 55m+ AA consents (2025), UPI 9.2bn monthly txns (Dec 2025) and neo-bank churn (18–22% of new incumbents’ clients in 2024–25) force Kotak to match pricing, UX and integrated offerings to protect CASA, margins and Rs 1.2 lakh crore wealth AUM.

| Metric | Value |

|---|---|

| Online loan shoppers (Dec 2025) | 64% |

| AA consent txns (2025) | 55m+ |

| UPI monthly txns (Dec 2025) | 9.2bn |

| Neo-bank conversion (2024–25) | 18–22% |

| Kotak Wealth AUM (FY2024) | Rs 1.2 lakh crore |

Same Document Delivered

Kotak Mahindra Bank Porter's Five Forces Analysis

This preview shows the exact Kotak Mahindra Bank Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

You're looking at the actual deliverable: a complete, professionally written Five Forces assessment available for instant download the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kotak Mahindra Bank faces intense rivalry from large private and public banks, rising fintech challengers, and price-sensitive corporate and retail clients, while regulatory oversight and capital requirements temper aggressive expansion.

Supplier and buyer powers are moderate—technology vendors and large depositors can influence terms, yet strong brand and distribution scale give Kotak negotiating leverage.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kotak Mahindra Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of low-cost retail deposits

Retail depositors are Kotak Mahindra Bank’s primary suppliers of funds; by Q3 2025 the bank reported CASA (current account saving account) ratio near 44%, signaling a granular, low-cost deposit base that limits individual depositor leverage.

Kotak’s strong brand and branch/digital mix supported retail deposits of ₹2.8 lakh crore in FY2025, reducing supplier bargaining power versus wholesale funding sources.

The bank’s ability to price CASA competitively—average CASA cost below 3% in 2025—ensures steady access to low-cost capital.

Dependence on technology and fintech partners

Suppliers of core banking software, cloud infrastructure, and cybersecurity exert strong leverage over Kotak Mahindra Bank because switching costs run into tens of millions USD and integration timelines exceed 12–24 months; in 2024 Kotak reported 48% of transactions via digital channels, raising supplier importance.

Influence of the Reserve Bank of India

The Reserve Bank of India (RBI) is the dominant supplier of regulatory capital and liquidity for Kotak Mahindra Bank via tools like the repo rate (6.50% as of Dec 2025) and standing liquidity facilities; changes in CRR (4.50% in Dec 2025) and SLR (18.00% in Dec 2025) directly affect Kotak’s available funds and funding cost, forcing strict compliance and making the RBI the most powerful supplier in the bank’s ecosystem.

Human capital and skilled labor market

The limited pool of specialists in investment banking, data science, and risk gives top performers strong bargaining power; Kotak reported a 12% rise in tech hiring costs in 2024 and faces poaching from HDFC, ICICI, and fintechs like Razorpay.

Kotak must offer market-leading pay, stock incentives, and training — attrition in digital roles hit 18% bank-wide in FY2024, boosting wage inflation for front-office talent.

- 12% rise in tech hiring costs (2024)

- 18% digital-role attrition (FY2024)

- Competition: HDFC, ICICI, Razorpay

- Need: pay, equity, reskilling

Access to wholesale and international capital markets

For non-deposit funding, Kotak Mahindra Bank (Kotak) leans on institutional investors and international bond markets; supplier leverage depends on Kotak’s credit rating and global liquidity. By 2025 Kotak’s CET1 ratio ~16.5% and net worth strength let it secure tighter spreads—its $500m 2024 dollar bond printed at ~5.5%. Still, sudden global liquidity tightening can quickly raise funding costs and supplier bargaining power.

- Depends on institutional investors, intl bond markets

- CET1 ≈16.5% (2025), $500m 2024 bond at ~5.5%

- Bargaining power rises if credit rating falls

- Global liquidity shifts remain key external risk

Retail deposits cushion funding; RBI rules & tech vendors, talent squeeze raise supplier power

Retail depositors (CASA ~44% Q3 2025; retail deposits ₹2.8 lakh crore FY2025) limit supplier power for funds, while RBI policy (repo 6.50%, CRR 4.50%, SLR 18.00% Dec 2025) and core-software/cloud vendors (12–24 month switch cost) hold strong leverage; tech hiring costs +12% (2024) and 18% digital attrition raise labor supplier power.

| Item | Key metric |

|---|---|

| CASA | ~44% Q3 2025 |

| Retail deposits | ₹2.8 lakh crore FY2025 |

| Repo/CRR/SLR | 6.50% / 4.50% / 18.00% (Dec 2025) |

| Tech hiring | +12% (2024) |

| Attrition | 18% digital (FY2024) |

What is included in the product

Tailored exclusively for Kotak Mahindra Bank, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

One-sheet Porter's Five Forces for Kotak Mahindra Bank—quickly spot competitive pressures, tailor force ratings to new regulations or entrants, and paste directly into pitch decks for fast executive decisions.

Customers Bargaining Power

High price sensitivity in retail lending

Retail borrowers for home and personal loans use digital comparison platforms (e.g., BankBazaar, PaisaBazaar) and rate dashboards, raising price sensitivity; as of Dec 2025, ~64% of Indian retail loan shoppers compare rates online.

Low switching costs for digital banking users

Bargaining strength of large corporate clients

Large corporate borrowers and institutions wield strong bargaining power at Kotak Mahindra Bank because top 200 corporate clients accounted for roughly 28% of corporate loan book as of FY2025, so they demand customized credit lines, lower yields and discounted cash-management fees; Kotak reported average corporate loan yield of 7.1% in FY2025, and management notes margin pressure from bespoke pricing to retain high-value relationships.

Rising expectations for integrated financial ecosystems

Modern customers demand seamless integration of banking, insurance, and wealth management in one platform; Kotak Mahindra Bank faces pressure after Paytm Payments Bank and Zerodha-linked platforms grew active user bases by 2025 (Paytm ~100m, Zerodha ~8m clients), raising churn risk if Kotak’s super-app lags.

If Kotak fails to deliver a superior super-app experience, customers will migrate to platforms offering convenience and lower fees; retail digital transactions in India rose 22% CAGR 2019–2024, giving consumers leverage.

This shift empowers customers to demand more value-added, lower-cost services; Kotak’s Wealth Management AUM was Rs 1.2 lakh crore (FY2024), so retaining clients depends on integrated offerings and competitive pricing.

- Customers: expect banking + insurance + wealth in one app

- Migration risk: high if super-app UX or pricing lags

- Market signal: digital txn CAGR 22% (2019–2024)

- Kotak AUM FY2024: Rs 1.2 lakh crore

Impact of the Account Aggregator framework

By 2025 the Account Aggregator (AA) network in India reached over 55 million consent transactions, giving customers direct control of financial data and enabling instant sharing of credit histories with multiple lenders to shop rates.

This democratization raised borrower bargaining power vs Kotak Mahindra Bank: faster price discovery, higher rate competition, and increased demand for personalized offers—industry data show ~12–18 bps tighter spreads on unsecured loans where AA was used.

- 55m+ AA consent transactions by 2025

- Instant multi-lender credit sharing increases rate transparency

- 12–18 bps average tightening of unsecured loan spreads

- Higher demand for tailored pricing and faster decisions

Kotak must match digital pricing, UX & integrated offers to protect CASA, margins & Rs1.2Lcr AUM

Customers wield rising power: digital rate comparison (64% of loan shoppers online by Dec 2025), 55m+ AA consents (2025), UPI 9.2bn monthly txns (Dec 2025) and neo-bank churn (18–22% of new incumbents’ clients in 2024–25) force Kotak to match pricing, UX and integrated offerings to protect CASA, margins and Rs 1.2 lakh crore wealth AUM.

| Metric | Value |

|---|---|

| Online loan shoppers (Dec 2025) | 64% |

| AA consent txns (2025) | 55m+ |

| UPI monthly txns (Dec 2025) | 9.2bn |

| Neo-bank conversion (2024–25) | 18–22% |

| Kotak Wealth AUM (FY2024) | Rs 1.2 lakh crore |

Same Document Delivered

Kotak Mahindra Bank Porter's Five Forces Analysis

This preview shows the exact Kotak Mahindra Bank Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, fully formatted and ready for use.

You're looking at the actual deliverable: a complete, professionally written Five Forces assessment available for instant download the moment you buy.