KPIT Technologies Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

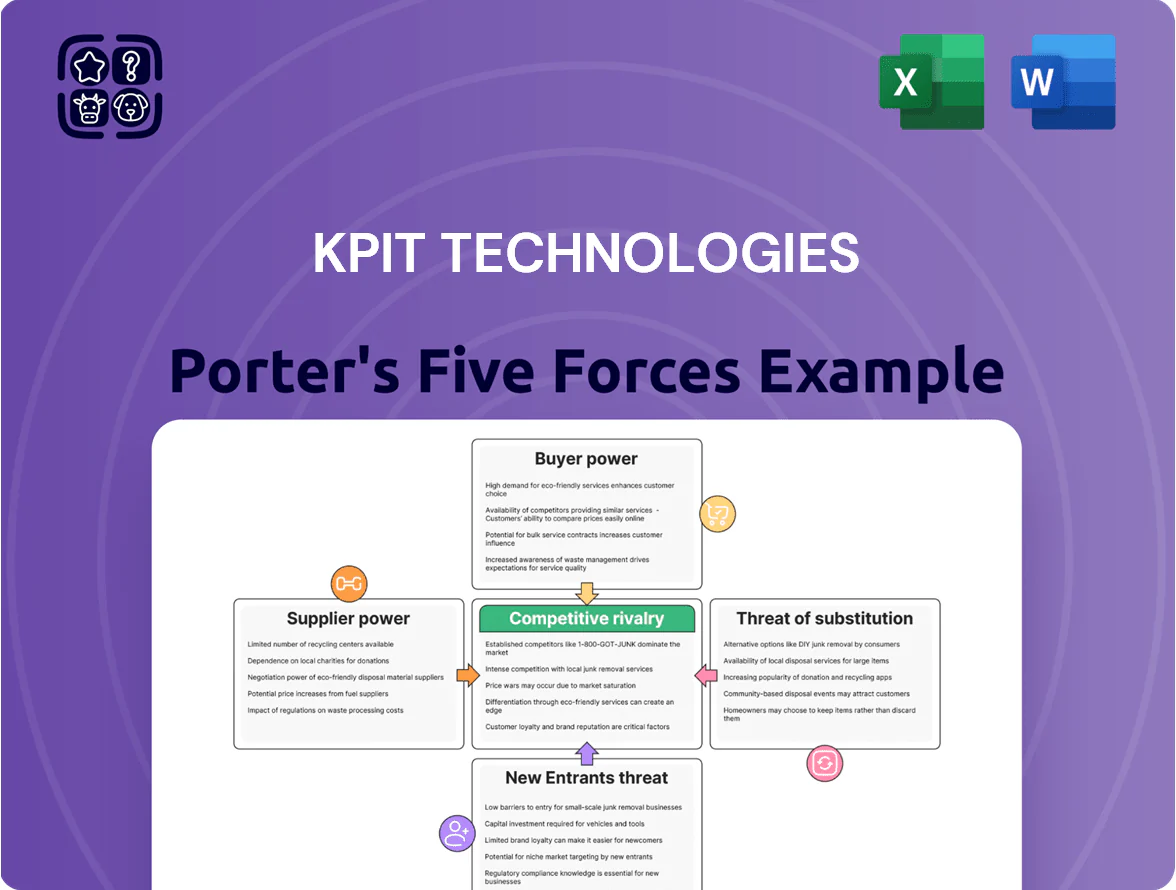

KPIT Technologies faces moderate rivalry driven by specialized automotive software competitors and pricing pressure from larger IT services firms, while supplier bargaining remains low and buyer power is rising with demand for integrated digital solutions.

Suppliers Bargaining Power

Access to Specialized Engineering Talent

Primary suppliers for KPIT are highly skilled software engineers in automotive electronics and embedded systems; their niche skills in autonomous driving and electrification give them strong leverage as of late 2025. Global shortage estimates show ~40% gap in autonomous-driving talent vs. demand, pushing median specialist salaries up 18–25% year-over-year in 2024–25. KPIT must invest ~8–10% of revenue in training, hiring bonuses, and retention to sustain delivery and offset rising wage inflation. If retention slips past 15% attrition, project timelines and margins will deteriorate quickly.

Dependence on Cloud Infrastructure Providers

KPIT depends on hyperscalers—AWS, Microsoft Azure, Google Cloud—to host and process petabyte-scale datasets for autonomous-vehicle testing; in 2024 cloud IaaS market share was ~64% for these three combined (Gartner, Nov 2024).

Their control of capacity, pricing, and specialized AI accelerators gives suppliers strong bargaining power over KPIT’s AI and data-analytics offerings.

KPIT can use multi-cloud, but estimated migration and integration costs of $0.5–2M per major workload plus months of revalidation create supplier stickiness.

Partnerships with Semiconductor and Hardware Vendors

KPIT’s ADAS and electrification software is tightly coupled with chipmakers such as Nvidia, Qualcomm, and NXP, so vendor roadmaps shape KPIT’s product timelines and R&D spend.

In 2024 KPIT reported R&D at ~13% of revenue (~INR 1,050 crore FY24), reflecting frequent rework to match new silicon architectures and SDKs.

Supply shifts or scarce dev kits can force engineering pivots; this gives suppliers moderate bargaining power over KPIT’s costs and time-to-market.

Software Tooling and Simulation Vendors

Specialized simulation and CAD/CAM vendors—few in number—hold pricing power over KPIT because high-fidelity automotive simulation is critical for virtual testing of ADAS and autonomous stacks; in 2024 the automotive simulation market was valued at about $3.2bn and is concentrated among vendors like ANSYS, dSPACE, and Siemens, keeping license and compute costs sticky.

- Few suppliers: high concentration (top vendors >60% market share)

- Critical input: enables virtual validation pre-prototype

- Pricing power: license + cloud compute raise project OPEX by ~5–12%

Academic and Research Collaborations

KPIT sources foundational research and talent from top technical universities and labs worldwide, which act like suppliers by controlling innovation pipelines and specialized engineers; in 2024 KPIT hired ~18% of its campus recruits from 15 target universities across India and Europe.

Maintaining these ties is critical to lead in solid-state batteries and hydrogen fuel cells—areas where KPIT partners with 6 academic consortia since 2022 and allocates ~3–4% of annual R&D spend to collaborative projects.

- 18% campus hires from 15 target universities (2024)

- 6 academic consortia partnerships since 2022

- 3–4% of annual R&D spend on collaborations

Supplier power hikes KPIT costs: talent gap, rising wages, hyperscaler & chip risks

Suppliers hold strong-to-moderate power: niche autonomous-electronics talent (40% global gap, salaries +18–25% in 2024–25) and concentrated hyperscalers (AWS/Azure/GCP ~64% IaaS share, Nov 2024) raise KPIT’s costs and stickiness; chip and simulation vendors (ANSYS, dSPACE, Nvidia, NXP) drive R&D rework (R&D ~13% revenue, INR 1,050 crore FY24) and delay risks if attrition >15%.

| Metric | Value |

|---|---|

| Autonomous talent gap | ~40% |

| Specialist salary rise (2024–25) | +18–25% |

| Hyperscaler IaaS share (2024) | ~64% |

| R&D spend (FY24) | ~13% rev / INR 1,050 crore |

| Attrition risk threshold | 15% |

What is included in the product

Tailored exclusively for KPIT Technologies, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging disruptive threats shaping its profitability and strategic positioning.

Compact Porter's Five Forces view for KPIT Technologies—spot supplier, buyer, and competitive pressures instantly to guide client-win strategies and pricing decisions.

Customers Bargaining Power

Concentration of Global Automotive OEMs

KPIT’s FY2024 revenue shows concentration: roughly 55% came from global automotive OEMs and Tier‑1s, so a few buyers drive most sales and can press on pricing and contract terms given their volume. These customers' bargaining power raises margin pressure—larger deals often demand fixed‑price or stringent SLAs. KPIT reduces this risk by acting as a strategic partner, offering IP‑led software and long‑term engineering programs that boost switching costs and recurring revenue.

High Switching Costs for Integrated Software

Once KPIT’s software is embedded in a vehicle’s electronic control units (ECUs), switching providers is technically complex and costly—OEMs face sensor, middleware, and validation rework that can exceed $5–20 million per model, creating strong lock-in across a typical 6–8 year model lifecycle. This deep tie to the Software Defined Vehicle (SDV) stack cuts customer bargaining power sharply after development starts, reducing renegotiation leverage and making post-integration provider changes rare.

Demand for Accelerated Time to Market

Requirement for Stringent Safety and Compliance Standards

Customers require strict adherence to ISO 26262 functional safety and UNECE WP.29 cybersecurity regs, raising switching costs; 2024 auto suppliers with ISO 26262 certification showed 18% lower contract churn in a BCG study. KPIT’s track record—>500 certification projects and 25% YoY revenue from safety/cyber services in FY2024—reduces customer willingness to switch to cheaper unproven vendors.

- ISO 26262 + WP.29 compliance required

- KPIT: ~500 certification projects

- 25% FY2024 revenue from safety/cyber

- BCG: 18% lower churn for certified suppliers

Shift Toward Strategic Co-Innovation Models

By 2025 many OEMs and Tier-1s shifted from vendor deals to co-innovation; KPIT reported ~20% of revenue from partnership-based IP-sharing projects in FY2024, reducing customer bargaining power as risk and IP are jointly held.

As KPIT functions like an R&D extension—phasing into product roadmaps and joint road-tested IP—clients face higher switching costs; firms estimate replacement would cost 30–50% more and add 9–18 months to timelines.

Customers Moderately Powered, But KPIT’s IP, Certifications & High Switch Costs Tilt Advantage

Customers hold moderate bargaining power: ~55% revenue from few OEMs/Tier‑1s raises leverage, but KPIT’s IP‑led stacks, >500 certification projects, 25% FY2024 safety/cyber revenue, ~20% IP‑sharing revenue, and high switching costs (replacement +30–50%, +9–18 months) tilt power toward KPIT.

| Metric | Value |

|---|---|

| Revenue concentration | ~55% |

| Cert projects | >500 |

| Safety/cyber rev | 25% FY2024 |

| IP‑sharing rev | ~20% FY2024 |

| Replacement cost premium | 30–50% |

What You See Is What You Get

KPIT Technologies Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of KPIT Technologies you'll receive immediately after purchase—no placeholders, fully formatted and ready for use. The document here is the same professionally written file available for instant download post-payment, containing detailed evaluation of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry. No mockups or samples—this is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

KPIT Technologies faces moderate rivalry driven by specialized automotive software competitors and pricing pressure from larger IT services firms, while supplier bargaining remains low and buyer power is rising with demand for integrated digital solutions.

Suppliers Bargaining Power

Access to Specialized Engineering Talent

Primary suppliers for KPIT are highly skilled software engineers in automotive electronics and embedded systems; their niche skills in autonomous driving and electrification give them strong leverage as of late 2025. Global shortage estimates show ~40% gap in autonomous-driving talent vs. demand, pushing median specialist salaries up 18–25% year-over-year in 2024–25. KPIT must invest ~8–10% of revenue in training, hiring bonuses, and retention to sustain delivery and offset rising wage inflation. If retention slips past 15% attrition, project timelines and margins will deteriorate quickly.

Dependence on Cloud Infrastructure Providers

KPIT depends on hyperscalers—AWS, Microsoft Azure, Google Cloud—to host and process petabyte-scale datasets for autonomous-vehicle testing; in 2024 cloud IaaS market share was ~64% for these three combined (Gartner, Nov 2024).

Their control of capacity, pricing, and specialized AI accelerators gives suppliers strong bargaining power over KPIT’s AI and data-analytics offerings.

KPIT can use multi-cloud, but estimated migration and integration costs of $0.5–2M per major workload plus months of revalidation create supplier stickiness.

Partnerships with Semiconductor and Hardware Vendors

KPIT’s ADAS and electrification software is tightly coupled with chipmakers such as Nvidia, Qualcomm, and NXP, so vendor roadmaps shape KPIT’s product timelines and R&D spend.

In 2024 KPIT reported R&D at ~13% of revenue (~INR 1,050 crore FY24), reflecting frequent rework to match new silicon architectures and SDKs.

Supply shifts or scarce dev kits can force engineering pivots; this gives suppliers moderate bargaining power over KPIT’s costs and time-to-market.

Software Tooling and Simulation Vendors

Specialized simulation and CAD/CAM vendors—few in number—hold pricing power over KPIT because high-fidelity automotive simulation is critical for virtual testing of ADAS and autonomous stacks; in 2024 the automotive simulation market was valued at about $3.2bn and is concentrated among vendors like ANSYS, dSPACE, and Siemens, keeping license and compute costs sticky.

- Few suppliers: high concentration (top vendors >60% market share)

- Critical input: enables virtual validation pre-prototype

- Pricing power: license + cloud compute raise project OPEX by ~5–12%

Academic and Research Collaborations

KPIT sources foundational research and talent from top technical universities and labs worldwide, which act like suppliers by controlling innovation pipelines and specialized engineers; in 2024 KPIT hired ~18% of its campus recruits from 15 target universities across India and Europe.

Maintaining these ties is critical to lead in solid-state batteries and hydrogen fuel cells—areas where KPIT partners with 6 academic consortia since 2022 and allocates ~3–4% of annual R&D spend to collaborative projects.

- 18% campus hires from 15 target universities (2024)

- 6 academic consortia partnerships since 2022

- 3–4% of annual R&D spend on collaborations

Supplier power hikes KPIT costs: talent gap, rising wages, hyperscaler & chip risks

Suppliers hold strong-to-moderate power: niche autonomous-electronics talent (40% global gap, salaries +18–25% in 2024–25) and concentrated hyperscalers (AWS/Azure/GCP ~64% IaaS share, Nov 2024) raise KPIT’s costs and stickiness; chip and simulation vendors (ANSYS, dSPACE, Nvidia, NXP) drive R&D rework (R&D ~13% revenue, INR 1,050 crore FY24) and delay risks if attrition >15%.

| Metric | Value |

|---|---|

| Autonomous talent gap | ~40% |

| Specialist salary rise (2024–25) | +18–25% |

| Hyperscaler IaaS share (2024) | ~64% |

| R&D spend (FY24) | ~13% rev / INR 1,050 crore |

| Attrition risk threshold | 15% |

What is included in the product

Tailored exclusively for KPIT Technologies, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging disruptive threats shaping its profitability and strategic positioning.

Compact Porter's Five Forces view for KPIT Technologies—spot supplier, buyer, and competitive pressures instantly to guide client-win strategies and pricing decisions.

Customers Bargaining Power

Concentration of Global Automotive OEMs

KPIT’s FY2024 revenue shows concentration: roughly 55% came from global automotive OEMs and Tier‑1s, so a few buyers drive most sales and can press on pricing and contract terms given their volume. These customers' bargaining power raises margin pressure—larger deals often demand fixed‑price or stringent SLAs. KPIT reduces this risk by acting as a strategic partner, offering IP‑led software and long‑term engineering programs that boost switching costs and recurring revenue.

High Switching Costs for Integrated Software

Once KPIT’s software is embedded in a vehicle’s electronic control units (ECUs), switching providers is technically complex and costly—OEMs face sensor, middleware, and validation rework that can exceed $5–20 million per model, creating strong lock-in across a typical 6–8 year model lifecycle. This deep tie to the Software Defined Vehicle (SDV) stack cuts customer bargaining power sharply after development starts, reducing renegotiation leverage and making post-integration provider changes rare.

Demand for Accelerated Time to Market

Requirement for Stringent Safety and Compliance Standards

Customers require strict adherence to ISO 26262 functional safety and UNECE WP.29 cybersecurity regs, raising switching costs; 2024 auto suppliers with ISO 26262 certification showed 18% lower contract churn in a BCG study. KPIT’s track record—>500 certification projects and 25% YoY revenue from safety/cyber services in FY2024—reduces customer willingness to switch to cheaper unproven vendors.

- ISO 26262 + WP.29 compliance required

- KPIT: ~500 certification projects

- 25% FY2024 revenue from safety/cyber

- BCG: 18% lower churn for certified suppliers

Shift Toward Strategic Co-Innovation Models

By 2025 many OEMs and Tier-1s shifted from vendor deals to co-innovation; KPIT reported ~20% of revenue from partnership-based IP-sharing projects in FY2024, reducing customer bargaining power as risk and IP are jointly held.

As KPIT functions like an R&D extension—phasing into product roadmaps and joint road-tested IP—clients face higher switching costs; firms estimate replacement would cost 30–50% more and add 9–18 months to timelines.

Customers Moderately Powered, But KPIT’s IP, Certifications & High Switch Costs Tilt Advantage

Customers hold moderate bargaining power: ~55% revenue from few OEMs/Tier‑1s raises leverage, but KPIT’s IP‑led stacks, >500 certification projects, 25% FY2024 safety/cyber revenue, ~20% IP‑sharing revenue, and high switching costs (replacement +30–50%, +9–18 months) tilt power toward KPIT.

| Metric | Value |

|---|---|

| Revenue concentration | ~55% |

| Cert projects | >500 |

| Safety/cyber rev | 25% FY2024 |

| IP‑sharing rev | ~20% FY2024 |

| Replacement cost premium | 30–50% |

What You See Is What You Get

KPIT Technologies Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of KPIT Technologies you'll receive immediately after purchase—no placeholders, fully formatted and ready for use. The document here is the same professionally written file available for instant download post-payment, containing detailed evaluation of competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry. No mockups or samples—this is the final deliverable.