Kratos PESTLE Analysis

Your Shortcut to Market Insight Starts Here

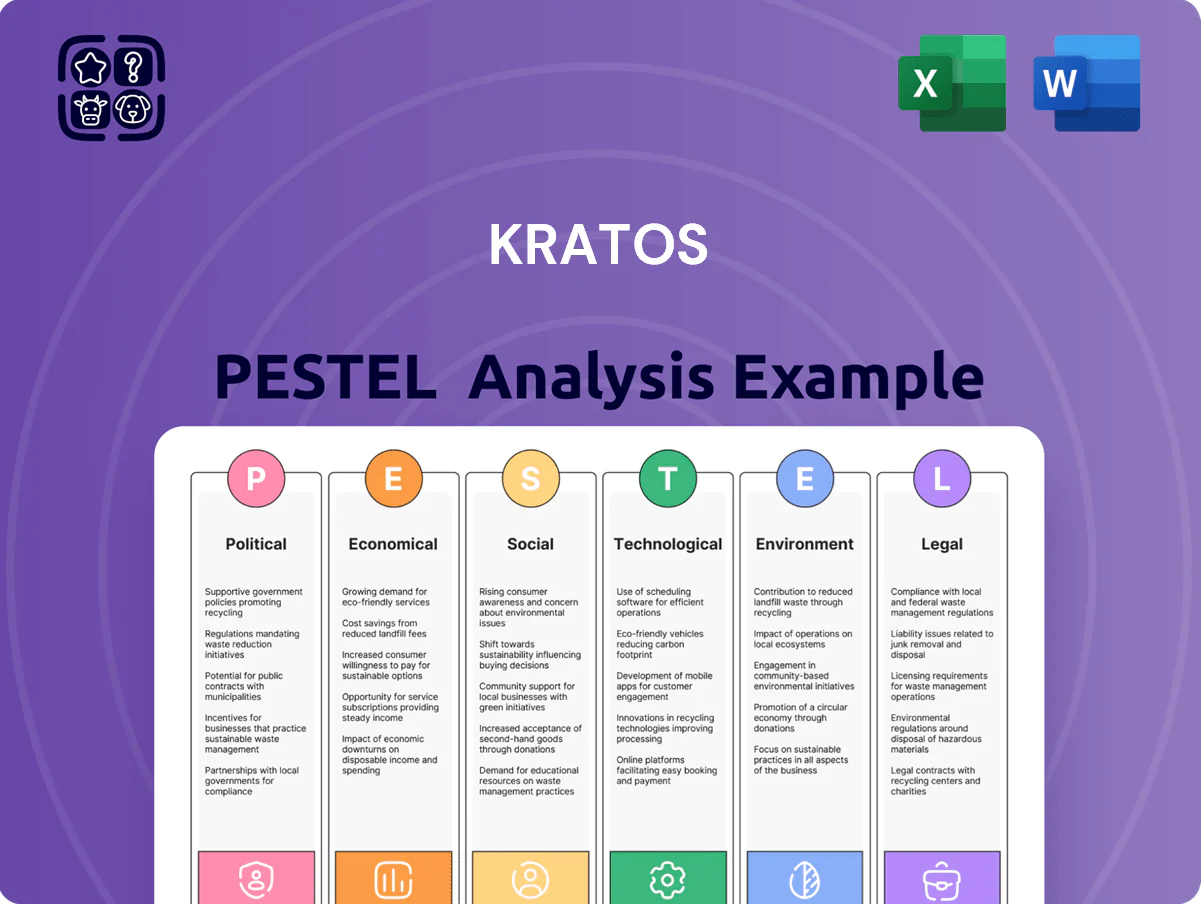

Our PESTLE Analysis for Kratos maps the political, economic, social, technological, legal, and environmental forces shaping its defense and aerospace trajectory—helping you anticipate risks and spot growth levers; download the full report for actionable insights and ready-to-use slides.

Political factors

Defense Budget Allocations

As of late 2025, Kratos’ revenue outlook is tied to DoD budget cycles, with the FY2025 defense budget at about $858 billion and unmanned systems funding rising—estimated $4–6 billion annually for attritable/loyal wingman programs—supporting Kratos’ drone pipeline.

Geopolitical Tensions

Increased friction in the Indo-Pacific and Eastern Europe has boosted demand for Kratos’s high-performance target drones and tactical UAVs, contributing to a 2024 defense order book up 18% year-over-year and revenue growth to $401 million in FY2024.

Political instability and rising defense budgets among NATO and Indo-Pacific allies—global defense spending reached $2.4 trillion in 2024—drive purchases of Kratos’s cost-effective solutions to counter peer adversaries.

Kratos’s alignment with U.S. and allied national security priorities, evidenced by multi-year contracts with the DoD and allied procurement programs, positions it as a key player in high-stakes geopolitical environments.

Export Control Policies

The US export control regime, including ITAR and recent 2024 restrictions on satellite and drone tech, directly influences Kratos’s FY2025 international revenue potential—35% of defense sector sales could be constrained if controls tighten. A 2023 uptick in allied procurement offers offsetting demand, but diplomatic shifts (e.g., US-EU/Indo-Pacific ties) can rapidly open or close markets.

Bipartisan Support for Defense Innovation

The US Congress and Pentagon have increased funding for rapid defense tech: 2025 budget boosts prototyping and innovation accounts by roughly $6.6B, benefitting non-traditional contractors like Kratos that emphasize UAVs, autonomy, and microwave electronics.

Policy shifts favor Other Transaction Authorities and OTA-like pathways, shortening procurement cycles and enabling Kratos to accelerate demonstration-to-deployment timelines for autonomous systems.

Government Contract Procurement Shifts

Political pressure to reduce the US deficit—federal budget deficit was about $1.7 trillion in FY2024—favors lower-cost, high-attrition systems over multi-decade platforms, benefiting Kratos which emphasizes affordable, rapidly manufactured unmanned systems and earned $612m revenue in FY2024.

Kratos’ cost-focused model and flexible production lines position it to capture shifting procurement; however, changes in administration or congressional priorities could reallocate defense budgets away from drones and missile systems, impacting specific business units.

- FY2024 US federal deficit ~$1.7T

- Kratos FY2024 revenue $612M

- Shift favors low-cost/high-attrition systems

- Political leadership changes risk reallocating defense spend

Kratos rides defense spending and R&D tailwinds—export controls cloud international upside

Kratos benefits from rising DoD and allied defense spend (US FY2025 ~$858B; global defense $2.4T in 2024), OTA/prototyping boosts (+$6.6B RDT&E 2025) and demand for low-cost attritable UAVs (Kratos FY2024 revenue $612M), but export controls (ITAR/2024 drone limits) and political shifts/congressional priorities pose downside risk to international sales.

| Metric | Value |

|---|---|

| US FY2025 defense | $858B |

| Global defense 2024 | $2.4T |

| RDT&E boost 2025 | +$6.6B |

| Kratos FY2024 rev | $612M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Kratos across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

A concise, visually segmented Kratos PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and align strategic planning.

Economic factors

Interest Rate Environment

By end-2025, Kratos faces a cost of capital sensitive to Fed-driven rates; the US 10-year yield rose to ~4.2% in 2024 and averaged ~4.0% in 2025, lifting borrowing costs and increasing annual interest expense on Kratos’s ~$300m long-term debt, squeezing EBITDA margins.

Higher rates raise servicing costs and can reduce free cash flow available for R&D and defense program investment, while a stabilizing rate trajectory would improve predictability for multi-year capital spending on manufacturing and infrastructure.

Supply Chain Inflation

Supply chain inflation—driven by a 12–18% rise (2023–2024) in prices for specialized composites and a 9% increase in semiconductors—raised Kratos’ unit production costs, prompting FY2024 cost-control programs that reduced procurement spend by an estimated $45–60 million and renegotiated multi-year supplier contracts to cap input-price exposure; managing these pressures is critical to keep unmanned systems price-competitive amid aerospace inflation outpacing CPI.

Labor Market Dynamics

The scarcity of aerospace engineers and cybersecurity experts raises labor costs; US median annual wage for aerospace engineers was about $122,270 in 2023 and cybersecurity roles saw median salaries near $103,590, pushing Kratos to offer premium compensation to compete. Competitive packages, including equity and training, are essential to retain talent for complex systems. Tech-sector hiring slowdowns in 2024–25 could ease pressure, while renewed defense spending may intensify it.

Global Defense Spending Trends

Global GDP growth slowed to an estimated 3.1% in 2024, pressuring defense spend in some NATO and allied states that collectively account for roughly 70% of Kratos’s defense market.

Economic downturns can delay noncritical procurements—2023 saw several allied maintenance contracts deferred—potentially reducing near-term demand for Kratos’s microwave and satellite systems.

Still, NATO defense spending rose to about US$1.2 trillion in 2024, showing resilience as security priorities keep budgets more stable than civilian sectors.

- Global GDP growth 2024 ~3.1%

- NATO/allied share ≈70% of Kratos market

- NATO defense spend ~US$1.2tn in 2024

- Downturns risk deferred nonessential orders

Currency Exchange Volatility

As Kratos expands internationally, U.S. dollar strength can erode export competitiveness; the dollar rose ~6% vs. a trade-weighted basket in 2024, raising foreign prices for defense electronics and space systems.

A strong dollar contributed to slower international wins in FY2024, prompting use of hedging—Kratos reported FX forward exposure hedged for ~40% of near-term receivables—and increased local production in key markets.

- Dollar +6% (2024 trade-weighted)

- ~40% of near-term receivables hedged

- Localized manufacturing expanded to mitigate FX

Rising rates, supply inflation squeeze Kratos margins; NATO demand cushions growth

Higher rates (US 10y ~4.0% avg 2025) raised Kratos’s borrowing costs on ~$300m debt, compressing EBITDA; supply-chain inflation (composites +12–18%, semiconductors +9% 2023–24) increased unit costs, prompting $45–60m procurement cuts; labor scarcity (aerospace median ~$122k, cyber ~$103k in 2023) lifted wages; NATO spend ~US$1.2tn (2024) supports demand despite GDP growth ~3.1% (2024).

| Metric | Value |

|---|---|

| US 10y (2025 avg) | ~4.0% |

| Long-term debt | ~$300m |

| Composites price rise (2023–24) | 12–18% |

| Semiconductor price rise | 9% |

| Procurement savings FY2024 | $45–60m |

| Aerospace median wage (2023) | $122,270 |

| Cyber median wage (2023) | $103,590 |

| Global GDP growth (2024) | ~3.1% |

| NATO defense spend (2024) | ~$1.2tn |

What You See Is What You Get

Kratos PESTLE Analysis

The preview shown here is the exact Kratos PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for Kratos maps the political, economic, social, technological, legal, and environmental forces shaping its defense and aerospace trajectory—helping you anticipate risks and spot growth levers; download the full report for actionable insights and ready-to-use slides.

Political factors

Defense Budget Allocations

As of late 2025, Kratos’ revenue outlook is tied to DoD budget cycles, with the FY2025 defense budget at about $858 billion and unmanned systems funding rising—estimated $4–6 billion annually for attritable/loyal wingman programs—supporting Kratos’ drone pipeline.

Geopolitical Tensions

Increased friction in the Indo-Pacific and Eastern Europe has boosted demand for Kratos’s high-performance target drones and tactical UAVs, contributing to a 2024 defense order book up 18% year-over-year and revenue growth to $401 million in FY2024.

Political instability and rising defense budgets among NATO and Indo-Pacific allies—global defense spending reached $2.4 trillion in 2024—drive purchases of Kratos’s cost-effective solutions to counter peer adversaries.

Kratos’s alignment with U.S. and allied national security priorities, evidenced by multi-year contracts with the DoD and allied procurement programs, positions it as a key player in high-stakes geopolitical environments.

Export Control Policies

The US export control regime, including ITAR and recent 2024 restrictions on satellite and drone tech, directly influences Kratos’s FY2025 international revenue potential—35% of defense sector sales could be constrained if controls tighten. A 2023 uptick in allied procurement offers offsetting demand, but diplomatic shifts (e.g., US-EU/Indo-Pacific ties) can rapidly open or close markets.

Bipartisan Support for Defense Innovation

The US Congress and Pentagon have increased funding for rapid defense tech: 2025 budget boosts prototyping and innovation accounts by roughly $6.6B, benefitting non-traditional contractors like Kratos that emphasize UAVs, autonomy, and microwave electronics.

Policy shifts favor Other Transaction Authorities and OTA-like pathways, shortening procurement cycles and enabling Kratos to accelerate demonstration-to-deployment timelines for autonomous systems.

Government Contract Procurement Shifts

Political pressure to reduce the US deficit—federal budget deficit was about $1.7 trillion in FY2024—favors lower-cost, high-attrition systems over multi-decade platforms, benefiting Kratos which emphasizes affordable, rapidly manufactured unmanned systems and earned $612m revenue in FY2024.

Kratos’ cost-focused model and flexible production lines position it to capture shifting procurement; however, changes in administration or congressional priorities could reallocate defense budgets away from drones and missile systems, impacting specific business units.

- FY2024 US federal deficit ~$1.7T

- Kratos FY2024 revenue $612M

- Shift favors low-cost/high-attrition systems

- Political leadership changes risk reallocating defense spend

Kratos rides defense spending and R&D tailwinds—export controls cloud international upside

Kratos benefits from rising DoD and allied defense spend (US FY2025 ~$858B; global defense $2.4T in 2024), OTA/prototyping boosts (+$6.6B RDT&E 2025) and demand for low-cost attritable UAVs (Kratos FY2024 revenue $612M), but export controls (ITAR/2024 drone limits) and political shifts/congressional priorities pose downside risk to international sales.

| Metric | Value |

|---|---|

| US FY2025 defense | $858B |

| Global defense 2024 | $2.4T |

| RDT&E boost 2025 | +$6.6B |

| Kratos FY2024 rev | $612M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Kratos across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

A concise, visually segmented Kratos PESTLE summary that’s easily dropped into presentations or shared across teams to streamline external risk discussions and align strategic planning.

Economic factors

Interest Rate Environment

By end-2025, Kratos faces a cost of capital sensitive to Fed-driven rates; the US 10-year yield rose to ~4.2% in 2024 and averaged ~4.0% in 2025, lifting borrowing costs and increasing annual interest expense on Kratos’s ~$300m long-term debt, squeezing EBITDA margins.

Higher rates raise servicing costs and can reduce free cash flow available for R&D and defense program investment, while a stabilizing rate trajectory would improve predictability for multi-year capital spending on manufacturing and infrastructure.

Supply Chain Inflation

Supply chain inflation—driven by a 12–18% rise (2023–2024) in prices for specialized composites and a 9% increase in semiconductors—raised Kratos’ unit production costs, prompting FY2024 cost-control programs that reduced procurement spend by an estimated $45–60 million and renegotiated multi-year supplier contracts to cap input-price exposure; managing these pressures is critical to keep unmanned systems price-competitive amid aerospace inflation outpacing CPI.

Labor Market Dynamics

The scarcity of aerospace engineers and cybersecurity experts raises labor costs; US median annual wage for aerospace engineers was about $122,270 in 2023 and cybersecurity roles saw median salaries near $103,590, pushing Kratos to offer premium compensation to compete. Competitive packages, including equity and training, are essential to retain talent for complex systems. Tech-sector hiring slowdowns in 2024–25 could ease pressure, while renewed defense spending may intensify it.

Global Defense Spending Trends

Global GDP growth slowed to an estimated 3.1% in 2024, pressuring defense spend in some NATO and allied states that collectively account for roughly 70% of Kratos’s defense market.

Economic downturns can delay noncritical procurements—2023 saw several allied maintenance contracts deferred—potentially reducing near-term demand for Kratos’s microwave and satellite systems.

Still, NATO defense spending rose to about US$1.2 trillion in 2024, showing resilience as security priorities keep budgets more stable than civilian sectors.

- Global GDP growth 2024 ~3.1%

- NATO/allied share ≈70% of Kratos market

- NATO defense spend ~US$1.2tn in 2024

- Downturns risk deferred nonessential orders

Currency Exchange Volatility

As Kratos expands internationally, U.S. dollar strength can erode export competitiveness; the dollar rose ~6% vs. a trade-weighted basket in 2024, raising foreign prices for defense electronics and space systems.

A strong dollar contributed to slower international wins in FY2024, prompting use of hedging—Kratos reported FX forward exposure hedged for ~40% of near-term receivables—and increased local production in key markets.

- Dollar +6% (2024 trade-weighted)

- ~40% of near-term receivables hedged

- Localized manufacturing expanded to mitigate FX

Rising rates, supply inflation squeeze Kratos margins; NATO demand cushions growth

Higher rates (US 10y ~4.0% avg 2025) raised Kratos’s borrowing costs on ~$300m debt, compressing EBITDA; supply-chain inflation (composites +12–18%, semiconductors +9% 2023–24) increased unit costs, prompting $45–60m procurement cuts; labor scarcity (aerospace median ~$122k, cyber ~$103k in 2023) lifted wages; NATO spend ~US$1.2tn (2024) supports demand despite GDP growth ~3.1% (2024).

| Metric | Value |

|---|---|

| US 10y (2025 avg) | ~4.0% |

| Long-term debt | ~$300m |

| Composites price rise (2023–24) | 12–18% |

| Semiconductor price rise | 9% |

| Procurement savings FY2024 | $45–60m |

| Aerospace median wage (2023) | $122,270 |

| Cyber median wage (2023) | $103,590 |

| Global GDP growth (2024) | ~3.1% |

| NATO defense spend (2024) | ~$1.2tn |

What You See Is What You Get

Kratos PESTLE Analysis

The preview shown here is the exact Kratos PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.