Kreate Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

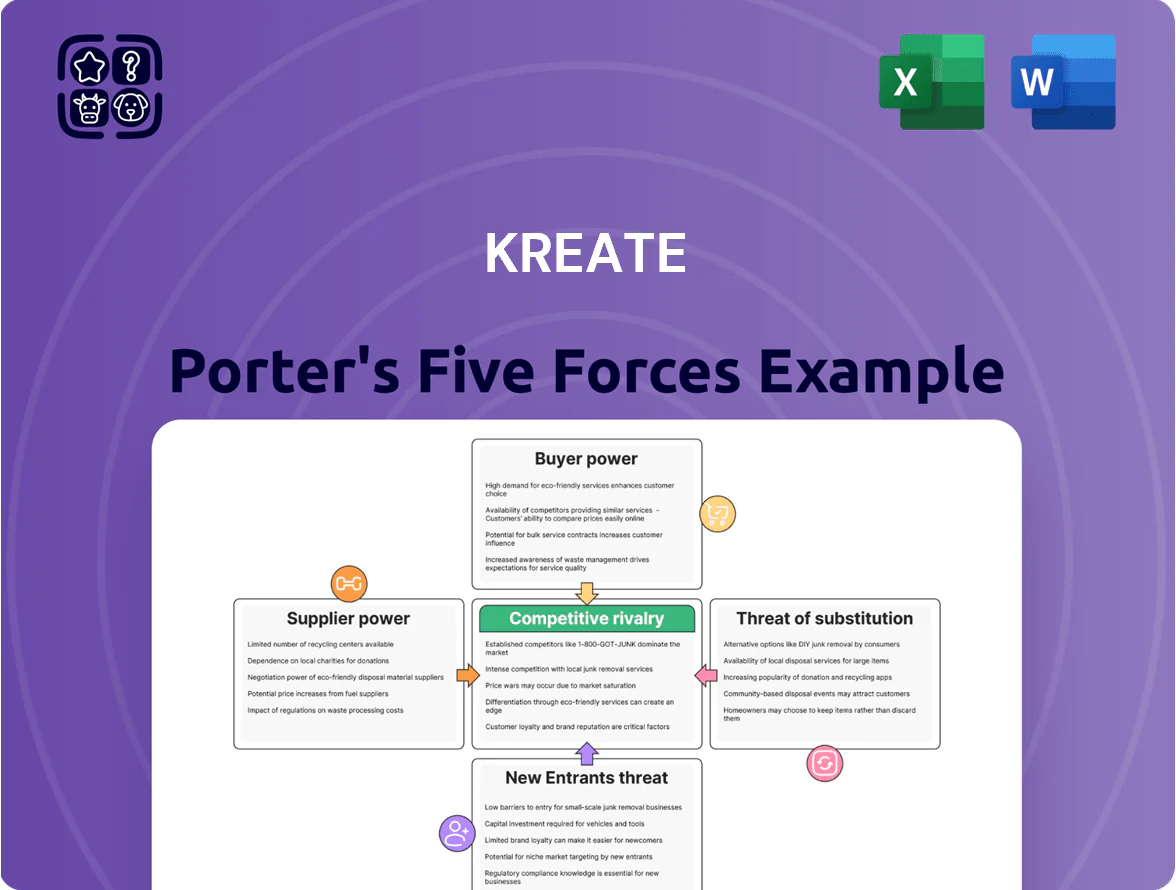

Kreate faces moderate competitive rivalry with niche differentiation in product design and a growing threat from low-cost entrants and substitutes as digital tools lower switching costs for customers.

Supplier power is contained by diversified sourcing, while buyer power is rising as enterprise clients demand customization and lower prices—pressures that could compress margins without strategic action.

This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for Kreate’s strategy and investment decisions.

Suppliers Bargaining Power

Raw material price volatility

The construction sector relies on steel, cement, and bitumen tied to global commodity markets, and Kreate faces risk from price swings—steel rose 18% in 2023–24 and global bitumen surged 12% in 2024, which can erode margins on fixed-price contracts signed months earlier.

By late 2025 supply chains largely stabilized, cutting average lead-time variability from 40% in 2022 to ~12%, but Kreate now pays a premium for green materials: recycled steel and low-carbon cement cost 8–20% more from specialized suppliers, adding fresh cost pressure.

Specialized subcontractor reliance

For highly technical projects like bridge or tunnel construction, Kreate depends on niche subcontractors with specialist gear and certifications, giving these suppliers strong leverage since fewer than 10 Finnish firms meet required engineering standards for large-scale civil works (2024 industry registry); long-term contracts and preferred-supplier agreements cut risk, secure capacity during peak summer months when demand spikes ~25%, and help control subcontractor-driven cost premiums that can add 8–12% to project budgets.

Energy and logistics costs

Suppliers of transport and heavy machinery tie prices to diesel and electricity; a 40% rise in EU diesel costs in 2022–24 pushed average haulage rates up ~22%, directly raising Kreate’s unit OPEX.

Northern Europe tightened carbon pricing to €80/ton CO2 by Jan 2025, and logistics firms now itemize CO2 levies—Kreate faces ~1.5–3.0% higher logistics bills on typical projects.

Kreate’s negotiating power hinges on scale and schedule efficiency; contractors with >€50m annual spend get discounts ~5–8%, and tighter scheduling can cut idle machinery costs by 12%.

Machinery and technology providers

The shift to automated and electric construction machinery concentrates supplier power among a few global OEMs (Caterpillar, Komatsu, Volvo CE), who control key EV powertrains and autonomy stacks; global construction equipment EV sales rose ~18% in 2024, reinforcing supplier leverage.

Kreate depends on firmware, telematics, and software updates to meet project specs, creating vendor lock-in and service-contract revenue for suppliers; average fleet electrification retrofit costs range $80k–$200k per unit.

High switching costs for battery packs, charging infrastructure, and integration (5–7 year payback on capex) further strengthen supplier bargaining power and raise Kreate’s procurement risk.

- Few dominant OEMs control EV/autonomy tech

- 2024 EV equipment sales +18%, boosting supplier leverage

- Retrofit cost $80k–$200k per unit = high switching costs

- 5–7 year capex payback increases vendor lock-in

Skilled labor availability

The supply of specialized labor in Finland—civil engineers and heavy machinery operators—is tight, with unemployment for construction engineers at 1.9% in 2024 and vacancies up 18% year-on-year, boosting worker leverage.

Strong unions and niche recruiters extract premium rates; average hourly wages for site specialists rose 6.5% in 2024, increasing project OPEX and schedule risk.

Kreate must invest in employer branding, apprenticeships, and a 12–24 month training pipeline to reduce dependency and ensure continuity.

- 1.9% unemployment (construction engineers, 2024)

- +18% vacancies YoY (2024)

- +6.5% specialist wage growth (2024)

- 12–24 month training payback

Kreate squeezed: rising commodity, green premiums & tight labor drive margin pressure

Kreate faces strong supplier power: commodity swings (steel +18% 2023–24, bitumen +12% 2024) and premium green inputs (+8–20%) squeeze margins; niche subcontractors (<10 Finnish firms for major civil works) and OEMs (Caterpillar, Komatsu, Volvo CE) dominate EV/autonomy, raising switching costs (retrofit $80k–$200k; 5–7 yr payback). Tight labor (1.9% unemployment, vacancies +18% 2024) adds wage pressure (+6.5%).

| Metric | Value |

|---|---|

| Steel price change | +18% (2023–24) |

| Bitumen | +12% (2024) |

| Green premium | +8–20% |

| Retrofit cost | $80k–$200k/unit |

| Labor unemployment | 1.9% (2024) |

| Vacancies YoY | +18% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Kreate that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic positioning and pricing decisions.

A concise, one-sheet Porter's Five Forces dashboard that quantifies competitive pressures and lets teams quickly adjust inputs to model scenarios—ideal for fast, board-ready decision-making.

Customers Bargaining Power

Dominance of public sector entities

Formalized tendering frameworks

Public procurement laws force transparent competitive bidding, letting buyers pick lowest-cost or best-quality bids and reducing Kreate’s room for bespoke price talks.

This framework makes bid comparison easy: EU public tenders saw 22% lower average contract prices in 2023 versus private deals, constraining margin capture for suppliers like Kreate.

By 2025, 68% of large public buyers factor ESG criteria alongside price, so Kreate must compete on verified sustainability metrics, not just cost.

Project financing constraints

Private-sector clients in industrial and environmental construction are highly rate-sensitive; with global corporate loan spreads rising ~120 bps in 2024 and India's lending rate at 6.5% (Dec 2025) projects stall when financing tightens.

When credit costs rise, clients delay capex or demand extended payment terms from Kreate, reducing cash conversion and pressuring margins.

That leverage lets customers insist on cost-saving design tweaks or risk-sharing contracts; 28% of EPC contracts in 2024 included shared-risk clauses.

Service quality and safety expectations

Customers in infrastructure demand zero tolerance for safety failures and top-tier engineering to ensure assets exceed planned life; global infrastructure clients reported 23% of contracts in 2024 included strict liquidated damages clauses for safety or quality breaches.

Those clauses shift operational risk to Kreate, letting clients levy heavy penalties—industry median penalty rates hit 0.8% of contract value per week of delay in 2024—compressing margins.

A single failed project cuts future win probability by 30% for suppliers, so reputational risk gives customers strong psychological leverage in pricing and contract terms.

- Zero-tolerance safety: standard in 90%+ of large infra contracts (2024)

- Median liquidated damages: 0.8% contract value/week (2024)

- Reputational hit: ~30% lower rebid win-rate after failures

Contractual penalty clauses

- LDs avg 0.05–0.2%/day

- $100m project: $50k–$200k/day

- 10-day delay @0.1% = $10m loss

- ~35% contracts tie LDs to ESG targets (2025)

Public buyers squeeze margins: low-price tenders, strict LDs and ESG-driven risk shift

| Metric | Value |

|---|---|

| Public revenue share | 60–70% |

| Adj. OPM (2024) | 4.8% |

| LDs median | 0.8%/week |

| Buyers using ESG (2025) | 68% |

| Contracts tying LDs to ESG | 35% |

Same Document Delivered

Kreate Porter's Five Forces Analysis

This preview shows the exact Kreate Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Kreate faces moderate competitive rivalry with niche differentiation in product design and a growing threat from low-cost entrants and substitutes as digital tools lower switching costs for customers.

Supplier power is contained by diversified sourcing, while buyer power is rising as enterprise clients demand customization and lower prices—pressures that could compress margins without strategic action.

This preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for Kreate’s strategy and investment decisions.

Suppliers Bargaining Power

Raw material price volatility

The construction sector relies on steel, cement, and bitumen tied to global commodity markets, and Kreate faces risk from price swings—steel rose 18% in 2023–24 and global bitumen surged 12% in 2024, which can erode margins on fixed-price contracts signed months earlier.

By late 2025 supply chains largely stabilized, cutting average lead-time variability from 40% in 2022 to ~12%, but Kreate now pays a premium for green materials: recycled steel and low-carbon cement cost 8–20% more from specialized suppliers, adding fresh cost pressure.

Specialized subcontractor reliance

For highly technical projects like bridge or tunnel construction, Kreate depends on niche subcontractors with specialist gear and certifications, giving these suppliers strong leverage since fewer than 10 Finnish firms meet required engineering standards for large-scale civil works (2024 industry registry); long-term contracts and preferred-supplier agreements cut risk, secure capacity during peak summer months when demand spikes ~25%, and help control subcontractor-driven cost premiums that can add 8–12% to project budgets.

Energy and logistics costs

Suppliers of transport and heavy machinery tie prices to diesel and electricity; a 40% rise in EU diesel costs in 2022–24 pushed average haulage rates up ~22%, directly raising Kreate’s unit OPEX.

Northern Europe tightened carbon pricing to €80/ton CO2 by Jan 2025, and logistics firms now itemize CO2 levies—Kreate faces ~1.5–3.0% higher logistics bills on typical projects.

Kreate’s negotiating power hinges on scale and schedule efficiency; contractors with >€50m annual spend get discounts ~5–8%, and tighter scheduling can cut idle machinery costs by 12%.

Machinery and technology providers

The shift to automated and electric construction machinery concentrates supplier power among a few global OEMs (Caterpillar, Komatsu, Volvo CE), who control key EV powertrains and autonomy stacks; global construction equipment EV sales rose ~18% in 2024, reinforcing supplier leverage.

Kreate depends on firmware, telematics, and software updates to meet project specs, creating vendor lock-in and service-contract revenue for suppliers; average fleet electrification retrofit costs range $80k–$200k per unit.

High switching costs for battery packs, charging infrastructure, and integration (5–7 year payback on capex) further strengthen supplier bargaining power and raise Kreate’s procurement risk.

- Few dominant OEMs control EV/autonomy tech

- 2024 EV equipment sales +18%, boosting supplier leverage

- Retrofit cost $80k–$200k per unit = high switching costs

- 5–7 year capex payback increases vendor lock-in

Skilled labor availability

The supply of specialized labor in Finland—civil engineers and heavy machinery operators—is tight, with unemployment for construction engineers at 1.9% in 2024 and vacancies up 18% year-on-year, boosting worker leverage.

Strong unions and niche recruiters extract premium rates; average hourly wages for site specialists rose 6.5% in 2024, increasing project OPEX and schedule risk.

Kreate must invest in employer branding, apprenticeships, and a 12–24 month training pipeline to reduce dependency and ensure continuity.

- 1.9% unemployment (construction engineers, 2024)

- +18% vacancies YoY (2024)

- +6.5% specialist wage growth (2024)

- 12–24 month training payback

Kreate squeezed: rising commodity, green premiums & tight labor drive margin pressure

Kreate faces strong supplier power: commodity swings (steel +18% 2023–24, bitumen +12% 2024) and premium green inputs (+8–20%) squeeze margins; niche subcontractors (<10 Finnish firms for major civil works) and OEMs (Caterpillar, Komatsu, Volvo CE) dominate EV/autonomy, raising switching costs (retrofit $80k–$200k; 5–7 yr payback). Tight labor (1.9% unemployment, vacancies +18% 2024) adds wage pressure (+6.5%).

| Metric | Value |

|---|---|

| Steel price change | +18% (2023–24) |

| Bitumen | +12% (2024) |

| Green premium | +8–20% |

| Retrofit cost | $80k–$200k/unit |

| Labor unemployment | 1.9% (2024) |

| Vacancies YoY | +18% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Kreate that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to inform strategic positioning and pricing decisions.

A concise, one-sheet Porter's Five Forces dashboard that quantifies competitive pressures and lets teams quickly adjust inputs to model scenarios—ideal for fast, board-ready decision-making.

Customers Bargaining Power

Dominance of public sector entities

Formalized tendering frameworks

Public procurement laws force transparent competitive bidding, letting buyers pick lowest-cost or best-quality bids and reducing Kreate’s room for bespoke price talks.

This framework makes bid comparison easy: EU public tenders saw 22% lower average contract prices in 2023 versus private deals, constraining margin capture for suppliers like Kreate.

By 2025, 68% of large public buyers factor ESG criteria alongside price, so Kreate must compete on verified sustainability metrics, not just cost.

Project financing constraints

Private-sector clients in industrial and environmental construction are highly rate-sensitive; with global corporate loan spreads rising ~120 bps in 2024 and India's lending rate at 6.5% (Dec 2025) projects stall when financing tightens.

When credit costs rise, clients delay capex or demand extended payment terms from Kreate, reducing cash conversion and pressuring margins.

That leverage lets customers insist on cost-saving design tweaks or risk-sharing contracts; 28% of EPC contracts in 2024 included shared-risk clauses.

Service quality and safety expectations

Customers in infrastructure demand zero tolerance for safety failures and top-tier engineering to ensure assets exceed planned life; global infrastructure clients reported 23% of contracts in 2024 included strict liquidated damages clauses for safety or quality breaches.

Those clauses shift operational risk to Kreate, letting clients levy heavy penalties—industry median penalty rates hit 0.8% of contract value per week of delay in 2024—compressing margins.

A single failed project cuts future win probability by 30% for suppliers, so reputational risk gives customers strong psychological leverage in pricing and contract terms.

- Zero-tolerance safety: standard in 90%+ of large infra contracts (2024)

- Median liquidated damages: 0.8% contract value/week (2024)

- Reputational hit: ~30% lower rebid win-rate after failures

Contractual penalty clauses

- LDs avg 0.05–0.2%/day

- $100m project: $50k–$200k/day

- 10-day delay @0.1% = $10m loss

- ~35% contracts tie LDs to ESG targets (2025)

Public buyers squeeze margins: low-price tenders, strict LDs and ESG-driven risk shift

| Metric | Value |

|---|---|

| Public revenue share | 60–70% |

| Adj. OPM (2024) | 4.8% |

| LDs median | 0.8%/week |

| Buyers using ESG (2025) | 68% |

| Contracts tying LDs to ESG | 35% |

Same Document Delivered

Kreate Porter's Five Forces Analysis

This preview shows the exact Kreate Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.