King & Spalding PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

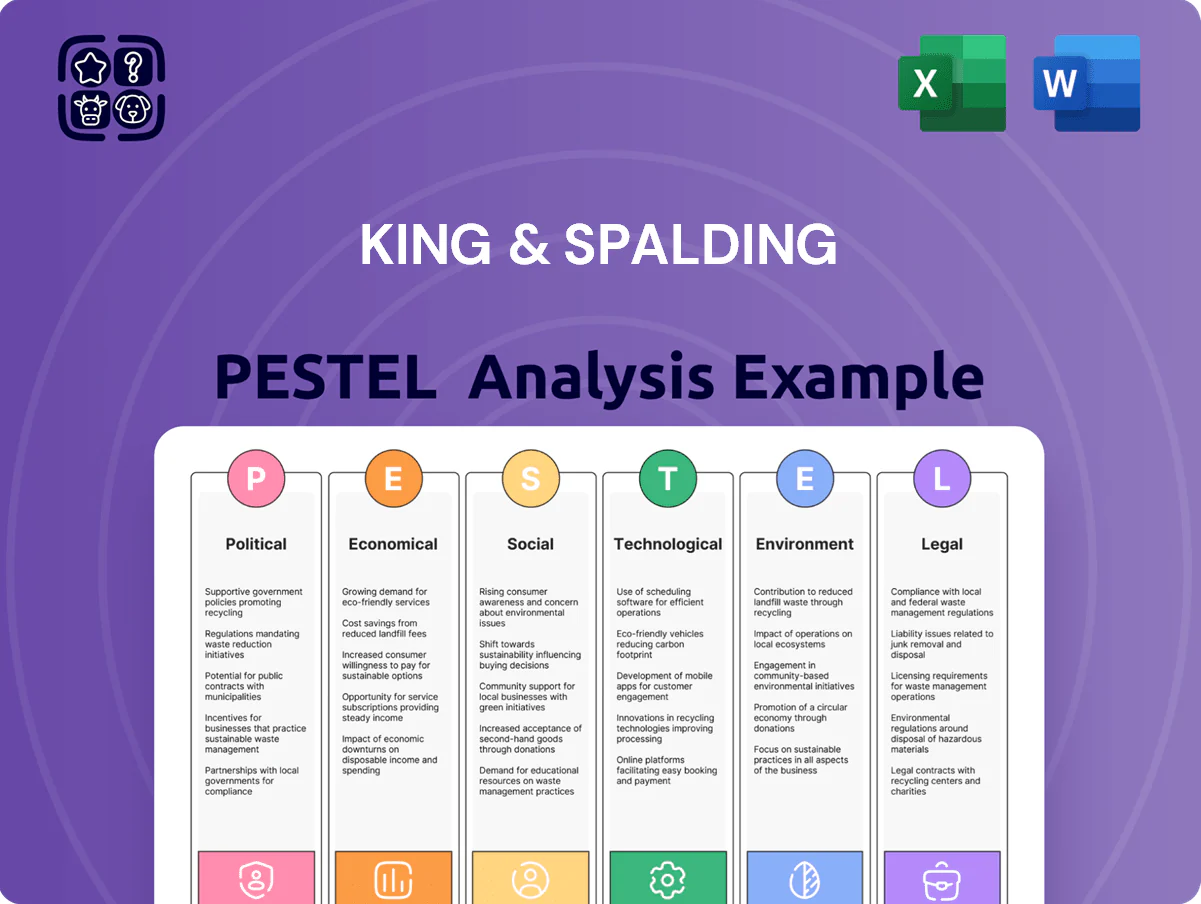

Gain a competitive edge with our targeted PESTLE Analysis of King & Spalding—unpack the political, economic, social, technological, legal, and environmental forces shaping the firm’s strategy and risks; buy the full report for a ready-to-use, editable deep-dive that accelerates your research, pitches, or investment decisions.

Political factors

US Post-Election Policy Shifts

The 2024 US election results continue to reshape the 2025 regulatory landscape, increasing demand for King & Spalding’s government relations practice as federal rulemakings rose 12% year-over-year through Q1 2025. Changes in federal agency leadership have reprioritized enforcement in energy and healthcare, with EPA and HHS issuing 18 major guidance documents combined in 2024–25. The firm must rapidly adjust to these shifts to provide accurate strategic counsel to corporate clients navigating heightened compliance risk.

Middle East Geopolitical Expansion

King & Spalding's strong foothold in Riyadh and Dubai aligns with Gulf economic diversification programs—Saudi Vision 2030 and UAE's Axiom plans—driving a 14% CAGR in GCC FDI inflows (2019–2024) and raising demand for advisory on energy transition and infrastructure projects.

Regional political stability and diplomatic ties shape cross-border investment volumes; GCC cross-border M&A value fell 28% in 2023 amid tensions but recovered partially to $42bn in 2024, affecting the firm's deal pipeline.

The firm leverages deep local networks and on‑the‑ground teams to mitigate geopolitical risk, enabling continuity in client mandates across sanctions, regulatory shifts, and supply‑chain disruptions in the Middle East.

International Trade Sanctions

Ongoing global conflicts have produced over 4,000 active sanctions measures worldwide as of 2025, creating a complex compliance landscape that King & Spalding must monitor continuously.

The firm advises multinationals on evolving export controls and economic restrictions, reflecting a 22% year-on-year rise in demand for trade-compliance counsel reported across big law firms in 2024.

This political climate drives strong demand for King & Spalding’s international trade and disputes practices, contributing to cross-border engagement growth and higher billing for sanctions-related matters.

Government Relations and Lobbying

As a major Washington D.C. player, King & Spalding leverages lobbying as a strategic asset, reporting 2024 federal lobbying expenditures industry-wide up ~9% to $4.1 billion, with the firm advising clients on tech policy and CHIPS Act-related incentives worth $52 billion in authorized funding.

Clients depend on the firm to translate legislative shifts into corporate strategy, notably around AI regulation and manufacturing tax credits, with advisory engagements growing an estimated 12% in 2024.

- 2024 federal lobbying market ~ $4.1B, +9%

- CHIPS Act funding authorized ~$52B

- Firm advisory engagements on emerging tech up ~12% (2024)

- Focus: AI regulation, domestic manufacturing incentives

Global Regulatory Divergence

The growing divide between Western and Eastern regulatory frameworks complicates cross-border operations, with 68% of multinational firms reporting increased compliance costs in 2024 due to divergent data, trade, and sanctions regimes.

King & Spalding helps clients reconcile conflicting political mandates across jurisdictions, leveraging local counsel networks and having handled 120+ cross-border disputes and regulatory matters in 2023–2025.

Ensuring global operational continuity requires nuanced reading of local political climates, using jurisdictional risk scoring and scenario planning to limit supply-chain and licensing disruptions.

- 68% of multinationals saw higher compliance costs (2024)

- King & Spalding: 120+ cross-border matters (2023–2025)

- Focus: jurisdictional risk scoring and scenario planning

King & Spalding surges in sanctions, compliance and GCC cross‑border work amid regulatory spike

Political shifts since 2024 elevated King & Spalding’s regulatory and sanctions work—federal rulemakings +12% Y/Y (Q1 2025), global sanctions >4,000 measures (2025), GCC FDI CAGR 14% (2019–24) with 2024 M&A $42bn, and multinationals reporting 68% higher compliance costs (2024); firm handled 120+ cross-border matters (2023–25).

| Metric | Value |

|---|---|

| Federal rulemakings | +12% Y/Y |

| Global sanctions | >4,000 (2025) |

| GCC FDI CAGR | 14% (2019–24) |

| GCC M&A 2024 | $42bn |

| Higher compliance costs | 68% (2024) |

| Cross-border matters | 120+ (2023–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect King & Spalding across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, forward-looking insights, and detailed sub-points tailored for executives, consultants, and investors to identify risks and opportunities and inform strategy, reporting, and funding decisions.

A concise, visually segmented King & Spalding PESTLE summary that’s easy to drop into presentations or share across teams, helping streamline external risk discussions and strategic planning.

Economic factors

M&A Market Stabilization

By end-2025 global M&A value recovered to about $2.5 trillion, up roughly 18% year-over-year, restoring deal confidence after 2022–23 volatility.

King & Spalding benefits as corporate cash holdings near $5.5 trillion and private equity dry powder exceeded $1.7 trillion in 2025, driving higher deal flow.

The firm’s expertise in structuring multi-billion-dollar cross-border deals positions it to capture increased demand for complex transaction legal architecture in a stabilizing market.

Inflation and Billable Rates

Persistent inflation pushed US CPI to 3.4% in 2024, prompting King & Spalding to raise rates and tighten billable-hour targets; firms saw average associate salary increases near 6–8% in 2024, pressuring margins.

Balancing higher compensation against client sensitivity—legal spend growth slowed to ~1%–2% in 2024—has driven uptake of alternative fee arrangements, which accounted for an estimated 20%–30% of engagements to protect profitability.

Energy Transition Financing

King & Spalding’s project finance teams capture a share of the estimated $1.3 trillion yearly global clean energy investment (IEA 2024), advising on hydrogen, solar and wind deals where project costs range $500M–$3B; the firm markets itself as a leader in structuring offtake, tax equity and M&A for green hydrogen (projected $700B cumulative investment by 2030, BloombergNEF 2025) and utility-scale solar/wind, a sector showing resilient revenue growth despite macro volatility.

Global Interest Rate Volatility

Fluctuations in central bank policies—with global rates rising to averages of ~3.5% in 2024 from near zero post-2021—raise borrowing costs and reshape debt structuring, affecting cross-border financings handled by King & Spalding.

The firm’s finance practice adapts by advising on interest rate swaps, floating-to-fixed conversions and covenant design to optimize client capital structures amid rate volatility.

Heightened economic uncertainty has driven a 2023–2024 uptick in restructuring demand; global corporate insolvencies rose ~12% in 2024, increasing need for insolvency and turnaround services.

- Rising global rates (~3.5% avg in 2024) increase cost of capital

- Greater use of hedging and covenant negotiation in financings

- ~12% rise in corporate insolvencies (2023–24) boosts restructuring demand

Emerging Market Growth

Economic expansion in Southeast Asia (2024 GDP growth: 4.7% for ASEAN) and sub-Saharan Africa (2024 GDP growth: ~3.8 IMF estimate) creates demand for cross-border legal services; King & Spalding targets these regions to diversify beyond US/EU revenues.

Success hinges on managing local risks: commodity-linked volatility, political instability, and 2024 FX swings (e.g., NGN -12% vs USD, IDR -4% in 2024) that can compress fee margins.

- ASEAN 2024 GDP growth ~4.7%

- Sub-Saharan Africa 2024 GDP ~3.8%

- 2024 notable FX moves: NGN -12%, IDR -4%

- Diversification reduces dependence on US/EU markets

M&A rebounds to $2.5T as $1.7T+ PE dry powder and $5.5T cash fuel deals amid rising costs

Global M&A rebounded to ~$2.5T by end-2025, PE dry powder >$1.7T and corporate cash ~ $5.5T, lifting transactional demand; US CPI 3.4% in 2024 and avg rates ~3.5% raised costs, driving AFAs (~20–30%) and hedging use; restructuring needs rose with insolvencies +12% (2023–24); ASEAN GDP 2024 ~4.7%, Sub‑Saharan Africa ~3.8%, offering regional diversification but FX volatility risks.

| Metric | Value |

|---|---|

| Global M&A (end-2025) | $2.5T |

| PE dry powder (2025) | $1.7T+ |

| Corporate cash (2025) | $5.5T |

| US CPI (2024) | 3.4% |

| Avg rates (2024) | ~3.5% |

| Insolvencies (2023–24) | +12% |

| ASEAN GDP (2024) | 4.7% |

| Sub‑Saharan Africa GDP (2024) | 3.8% |

What You See Is What You Get

King & Spalding PESTLE Analysis

The preview shown here is the exact King & Spalding PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of King & Spalding—unpack the political, economic, social, technological, legal, and environmental forces shaping the firm’s strategy and risks; buy the full report for a ready-to-use, editable deep-dive that accelerates your research, pitches, or investment decisions.

Political factors

US Post-Election Policy Shifts

The 2024 US election results continue to reshape the 2025 regulatory landscape, increasing demand for King & Spalding’s government relations practice as federal rulemakings rose 12% year-over-year through Q1 2025. Changes in federal agency leadership have reprioritized enforcement in energy and healthcare, with EPA and HHS issuing 18 major guidance documents combined in 2024–25. The firm must rapidly adjust to these shifts to provide accurate strategic counsel to corporate clients navigating heightened compliance risk.

Middle East Geopolitical Expansion

King & Spalding's strong foothold in Riyadh and Dubai aligns with Gulf economic diversification programs—Saudi Vision 2030 and UAE's Axiom plans—driving a 14% CAGR in GCC FDI inflows (2019–2024) and raising demand for advisory on energy transition and infrastructure projects.

Regional political stability and diplomatic ties shape cross-border investment volumes; GCC cross-border M&A value fell 28% in 2023 amid tensions but recovered partially to $42bn in 2024, affecting the firm's deal pipeline.

The firm leverages deep local networks and on‑the‑ground teams to mitigate geopolitical risk, enabling continuity in client mandates across sanctions, regulatory shifts, and supply‑chain disruptions in the Middle East.

International Trade Sanctions

Ongoing global conflicts have produced over 4,000 active sanctions measures worldwide as of 2025, creating a complex compliance landscape that King & Spalding must monitor continuously.

The firm advises multinationals on evolving export controls and economic restrictions, reflecting a 22% year-on-year rise in demand for trade-compliance counsel reported across big law firms in 2024.

This political climate drives strong demand for King & Spalding’s international trade and disputes practices, contributing to cross-border engagement growth and higher billing for sanctions-related matters.

Government Relations and Lobbying

As a major Washington D.C. player, King & Spalding leverages lobbying as a strategic asset, reporting 2024 federal lobbying expenditures industry-wide up ~9% to $4.1 billion, with the firm advising clients on tech policy and CHIPS Act-related incentives worth $52 billion in authorized funding.

Clients depend on the firm to translate legislative shifts into corporate strategy, notably around AI regulation and manufacturing tax credits, with advisory engagements growing an estimated 12% in 2024.

- 2024 federal lobbying market ~ $4.1B, +9%

- CHIPS Act funding authorized ~$52B

- Firm advisory engagements on emerging tech up ~12% (2024)

- Focus: AI regulation, domestic manufacturing incentives

Global Regulatory Divergence

The growing divide between Western and Eastern regulatory frameworks complicates cross-border operations, with 68% of multinational firms reporting increased compliance costs in 2024 due to divergent data, trade, and sanctions regimes.

King & Spalding helps clients reconcile conflicting political mandates across jurisdictions, leveraging local counsel networks and having handled 120+ cross-border disputes and regulatory matters in 2023–2025.

Ensuring global operational continuity requires nuanced reading of local political climates, using jurisdictional risk scoring and scenario planning to limit supply-chain and licensing disruptions.

- 68% of multinationals saw higher compliance costs (2024)

- King & Spalding: 120+ cross-border matters (2023–2025)

- Focus: jurisdictional risk scoring and scenario planning

King & Spalding surges in sanctions, compliance and GCC cross‑border work amid regulatory spike

Political shifts since 2024 elevated King & Spalding’s regulatory and sanctions work—federal rulemakings +12% Y/Y (Q1 2025), global sanctions >4,000 measures (2025), GCC FDI CAGR 14% (2019–24) with 2024 M&A $42bn, and multinationals reporting 68% higher compliance costs (2024); firm handled 120+ cross-border matters (2023–25).

| Metric | Value |

|---|---|

| Federal rulemakings | +12% Y/Y |

| Global sanctions | >4,000 (2025) |

| GCC FDI CAGR | 14% (2019–24) |

| GCC M&A 2024 | $42bn |

| Higher compliance costs | 68% (2024) |

| Cross-border matters | 120+ (2023–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect King & Spalding across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, forward-looking insights, and detailed sub-points tailored for executives, consultants, and investors to identify risks and opportunities and inform strategy, reporting, and funding decisions.

A concise, visually segmented King & Spalding PESTLE summary that’s easy to drop into presentations or share across teams, helping streamline external risk discussions and strategic planning.

Economic factors

M&A Market Stabilization

By end-2025 global M&A value recovered to about $2.5 trillion, up roughly 18% year-over-year, restoring deal confidence after 2022–23 volatility.

King & Spalding benefits as corporate cash holdings near $5.5 trillion and private equity dry powder exceeded $1.7 trillion in 2025, driving higher deal flow.

The firm’s expertise in structuring multi-billion-dollar cross-border deals positions it to capture increased demand for complex transaction legal architecture in a stabilizing market.

Inflation and Billable Rates

Persistent inflation pushed US CPI to 3.4% in 2024, prompting King & Spalding to raise rates and tighten billable-hour targets; firms saw average associate salary increases near 6–8% in 2024, pressuring margins.

Balancing higher compensation against client sensitivity—legal spend growth slowed to ~1%–2% in 2024—has driven uptake of alternative fee arrangements, which accounted for an estimated 20%–30% of engagements to protect profitability.

Energy Transition Financing

King & Spalding’s project finance teams capture a share of the estimated $1.3 trillion yearly global clean energy investment (IEA 2024), advising on hydrogen, solar and wind deals where project costs range $500M–$3B; the firm markets itself as a leader in structuring offtake, tax equity and M&A for green hydrogen (projected $700B cumulative investment by 2030, BloombergNEF 2025) and utility-scale solar/wind, a sector showing resilient revenue growth despite macro volatility.

Global Interest Rate Volatility

Fluctuations in central bank policies—with global rates rising to averages of ~3.5% in 2024 from near zero post-2021—raise borrowing costs and reshape debt structuring, affecting cross-border financings handled by King & Spalding.

The firm’s finance practice adapts by advising on interest rate swaps, floating-to-fixed conversions and covenant design to optimize client capital structures amid rate volatility.

Heightened economic uncertainty has driven a 2023–2024 uptick in restructuring demand; global corporate insolvencies rose ~12% in 2024, increasing need for insolvency and turnaround services.

- Rising global rates (~3.5% avg in 2024) increase cost of capital

- Greater use of hedging and covenant negotiation in financings

- ~12% rise in corporate insolvencies (2023–24) boosts restructuring demand

Emerging Market Growth

Economic expansion in Southeast Asia (2024 GDP growth: 4.7% for ASEAN) and sub-Saharan Africa (2024 GDP growth: ~3.8 IMF estimate) creates demand for cross-border legal services; King & Spalding targets these regions to diversify beyond US/EU revenues.

Success hinges on managing local risks: commodity-linked volatility, political instability, and 2024 FX swings (e.g., NGN -12% vs USD, IDR -4% in 2024) that can compress fee margins.

- ASEAN 2024 GDP growth ~4.7%

- Sub-Saharan Africa 2024 GDP ~3.8%

- 2024 notable FX moves: NGN -12%, IDR -4%

- Diversification reduces dependence on US/EU markets

M&A rebounds to $2.5T as $1.7T+ PE dry powder and $5.5T cash fuel deals amid rising costs

Global M&A rebounded to ~$2.5T by end-2025, PE dry powder >$1.7T and corporate cash ~ $5.5T, lifting transactional demand; US CPI 3.4% in 2024 and avg rates ~3.5% raised costs, driving AFAs (~20–30%) and hedging use; restructuring needs rose with insolvencies +12% (2023–24); ASEAN GDP 2024 ~4.7%, Sub‑Saharan Africa ~3.8%, offering regional diversification but FX volatility risks.

| Metric | Value |

|---|---|

| Global M&A (end-2025) | $2.5T |

| PE dry powder (2025) | $1.7T+ |

| Corporate cash (2025) | $5.5T |

| US CPI (2024) | 3.4% |

| Avg rates (2024) | ~3.5% |

| Insolvencies (2023–24) | +12% |

| ASEAN GDP (2024) | 4.7% |

| Sub‑Saharan Africa GDP (2024) | 3.8% |

What You See Is What You Get

King & Spalding PESTLE Analysis

The preview shown here is the exact King & Spalding PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.