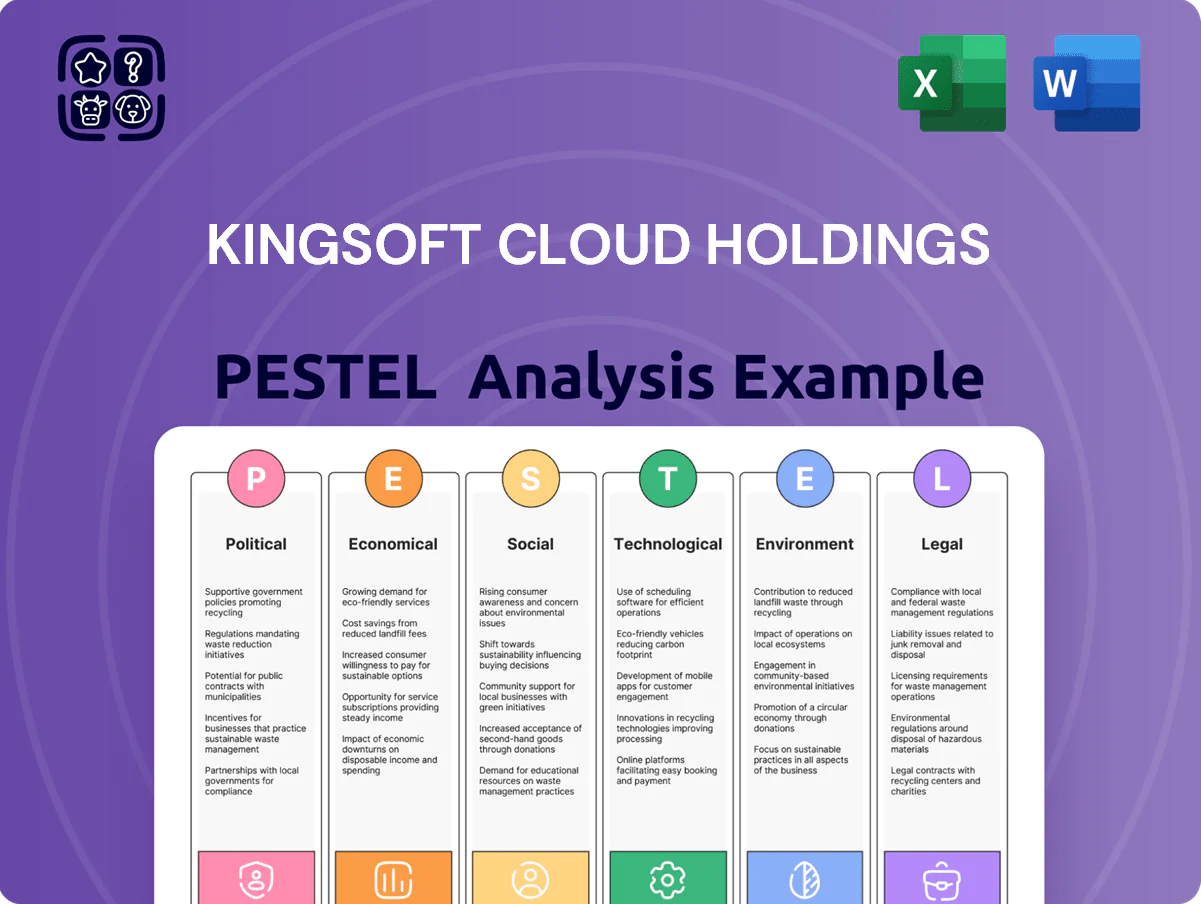

Kingsoft Cloud Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive advantage with our concise PESTLE Analysis of Kingsoft Cloud Holdings—highlighting political, economic, social, technological, legal, and environmental forces shaping its growth and risks; purchase the full report to access detailed, actionable insights and ready-to-use charts for investment decisions or strategic planning.

Political factors

Government Support for Digital Economy

The Chinese government lists the digital economy as a core growth pillar through 2025, targeting digital GDP to exceed 10 trillion yuan by 2025; Kingsoft Cloud benefits from policies subsidizing cloud migration and tax incentives that accelerate enterprise modernization.

This political alignment supports Kingsoft Cloud’s expansion into public services and SOE projects, where China’s public cloud spending grew ~28% year-on-year in 2024, boosting addressable demand.

Geopolitical Tensions and Supply Chain Risks

Persistent US-China trade tensions have constrained Kingsoft Cloud's access to high-end semiconductors, with US export controls since 2022 cutting off certain GPUs and contributing to a 12-18% premium on imported AI accelerators in 2024.

Restrictions on advanced GPUs—central to AI training and HPC—force Kingsoft Cloud to redesign procurement and risk management, as roughly 30-40% of its AI-capable fleet relied on Western chips in 2023.

These frictions drive a strategic pivot toward domestic hardware and collaborations with Chinese chipmakers to secure capacity and reduce supply-chain exposure, aiming to replace up to 60% of foreign-dependent units by 2026.

Data Sovereignty and National Security

Stringent data sovereignty laws force cloud firms to localize data and bolster security; China’s 2023 Personal Information Protection Law and Data Security Law, plus a 2024 draft critical data rules, raise compliance costs—Kingsoft Cloud reported Rmb5.1bn capex in 2024 investments in infrastructure and security. As an independent domestic provider it is favored by government and finance clients, but ongoing national security scrutiny increases audit frequency and legal risk.

State-Owned Enterprise Cloud Adoption

The political push for SOE cloud adoption in China has opened a large addressable market for Kingsoft Cloud, with government cloud procurement spending exceeding RMB 200 billion in 2024 and SOE digital budgets growing ~18% year-over-year.

By positioning as a secure, domestically controlled alternative to AWS/Alibaba, Kingsoft Cloud captured meaningful SOE deals contributing to its 2024 enterprise revenue growth of ~40% and narrowing gross margin gaps with larger peers.

Mandates to reduce dependence on foreign tech across critical infrastructure—reinforced by regulatory guidance in 2023–2025—favor Kingsoft Cloud’s compliance credentials and long-term contract pipelines.

- RMB 200B+ government cloud procurement (2024)

- SOE digital budgets +18% YoY (2024)

- Kingsoft Cloud enterprise revenue +40% (2024)

- Regulatory mandates 2023–2025 supporting domestic providers

Regional Expansion and Belt and Road Initiative

Kingsoft Cloud leverages China’s diplomatic outreach, including Belt and Road, to expand into Southeast Asia and emerging markets, securing partnerships with local telcos and governments that boosted international revenue to about 14% of total revenue in FY2024 (RMB 1.2 billion of RMB 8.5 billion).

Political backing through BRI eases market entry, regulatory alignment, and infrastructure deals, supporting multi-region data center deployments and lowering single‑market concentration risk.

Expansion diversifies revenue streams, reducing reliance on China where FY2024 domestic revenue was ~86%, and targets faster-growing markets with cloud CAGR >20% in SEA (2024).

- International revenue FY2024: ~14% (RMB 1.2bn)

Kingsoft Cloud surges on RMB200B state demand, 40% enterprise growth, ramping domestic AI chips

Favorable domestic policy, strong SOE/government demand (RMB200B+ procurement 2024), and data‑sovereignty rules boost Kingsoft Cloud (enterprise rev +40% 2024; international rev ~14%); US export controls raised AI accelerator costs ~12–18% and prompted shift to domestic chips targeting 60% replacement by 2026, driving Rmb5.1bn 2024 capex in security/infrastructure.

| Metric | 2024 |

|---|---|

| Govt cloud procurement | RMB200B+ |

| Enterprise rev growth | +40% |

| Intl revenue | ~14% (RMB1.2bn) |

| Capex security/infrastructure | RMB5.1bn |

| AI accelerator premium | 12–18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely influence Kingsoft Cloud Holdings, with data-driven subpoints and trend-backed examples to highlight risks and opportunities for executives, investors and strategists.

A concise PESTLE summary of Kingsoft Cloud that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline discussions on regulatory, technological, economic, and competitive risks during planning sessions.

Economic factors

Post-Pandemic Macroeconomic Recovery

China's GDP growth stabilized at about 5.2% in 2024 and is projected near 4.8–5.0% for 2025, supporting gradual recovery in corporate IT budgets; this underpins rising cloud adoption and benefits Kingsoft Cloud. As enterprises prioritize cost-efficiency, demand for scalable cloud infrastructure grew ~28% YoY in 2024 across China’s cloud market, directly boosting Kingsoft Cloud’s addressable market. The firm’s revenue is sensitive to the Chinese internet sector performance and enterprise purchasing power, with enterprise IT spend recovery central to FY2025 forecasts.

Shift Toward High-Quality Growth and Profitability

The economic shift favors profitability over share gains, driving cloud providers to chase margins; in China cloud margins rose median 4 ppt in 2024, prompting strategic pivots.

Kingsoft Cloud is trimming low-margin CDN exposure and scaling enterprise IaaS/PaaS and security offerings, which represented 62% of 2024 revenue mix vs 54% in 2022.

This focus on cash flow helped EBITDA turn positive in H2 2024 and supports investor confidence as markets price cash-generative growth at higher multiples.

Competitive Pricing Pressures

Intense competition from Alibaba Cloud, Tencent Cloud and Huawei Cloud pushed average IaaS pricing down ~6–8% YoY in China 2024, squeezing margins for Kingsoft Cloud which reported capex of RMB 1.2bn in FY2024 to expand data centers. Kingsoft must balance lower prices to protect its ~3%–4% domestic market share with covering heavy infrastructure spending. This dynamic accelerates a shift toward differentiated, industry-focused cloud offerings (gaming, healthcare, finance) rather than pure price-per-unit competition.

Interest Rate Environment and Capital Access

Fluctuations in global and Chinese policy rates directly affect Kingsoft Cloud’s weighted average cost of capital; a 100 bps rise in rates in 2024 would materially increase borrowing costs for its capex-heavy data center rollouts.

Kingsoft Cloud spent RMB 1.8bn on capex in FY2023 and needs continuous R&D/data center investment to compete, so tighter credit markets could slow expansion or raise refinancing costs.

- FY2023 capex RMB 1.8bn; higher rates raise WACC

- Expansion depends on favorable financing conditions

- Debt refinancing sensitive to domestic policy rate moves

Growth in Vertically Integrated Cloud Solutions

Economic demand for vertical cloud—notably healthcare and finance—rose as these sectors grew cloud spend; global vertical cloud market was ~$45B in 2024 with 12% CAGR (2024–2029), favoring specialized providers.

Kingsoft Cloud leverages tailored stacks, compliance and low-latency services to capture higher ARPU; its enterprise cloud revenue grew ~28% YoY in 2024, outpacing overall cloud growth in China.

China's cloud surge: 28% growth fuels Kingsoft gains and $45B vertical opportunity

Slower but stable GDP (~5.2% in 2024; ~4.8–5.0% 2025) supports rising cloud spend; China cloud market grew ~28% YoY in 2024 boosting Kingsoft Cloud enterprise revenue +28% YoY. Margin focus lifted median cloud margins +4 ppt in 2024; Kingsoft’s H2 2024 EBITDA turned positive amid RMB capex ~1.2–1.8bn (FY2023–2024). Vertical cloud ~$45B (2024), 12% CAGR favors higher-ARPU industry stacks.

| Metric | 2024 | Note |

|---|---|---|

| China GDP | ~5.2% | 2024 actual |

| Cloud market growth | ~28% YoY | China 2024 |

| Kingsoft enterprise rev growth | +28% YoY | 2024 |

| Vertical cloud market | $45B | 2024, 12% CAGR |

| Capex | RMB 1.2–1.8bn | FY2023–2024 |

Full Version Awaits

Kingsoft Cloud Holdings PESTLE Analysis

The preview shown here is the exact Kingsoft Cloud Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same document you’ll download immediately after payment.

What you see is the final product—comprehensive, actionable, and delivered exactly as presented.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive advantage with our concise PESTLE Analysis of Kingsoft Cloud Holdings—highlighting political, economic, social, technological, legal, and environmental forces shaping its growth and risks; purchase the full report to access detailed, actionable insights and ready-to-use charts for investment decisions or strategic planning.

Political factors

Government Support for Digital Economy

The Chinese government lists the digital economy as a core growth pillar through 2025, targeting digital GDP to exceed 10 trillion yuan by 2025; Kingsoft Cloud benefits from policies subsidizing cloud migration and tax incentives that accelerate enterprise modernization.

This political alignment supports Kingsoft Cloud’s expansion into public services and SOE projects, where China’s public cloud spending grew ~28% year-on-year in 2024, boosting addressable demand.

Geopolitical Tensions and Supply Chain Risks

Persistent US-China trade tensions have constrained Kingsoft Cloud's access to high-end semiconductors, with US export controls since 2022 cutting off certain GPUs and contributing to a 12-18% premium on imported AI accelerators in 2024.

Restrictions on advanced GPUs—central to AI training and HPC—force Kingsoft Cloud to redesign procurement and risk management, as roughly 30-40% of its AI-capable fleet relied on Western chips in 2023.

These frictions drive a strategic pivot toward domestic hardware and collaborations with Chinese chipmakers to secure capacity and reduce supply-chain exposure, aiming to replace up to 60% of foreign-dependent units by 2026.

Data Sovereignty and National Security

Stringent data sovereignty laws force cloud firms to localize data and bolster security; China’s 2023 Personal Information Protection Law and Data Security Law, plus a 2024 draft critical data rules, raise compliance costs—Kingsoft Cloud reported Rmb5.1bn capex in 2024 investments in infrastructure and security. As an independent domestic provider it is favored by government and finance clients, but ongoing national security scrutiny increases audit frequency and legal risk.

State-Owned Enterprise Cloud Adoption

The political push for SOE cloud adoption in China has opened a large addressable market for Kingsoft Cloud, with government cloud procurement spending exceeding RMB 200 billion in 2024 and SOE digital budgets growing ~18% year-over-year.

By positioning as a secure, domestically controlled alternative to AWS/Alibaba, Kingsoft Cloud captured meaningful SOE deals contributing to its 2024 enterprise revenue growth of ~40% and narrowing gross margin gaps with larger peers.

Mandates to reduce dependence on foreign tech across critical infrastructure—reinforced by regulatory guidance in 2023–2025—favor Kingsoft Cloud’s compliance credentials and long-term contract pipelines.

- RMB 200B+ government cloud procurement (2024)

- SOE digital budgets +18% YoY (2024)

- Kingsoft Cloud enterprise revenue +40% (2024)

- Regulatory mandates 2023–2025 supporting domestic providers

Regional Expansion and Belt and Road Initiative

Kingsoft Cloud leverages China’s diplomatic outreach, including Belt and Road, to expand into Southeast Asia and emerging markets, securing partnerships with local telcos and governments that boosted international revenue to about 14% of total revenue in FY2024 (RMB 1.2 billion of RMB 8.5 billion).

Political backing through BRI eases market entry, regulatory alignment, and infrastructure deals, supporting multi-region data center deployments and lowering single‑market concentration risk.

Expansion diversifies revenue streams, reducing reliance on China where FY2024 domestic revenue was ~86%, and targets faster-growing markets with cloud CAGR >20% in SEA (2024).

- International revenue FY2024: ~14% (RMB 1.2bn)

Kingsoft Cloud surges on RMB200B state demand, 40% enterprise growth, ramping domestic AI chips

Favorable domestic policy, strong SOE/government demand (RMB200B+ procurement 2024), and data‑sovereignty rules boost Kingsoft Cloud (enterprise rev +40% 2024; international rev ~14%); US export controls raised AI accelerator costs ~12–18% and prompted shift to domestic chips targeting 60% replacement by 2026, driving Rmb5.1bn 2024 capex in security/infrastructure.

| Metric | 2024 |

|---|---|

| Govt cloud procurement | RMB200B+ |

| Enterprise rev growth | +40% |

| Intl revenue | ~14% (RMB1.2bn) |

| Capex security/infrastructure | RMB5.1bn |

| AI accelerator premium | 12–18% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely influence Kingsoft Cloud Holdings, with data-driven subpoints and trend-backed examples to highlight risks and opportunities for executives, investors and strategists.

A concise PESTLE summary of Kingsoft Cloud that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline discussions on regulatory, technological, economic, and competitive risks during planning sessions.

Economic factors

Post-Pandemic Macroeconomic Recovery

China's GDP growth stabilized at about 5.2% in 2024 and is projected near 4.8–5.0% for 2025, supporting gradual recovery in corporate IT budgets; this underpins rising cloud adoption and benefits Kingsoft Cloud. As enterprises prioritize cost-efficiency, demand for scalable cloud infrastructure grew ~28% YoY in 2024 across China’s cloud market, directly boosting Kingsoft Cloud’s addressable market. The firm’s revenue is sensitive to the Chinese internet sector performance and enterprise purchasing power, with enterprise IT spend recovery central to FY2025 forecasts.

Shift Toward High-Quality Growth and Profitability

The economic shift favors profitability over share gains, driving cloud providers to chase margins; in China cloud margins rose median 4 ppt in 2024, prompting strategic pivots.

Kingsoft Cloud is trimming low-margin CDN exposure and scaling enterprise IaaS/PaaS and security offerings, which represented 62% of 2024 revenue mix vs 54% in 2022.

This focus on cash flow helped EBITDA turn positive in H2 2024 and supports investor confidence as markets price cash-generative growth at higher multiples.

Competitive Pricing Pressures

Intense competition from Alibaba Cloud, Tencent Cloud and Huawei Cloud pushed average IaaS pricing down ~6–8% YoY in China 2024, squeezing margins for Kingsoft Cloud which reported capex of RMB 1.2bn in FY2024 to expand data centers. Kingsoft must balance lower prices to protect its ~3%–4% domestic market share with covering heavy infrastructure spending. This dynamic accelerates a shift toward differentiated, industry-focused cloud offerings (gaming, healthcare, finance) rather than pure price-per-unit competition.

Interest Rate Environment and Capital Access

Fluctuations in global and Chinese policy rates directly affect Kingsoft Cloud’s weighted average cost of capital; a 100 bps rise in rates in 2024 would materially increase borrowing costs for its capex-heavy data center rollouts.

Kingsoft Cloud spent RMB 1.8bn on capex in FY2023 and needs continuous R&D/data center investment to compete, so tighter credit markets could slow expansion or raise refinancing costs.

- FY2023 capex RMB 1.8bn; higher rates raise WACC

- Expansion depends on favorable financing conditions

- Debt refinancing sensitive to domestic policy rate moves

Growth in Vertically Integrated Cloud Solutions

Economic demand for vertical cloud—notably healthcare and finance—rose as these sectors grew cloud spend; global vertical cloud market was ~$45B in 2024 with 12% CAGR (2024–2029), favoring specialized providers.

Kingsoft Cloud leverages tailored stacks, compliance and low-latency services to capture higher ARPU; its enterprise cloud revenue grew ~28% YoY in 2024, outpacing overall cloud growth in China.

China's cloud surge: 28% growth fuels Kingsoft gains and $45B vertical opportunity

Slower but stable GDP (~5.2% in 2024; ~4.8–5.0% 2025) supports rising cloud spend; China cloud market grew ~28% YoY in 2024 boosting Kingsoft Cloud enterprise revenue +28% YoY. Margin focus lifted median cloud margins +4 ppt in 2024; Kingsoft’s H2 2024 EBITDA turned positive amid RMB capex ~1.2–1.8bn (FY2023–2024). Vertical cloud ~$45B (2024), 12% CAGR favors higher-ARPU industry stacks.

| Metric | 2024 | Note |

|---|---|---|

| China GDP | ~5.2% | 2024 actual |

| Cloud market growth | ~28% YoY | China 2024 |

| Kingsoft enterprise rev growth | +28% YoY | 2024 |

| Vertical cloud market | $45B | 2024, 12% CAGR |

| Capex | RMB 1.2–1.8bn | FY2023–2024 |

Full Version Awaits

Kingsoft Cloud Holdings PESTLE Analysis

The preview shown here is the exact Kingsoft Cloud Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same document you’ll download immediately after payment.

What you see is the final product—comprehensive, actionable, and delivered exactly as presented.