KT Boston Consulting Group Matrix

Download Your Competitive Advantage

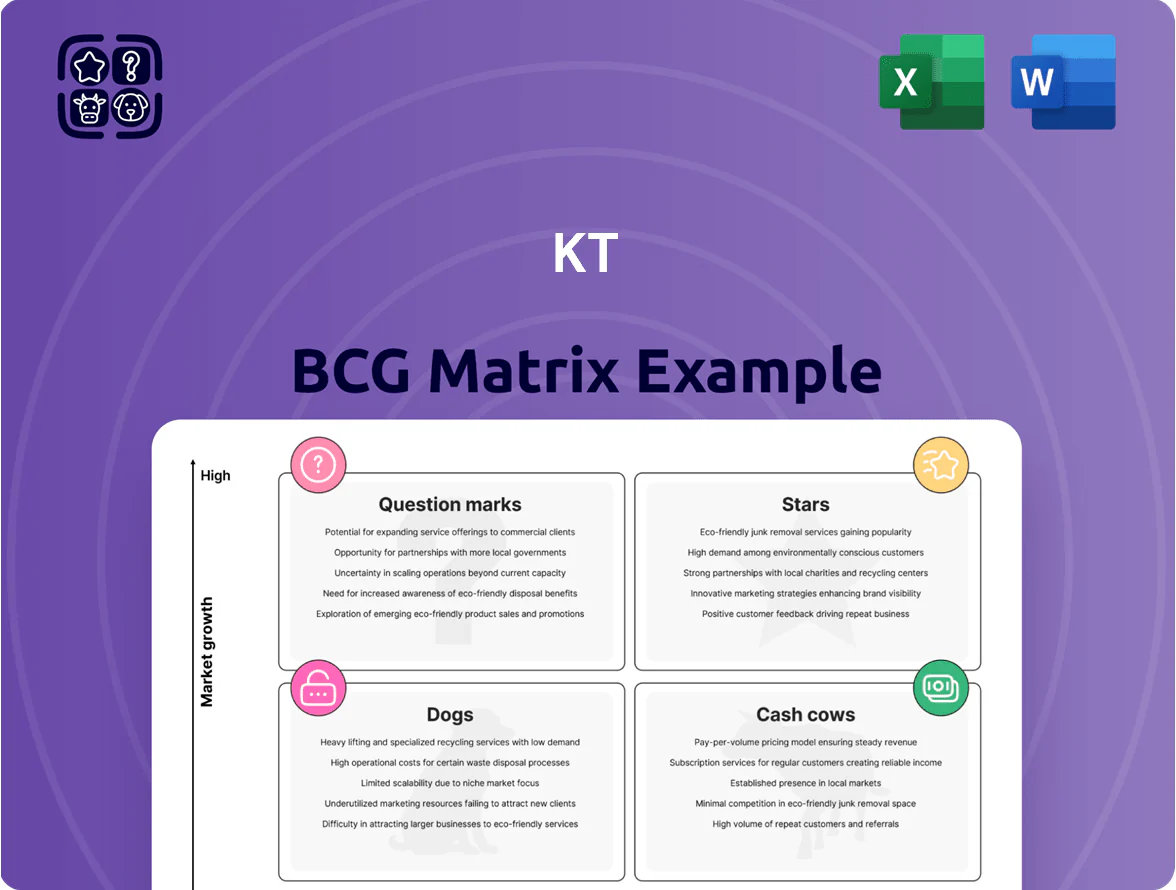

The KT BCG Matrix preview highlights how the company’s offerings map to market growth and relative share—spotting Stars worth scaling, Cash Cows funding growth, Question Marks needing decisions, and Dogs to divest. This snapshot reveals strategic tensions and immediate allocation priorities. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and ready-to-use Word and Excel files to guide investment and product strategy with confidence.

Stars

AI-Powered Cloud and IDC Services

KT has cemented leadership in South Korea’s cloud market by adding AI-optimized infrastructure to its data centers, capturing ~35% share of AI-ready sovereign cloud demand by Q4 2025, per industry reports.

Surging local demand—estimated CAGR ~28% 2023–2025 for AI-ready cloud—let KT win large enterprise contracts, driving the unit to generate roughly KRW 1.2 trillion in 2025 revenue.

The unit needs heavy capex—KT invested ~KRW 450 billion in 2024–2025 for GPUs, networking, and cooling to keep parity with hyperscalers and meet regulatory data-sovereignty rules.

Enterprise 5G and Private Networks

Enterprise 5G and Private Networks: KT has pivoted from consumer 5G to B2B, supplying smart factories and autonomous logistics hubs and holding about 45% share of South Korea’s dedicated private network market as of 2025.

Demand is high—IDC forecasts 5G private network spend in Korea to grow ~22% CAGR 2024–2027—so KT’s continuous capex in network slicing and edge computing (≈KRW 300bn planned 2025) is critical to defend leadership.

Content Production via Studio Genie

KT Studio Genie produces premium Korean content that feeds KT’s ecosystem; in 2025 it reported content revenues of KRW 410 billion, up 28% YoY, and licensed titles earned KRW 95 billion abroad through 120 deals across 35 countries.

AICT Digital Transformation Consulting

AICT Digital Transformation Consulting is a Star in KT’s BCG matrix, driving double-digit revenue growth as public-sector AI spend surged 38% in 2024 to $2.9B in South Korea; KT’s tailored generative-AI solutions capture an estimated 32% market share in government digital projects.

KT’s long-standing government contracts create a durable moat, supporting high market share and 20–25% EBITDA margins in 2024 for the unit, while private-sector uptake lifts total addressable market forecasts to $6.5B by 2027.

- 2024 public AI spend +38% to $2.9B

- KT market share ~32% in gov projects

- Unit EBITDA margin 20–25% (2024)

- TAM projected $6.5B by 2027

Next-Generation Financial Services

KT’s Next-Generation Financial Services is a Star: owning BC Card and K-Bank, KT combines telco data with banking to launch fintech products—K-Bank had ~5.2 million customers by end-2024 and BC Card processed ~120 trillion KRW in 2024 transactions, driving high growth.

Digital banking adoption among Koreans aged 20–39 was ~78% in 2024, boosting market growth; KT cross-sells to its ~22 million mobile subscribers, securing high market share and strong competitive positioning.

- K-Bank customers ~5.2M (2024)

- BC Card volume ~120T KRW (2024)

- Mobile subs ~22M (KT, 2024)

- Digital banking usage 78% (age 20–39, 2024)

KT’s Growth Engines: AI Cloud, Private 5G, Studio Genie, AICT & Fintech Powerhouses

KT’s Stars: AI-ready cloud (~35% sovereign share, KRW 1.2T rev 2025), Private 5G (~45% private network share, KRW 300bn capex 2025), Studio Genie (KRW 410bn content rev 2025), AICT consulting (32% gov share, 20–25% EBITDA 2024), Next‑Gen finance (K‑Bank 5.2M, BC Card KRW 120T vol 2024).

| Unit | Key metric |

|---|---|

| AI Cloud | 35% share; KRW 1.2T |

| Private 5G | 45% share; KRW 300bn capex |

| Studio Genie | KRW 410bn rev |

| AICT | 32% gov; 20–25% EBITDA |

| Fintech | K‑Bank 5.2M; BC 120T KRW |

What is included in the product

Comprehensive KT BCG Matrix review: quadrant strategies, investment/exit guidance, competitive threats, and trend-driven portfolio actions.

One-page KT BCG Matrix mapping units to quadrants for instant strategic clarity and resource prioritization

Cash Cows

Wireless Mobile Communications

KT's wireless mobile segment sits as a classic Cash Cow: South Korea's mobile market is mature, yet KT held about 31% share of 2024 wireless subscribers (~15.6 million lines) delivering stable EBITDA margins near 32% in FY2024.

With 5G penetration at ~95% nationwide by end-2025, subscriber churn falls and marketing spend declines, lifting unit margins and free cash flow.

That steady cash stream funded KT's 2024–25 capex and R&D push into AI and cloud, contributing roughly KRW 600 billion freed cash used for cloud expansion and AI platform investments.

Giga Internet and Broadband

KT remains the undisputed leader in South Korea’s high‑speed internet, operating about 220,000 km of fiber—roughly 35% more than its nearest rival as of 2025—making Giga Internet a cash cow with low market growth due to near‑saturation.

High barriers to entry—capital‑intensive fiber rollout and nationwide access agreements—protect margins; stable ARPU (about KRW 28,000/month in 2024) from 8.7 million broadband subscribers supplies predictable cash for dividends and group investments.

IPTV and Genie TV Services

The IPTV segment is mature; KT held about 45% market share in South Korea IPTV subscriptions in 2024, delivering stable monthly recurring revenue of roughly KRW 1.2 trillion annually from pay-TV services.

Despite global OTT growth, Genie TV remained a domestic hub with reported churn near 2.5% in 2024, keeping ARPU steady at ~KRW 18,000 per user.

KT now targets minor UX and content bundling upgrades rather than heavy capex; operating margins for the unit stayed high at ~28% in FY2024, maximizing cash yield.

Fixed-line Voice Services

Fixed-line voice services are a declining market, but KT (Korea Telecom) leverages legacy copper and fiber assets to retain ~2.1 million fixed voice subscribers as of FY2024, requiring almost no new capex and generating steady EBITDA margins >50%—making it a low-growth, high-cash segment.

Growth is flat-to-negative (-3% CAGR 2021–24), operating costs are minimal, and net cash contribution helped KT fund broadband and 5G investments in 2024, so this aging tech remains a defensive cash cow.

- ~2.1M subscribers (FY2024)

- -3% voice revenue CAGR 2021–24

- EBITDA margin >50% on segment

- Minimal capex; funding other growth units

Real Estate Management

KT Estate leverages KT’s historic land and building portfolio across South Korea to generate stable rental income, contributing roughly KRW 120–150 billion annual EBITDA (2024 estimate) from converted telephone offices into residential and commercial units.

The conversions yield high margins—operating margins near 35%—and low annual capex (<5% of revenue), offering a hedge against telecom cyclicality and lower volatility versus KT’s high-tech units.

- Stable cash flow: KRW 200–250B revenue (2024 est.)

- High margin: ~35% operating margin

- Low maintenance: capex <5% revenue

- Low growth: single-digit CAGR expected

KT’s Core Cash Cows: Mobile, Broadband, IPTV, Fixed Voice & Estate Driving Profits

KT's Cash Cows: mobile (31% share, ~15.6M lines, 32% EBITDA FY2024), broadband (8.7M subs, KRW 28,000 ARPU, 220,000 km fiber), IPTV (45% share, KRW 1.2T revenue, ~28% margin), fixed voice (2.1M subs, >50% EBITDA, -3% CAGR 2021–24), KT Estate (KRW 200–250B revenue, ~35% margin).

| Unit | Key metric |

|---|---|

| Mobile | 15.6M lines; 32% EBITDA |

| Broadband | 8.7M subs; KRW28,000 ARPU |

| IPTV | 45% share; KRW1.2T rev |

| Fixed voice | 2.1M subs; >50% EBITDA |

| Estate | KRW200–250B rev; 35% margin |

Full Transparency, Always

KT BCG Matrix

The file you're previewing is the exact KT BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted and analysis-ready for strategic planning or presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The KT BCG Matrix preview highlights how the company’s offerings map to market growth and relative share—spotting Stars worth scaling, Cash Cows funding growth, Question Marks needing decisions, and Dogs to divest. This snapshot reveals strategic tensions and immediate allocation priorities. Purchase the full BCG Matrix for quadrant-level placements, data-backed recommendations, and ready-to-use Word and Excel files to guide investment and product strategy with confidence.

Stars

AI-Powered Cloud and IDC Services

KT has cemented leadership in South Korea’s cloud market by adding AI-optimized infrastructure to its data centers, capturing ~35% share of AI-ready sovereign cloud demand by Q4 2025, per industry reports.

Surging local demand—estimated CAGR ~28% 2023–2025 for AI-ready cloud—let KT win large enterprise contracts, driving the unit to generate roughly KRW 1.2 trillion in 2025 revenue.

The unit needs heavy capex—KT invested ~KRW 450 billion in 2024–2025 for GPUs, networking, and cooling to keep parity with hyperscalers and meet regulatory data-sovereignty rules.

Enterprise 5G and Private Networks

Enterprise 5G and Private Networks: KT has pivoted from consumer 5G to B2B, supplying smart factories and autonomous logistics hubs and holding about 45% share of South Korea’s dedicated private network market as of 2025.

Demand is high—IDC forecasts 5G private network spend in Korea to grow ~22% CAGR 2024–2027—so KT’s continuous capex in network slicing and edge computing (≈KRW 300bn planned 2025) is critical to defend leadership.

Content Production via Studio Genie

KT Studio Genie produces premium Korean content that feeds KT’s ecosystem; in 2025 it reported content revenues of KRW 410 billion, up 28% YoY, and licensed titles earned KRW 95 billion abroad through 120 deals across 35 countries.

AICT Digital Transformation Consulting

AICT Digital Transformation Consulting is a Star in KT’s BCG matrix, driving double-digit revenue growth as public-sector AI spend surged 38% in 2024 to $2.9B in South Korea; KT’s tailored generative-AI solutions capture an estimated 32% market share in government digital projects.

KT’s long-standing government contracts create a durable moat, supporting high market share and 20–25% EBITDA margins in 2024 for the unit, while private-sector uptake lifts total addressable market forecasts to $6.5B by 2027.

- 2024 public AI spend +38% to $2.9B

- KT market share ~32% in gov projects

- Unit EBITDA margin 20–25% (2024)

- TAM projected $6.5B by 2027

Next-Generation Financial Services

KT’s Next-Generation Financial Services is a Star: owning BC Card and K-Bank, KT combines telco data with banking to launch fintech products—K-Bank had ~5.2 million customers by end-2024 and BC Card processed ~120 trillion KRW in 2024 transactions, driving high growth.

Digital banking adoption among Koreans aged 20–39 was ~78% in 2024, boosting market growth; KT cross-sells to its ~22 million mobile subscribers, securing high market share and strong competitive positioning.

- K-Bank customers ~5.2M (2024)

- BC Card volume ~120T KRW (2024)

- Mobile subs ~22M (KT, 2024)

- Digital banking usage 78% (age 20–39, 2024)

KT’s Growth Engines: AI Cloud, Private 5G, Studio Genie, AICT & Fintech Powerhouses

KT’s Stars: AI-ready cloud (~35% sovereign share, KRW 1.2T rev 2025), Private 5G (~45% private network share, KRW 300bn capex 2025), Studio Genie (KRW 410bn content rev 2025), AICT consulting (32% gov share, 20–25% EBITDA 2024), Next‑Gen finance (K‑Bank 5.2M, BC Card KRW 120T vol 2024).

| Unit | Key metric |

|---|---|

| AI Cloud | 35% share; KRW 1.2T |

| Private 5G | 45% share; KRW 300bn capex |

| Studio Genie | KRW 410bn rev |

| AICT | 32% gov; 20–25% EBITDA |

| Fintech | K‑Bank 5.2M; BC 120T KRW |

What is included in the product

Comprehensive KT BCG Matrix review: quadrant strategies, investment/exit guidance, competitive threats, and trend-driven portfolio actions.

One-page KT BCG Matrix mapping units to quadrants for instant strategic clarity and resource prioritization

Cash Cows

Wireless Mobile Communications

KT's wireless mobile segment sits as a classic Cash Cow: South Korea's mobile market is mature, yet KT held about 31% share of 2024 wireless subscribers (~15.6 million lines) delivering stable EBITDA margins near 32% in FY2024.

With 5G penetration at ~95% nationwide by end-2025, subscriber churn falls and marketing spend declines, lifting unit margins and free cash flow.

That steady cash stream funded KT's 2024–25 capex and R&D push into AI and cloud, contributing roughly KRW 600 billion freed cash used for cloud expansion and AI platform investments.

Giga Internet and Broadband

KT remains the undisputed leader in South Korea’s high‑speed internet, operating about 220,000 km of fiber—roughly 35% more than its nearest rival as of 2025—making Giga Internet a cash cow with low market growth due to near‑saturation.

High barriers to entry—capital‑intensive fiber rollout and nationwide access agreements—protect margins; stable ARPU (about KRW 28,000/month in 2024) from 8.7 million broadband subscribers supplies predictable cash for dividends and group investments.

IPTV and Genie TV Services

The IPTV segment is mature; KT held about 45% market share in South Korea IPTV subscriptions in 2024, delivering stable monthly recurring revenue of roughly KRW 1.2 trillion annually from pay-TV services.

Despite global OTT growth, Genie TV remained a domestic hub with reported churn near 2.5% in 2024, keeping ARPU steady at ~KRW 18,000 per user.

KT now targets minor UX and content bundling upgrades rather than heavy capex; operating margins for the unit stayed high at ~28% in FY2024, maximizing cash yield.

Fixed-line Voice Services

Fixed-line voice services are a declining market, but KT (Korea Telecom) leverages legacy copper and fiber assets to retain ~2.1 million fixed voice subscribers as of FY2024, requiring almost no new capex and generating steady EBITDA margins >50%—making it a low-growth, high-cash segment.

Growth is flat-to-negative (-3% CAGR 2021–24), operating costs are minimal, and net cash contribution helped KT fund broadband and 5G investments in 2024, so this aging tech remains a defensive cash cow.

- ~2.1M subscribers (FY2024)

- -3% voice revenue CAGR 2021–24

- EBITDA margin >50% on segment

- Minimal capex; funding other growth units

Real Estate Management

KT Estate leverages KT’s historic land and building portfolio across South Korea to generate stable rental income, contributing roughly KRW 120–150 billion annual EBITDA (2024 estimate) from converted telephone offices into residential and commercial units.

The conversions yield high margins—operating margins near 35%—and low annual capex (<5% of revenue), offering a hedge against telecom cyclicality and lower volatility versus KT’s high-tech units.

- Stable cash flow: KRW 200–250B revenue (2024 est.)

- High margin: ~35% operating margin

- Low maintenance: capex <5% revenue

- Low growth: single-digit CAGR expected

KT’s Core Cash Cows: Mobile, Broadband, IPTV, Fixed Voice & Estate Driving Profits

KT's Cash Cows: mobile (31% share, ~15.6M lines, 32% EBITDA FY2024), broadband (8.7M subs, KRW 28,000 ARPU, 220,000 km fiber), IPTV (45% share, KRW 1.2T revenue, ~28% margin), fixed voice (2.1M subs, >50% EBITDA, -3% CAGR 2021–24), KT Estate (KRW 200–250B revenue, ~35% margin).

| Unit | Key metric |

|---|---|

| Mobile | 15.6M lines; 32% EBITDA |

| Broadband | 8.7M subs; KRW28,000 ARPU |

| IPTV | 45% share; KRW1.2T rev |

| Fixed voice | 2.1M subs; >50% EBITDA |

| Estate | KRW200–250B rev; 35% margin |

Full Transparency, Always

KT BCG Matrix

The file you're previewing is the exact KT BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—fully formatted and analysis-ready for strategic planning or presentations.