KT Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

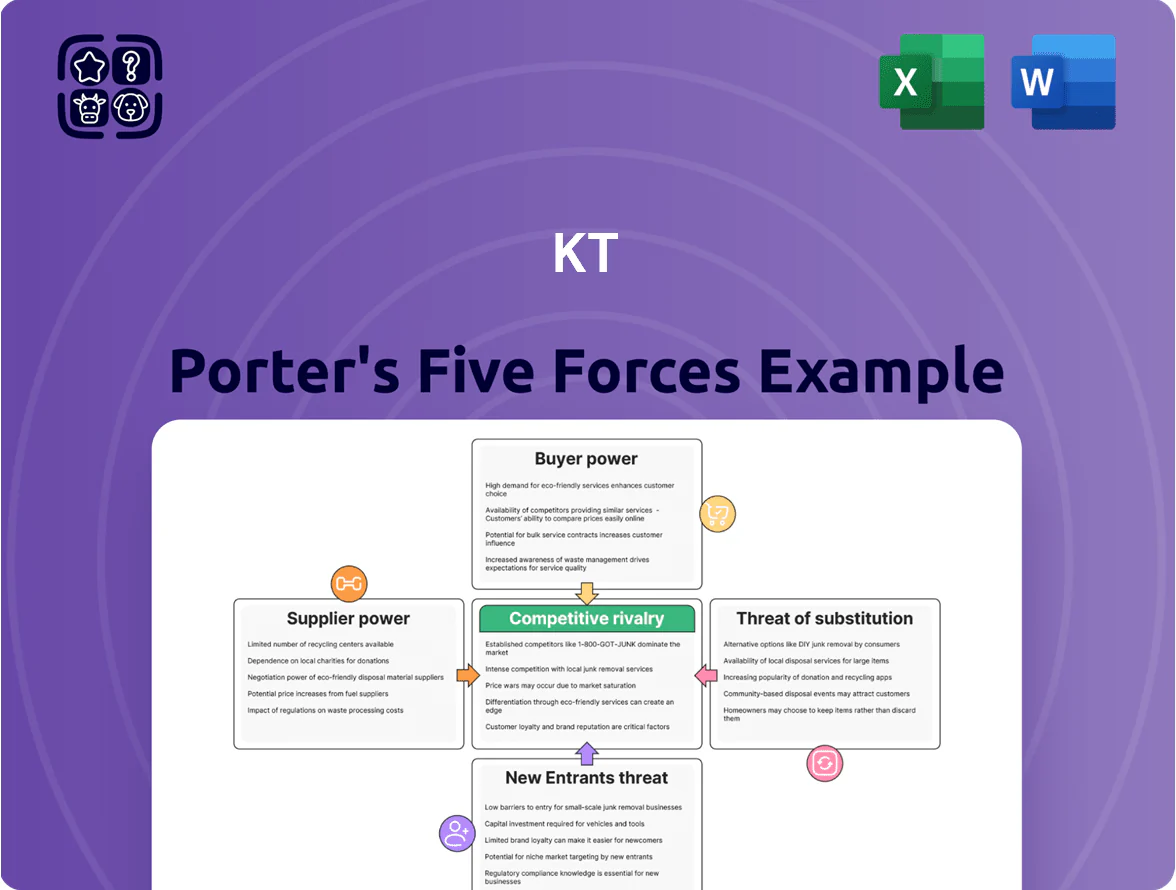

KT’s Porter’s Five Forces snapshot highlights supplier bargaining, buyer power, competitive rivalry, threat of substitutes, and new entrants—each shaping profitability and strategic choices for the firm.

Suppliers Bargaining Power

Dependency on Global Network Equipment Vendors

KT depends on a few global vendors—Samsung Electronics, Ericsson, and Nokia—for 5G/6G core and radio gear; in 2024 these three supplied roughly 70–80% of global RAN shipments, giving them clear leverage.

Specialized hardware needs for upgrades raise supplier bargaining power, as switching core suppliers can cost hundreds of millions and delay deployments months.

As KT densifies networks and adds AI-driven architecture, high integration and interoperability costs keep supplier power at moderate to high levels.

Specialized AI and Semiconductor Procurement

Content Acquisition Costs for Media Services

As a major IPTV and media provider, KT must negotiate distribution rights with global giants like Disney and Netflix and domestic broadcasters, where average U.S. drama licensing fees rose ~15% in 2024 and top-tier bundles now command millions per title.

Rising global streaming demand gives production houses more leverage; in 2024 exclusive window deals pushed premium content prices up 10–20%, squeezing license margins for distributors.

KT’s subscriber retention hinges on that content, so KT either pays higher licensing costs—pressuring EBITDA—or must invest in originals, where successful K-drama productions can cost $2–5 million per episode.

Energy Providers and Infrastructure Maintenance

Operating massive data centers and nationwide networks makes KT highly sensitive to energy prices and utility rules; energy is a non-differentiable essential input so utility providers exert strong bargaining power over KT’s OPEX.

Global energy price swings through 2023–2025 cut margins for infrastructure-heavy telcos; KT reported energy-related network costs rose ~8–12% year-on-year in 2024, with limited negotiation room against state-linked utility monopolies.

- Essential input: energy not substitutable

- Supplier power: state-linked utilities dominant

- Impact: energy costs up ~8–12% YoY in 2024

- Negotiation: limited leverage vs. monopolies

Software and Cloud Platform Dependencies

KT runs its own cloud but still depends on global ERP and cybersecurity vendors that command leverage via multi-year licenses and complex integrations; Gartner estimated enterprise security renewal rates at ~85% in 2024, reflecting vendor stickiness.

Switching costs are high—technical debt, data migration, and retraining—so suppliers frequently secure price leverage during renewals; KT’s 2023 capex shift showed 18% of IT spend tied to third-party software contracts.

- 85% security renewal rate (Gartner 2024)

- 18% of IT spend bound to third-party software (KT 2023)

- Long-term licenses + integration complexity = high switching cost

KT Faces Concentrated Supplier Power: RAN, NVIDIA GPUs, Rising Energy & Vendor Risks

KT faces moderate–high supplier power: core RAN vendors (Samsung, Ericsson, Nokia) supplied ~70–80% RAN in 2024; NVIDIA held ~80% data‑center GPU share in 2024; AI chip revenue rose 45% to $34B in 2024; energy costs increased ~8–12% YoY in 2024; 85% security renewal rate (Gartner 2024); 18% of IT spend tied to third‑party software (KT 2023).

| Supplier | 2024 metric |

|---|---|

| RAN vendors | 70–80% global RAN |

| GPUs (NVIDIA) | ~80% market share |

| AI chips | $34B, +45% YoY |

| Energy | +8–12% YoY |

| Security renewals | 85% rate |

| IT spend to vendors | 18% |

What is included in the product

Concise Porter’s Five Forces for KT: dissects competitive rivalry, buyer/supplier power, substitution threats, and entry barriers with industry data and strategic insights to reveal KT’s market leverage and vulnerabilities.

KT Porter's Five Forces condensed into a single, editable sheet—speed up strategic decisions with a clean radar chart, customizable pressure levels, and plug-and-play integration for decks and dashboards.

Customers Bargaining Power

High Market Saturation and Switching Ease

The South Korean mobile and broadband market is mature: mobile penetration was 127% and fixed broadband penetration 40% in 2024, so growth mostly means stealing subscribers. Mobile number portability and similar package structures make switching easy, raising retail bargaining power. KT must run ongoing promotions and loyalty programs—KT spent KRW 320 billion on marketing and subsidies in 2024—to limit churn among price-sensitive consumers.

Regulatory Pressure on Telecommunication Fees

The South Korean government repeatedly intervenes to keep telecom prices low; in 2024 regulators pushed carriers to cut avg 5G plan prices by about 12%, squeezing margins for KT (KT Corporation reported 2024 roaming/ARPU pressures in its Feb 2025 disclosure).

Growth of MVNOs Providing Cheaper Alternatives

MVNOs in South Korea grabbed about 15% of mobile subscribers by end-2024 (roughly 8.1M users), selling low-cost plans on KT’s network and cutting average revenue per user (ARPU) pressure; KT’s 2024 mobile ARPU fell 3.2% YoY to ~KRW 31,200.

Corporate and Enterprise Client Leverage

Large enterprise clients and government agencies negotiate bespoke contracts for IT, cloud, and dedicated network services, using in-house procurement teams to extract discounts and tailored SLAs.

These customers often evaluate multiple bidders and secure price concessions; in 2024 KT reported that top-20 B2B clients accounted for about 38% of enterprise revenue, so losing one can cut EBIT by several percentage points.

- Top-20 clients = ~38% B2B revenue (KT, 2024)

- Bespoke SLAs & discounts common

- High switching cost but concentrated risk

Demand for Integrated Digital Services

Modern customers want bundled mobile, broadband, IPTV, and home AI; in 2024 KT reported 42% of postpaid subscribers on at least one bundle, raising average revenue per user (ARPU) by KRW 3,800/month.

Bundling boosts stickiness but gives customers leverage to demand multi-service discounts—KT offered up to 25% off on quad-play plans in 2025, pressuring margins.

KT must refresh bundles and add AI features; churn rises quickly if the integrated ecosystem trails competitors—Korea’s quad-play churn gap was 1.4x higher in lagging providers (2024).

- 42% bundled postpaid users (KT, 2024)

- ARPU +KRW 3,800/month for bundled users

- Up to 25% discounts on quad-play (2025)

- 1.4x higher churn for lagging providers (2024)

KT squeezed by powerful customers, MVNOs and regulatory price cuts—ARPU under pressure

Customers hold strong bargaining power: high mobile penetration (127% in 2024) and easy switching push KT into heavy marketing (KRW 320bn in 2024) and discounts; regulators cut 5G prices ~12% in 2024; MVNOs ~15% share (~8.1M users) and KT mobile ARPU fell 3.2% to KRW 31,200. Large B2B clients (top-20 = 38% revenue) extract bespoke SLAs and discounts, while 42% of postpaid users take bundles (+KRW 3,800 ARPU).

| Metric | 2024/2025 |

|---|---|

| Mobile penetration | 127% |

| Fixed broadband | 40% |

| MVNO share | 15% (~8.1M) |

| KT marketing spend | KRW 320bn |

| KT mobile ARPU | KRW 31,200 (-3.2%) |

| Top-20 B2B rev | 38% |

| Bundled postpaid | 42% (+KRW 3,800) |

Full Version Awaits

KT Porter's Five Forces Analysis

This preview shows the exact KT Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

KT’s Porter’s Five Forces snapshot highlights supplier bargaining, buyer power, competitive rivalry, threat of substitutes, and new entrants—each shaping profitability and strategic choices for the firm.

Suppliers Bargaining Power

Dependency on Global Network Equipment Vendors

KT depends on a few global vendors—Samsung Electronics, Ericsson, and Nokia—for 5G/6G core and radio gear; in 2024 these three supplied roughly 70–80% of global RAN shipments, giving them clear leverage.

Specialized hardware needs for upgrades raise supplier bargaining power, as switching core suppliers can cost hundreds of millions and delay deployments months.

As KT densifies networks and adds AI-driven architecture, high integration and interoperability costs keep supplier power at moderate to high levels.

Specialized AI and Semiconductor Procurement

Content Acquisition Costs for Media Services

As a major IPTV and media provider, KT must negotiate distribution rights with global giants like Disney and Netflix and domestic broadcasters, where average U.S. drama licensing fees rose ~15% in 2024 and top-tier bundles now command millions per title.

Rising global streaming demand gives production houses more leverage; in 2024 exclusive window deals pushed premium content prices up 10–20%, squeezing license margins for distributors.

KT’s subscriber retention hinges on that content, so KT either pays higher licensing costs—pressuring EBITDA—or must invest in originals, where successful K-drama productions can cost $2–5 million per episode.

Energy Providers and Infrastructure Maintenance

Operating massive data centers and nationwide networks makes KT highly sensitive to energy prices and utility rules; energy is a non-differentiable essential input so utility providers exert strong bargaining power over KT’s OPEX.

Global energy price swings through 2023–2025 cut margins for infrastructure-heavy telcos; KT reported energy-related network costs rose ~8–12% year-on-year in 2024, with limited negotiation room against state-linked utility monopolies.

- Essential input: energy not substitutable

- Supplier power: state-linked utilities dominant

- Impact: energy costs up ~8–12% YoY in 2024

- Negotiation: limited leverage vs. monopolies

Software and Cloud Platform Dependencies

KT runs its own cloud but still depends on global ERP and cybersecurity vendors that command leverage via multi-year licenses and complex integrations; Gartner estimated enterprise security renewal rates at ~85% in 2024, reflecting vendor stickiness.

Switching costs are high—technical debt, data migration, and retraining—so suppliers frequently secure price leverage during renewals; KT’s 2023 capex shift showed 18% of IT spend tied to third-party software contracts.

- 85% security renewal rate (Gartner 2024)

- 18% of IT spend bound to third-party software (KT 2023)

- Long-term licenses + integration complexity = high switching cost

KT Faces Concentrated Supplier Power: RAN, NVIDIA GPUs, Rising Energy & Vendor Risks

KT faces moderate–high supplier power: core RAN vendors (Samsung, Ericsson, Nokia) supplied ~70–80% RAN in 2024; NVIDIA held ~80% data‑center GPU share in 2024; AI chip revenue rose 45% to $34B in 2024; energy costs increased ~8–12% YoY in 2024; 85% security renewal rate (Gartner 2024); 18% of IT spend tied to third‑party software (KT 2023).

| Supplier | 2024 metric |

|---|---|

| RAN vendors | 70–80% global RAN |

| GPUs (NVIDIA) | ~80% market share |

| AI chips | $34B, +45% YoY |

| Energy | +8–12% YoY |

| Security renewals | 85% rate |

| IT spend to vendors | 18% |

What is included in the product

Concise Porter’s Five Forces for KT: dissects competitive rivalry, buyer/supplier power, substitution threats, and entry barriers with industry data and strategic insights to reveal KT’s market leverage and vulnerabilities.

KT Porter's Five Forces condensed into a single, editable sheet—speed up strategic decisions with a clean radar chart, customizable pressure levels, and plug-and-play integration for decks and dashboards.

Customers Bargaining Power

High Market Saturation and Switching Ease

The South Korean mobile and broadband market is mature: mobile penetration was 127% and fixed broadband penetration 40% in 2024, so growth mostly means stealing subscribers. Mobile number portability and similar package structures make switching easy, raising retail bargaining power. KT must run ongoing promotions and loyalty programs—KT spent KRW 320 billion on marketing and subsidies in 2024—to limit churn among price-sensitive consumers.

Regulatory Pressure on Telecommunication Fees

The South Korean government repeatedly intervenes to keep telecom prices low; in 2024 regulators pushed carriers to cut avg 5G plan prices by about 12%, squeezing margins for KT (KT Corporation reported 2024 roaming/ARPU pressures in its Feb 2025 disclosure).

Growth of MVNOs Providing Cheaper Alternatives

MVNOs in South Korea grabbed about 15% of mobile subscribers by end-2024 (roughly 8.1M users), selling low-cost plans on KT’s network and cutting average revenue per user (ARPU) pressure; KT’s 2024 mobile ARPU fell 3.2% YoY to ~KRW 31,200.

Corporate and Enterprise Client Leverage

Large enterprise clients and government agencies negotiate bespoke contracts for IT, cloud, and dedicated network services, using in-house procurement teams to extract discounts and tailored SLAs.

These customers often evaluate multiple bidders and secure price concessions; in 2024 KT reported that top-20 B2B clients accounted for about 38% of enterprise revenue, so losing one can cut EBIT by several percentage points.

- Top-20 clients = ~38% B2B revenue (KT, 2024)

- Bespoke SLAs & discounts common

- High switching cost but concentrated risk

Demand for Integrated Digital Services

Modern customers want bundled mobile, broadband, IPTV, and home AI; in 2024 KT reported 42% of postpaid subscribers on at least one bundle, raising average revenue per user (ARPU) by KRW 3,800/month.

Bundling boosts stickiness but gives customers leverage to demand multi-service discounts—KT offered up to 25% off on quad-play plans in 2025, pressuring margins.

KT must refresh bundles and add AI features; churn rises quickly if the integrated ecosystem trails competitors—Korea’s quad-play churn gap was 1.4x higher in lagging providers (2024).

- 42% bundled postpaid users (KT, 2024)

- ARPU +KRW 3,800/month for bundled users

- Up to 25% discounts on quad-play (2025)

- 1.4x higher churn for lagging providers (2024)

KT squeezed by powerful customers, MVNOs and regulatory price cuts—ARPU under pressure

Customers hold strong bargaining power: high mobile penetration (127% in 2024) and easy switching push KT into heavy marketing (KRW 320bn in 2024) and discounts; regulators cut 5G prices ~12% in 2024; MVNOs ~15% share (~8.1M users) and KT mobile ARPU fell 3.2% to KRW 31,200. Large B2B clients (top-20 = 38% revenue) extract bespoke SLAs and discounts, while 42% of postpaid users take bundles (+KRW 3,800 ARPU).

| Metric | 2024/2025 |

|---|---|

| Mobile penetration | 127% |

| Fixed broadband | 40% |

| MVNO share | 15% (~8.1M) |

| KT marketing spend | KRW 320bn |

| KT mobile ARPU | KRW 31,200 (-3.2%) |

| Top-20 B2B rev | 38% |

| Bundled postpaid | 42% (+KRW 3,800) |

Full Version Awaits

KT Porter's Five Forces Analysis

This preview shows the exact KT Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s fully formatted, professionally written, and ready for download and use the moment you buy.