Kudelski Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

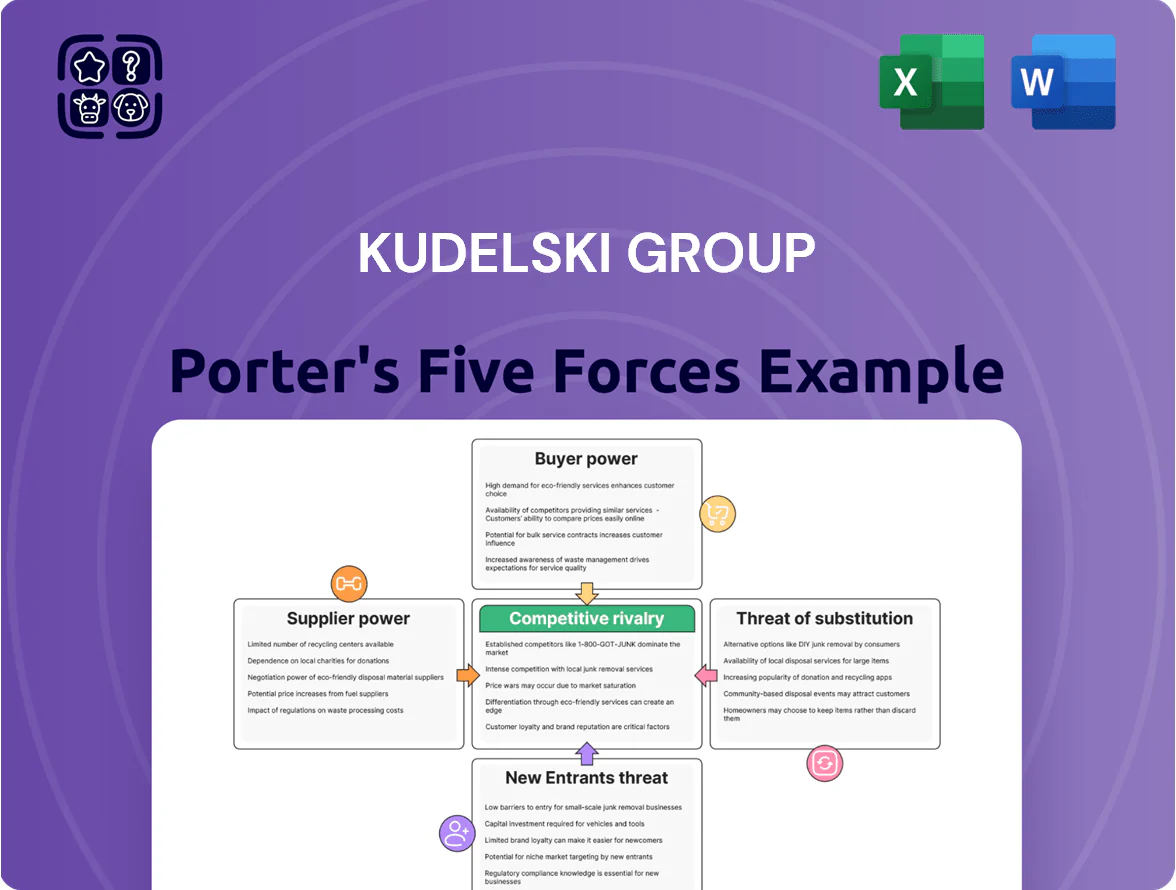

Kudelski Group operates at the intersection of cybersecurity, digital TV and IoT, facing moderate supplier power, high buyer expectations for integrated solutions, strong rivalry from tech incumbents and niche specialists, a tangible threat from new platform entrants, and substitution risks from software-only security providers; strategic differentiation and scalable SaaS offerings are critical. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kudelski Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor Manufacturers

The Group depends on high-end chipmakers for secure elements and hardware modules in conditional access systems, and only a handful of fabs—TSMC, Samsung, GlobalFoundries—can meet required nodes, giving suppliers strong leverage. In 2024 global semiconductor revenue hit $614 billion (SEMI), and foundry utilization averaged >80%, so supply tightness and price hikes can raise Kudelski hardware costs and compress gross margins. A single-month fab outage can delay deliveries by 6–12 weeks, increasing working capital and risking service SLAs.

Cloud Infrastructure Providers

As Kudelski shifts services to cloud, reliance on Amazon Web Services and Microsoft Azure rises; AWS and Azure together held ~62% of global cloud IaaS/PaaS market in 2024, strengthening supplier power.

These providers set pricing and SLAs for the infrastructure hosting Kudelski’s cybersecurity and media platforms, influencing margins and contract terms.

High switching costs for moving petabytes and integrated services—migration often >$1M and months of downtime—further tilt leverage to the cloud giants.

High-Skilled Cybersecurity Talent

The supply of specialized engineers and security researchers is a bottleneck for Kudelski Group; demand from cloud, AI and finance firms pushed global cybersecurity vacancy rates to 3.5M in 2024, keeping talent scarce.

High demand creates a seller’s market, lifting median cybersecurity salaries 18% YoY to about $130k in 2024, which raised Kudelski’s personnel costs and gross margin pressure.

Kudelski competes directly with FAANG and cloud providers for the same specialists, so human capital acts as a supplier group that materially influences operating expenses and service capacity.

Third-Party Software and IP Licensors

Integrating third-party software and IP is critical for Kudelski Group’s media and security products; many licensors hold patents or proprietary code that require product redesigns if removed, creating high switching costs.

That dependency lets IP suppliers demand favorable licensing fees or royalties; Kudelski reported 2024 R&D spend EUR 93.6m, so even 1–3% royalty shifts materially affect margins.

- High switching cost: proprietary IP

- Licensors hold essential patents

- Royalty sensitivity: 1–3% margin impact

- Convergent media increases leverage

Logistics and Distribution Partners

Kudelski relies on global logistics firms for physical access-control and IoT hardware; in 2024 global air freight rates rose ~12% year-over-year and container shipping spot rates spiked intermittently, letting carriers pass costs to clients.

Energy-price swings and rerouted lanes after 2022–23 geopolitical events give logistics partners leverage to raise fees; timely delivery is critical for SLAs, so these suppliers hold moderate bargaining power over operational reliability.

- 2024 air freight +12% yoy

- Container spot volatility, peak surges in 2023–24

- Moderate supplier power due to SLA sensitivity

- Cost pass-through risk from fuel/geopolitics

Supplier squeeze: foundries, cloud duopoly, cyber talent shortage and rising logistics

Suppliers hold strong power: few advanced foundries (TSMC, Samsung, GF) and 2024 semiconductor revenue $614B with >80% foundry utilization raise hardware costs; AWS+Azure ~62% IaaS/PaaS share increases cloud vendor leverage; cybersecurity talent shortfall 3.5M vacancies and median pay ~$130k lift personnel costs; IP royalties (1–3%) and 2024 air freight +12% further pressure margins.

| Supplier | Key stat (2024) |

|---|---|

| Foundries | $614B semis; >80% util |

| Cloud (AWS+Azure) | ~62% IaaS/PaaS |

| Cyber talent | 3.5M vacancies; median $130k |

| Logistics | Air freight +12% YoY |

What is included in the product

Tailored exclusively for Kudelski Group, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its pricing power and long-term profitability.

A concise Porter's Five Forces snapshot for Kudelski Group—quickly visualize competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Consolidation of Pay-TV and Media Operators

The wave of mergers—eg, 2024’s completion of Comcast-Charter deals and DISH’s partnerships—has concentrated pay-TV buyers into a few giants that negotiate heavy volume discounts; top 10 global operators now account for ~45% of pay-TV subscriptions, letting them demand price cuts and bespoke features.

For Kudelski Group a single global operator contract can equal double-digit percent of annual revenue (Kudelski reported CHF 640m revenue in 2024), so losing one large client would materially hit margins and cash flow.

Low Switching Costs for Software-Based Security

As security shifts to software and DRM, switching costs fall: software-only integrations let large streamers swap vendors with weeks of engineering work versus months for hardware, raising customer bargaining power. For example, Netflix and Amazon Prime manage multi-vendor security stacks and can reallocate ~1–3% of CV spend to test alternatives, so Kudelski must match competitors on price and show measurable ROI to defend contracts.

In-House Development Capabilities

Large tech and media firms (eg, Google, Meta) spent an estimated $55–65B on cybersecurity in 2024, with many building internal platforms to cut vendor spend; that gives them strong leverage to threaten insourcing and negotiate lower fees from vendors like Kudelski Group.

To counter this, Kudelski must sell niche, high-complexity services—cryptographic key management, DRM for pay-TV, and embedded security modules—that clients report would cost 30–50% more to replicate internally and delay time-to-market by 12–18 months.

IoT Device Manufacturers and Ecosystems

IoT device makers run on thin margins and treat security as a cost; many will choose cheaper or embedded options rather than premium services, boosting buyer leverage. In 2024, global IoT device shipments reached ~14.6 billion units and average OEM security spend per device stayed below $1, so scale buying power pressures prices. If perceived risk is low, switching to lower-cost vendors or basic firmware security is common, increasing bargaining strength.

- 14.6B IoT units shipped (2024)

- OEM security spend < $1/device (avg, 2024)

- Wide vendor choice raises price competition

- Perceived low risk → preference for basic security

Government and Public Sector Procurement

Kudelski’s public-sector work (defense, infrastructure) ties it to rigid, competitive government tenders where agencies set compliance rules and long-term price ceilings; for 2024 Kudelski reported 22% of revenue from public contracts, magnifying customer leverage. Bureaucratic budget cycles and regulatory oversight give governments bargaining power via multi-year procurements, specification control, and slow renegotiation, raising margin pressure and contract concentration risk.

- 22% revenue from public contracts (2024)

- Competitive tenders raise price pressure

- Governments set compliance and long-term caps

- Budget cycles enable regulatory leverage

Buyer concentration and low‑cost DRM threaten Kudelski’s revenue and increase churn

Buyers are highly concentrated (top 10 pay‑TV operators ≈45% subscriptions) and can demand discounts; single global contracts can equal double‑digit % of Kudelski’s CHF 640m 2024 revenue, raising churn risk. Software DRM lowers switching costs (weeks vs months), while Big Tech’s $55–65B cybersecurity spend in 2024 enables insourcing. Public tenders (22% revenue) and low‑margin IoT ($1/device avg spend; 14.6B units) further boost buyer leverage.

| Metric | 2024 |

|---|---|

| Revenue (Kudelski) | CHF 640m |

| Top‑10 pay‑TV share | ≈45% |

| Public contracts % | 22% |

| IoT units shipped | 14.6B |

| OEM security spend/device | < $1 |

| Big Tech cyber spend | $55–65B |

Preview Before You Purchase

Kudelski Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of the Kudelski Group you'll receive immediately after purchase—no surprises, no placeholders; it covers supplier power, buyer power, competitive rivalry, threat of new entrants, and threat of substitutes with sector-specific evidence and implications.

The document displayed here is the part of the full version you’ll get—fully formatted, ready to download, and includes concise strategic recommendations and risk considerations tailored to Kudelski's digital security and content protection businesses.

You're looking at the actual deliverable; once you complete your purchase, you’ll get instant access to this exact file for immediate use in decision-making, presentations, or further analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Kudelski Group operates at the intersection of cybersecurity, digital TV and IoT, facing moderate supplier power, high buyer expectations for integrated solutions, strong rivalry from tech incumbents and niche specialists, a tangible threat from new platform entrants, and substitution risks from software-only security providers; strategic differentiation and scalable SaaS offerings are critical. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kudelski Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor Manufacturers

The Group depends on high-end chipmakers for secure elements and hardware modules in conditional access systems, and only a handful of fabs—TSMC, Samsung, GlobalFoundries—can meet required nodes, giving suppliers strong leverage. In 2024 global semiconductor revenue hit $614 billion (SEMI), and foundry utilization averaged >80%, so supply tightness and price hikes can raise Kudelski hardware costs and compress gross margins. A single-month fab outage can delay deliveries by 6–12 weeks, increasing working capital and risking service SLAs.

Cloud Infrastructure Providers

As Kudelski shifts services to cloud, reliance on Amazon Web Services and Microsoft Azure rises; AWS and Azure together held ~62% of global cloud IaaS/PaaS market in 2024, strengthening supplier power.

These providers set pricing and SLAs for the infrastructure hosting Kudelski’s cybersecurity and media platforms, influencing margins and contract terms.

High switching costs for moving petabytes and integrated services—migration often >$1M and months of downtime—further tilt leverage to the cloud giants.

High-Skilled Cybersecurity Talent

The supply of specialized engineers and security researchers is a bottleneck for Kudelski Group; demand from cloud, AI and finance firms pushed global cybersecurity vacancy rates to 3.5M in 2024, keeping talent scarce.

High demand creates a seller’s market, lifting median cybersecurity salaries 18% YoY to about $130k in 2024, which raised Kudelski’s personnel costs and gross margin pressure.

Kudelski competes directly with FAANG and cloud providers for the same specialists, so human capital acts as a supplier group that materially influences operating expenses and service capacity.

Third-Party Software and IP Licensors

Integrating third-party software and IP is critical for Kudelski Group’s media and security products; many licensors hold patents or proprietary code that require product redesigns if removed, creating high switching costs.

That dependency lets IP suppliers demand favorable licensing fees or royalties; Kudelski reported 2024 R&D spend EUR 93.6m, so even 1–3% royalty shifts materially affect margins.

- High switching cost: proprietary IP

- Licensors hold essential patents

- Royalty sensitivity: 1–3% margin impact

- Convergent media increases leverage

Logistics and Distribution Partners

Kudelski relies on global logistics firms for physical access-control and IoT hardware; in 2024 global air freight rates rose ~12% year-over-year and container shipping spot rates spiked intermittently, letting carriers pass costs to clients.

Energy-price swings and rerouted lanes after 2022–23 geopolitical events give logistics partners leverage to raise fees; timely delivery is critical for SLAs, so these suppliers hold moderate bargaining power over operational reliability.

- 2024 air freight +12% yoy

- Container spot volatility, peak surges in 2023–24

- Moderate supplier power due to SLA sensitivity

- Cost pass-through risk from fuel/geopolitics

Supplier squeeze: foundries, cloud duopoly, cyber talent shortage and rising logistics

Suppliers hold strong power: few advanced foundries (TSMC, Samsung, GF) and 2024 semiconductor revenue $614B with >80% foundry utilization raise hardware costs; AWS+Azure ~62% IaaS/PaaS share increases cloud vendor leverage; cybersecurity talent shortfall 3.5M vacancies and median pay ~$130k lift personnel costs; IP royalties (1–3%) and 2024 air freight +12% further pressure margins.

| Supplier | Key stat (2024) |

|---|---|

| Foundries | $614B semis; >80% util |

| Cloud (AWS+Azure) | ~62% IaaS/PaaS |

| Cyber talent | 3.5M vacancies; median $130k |

| Logistics | Air freight +12% YoY |

What is included in the product

Tailored exclusively for Kudelski Group, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its pricing power and long-term profitability.

A concise Porter's Five Forces snapshot for Kudelski Group—quickly visualize competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Consolidation of Pay-TV and Media Operators

The wave of mergers—eg, 2024’s completion of Comcast-Charter deals and DISH’s partnerships—has concentrated pay-TV buyers into a few giants that negotiate heavy volume discounts; top 10 global operators now account for ~45% of pay-TV subscriptions, letting them demand price cuts and bespoke features.

For Kudelski Group a single global operator contract can equal double-digit percent of annual revenue (Kudelski reported CHF 640m revenue in 2024), so losing one large client would materially hit margins and cash flow.

Low Switching Costs for Software-Based Security

As security shifts to software and DRM, switching costs fall: software-only integrations let large streamers swap vendors with weeks of engineering work versus months for hardware, raising customer bargaining power. For example, Netflix and Amazon Prime manage multi-vendor security stacks and can reallocate ~1–3% of CV spend to test alternatives, so Kudelski must match competitors on price and show measurable ROI to defend contracts.

In-House Development Capabilities

Large tech and media firms (eg, Google, Meta) spent an estimated $55–65B on cybersecurity in 2024, with many building internal platforms to cut vendor spend; that gives them strong leverage to threaten insourcing and negotiate lower fees from vendors like Kudelski Group.

To counter this, Kudelski must sell niche, high-complexity services—cryptographic key management, DRM for pay-TV, and embedded security modules—that clients report would cost 30–50% more to replicate internally and delay time-to-market by 12–18 months.

IoT Device Manufacturers and Ecosystems

IoT device makers run on thin margins and treat security as a cost; many will choose cheaper or embedded options rather than premium services, boosting buyer leverage. In 2024, global IoT device shipments reached ~14.6 billion units and average OEM security spend per device stayed below $1, so scale buying power pressures prices. If perceived risk is low, switching to lower-cost vendors or basic firmware security is common, increasing bargaining strength.

- 14.6B IoT units shipped (2024)

- OEM security spend < $1/device (avg, 2024)

- Wide vendor choice raises price competition

- Perceived low risk → preference for basic security

Government and Public Sector Procurement

Kudelski’s public-sector work (defense, infrastructure) ties it to rigid, competitive government tenders where agencies set compliance rules and long-term price ceilings; for 2024 Kudelski reported 22% of revenue from public contracts, magnifying customer leverage. Bureaucratic budget cycles and regulatory oversight give governments bargaining power via multi-year procurements, specification control, and slow renegotiation, raising margin pressure and contract concentration risk.

- 22% revenue from public contracts (2024)

- Competitive tenders raise price pressure

- Governments set compliance and long-term caps

- Budget cycles enable regulatory leverage

Buyer concentration and low‑cost DRM threaten Kudelski’s revenue and increase churn

Buyers are highly concentrated (top 10 pay‑TV operators ≈45% subscriptions) and can demand discounts; single global contracts can equal double‑digit % of Kudelski’s CHF 640m 2024 revenue, raising churn risk. Software DRM lowers switching costs (weeks vs months), while Big Tech’s $55–65B cybersecurity spend in 2024 enables insourcing. Public tenders (22% revenue) and low‑margin IoT ($1/device avg spend; 14.6B units) further boost buyer leverage.

| Metric | 2024 |

|---|---|

| Revenue (Kudelski) | CHF 640m |

| Top‑10 pay‑TV share | ≈45% |

| Public contracts % | 22% |

| IoT units shipped | 14.6B |

| OEM security spend/device | < $1 |

| Big Tech cyber spend | $55–65B |

Preview Before You Purchase

Kudelski Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of the Kudelski Group you'll receive immediately after purchase—no surprises, no placeholders; it covers supplier power, buyer power, competitive rivalry, threat of new entrants, and threat of substitutes with sector-specific evidence and implications.

The document displayed here is the part of the full version you’ll get—fully formatted, ready to download, and includes concise strategic recommendations and risk considerations tailored to Kudelski's digital security and content protection businesses.

You're looking at the actual deliverable; once you complete your purchase, you’ll get instant access to this exact file for immediate use in decision-making, presentations, or further analysis.