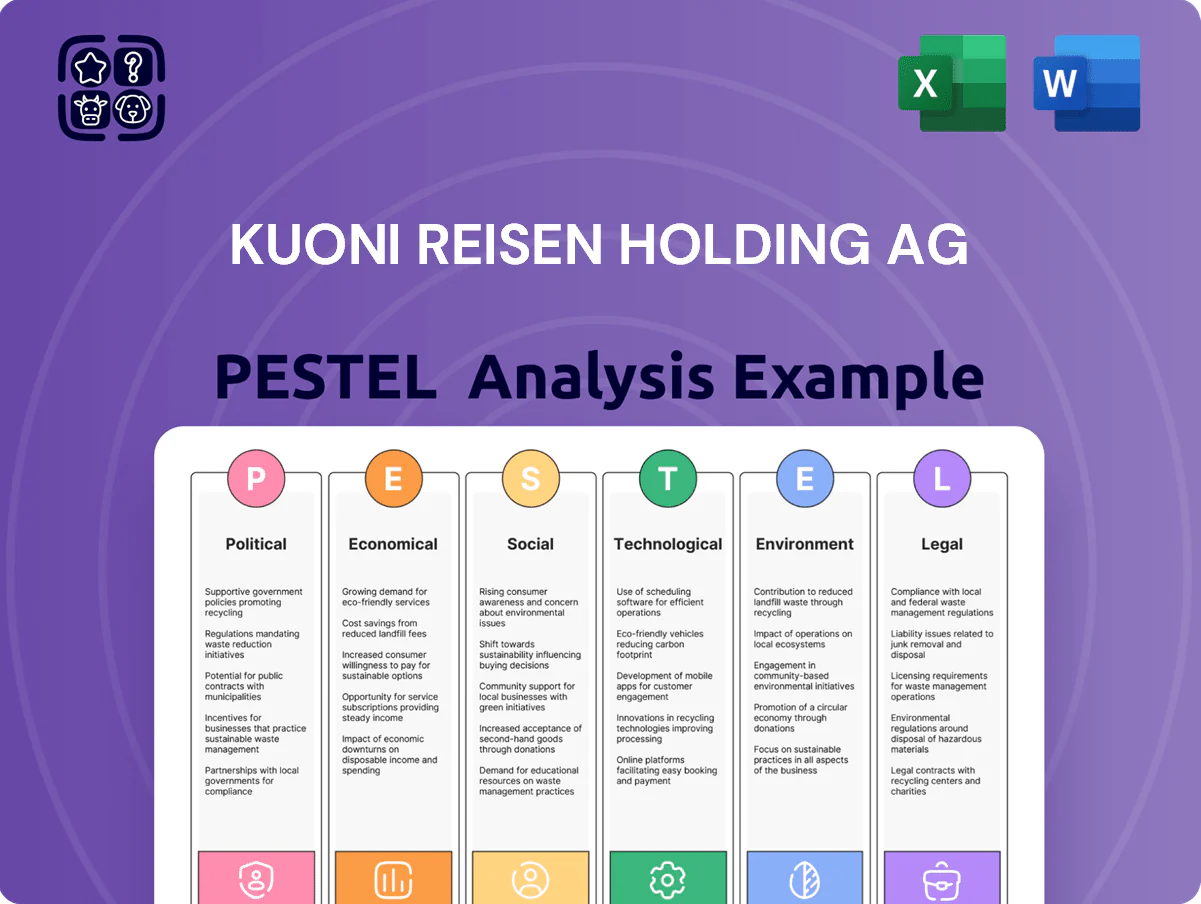

Kuoni Reisen Holding AG PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological disruption are reshaping Kuoni Reisen Holding AG’s prospects—our concise PESTLE snapshot highlights the critical external drivers you need to know.

Ready-made for investors and strategists, the full PESTLE delivers detailed risk assessments and growth levers to inform decisions—purchase now to download the complete, actionable report.

Political factors

Geopolitical Stability in Key Markets

Political stability in Kuoni’s top luxury destinations—Switzerland, UAE, Maldives and Italy—directly affects safety and demand; 2024–25 travel advisories rose 18% globally, increasing itinerary changes for luxury operators by 12% year-over-year.

Regional conflicts and diplomatic shifts (e.g., Red Sea tensions, 2024 Gaza escalation) forced route diversions that added average per-trip costs of $320 for luxury tours in 2025.

Strategic planning must model volatility: between 2023–2025 sudden border closures increased cancellation rates by 9%, so Kuoni should stress-test scenarios against updated 2025 advisory data to limit revenue shocks.

Visa Liberalization Policies

Visa liberalization in 2024–25 has cut entry barriers: ASEAN e-visa uptake rose 28% YoY and UAE visa waivers expanded to 85 countries, easing transit for Kuoni’s luxury clients and boosting bookings to those hubs; reciprocal EU-Asia/MENA agreements (eg. recent Schengen facilitation talks with India targeting 10% travel growth) shift destination popularity; monitoring these legislative changes lets Kuoni reallocate marketing spend toward low-friction markets to maximize yield and occupancy.

Government Tourism Subsidies and Support

Post-pandemic tourism recovery morphed into sustained government support for upscale sustainable travel, with OECD reporting tourism-related fiscal measures totaling about USD 200 billion globally in 2023–24; Kuoni can tap these funds via public-private partnerships to scale destination management and ESG-certified product lines.

Yet IMF fiscal tightening forecasts for 2025–26 indicate many EU and LATAM governments may cut discretionary tourism subsidies by up to 10–15%, which would raise operational costs for travel providers and pressure margins for Kuoni’s subsidized programs.

Trade Agreements Affecting Aviation

International trade deals and open-skies agreements shape route access and costs for Kuoni Reisen Holding AG’s premium packages; ICAO data shows international scheduled services carried 4.4 billion passengers in 2024, impacting capacity and fares on long-haul sectors critical to luxury itineraries.

Revisions to agreements can push ticket prices ±10–20% on affected routes and reduce direct long-haul options, forcing rerouting or higher-stop itineraries that affect product appeal for high-net-worth clients.

Monitoring trade negotiations enabled travel firms to secure lower block-seat rates and better logistics; in 2024 negotiated partnerships reduced average premium-class procurement costs by ~8% for some tour operators.

- 4.4 billion international passengers (2024)

- Ticket price swings on reopened/restricted routes: ±10–20%

- Average premium-class procurement savings via negotiated deals: ~8% (2024)

Regulatory Influence on Global Alliances

The tightening political environment constrains cross-border mergers for Kuoni Reisen Holding AG, with EU antitrust fines totaling EUR 6.5bn in 2024 signaling stricter merger scrutiny across travel and hospitality sectors.

Nationalistic policies in key markets (e.g., 2025 protection measures in India and Brazil) could block acquisitions, limiting Kuoni’s inorganic growth options and raising integration costs by an estimated 8–12%.

Effective expansion requires local legal expertise and monitoring of competition law shifts; failure to comply risks fines and blocked deals that would dent FY2025 revenue targets.

- EU antitrust enforcement: EUR 6.5bn fines in 2024

- Protectionist moves in India/Brazil (2025) affect deal access

- Estimated 8–12% increase in integration costs under restrictive regimes

Geopolitical shocks lift travel costs, boost visas & stimulus, squeeze M&A

Political risks—rising travel advisories (+18% in 2024–25) and regional conflicts (route diversions adding ~$320/trip in 2025)—increase costs and cancellations (+9% 2023–25), while visa liberalization (ASEAN e-visas +28% YoY; UAE waivers to 85 countries) and public tourism stimulus (~USD 200bn global 2023–24) create demand shifts; EU antitrust fines €6.5bn (2024) and protectionism (India/Brazil 2025) raise M&A barriers.

| Metric | Value |

|---|---|

| Travel advisories | +18% (2024–25) |

| Route diversion cost | $320 avg (2025) |

| Cancellations | +9% (2023–25) |

| ASEAN e-visa uptake | +28% YoY (2024) |

| Tourism stimulus | ~$200bn (2023–24) |

| EU antitrust fines | €6.5bn (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Kuoni Reisen Holding AG, offering data-backed insights and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses tailored to the travel and tourism sector.

A concise PESTLE snapshot for Kuoni Reisen Holding AG, organized by category for quick reference in presentations, enabling teams to assess external risks and market positioning rapidly and add context-specific notes for strategic planning.

Economic factors

Currency Volatility and Exchange Rates

Fluctuations between the Swiss franc, euro and US dollar materially affect Kuoni Reisen Holding AG’s pricing power; a 5% CHF appreciation vs EUR in 2024 raised package costs for Eurozone customers, eroding competitiveness.

Exchange-rate swings compress margins on cross-border operations and raised international destination management costs by an estimated 2–3% in 2023–24 for similar peers.

By end-2025 heightened FX volatility—USD/EUR swings >8% YTD—makes financial hedging essential; forward contracts and natural hedges reduced FX losses by up to 60% in 2024 for travel firms.

Inflationary Pressures on Luxury Services

Persistent inflation in hospitality and aviation has raised base costs for luxury travel; global airline fuel costs rose ~35% in 2024 vs 2022 and hotel operating costs increased ~8–10% in 2023–24, pressuring Kuoni Reisen Holding AG’s margins.

Kuoni’s affluent clientele shows price resilience—lux travel spending among HNW households rose ~6% in 2024—but extreme inflation can shift demand to shorter or domestic trips.

Balancing premium pricing with clear value delivery is critical as input cost inflation risks eroding bookings if perceived value falls, forcing careful yield management and cost-pass-through strategies.

Global Wealth Distribution Trends

Rising ultra-high-net-worth individuals (UHNWIs) in emerging markets—UHNW population in Asia grew 27% from 2019–2024 to ~310,000 and Middle East wealth up ~18% over same period—opens major demand for Kuoni’s bespoke travel. Southeast Asia’s luxury travel spend reached an estimated $45–50 billion in 2024, signaling high-yield segments. Tailoring offerings to local spending patterns and tax/legal preferences of these wealth clusters is essential for sustained revenue growth.

Interest Rate Impact on Capital Expenditure

The 2024 Swiss policy rate at 1.75% and average corporate borrowing costs rising ~120 bps vs 2021 increase financing costs for Kuoni Reisen Holding AG’s infrastructure and digital projects, potentially delaying upgrades or luxury property expansion.

Higher rates push management to prioritize projects with IRRs above current WACC (~7–9% for similar travel groups in 2024) to protect margins and preserve liquidity amid volatile credit conditions.

- 2024 Swiss policy rate 1.75%

- Corporate borrowing +120 bps vs 2021

- Target project IRR >7–9%

Labor Market Shortages in Hospitality

- 2024 Swiss vacancy rate ~12%

- EU hospitality wage growth ~6.5% YoY (2024)

- Turnover cost ≈20–30% of salary

FX shocks, rising costs & UHNW shifts force hedging and high‑IRR focus

FX volatility, with CHF up ~5% vs EUR in 2024 and USD/EUR swings >8% YTD in 2025, eroded pricing and made hedging essential; forwards cut FX losses up to 60% in 2024. Inflation raised airline fuel ~35% (2022–24) and hotel costs ~8–10%, squeezing margins despite ~6% luxury spend growth among HNW households in 2024. Rising UHNW in Asia (+27% 2019–24) and higher borrowing costs (+120 bps vs 2021; Swiss policy rate 1.75% 2024) shift capital allocation toward high-IRR projects.

| Metric | Value |

|---|---|

| CHF vs EUR (2024) | +5% |

| USD/EUR volatility (YTD 2025) | >8% |

| Airline fuel (2022–24) | +35% |

| Hotel costs (2023–24) | +8–10% |

| Luxury spend HNW (2024) | +6% |

| Asia UHNW growth (2019–24) | +27% |

| Swiss policy rate (2024) | 1.75% |

| Corporate borrowing vs 2021 | +120 bps |

Full Version Awaits

Kuoni Reisen Holding AG PESTLE Analysis

The preview shown here is the exact Kuoni Reisen Holding AG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and technological disruption are reshaping Kuoni Reisen Holding AG’s prospects—our concise PESTLE snapshot highlights the critical external drivers you need to know.

Ready-made for investors and strategists, the full PESTLE delivers detailed risk assessments and growth levers to inform decisions—purchase now to download the complete, actionable report.

Political factors

Geopolitical Stability in Key Markets

Political stability in Kuoni’s top luxury destinations—Switzerland, UAE, Maldives and Italy—directly affects safety and demand; 2024–25 travel advisories rose 18% globally, increasing itinerary changes for luxury operators by 12% year-over-year.

Regional conflicts and diplomatic shifts (e.g., Red Sea tensions, 2024 Gaza escalation) forced route diversions that added average per-trip costs of $320 for luxury tours in 2025.

Strategic planning must model volatility: between 2023–2025 sudden border closures increased cancellation rates by 9%, so Kuoni should stress-test scenarios against updated 2025 advisory data to limit revenue shocks.

Visa Liberalization Policies

Visa liberalization in 2024–25 has cut entry barriers: ASEAN e-visa uptake rose 28% YoY and UAE visa waivers expanded to 85 countries, easing transit for Kuoni’s luxury clients and boosting bookings to those hubs; reciprocal EU-Asia/MENA agreements (eg. recent Schengen facilitation talks with India targeting 10% travel growth) shift destination popularity; monitoring these legislative changes lets Kuoni reallocate marketing spend toward low-friction markets to maximize yield and occupancy.

Government Tourism Subsidies and Support

Post-pandemic tourism recovery morphed into sustained government support for upscale sustainable travel, with OECD reporting tourism-related fiscal measures totaling about USD 200 billion globally in 2023–24; Kuoni can tap these funds via public-private partnerships to scale destination management and ESG-certified product lines.

Yet IMF fiscal tightening forecasts for 2025–26 indicate many EU and LATAM governments may cut discretionary tourism subsidies by up to 10–15%, which would raise operational costs for travel providers and pressure margins for Kuoni’s subsidized programs.

Trade Agreements Affecting Aviation

International trade deals and open-skies agreements shape route access and costs for Kuoni Reisen Holding AG’s premium packages; ICAO data shows international scheduled services carried 4.4 billion passengers in 2024, impacting capacity and fares on long-haul sectors critical to luxury itineraries.

Revisions to agreements can push ticket prices ±10–20% on affected routes and reduce direct long-haul options, forcing rerouting or higher-stop itineraries that affect product appeal for high-net-worth clients.

Monitoring trade negotiations enabled travel firms to secure lower block-seat rates and better logistics; in 2024 negotiated partnerships reduced average premium-class procurement costs by ~8% for some tour operators.

- 4.4 billion international passengers (2024)

- Ticket price swings on reopened/restricted routes: ±10–20%

- Average premium-class procurement savings via negotiated deals: ~8% (2024)

Regulatory Influence on Global Alliances

The tightening political environment constrains cross-border mergers for Kuoni Reisen Holding AG, with EU antitrust fines totaling EUR 6.5bn in 2024 signaling stricter merger scrutiny across travel and hospitality sectors.

Nationalistic policies in key markets (e.g., 2025 protection measures in India and Brazil) could block acquisitions, limiting Kuoni’s inorganic growth options and raising integration costs by an estimated 8–12%.

Effective expansion requires local legal expertise and monitoring of competition law shifts; failure to comply risks fines and blocked deals that would dent FY2025 revenue targets.

- EU antitrust enforcement: EUR 6.5bn fines in 2024

- Protectionist moves in India/Brazil (2025) affect deal access

- Estimated 8–12% increase in integration costs under restrictive regimes

Geopolitical shocks lift travel costs, boost visas & stimulus, squeeze M&A

Political risks—rising travel advisories (+18% in 2024–25) and regional conflicts (route diversions adding ~$320/trip in 2025)—increase costs and cancellations (+9% 2023–25), while visa liberalization (ASEAN e-visas +28% YoY; UAE waivers to 85 countries) and public tourism stimulus (~USD 200bn global 2023–24) create demand shifts; EU antitrust fines €6.5bn (2024) and protectionism (India/Brazil 2025) raise M&A barriers.

| Metric | Value |

|---|---|

| Travel advisories | +18% (2024–25) |

| Route diversion cost | $320 avg (2025) |

| Cancellations | +9% (2023–25) |

| ASEAN e-visa uptake | +28% YoY (2024) |

| Tourism stimulus | ~$200bn (2023–24) |

| EU antitrust fines | €6.5bn (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Kuoni Reisen Holding AG, offering data-backed insights and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses tailored to the travel and tourism sector.

A concise PESTLE snapshot for Kuoni Reisen Holding AG, organized by category for quick reference in presentations, enabling teams to assess external risks and market positioning rapidly and add context-specific notes for strategic planning.

Economic factors

Currency Volatility and Exchange Rates

Fluctuations between the Swiss franc, euro and US dollar materially affect Kuoni Reisen Holding AG’s pricing power; a 5% CHF appreciation vs EUR in 2024 raised package costs for Eurozone customers, eroding competitiveness.

Exchange-rate swings compress margins on cross-border operations and raised international destination management costs by an estimated 2–3% in 2023–24 for similar peers.

By end-2025 heightened FX volatility—USD/EUR swings >8% YTD—makes financial hedging essential; forward contracts and natural hedges reduced FX losses by up to 60% in 2024 for travel firms.

Inflationary Pressures on Luxury Services

Persistent inflation in hospitality and aviation has raised base costs for luxury travel; global airline fuel costs rose ~35% in 2024 vs 2022 and hotel operating costs increased ~8–10% in 2023–24, pressuring Kuoni Reisen Holding AG’s margins.

Kuoni’s affluent clientele shows price resilience—lux travel spending among HNW households rose ~6% in 2024—but extreme inflation can shift demand to shorter or domestic trips.

Balancing premium pricing with clear value delivery is critical as input cost inflation risks eroding bookings if perceived value falls, forcing careful yield management and cost-pass-through strategies.

Global Wealth Distribution Trends

Rising ultra-high-net-worth individuals (UHNWIs) in emerging markets—UHNW population in Asia grew 27% from 2019–2024 to ~310,000 and Middle East wealth up ~18% over same period—opens major demand for Kuoni’s bespoke travel. Southeast Asia’s luxury travel spend reached an estimated $45–50 billion in 2024, signaling high-yield segments. Tailoring offerings to local spending patterns and tax/legal preferences of these wealth clusters is essential for sustained revenue growth.

Interest Rate Impact on Capital Expenditure

The 2024 Swiss policy rate at 1.75% and average corporate borrowing costs rising ~120 bps vs 2021 increase financing costs for Kuoni Reisen Holding AG’s infrastructure and digital projects, potentially delaying upgrades or luxury property expansion.

Higher rates push management to prioritize projects with IRRs above current WACC (~7–9% for similar travel groups in 2024) to protect margins and preserve liquidity amid volatile credit conditions.

- 2024 Swiss policy rate 1.75%

- Corporate borrowing +120 bps vs 2021

- Target project IRR >7–9%

Labor Market Shortages in Hospitality

- 2024 Swiss vacancy rate ~12%

- EU hospitality wage growth ~6.5% YoY (2024)

- Turnover cost ≈20–30% of salary

FX shocks, rising costs & UHNW shifts force hedging and high‑IRR focus

FX volatility, with CHF up ~5% vs EUR in 2024 and USD/EUR swings >8% YTD in 2025, eroded pricing and made hedging essential; forwards cut FX losses up to 60% in 2024. Inflation raised airline fuel ~35% (2022–24) and hotel costs ~8–10%, squeezing margins despite ~6% luxury spend growth among HNW households in 2024. Rising UHNW in Asia (+27% 2019–24) and higher borrowing costs (+120 bps vs 2021; Swiss policy rate 1.75% 2024) shift capital allocation toward high-IRR projects.

| Metric | Value |

|---|---|

| CHF vs EUR (2024) | +5% |

| USD/EUR volatility (YTD 2025) | >8% |

| Airline fuel (2022–24) | +35% |

| Hotel costs (2023–24) | +8–10% |

| Luxury spend HNW (2024) | +6% |

| Asia UHNW growth (2019–24) | +27% |

| Swiss policy rate (2024) | 1.75% |

| Corporate borrowing vs 2021 | +120 bps |

Full Version Awaits

Kuoni Reisen Holding AG PESTLE Analysis

The preview shown here is the exact Kuoni Reisen Holding AG PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.