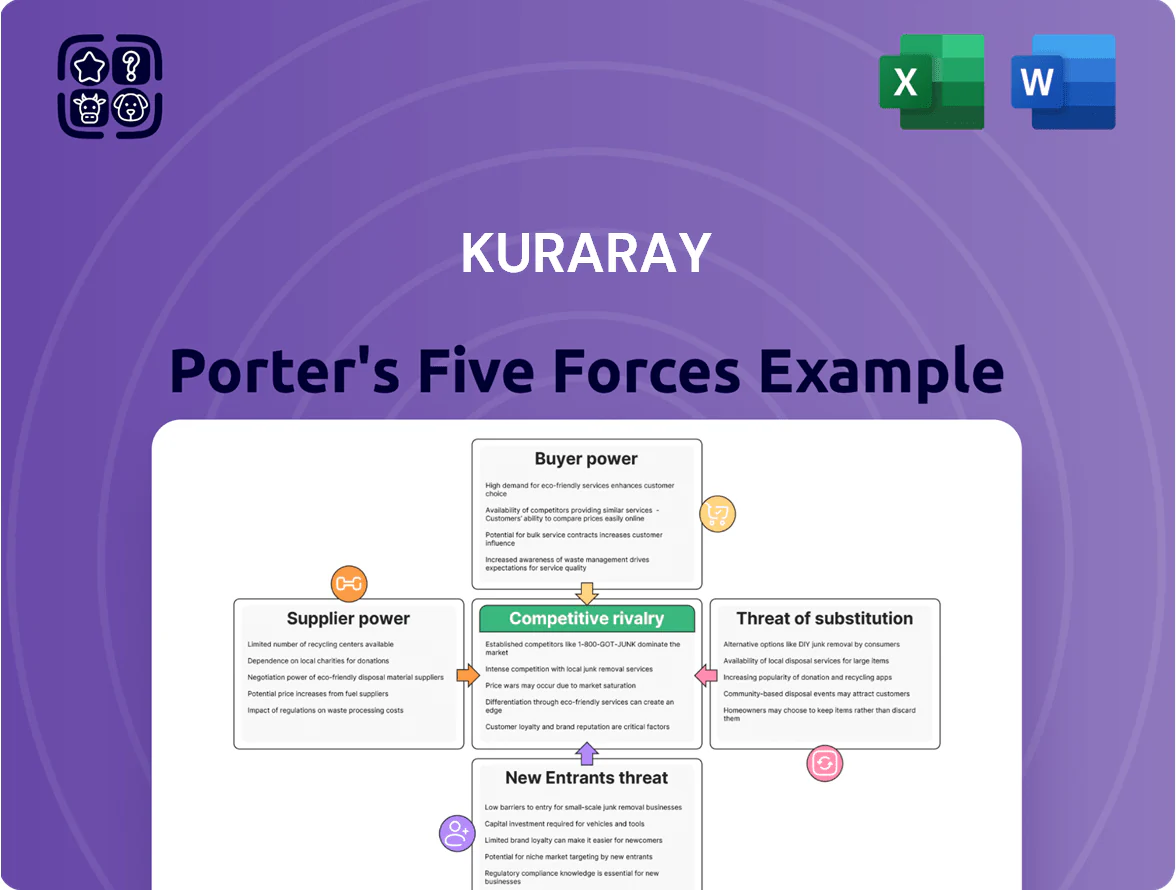

Kuraray Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Kuraray faces moderate supplier power, steady buyer demands, and niche substitute threats driven by specialty polymers and sustainable materials—factors shaping margins and strategic moves.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kuraray’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Kuraray depends on feedstocks like ethylene and vinyl acetate monomer, whose prices rose ~28% YoY in 2024 and remained volatile into 2025 due to geopolitical shifts and energy-transition policies that tightened petroleum supply.

By end-2025 benchmark naphtha-linked ethylene costs averaged ~$950/ton, forcing Kuraray to use long-term supply contracts and commodity hedges; without these, a 10% upstream spike would cut EBITDA margin by roughly 150–200 basis points.

Concentration of petrochemical providers

The global supply of specialized chemical precursors for polymers is concentrated among a few petrochemical giants—Shell, BASF, and SABIC controlled roughly 40% of selected feedstocks in 2024—giving suppliers strong pricing and allocation leverage during shortages. Kuraray reduces this risk by sourcing from multiple regions (Japan, Southeast Asia, and the US), holding dual-sourcing contracts and safety stocks covering ~3 months of production to maintain continuity.

Energy and utility costs

Chemical manufacturing is energy intensive, with Kuraray using large electricity and natural gas volumes for high-temperature synthesis; industrial users in Japan paid about ¥23.5/kWh average electricity in 2024 and LNG spot-linked gas rose 18% YoY. Tightening carbon pricing and renewable mandates by late 2025 raise utility leverage over Kuraray’s margins. Kuraray is expanding on-site renewables—aiming for 30% self-generated power at key plants by 2026—to cut supplier dependency.

Logistics and transport availability

Specialized transport for chemicals needs certified carriers for hazardous and sensitive materials; in 2024, global chemical logistics capacity tightened with a 7% shortfall in tank-container availability versus demand, pushing spot rates up ~22% year-over-year.

Limited qualified trucking and shipping capacity raises Kuraray’s freight costs and delay risk; providers can demand premium terms because few alternatives meet safety and certification standards.

- Certified carriers required for hazardous loads

- 2024: ~7% tank-container capacity shortfall

- Spot rates +22% YoY in 2024

- Providers set terms in thin market

Limited substitutes for specific catalysts

Suppliers of niche catalysts for EVAL (ethylene vinyl alcohol) and PVA (polyvinyl alcohol) hold strong leverage because few direct substitutes exist; replacing inputs can force Kuraray to re-certify processes and customer approvals, adding time and cost. In 2024 Kuraray reported R&D and quality compliance expenses rising 8% YoY, reflecting this certification burden and supplier-driven risk. This technical lock-in raises supplier bargaining power and potential price pass-through.

- Few substitutes → high supplier leverage

- Process re-certification risk → added cost/time

- 2024: Kuraray compliance/R&D costs +8% YoY

- Specialty vendors can impose price/policy terms

Supplier squeeze lifts costs; Kuraray hedges, multi‑sourcing & renewables cut risk

Suppliers hold moderate–high power: concentrated feedstock/catalyst markets (Shell/BASF/SABIC ~40% share in 2024), naphtha-linked ethylene ~950$/t in 2025, 3 months safety stock, freight tightness (7% tank shortfall, spot rates +22% in 2024) and rising utilities (¥23.5/kWh in 2024) squeeze margins; Kuraray’s hedges, multi‑sourcing and 30% on-site renewables target lower supplier risk.

| Metric | 2024–25 |

|---|---|

| Ethylene price (avg) | ~950 $/t (end‑2025) |

| Feedstock concentration | Shell/BASF/SABIC ~40% |

| Safety stock | ~3 months |

| Tank capacity gap | −7% (2024) |

| Spot freight | +22% YoY (2024) |

| Electricity (Japan) | ¥23.5/kWh (2024) |

| On-site renewables goal | 30% by 2026 |

What is included in the product

Tailored exclusively for Kuraray, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, substitution threats, and entry barriers, highlighting disruptive forces and strategic levers that influence Kuraray’s pricing, margins, and market resilience.

A concise Porter's Five Forces snapshot for Kuraray—quickly assess supplier, buyer, competitor, new entrant, and substitute pressures to guide strategic moves.

Customers Bargaining Power

Concentration in the packaging industry

Switching costs for specialized polymers

Customers in automotive and medical sectors face high switching costs for Kuraray’s specialized polymers because regulatory re-validation often takes 12–24 months and can cost $0.5–$5M per component, per industry estimates in 2024. Once Kuraray’s material is integrated into a vehicle or device, qualifying an alternative requires lengthy testing, certification, and retooling, reducing buyers’ price leverage. This technical integration and compliance burden gives Kuraray measurable protection against customer bargaining power, sustaining higher margins—Kuraray’s specialty polymer segment reported ~18% operating margin in FY2024.

Demand for sustainable and circular solutions

Modern industrial buyers push Kuraray toward circular materials—recyclable or bio-based resins—raising customer bargaining power as 64% of global CPGs had public circularity targets by 2024 (Ellen MacArthur/BCG).

Clients now demand carbon-footprint transparency; 72% of procurement teams use Scope 1–3 data in supplier selection (2023 ISM survey), so Kuraray must report lifecycle emissions to stay preferred.

Kuraray’s R&D and CAPEX must shift: 2024 green-petrochemical investments rose 18% industrywide, or risk losing contracts to greener competitors.

Price sensitivity in commodity segments

In commodity segments like standard polyvinyl alcohol (PVA) and basic fibers, buyers face many global suppliers and high price sensitivity; spot PVA prices fell ~12% worldwide in 2024, pressuring margins across the industry.

Low product differentiation lets purchasers switch to the lowest-cost provider, compressing EBITDA margins for commoditized lines (industry average ~6–8% in 2024).

Kuraray mitigates this by shifting sales mix to specialty grades—e.g., high-strength PVA and functionalized fibers—where contracts, performance specs, and after-sales support raise customer stickiness and sustain higher margins (~15–22%).

- Commoditized PVA: many suppliers, price-driven

- 2024 spot PVA: ~12% price decline

- Commodity EBITDA: ~6–8%

- Specialty grades EBITDA: ~15–22%

- Kuraray strategy: focus on performance-led, contract-based sales

Requirements for technical support and co-development

Sophisticated customers demand extensive technical support and co-development, so Kuraray embeds engineers into client design teams to tailor polymers and elastomers, lowering price-only switching—industrial clients report 30–40% faster time-to-market with such partnerships (2024 supplier surveys).

This service-based dependency raises switching costs and preserves margins: co-development projects often add 5–12% ASP (average selling price) premium and recur in multi-year supply contracts, reducing pure bargaining leverage.

- Embedded engineers: reduces switching

- 30–40% faster time-to-market (2024)

- 5–12% ASP premium on co-dev projects

- Multi-year contracts stabilize margins

Concentrated EVOH buyers boost bargaining power; specialty margins & switching costs cap risk

| Metric | 2024–25 |

|---|---|

| EVOH demand share | 40–50% |

| Buyer consolidation | −20% |

| Switching cost | $0.5–$5M;12–24m |

| Commodity EBITDA | 6–8% |

| Specialty EBITDA | 15–22% |

Full Version Awaits

Kuraray Porter's Five Forces Analysis

This preview shows the exact Kuraray Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Kuraray faces moderate supplier power, steady buyer demands, and niche substitute threats driven by specialty polymers and sustainable materials—factors shaping margins and strategic moves.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kuraray’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Kuraray depends on feedstocks like ethylene and vinyl acetate monomer, whose prices rose ~28% YoY in 2024 and remained volatile into 2025 due to geopolitical shifts and energy-transition policies that tightened petroleum supply.

By end-2025 benchmark naphtha-linked ethylene costs averaged ~$950/ton, forcing Kuraray to use long-term supply contracts and commodity hedges; without these, a 10% upstream spike would cut EBITDA margin by roughly 150–200 basis points.

Concentration of petrochemical providers

The global supply of specialized chemical precursors for polymers is concentrated among a few petrochemical giants—Shell, BASF, and SABIC controlled roughly 40% of selected feedstocks in 2024—giving suppliers strong pricing and allocation leverage during shortages. Kuraray reduces this risk by sourcing from multiple regions (Japan, Southeast Asia, and the US), holding dual-sourcing contracts and safety stocks covering ~3 months of production to maintain continuity.

Energy and utility costs

Chemical manufacturing is energy intensive, with Kuraray using large electricity and natural gas volumes for high-temperature synthesis; industrial users in Japan paid about ¥23.5/kWh average electricity in 2024 and LNG spot-linked gas rose 18% YoY. Tightening carbon pricing and renewable mandates by late 2025 raise utility leverage over Kuraray’s margins. Kuraray is expanding on-site renewables—aiming for 30% self-generated power at key plants by 2026—to cut supplier dependency.

Logistics and transport availability

Specialized transport for chemicals needs certified carriers for hazardous and sensitive materials; in 2024, global chemical logistics capacity tightened with a 7% shortfall in tank-container availability versus demand, pushing spot rates up ~22% year-over-year.

Limited qualified trucking and shipping capacity raises Kuraray’s freight costs and delay risk; providers can demand premium terms because few alternatives meet safety and certification standards.

- Certified carriers required for hazardous loads

- 2024: ~7% tank-container capacity shortfall

- Spot rates +22% YoY in 2024

- Providers set terms in thin market

Limited substitutes for specific catalysts

Suppliers of niche catalysts for EVAL (ethylene vinyl alcohol) and PVA (polyvinyl alcohol) hold strong leverage because few direct substitutes exist; replacing inputs can force Kuraray to re-certify processes and customer approvals, adding time and cost. In 2024 Kuraray reported R&D and quality compliance expenses rising 8% YoY, reflecting this certification burden and supplier-driven risk. This technical lock-in raises supplier bargaining power and potential price pass-through.

- Few substitutes → high supplier leverage

- Process re-certification risk → added cost/time

- 2024: Kuraray compliance/R&D costs +8% YoY

- Specialty vendors can impose price/policy terms

Supplier squeeze lifts costs; Kuraray hedges, multi‑sourcing & renewables cut risk

Suppliers hold moderate–high power: concentrated feedstock/catalyst markets (Shell/BASF/SABIC ~40% share in 2024), naphtha-linked ethylene ~950$/t in 2025, 3 months safety stock, freight tightness (7% tank shortfall, spot rates +22% in 2024) and rising utilities (¥23.5/kWh in 2024) squeeze margins; Kuraray’s hedges, multi‑sourcing and 30% on-site renewables target lower supplier risk.

| Metric | 2024–25 |

|---|---|

| Ethylene price (avg) | ~950 $/t (end‑2025) |

| Feedstock concentration | Shell/BASF/SABIC ~40% |

| Safety stock | ~3 months |

| Tank capacity gap | −7% (2024) |

| Spot freight | +22% YoY (2024) |

| Electricity (Japan) | ¥23.5/kWh (2024) |

| On-site renewables goal | 30% by 2026 |

What is included in the product

Tailored exclusively for Kuraray, this Porter's Five Forces overview uncovers competitive intensity, supplier and buyer power, substitution threats, and entry barriers, highlighting disruptive forces and strategic levers that influence Kuraray’s pricing, margins, and market resilience.

A concise Porter's Five Forces snapshot for Kuraray—quickly assess supplier, buyer, competitor, new entrant, and substitute pressures to guide strategic moves.

Customers Bargaining Power

Concentration in the packaging industry

Switching costs for specialized polymers

Customers in automotive and medical sectors face high switching costs for Kuraray’s specialized polymers because regulatory re-validation often takes 12–24 months and can cost $0.5–$5M per component, per industry estimates in 2024. Once Kuraray’s material is integrated into a vehicle or device, qualifying an alternative requires lengthy testing, certification, and retooling, reducing buyers’ price leverage. This technical integration and compliance burden gives Kuraray measurable protection against customer bargaining power, sustaining higher margins—Kuraray’s specialty polymer segment reported ~18% operating margin in FY2024.

Demand for sustainable and circular solutions

Modern industrial buyers push Kuraray toward circular materials—recyclable or bio-based resins—raising customer bargaining power as 64% of global CPGs had public circularity targets by 2024 (Ellen MacArthur/BCG).

Clients now demand carbon-footprint transparency; 72% of procurement teams use Scope 1–3 data in supplier selection (2023 ISM survey), so Kuraray must report lifecycle emissions to stay preferred.

Kuraray’s R&D and CAPEX must shift: 2024 green-petrochemical investments rose 18% industrywide, or risk losing contracts to greener competitors.

Price sensitivity in commodity segments

In commodity segments like standard polyvinyl alcohol (PVA) and basic fibers, buyers face many global suppliers and high price sensitivity; spot PVA prices fell ~12% worldwide in 2024, pressuring margins across the industry.

Low product differentiation lets purchasers switch to the lowest-cost provider, compressing EBITDA margins for commoditized lines (industry average ~6–8% in 2024).

Kuraray mitigates this by shifting sales mix to specialty grades—e.g., high-strength PVA and functionalized fibers—where contracts, performance specs, and after-sales support raise customer stickiness and sustain higher margins (~15–22%).

- Commoditized PVA: many suppliers, price-driven

- 2024 spot PVA: ~12% price decline

- Commodity EBITDA: ~6–8%

- Specialty grades EBITDA: ~15–22%

- Kuraray strategy: focus on performance-led, contract-based sales

Requirements for technical support and co-development

Sophisticated customers demand extensive technical support and co-development, so Kuraray embeds engineers into client design teams to tailor polymers and elastomers, lowering price-only switching—industrial clients report 30–40% faster time-to-market with such partnerships (2024 supplier surveys).

This service-based dependency raises switching costs and preserves margins: co-development projects often add 5–12% ASP (average selling price) premium and recur in multi-year supply contracts, reducing pure bargaining leverage.

- Embedded engineers: reduces switching

- 30–40% faster time-to-market (2024)

- 5–12% ASP premium on co-dev projects

- Multi-year contracts stabilize margins

Concentrated EVOH buyers boost bargaining power; specialty margins & switching costs cap risk

| Metric | 2024–25 |

|---|---|

| EVOH demand share | 40–50% |

| Buyer consolidation | −20% |

| Switching cost | $0.5–$5M;12–24m |

| Commodity EBITDA | 6–8% |

| Specialty EBITDA | 15–22% |

Full Version Awaits

Kuraray Porter's Five Forces Analysis

This preview shows the exact Kuraray Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use.