Kyushu Electric Power Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

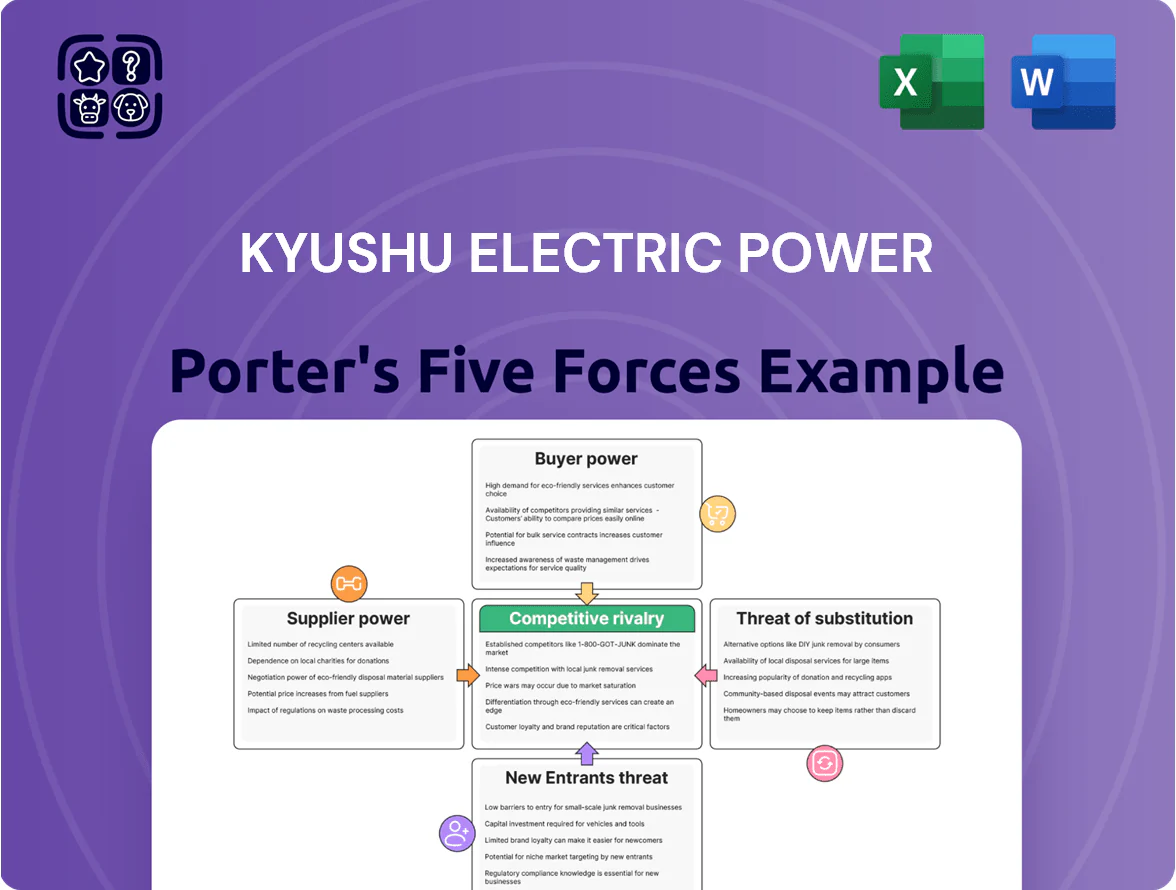

Kyushu Electric Power faces moderate buyer power and regulatory pressure, while capital intensity and established networks limit new entrants—creating a defensible but evolving competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kyushu Electric Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global fuel market volatility

Kyushu Electric Power relies on imported liquefied natural gas (LNG) and coal for ~60% of its thermal generation; by end-2025 LNG spot prices averaged about $12/MMBtu versus $7/MMBtu in 2020, lifting fuel costs and ceding pricing power to major exporters. Geopolitical tensions—notably in 2024–25 supply shifts from Russia and Middle East disruptions—kept freight rates and contract premia elevated, squeezing margins. As a net buyer of global commodities, Kyushu is a price taker exposed to volatile FX and shipping costs, increasing procurement risk.

Nuclear fuel and specialized maintenance

Kyushu Electric relies on a handful of global suppliers for nuclear fuel and specialized maintenance, giving suppliers high bargaining power; in 2024 Japan imported ~95% of reactor fuel components, leaving few alternatives.

Because safety and regulatory compliance are critical, suppliers can command premium pricing and strict contract terms; Kyushu Electric held long-term contracts worth an estimated ¥120–180 billion collectively in 2023–24 to secure fuel and services.

Renewable energy technology providers

As Kyushu Electric scales renewables to hit its 46% CO2 reduction by 2025 target, it relies on solar, turbine, and grid-battery makers; global concentration—top 5 wind-turbine makers hold ~70% market share (2024) and top 3 battery cell producers >60%—lets suppliers push prices during demand spikes.

Specialized engineering labor shortage

The aging Japanese workforce means fewer senior engineers for complex grid and nuclear upkeep; Japan’s 2024 METI report showed engineers aged 50+ account for ~48% of utilities’ technical staff, shrinking recruitment pools.

Specialized staffing firms now charge premiums, raising Kyushu Electric’s labour procurement costs; vendor rates reportedly rose ~12% in 2023–24 for high-skill contracts.

Higher costs threaten modernization and safety budgets, forcing trade-offs between capital projects and O&M spending.

- ~48% technical staff 50+ (METI 2024)

- Vendor premium +12% (2023–24)

- Rising O&M vs capex trade-offs

Grid component manufacturing concentration

The procurement of high-voltage transformers and specialized grid gear is concentrated among a few firms (Toshiba Energy Systems, Hitachi Energy, Mitsubishi Electric), letting them command ~30–40% equipment margin and typical lead times of 12–24 months as of 2025 due to Japan’s ¥3.6 trillion grid upgrade push for renewables.

Limited competition raises supplier bargaining power over Kyushu Electric, forcing price pass-through, longer contract horizons, and dependence on supplier capacity ramp-ups to meet intermittent renewable integration.

- Top 3 suppliers dominate niche market

- Estimated 30–40% equipment margins (2025)

- Lead times 12–24 months

- ¥3.6 trillion national grid upgrade (through 2025)

Supplier power squeezes Kyushu: high imported fuels, costly vendors & aging engineers

Suppliers hold high leverage: Kyushu is a price taker for ~60% imported LNG/coal (LNG ~ $12/MMBtu in 2025), relies on few nuclear/transformer vendors (top 3 hold ~70%/30–40% margins) and scarce skilled engineers (~48% aged 50+), causing higher procurement and O&M costs versus capex trade-offs.

| Metric | Value |

|---|---|

| Imported fuel share | ~60% |

| LNG price (2025) | $12/MMBtu |

| Tech staff 50+ | ~48% (METI 2024) |

| Top vendors' margins | 30–40% |

What is included in the product

Tailored exclusively for Kyushu Electric Power, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

Quick, one-sheet Porter’s Five Forces for Kyushu Electric Power—clarifies supplier, buyer, rivalry, entry, and substitute pressures so executives can act fast.

Customers Bargaining Power

Retail liberalization and switching ease

Full retail liberalization lets residential and small business customers switch electricity suppliers with just a few clicks, and by late 2025 over 6.5 million households (≈12% of Japan’s households) used comparison platforms, raising price sensitivity for Kyushu Electric Power.

Streamlined switching cut average churn friction to under 10 days and drove retail price spreads down ~4% year‑over‑year, giving individual consumers clear leverage to demand lower rates and better service terms.

Large industrial volume negotiation

Major industrial customers in Kyushu account for roughly 30–40% of Kyushu Electric Power Co Inc’s FY2024 revenue, giving them strong leverage to demand bespoke contracts and volume discounts.

These users can credibly threaten switching to Chugoku Electric or onsite cogeneration; a 100 MW shift could cut Kyushu Electric’s load by ~2–3%, pressuring averages rates.

Bulk demand moves support aggressive price talks and contract clauses on duration, indexation, and capacity charges, squeezing margins on large accounts.

Corporate demand for green energy

Aggregation of small consumers

Energy aggregators and community choice programs let small consumers pool demand; in Japan by 2024 roughly 1.2 million household contracts shifted to third-party suppliers, raising collective buying leverage against utilities like Kyushu Electric.

These aggregators negotiate on behalf of thousands, squeezing retail margins—Kyushu Electric reported a 2023 retail segment operating margin of about 4.5%, vulnerable to group procurement pressure.

- 1.2M households shifted by 2024

- Aggregators act as professional negotiators

- Kyushu Electric retail margin ~4.5% (2023)

Informed buyers and price transparency

Increased access to real-time data from the Japan Electric Power Exchange (JEPX) has made Kyushu Electric Power’s customers more aware of wholesale price trends, with average spot prices in Kyushu rising 22% in 2024 vs 2023, so customers expect retail rates to mirror market moves.

Informed buyers now pressure the utility to cut markups during low wholesale-cost periods; Kyushu’s retail margin compression reached 1.4 percentage points in 2024, reducing pricing power.

Transparency shifts bargaining power to consumers, forcing greater pricing accountability and faster tariff adjustments to avoid churn and regulatory scrutiny.

- JEPX spot price +22% (2024 vs 2023)

- Kyushu retail margin -1.4 pp (2024)

- Higher churn risk if tariffs lag spot market

Retail liberalization and green buyers squeeze margins as customers shift and prices jump

Customers hold strong leverage: retail liberalization and 6.5M comparison users (late‑2025) and 1.2M switched households (2024) raised churn and price sensitivity; spot prices +22% (2024) cut Kyushu retail margin 1.4pp to ~4.5% (2023), while large industrial buyers (30–40% of FY2024 revenue) and corporate RE demand (256 RE100 members, end‑2024) force discounts and green PPAs.

| Metric | Value |

|---|---|

| Comparison users (late‑2025) | 6.5M |

| Households switched (2024) | 1.2M |

| JEPX spot change (2024 vs 2023) | +22% |

| Retail margin (2023) | ~4.5% |

| Margin compression (2024) | -1.4 pp |

| Industrial share FY2024 | 30–40% |

| Japan RE100 (end‑2024) | 256 firms |

Preview the Actual Deliverable

Kyushu Electric Power Porter's Five Forces Analysis

This preview shows the exact Kyushu Electric Power Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted version you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use deliverable, containing the complete Five Forces insights for Kyushu Electric Power and available instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Kyushu Electric Power faces moderate buyer power and regulatory pressure, while capital intensity and established networks limit new entrants—creating a defensible but evolving competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kyushu Electric Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global fuel market volatility

Kyushu Electric Power relies on imported liquefied natural gas (LNG) and coal for ~60% of its thermal generation; by end-2025 LNG spot prices averaged about $12/MMBtu versus $7/MMBtu in 2020, lifting fuel costs and ceding pricing power to major exporters. Geopolitical tensions—notably in 2024–25 supply shifts from Russia and Middle East disruptions—kept freight rates and contract premia elevated, squeezing margins. As a net buyer of global commodities, Kyushu is a price taker exposed to volatile FX and shipping costs, increasing procurement risk.

Nuclear fuel and specialized maintenance

Kyushu Electric relies on a handful of global suppliers for nuclear fuel and specialized maintenance, giving suppliers high bargaining power; in 2024 Japan imported ~95% of reactor fuel components, leaving few alternatives.

Because safety and regulatory compliance are critical, suppliers can command premium pricing and strict contract terms; Kyushu Electric held long-term contracts worth an estimated ¥120–180 billion collectively in 2023–24 to secure fuel and services.

Renewable energy technology providers

As Kyushu Electric scales renewables to hit its 46% CO2 reduction by 2025 target, it relies on solar, turbine, and grid-battery makers; global concentration—top 5 wind-turbine makers hold ~70% market share (2024) and top 3 battery cell producers >60%—lets suppliers push prices during demand spikes.

Specialized engineering labor shortage

The aging Japanese workforce means fewer senior engineers for complex grid and nuclear upkeep; Japan’s 2024 METI report showed engineers aged 50+ account for ~48% of utilities’ technical staff, shrinking recruitment pools.

Specialized staffing firms now charge premiums, raising Kyushu Electric’s labour procurement costs; vendor rates reportedly rose ~12% in 2023–24 for high-skill contracts.

Higher costs threaten modernization and safety budgets, forcing trade-offs between capital projects and O&M spending.

- ~48% technical staff 50+ (METI 2024)

- Vendor premium +12% (2023–24)

- Rising O&M vs capex trade-offs

Grid component manufacturing concentration

The procurement of high-voltage transformers and specialized grid gear is concentrated among a few firms (Toshiba Energy Systems, Hitachi Energy, Mitsubishi Electric), letting them command ~30–40% equipment margin and typical lead times of 12–24 months as of 2025 due to Japan’s ¥3.6 trillion grid upgrade push for renewables.

Limited competition raises supplier bargaining power over Kyushu Electric, forcing price pass-through, longer contract horizons, and dependence on supplier capacity ramp-ups to meet intermittent renewable integration.

- Top 3 suppliers dominate niche market

- Estimated 30–40% equipment margins (2025)

- Lead times 12–24 months

- ¥3.6 trillion national grid upgrade (through 2025)

Supplier power squeezes Kyushu: high imported fuels, costly vendors & aging engineers

Suppliers hold high leverage: Kyushu is a price taker for ~60% imported LNG/coal (LNG ~ $12/MMBtu in 2025), relies on few nuclear/transformer vendors (top 3 hold ~70%/30–40% margins) and scarce skilled engineers (~48% aged 50+), causing higher procurement and O&M costs versus capex trade-offs.

| Metric | Value |

|---|---|

| Imported fuel share | ~60% |

| LNG price (2025) | $12/MMBtu |

| Tech staff 50+ | ~48% (METI 2024) |

| Top vendors' margins | 30–40% |

What is included in the product

Tailored exclusively for Kyushu Electric Power, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

Quick, one-sheet Porter’s Five Forces for Kyushu Electric Power—clarifies supplier, buyer, rivalry, entry, and substitute pressures so executives can act fast.

Customers Bargaining Power

Retail liberalization and switching ease

Full retail liberalization lets residential and small business customers switch electricity suppliers with just a few clicks, and by late 2025 over 6.5 million households (≈12% of Japan’s households) used comparison platforms, raising price sensitivity for Kyushu Electric Power.

Streamlined switching cut average churn friction to under 10 days and drove retail price spreads down ~4% year‑over‑year, giving individual consumers clear leverage to demand lower rates and better service terms.

Large industrial volume negotiation

Major industrial customers in Kyushu account for roughly 30–40% of Kyushu Electric Power Co Inc’s FY2024 revenue, giving them strong leverage to demand bespoke contracts and volume discounts.

These users can credibly threaten switching to Chugoku Electric or onsite cogeneration; a 100 MW shift could cut Kyushu Electric’s load by ~2–3%, pressuring averages rates.

Bulk demand moves support aggressive price talks and contract clauses on duration, indexation, and capacity charges, squeezing margins on large accounts.

Corporate demand for green energy

Aggregation of small consumers

Energy aggregators and community choice programs let small consumers pool demand; in Japan by 2024 roughly 1.2 million household contracts shifted to third-party suppliers, raising collective buying leverage against utilities like Kyushu Electric.

These aggregators negotiate on behalf of thousands, squeezing retail margins—Kyushu Electric reported a 2023 retail segment operating margin of about 4.5%, vulnerable to group procurement pressure.

- 1.2M households shifted by 2024

- Aggregators act as professional negotiators

- Kyushu Electric retail margin ~4.5% (2023)

Informed buyers and price transparency

Increased access to real-time data from the Japan Electric Power Exchange (JEPX) has made Kyushu Electric Power’s customers more aware of wholesale price trends, with average spot prices in Kyushu rising 22% in 2024 vs 2023, so customers expect retail rates to mirror market moves.

Informed buyers now pressure the utility to cut markups during low wholesale-cost periods; Kyushu’s retail margin compression reached 1.4 percentage points in 2024, reducing pricing power.

Transparency shifts bargaining power to consumers, forcing greater pricing accountability and faster tariff adjustments to avoid churn and regulatory scrutiny.

- JEPX spot price +22% (2024 vs 2023)

- Kyushu retail margin -1.4 pp (2024)

- Higher churn risk if tariffs lag spot market

Retail liberalization and green buyers squeeze margins as customers shift and prices jump

Customers hold strong leverage: retail liberalization and 6.5M comparison users (late‑2025) and 1.2M switched households (2024) raised churn and price sensitivity; spot prices +22% (2024) cut Kyushu retail margin 1.4pp to ~4.5% (2023), while large industrial buyers (30–40% of FY2024 revenue) and corporate RE demand (256 RE100 members, end‑2024) force discounts and green PPAs.

| Metric | Value |

|---|---|

| Comparison users (late‑2025) | 6.5M |

| Households switched (2024) | 1.2M |

| JEPX spot change (2024 vs 2023) | +22% |

| Retail margin (2023) | ~4.5% |

| Margin compression (2024) | -1.4 pp |

| Industrial share FY2024 | 30–40% |

| Japan RE100 (end‑2024) | 256 firms |

Preview the Actual Deliverable

Kyushu Electric Power Porter's Five Forces Analysis

This preview shows the exact Kyushu Electric Power Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full, professionally formatted version you’ll get—ready for download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use deliverable, containing the complete Five Forces insights for Kyushu Electric Power and available instantly after payment.