Lamb Weston Holdings Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

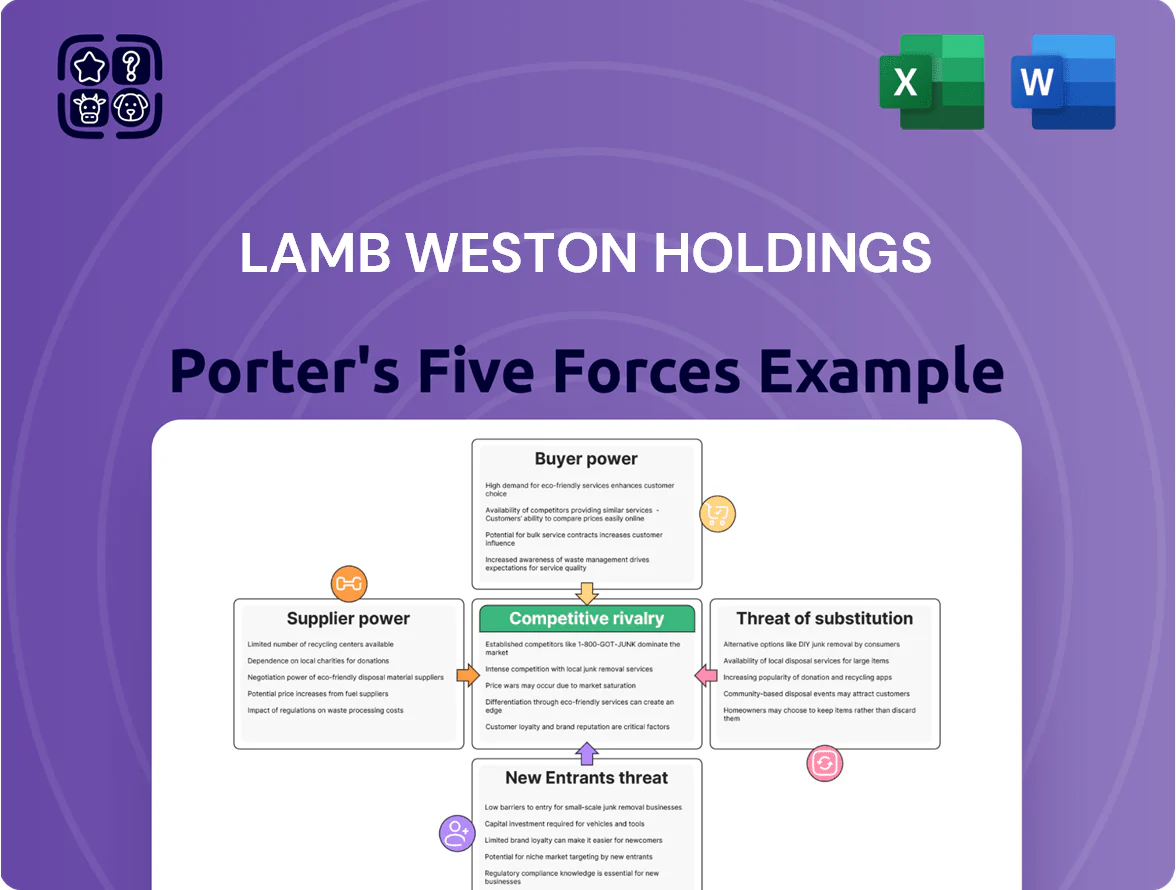

Suppliers Bargaining Power

Raw Potato Sourcing Concentration

Lamb Weston depends on long-term contracts with a small set of large growers in the Pacific Northwest; in 2024 roughly 60–70% of its U.S. processing potato volume came from that region, concentrating supplier risk.

Those contracts give price stability, but high switching costs for certified processing potatoes mean a single regional crop failure forces expensive spot buys or plant slowdowns.

By late 2025, climate volatility raised grower leverage: industry reports show yield variance up to 20% year-over-year, boosting growers who can guarantee quality and contracted volumes.

Energy and Fuel Input Costs

The frozen-potato manufacturing process is energy-intensive, using large volumes of natural gas and electricity for blanching, dehydration and freezing; Lamb Weston reported energy and utilities costs of about $360 million in FY2024, ~6% of COGS.

Energy and transportation-fuel suppliers hold moderate bargaining power since Lamb Weston is a price taker in global commodity markets and buys on spot and contracted terms; natural gas Henry Hub rose ~45% in 2022–23 before stabilizing in 2024.

Fluctuations in energy prices directly affect COGS and gross margin; Lamb Weston uses hedging—forward gas contracts and fuel swaps—to limit exposure, though a 10% gas-price spike still can shave several basis points off margins.

Specialized Processing Equipment

The frozen-potato industry needs specialized machinery for high-volume peeling, cutting, and IQF freezing, made by a handful of global engineering firms, concentrating supplier power. These vendors hold proprietary tech and control spare parts and service; downtime costs Lamb Weston about $200k–$500k per day in lost production in large plants. Meeting 2025 automation standards typically needs $50–150 million per plant in capex, increasing vendor dependence. Long-term service contracts and OEM parts cement supplier leverage.

Labor Market Constraints

- 2024 US food manufacturing wage growth: +5.2% YoY

- Lamb Weston automation capex plan: ~150 million USD (2024–25)

- Rural plant hiring premium: local wages typically 5–10% above regional averages

Packaging Material Volatility

Lamb Weston buys large volumes of plastic resin and paper pulp; resin prices rose ~45% from 2020–2022 and pulp spot prices jumped ~30% in 2021–2023, exposing gross margins to supplier pricing power.

Tighter packaging regs through 2025 raised demand for sustainable materials, which cost 10–30% more, giving niche eco-pack suppliers greater leverage on specs and lead times.

- Resin/pulp price swings: +30–45% (2020–2023)

- Sustainable premium: +10–30% cost

- Specialized suppliers = stronger procurement leverage

Suppliers Tighten Leverage: PNW Potatoes, Rising Energy, Wages & Packaging Costs

Suppliers exert moderate-to-high bargaining power: concentrated Pacific Northwest growers supply ~60–70% of US processing potatoes (2024), energy costs were ~$360m (FY2024, ~6% of COGS), and specialized machinery/service vendors plus rising wages (US food manufacturing wages +5.2% YoY in 2024) and pricier sustainable packaging (10–30% premium) tighten leverage.

| Factor | 2024–25 Data |

|---|---|

| PNW potato share | 60–70% |

| Energy costs (FY2024) | $360m (~6% COGS) |

| Wage growth | +5.2% YoY |

| Automation capex | $150m (2024–25) |

| Packaging premium | +10–30% |

What is included in the product

Tailored exclusively for Lamb Weston Holdings, this Porter’s Five Forces overview uncovers key competitive drivers, buyer and supplier power, threat of entrants and substitutes, and emerging disruptions that shape pricing, margins, and strategic positioning.

A concise Porter's Five Forces snapshot for Lamb Weston—clarifies supplier, buyer, substitute, entrant, and rivalry pressures for quick strategic decisions.

Customers Bargaining Power

Consolidation of Global Quick Service Restaurants

Major fast-food chains account for roughly 60% of Lamb Weston’s 2024 revenue, giving these buyers strong leverage to demand volume, strict quality specs, and lower prices.

QSR consolidation—e.g., top 5 global chains holding ~45% of systemwide sales by 2025—lets customers play major processors against one another at contract renewals.

High-volume contracts and narrow margin pressure force Lamb Weston to accept tighter pricing or invest in value-added services to retain key accounts.

Retail Private Label Expansion

Grocery retailers expanded private-label frozen potato share to about 28% of US category sales in 2024, squeezing branded vendors like Lamb Weston (LW). Retailers control shelf space and can swap LW’s SKUs for cheaper house brands, raising price sensitivity and margin pressure. LW responded with higher trade promotion spend—up ~160 basis points of sales in 2024—and increased marketing and innovation to defend market share.

Low Switching Costs for Foodservice Distributors

Broadline foodservice distributors can source frozen fries from multiple global suppliers, so switching for better price or service is easy; industry data shows top 10 distributors often negotiate 5–10% price concessions annually.

Lamb Weston’s 2024 revenue of $4.0B and global scale help secure contracts, but standardized potato SKUs keep price as a primary driver for many buyers.

Maintaining tight logistics (Lamb Weston reduced transit loss by 12% in 2023) and rolling out product innovation—new coatings and value-added SKUs—remains vital to prevent churn.

Price Sensitivity in Inflationary Environments

- US CPI 2024: +3.4%

- Potato price change 2024: ~+18%

- Fries = high-margin side; volume loss harms leverage

- Risk: customers resist price hikes, favor private label

Demand for Healthier and Sustainable Options

Institutional buyers and large chains now demand carbon-footprint and nutrition transparency; 2024 Q4 data show 62% of US foodservice operators rate ESG as critical for suppliers, pressuring Lamb Weston to disclose lifecycle emissions and sodium data.

Buyers force reformulations—lower-sodium, non-GMO—and contract terms tied to ESG KPIs; failing to comply risks losing multi-year contracts that represented ~40% of Lamb Weston’s 2023 US foodservice revenue.

- 62% foodservice buyers: ESG critical (2024 Q4)

- ~40% revenue from multi-year foodservice contracts (2023)

- Reformulation: lower-sodium, non-GMO, lifecycle emissions reporting

Lamb Weston under pricing pressure: scale helps, private-label and ESG squeeze margins

Large QSRs (≈60% of 2024 revenue) and consolidated distributors wield strong price and spec leverage, while private-label (≈28% US frozen potato share 2024) and price-sensitive consumers (US CPI +3.4% 2024) force Lamb Weston to accept tighter pricing or add value; LW scale ($4.0B 2024) helps, but standardized SKUs keep price primary and ESG demands (62% foodservice buyers 2024 Q4) add contract risk.

| Metric | Value |

|---|---|

| 2024 revenue | $4.0B |

| QSR share | ≈60% |

| Private-label share | ≈28% |

| US CPI 2024 | +3.4% |

| Potato price change 2024 | +18% |

| ESG critical (foodservice) | 62% (Q4 2024) |

Preview the Actual Deliverable

Lamb Weston Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Lamb Weston Holdings you’ll receive immediately after purchase—no placeholders or samples; it covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and supporting evidence.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Suppliers Bargaining Power

Raw Potato Sourcing Concentration

Lamb Weston depends on long-term contracts with a small set of large growers in the Pacific Northwest; in 2024 roughly 60–70% of its U.S. processing potato volume came from that region, concentrating supplier risk.

Those contracts give price stability, but high switching costs for certified processing potatoes mean a single regional crop failure forces expensive spot buys or plant slowdowns.

By late 2025, climate volatility raised grower leverage: industry reports show yield variance up to 20% year-over-year, boosting growers who can guarantee quality and contracted volumes.

Energy and Fuel Input Costs

The frozen-potato manufacturing process is energy-intensive, using large volumes of natural gas and electricity for blanching, dehydration and freezing; Lamb Weston reported energy and utilities costs of about $360 million in FY2024, ~6% of COGS.

Energy and transportation-fuel suppliers hold moderate bargaining power since Lamb Weston is a price taker in global commodity markets and buys on spot and contracted terms; natural gas Henry Hub rose ~45% in 2022–23 before stabilizing in 2024.

Fluctuations in energy prices directly affect COGS and gross margin; Lamb Weston uses hedging—forward gas contracts and fuel swaps—to limit exposure, though a 10% gas-price spike still can shave several basis points off margins.

Specialized Processing Equipment

The frozen-potato industry needs specialized machinery for high-volume peeling, cutting, and IQF freezing, made by a handful of global engineering firms, concentrating supplier power. These vendors hold proprietary tech and control spare parts and service; downtime costs Lamb Weston about $200k–$500k per day in lost production in large plants. Meeting 2025 automation standards typically needs $50–150 million per plant in capex, increasing vendor dependence. Long-term service contracts and OEM parts cement supplier leverage.

Labor Market Constraints

- 2024 US food manufacturing wage growth: +5.2% YoY

- Lamb Weston automation capex plan: ~150 million USD (2024–25)

- Rural plant hiring premium: local wages typically 5–10% above regional averages

Packaging Material Volatility

Lamb Weston buys large volumes of plastic resin and paper pulp; resin prices rose ~45% from 2020–2022 and pulp spot prices jumped ~30% in 2021–2023, exposing gross margins to supplier pricing power.

Tighter packaging regs through 2025 raised demand for sustainable materials, which cost 10–30% more, giving niche eco-pack suppliers greater leverage on specs and lead times.

- Resin/pulp price swings: +30–45% (2020–2023)

- Sustainable premium: +10–30% cost

- Specialized suppliers = stronger procurement leverage

Suppliers Tighten Leverage: PNW Potatoes, Rising Energy, Wages & Packaging Costs

Suppliers exert moderate-to-high bargaining power: concentrated Pacific Northwest growers supply ~60–70% of US processing potatoes (2024), energy costs were ~$360m (FY2024, ~6% of COGS), and specialized machinery/service vendors plus rising wages (US food manufacturing wages +5.2% YoY in 2024) and pricier sustainable packaging (10–30% premium) tighten leverage.

| Factor | 2024–25 Data |

|---|---|

| PNW potato share | 60–70% |

| Energy costs (FY2024) | $360m (~6% COGS) |

| Wage growth | +5.2% YoY |

| Automation capex | $150m (2024–25) |

| Packaging premium | +10–30% |

What is included in the product

Tailored exclusively for Lamb Weston Holdings, this Porter’s Five Forces overview uncovers key competitive drivers, buyer and supplier power, threat of entrants and substitutes, and emerging disruptions that shape pricing, margins, and strategic positioning.

A concise Porter's Five Forces snapshot for Lamb Weston—clarifies supplier, buyer, substitute, entrant, and rivalry pressures for quick strategic decisions.

Customers Bargaining Power

Consolidation of Global Quick Service Restaurants

Major fast-food chains account for roughly 60% of Lamb Weston’s 2024 revenue, giving these buyers strong leverage to demand volume, strict quality specs, and lower prices.

QSR consolidation—e.g., top 5 global chains holding ~45% of systemwide sales by 2025—lets customers play major processors against one another at contract renewals.

High-volume contracts and narrow margin pressure force Lamb Weston to accept tighter pricing or invest in value-added services to retain key accounts.

Retail Private Label Expansion

Grocery retailers expanded private-label frozen potato share to about 28% of US category sales in 2024, squeezing branded vendors like Lamb Weston (LW). Retailers control shelf space and can swap LW’s SKUs for cheaper house brands, raising price sensitivity and margin pressure. LW responded with higher trade promotion spend—up ~160 basis points of sales in 2024—and increased marketing and innovation to defend market share.

Low Switching Costs for Foodservice Distributors

Broadline foodservice distributors can source frozen fries from multiple global suppliers, so switching for better price or service is easy; industry data shows top 10 distributors often negotiate 5–10% price concessions annually.

Lamb Weston’s 2024 revenue of $4.0B and global scale help secure contracts, but standardized potato SKUs keep price as a primary driver for many buyers.

Maintaining tight logistics (Lamb Weston reduced transit loss by 12% in 2023) and rolling out product innovation—new coatings and value-added SKUs—remains vital to prevent churn.

Price Sensitivity in Inflationary Environments

- US CPI 2024: +3.4%

- Potato price change 2024: ~+18%

- Fries = high-margin side; volume loss harms leverage

- Risk: customers resist price hikes, favor private label

Demand for Healthier and Sustainable Options

Institutional buyers and large chains now demand carbon-footprint and nutrition transparency; 2024 Q4 data show 62% of US foodservice operators rate ESG as critical for suppliers, pressuring Lamb Weston to disclose lifecycle emissions and sodium data.

Buyers force reformulations—lower-sodium, non-GMO—and contract terms tied to ESG KPIs; failing to comply risks losing multi-year contracts that represented ~40% of Lamb Weston’s 2023 US foodservice revenue.

- 62% foodservice buyers: ESG critical (2024 Q4)

- ~40% revenue from multi-year foodservice contracts (2023)

- Reformulation: lower-sodium, non-GMO, lifecycle emissions reporting

Lamb Weston under pricing pressure: scale helps, private-label and ESG squeeze margins

Large QSRs (≈60% of 2024 revenue) and consolidated distributors wield strong price and spec leverage, while private-label (≈28% US frozen potato share 2024) and price-sensitive consumers (US CPI +3.4% 2024) force Lamb Weston to accept tighter pricing or add value; LW scale ($4.0B 2024) helps, but standardized SKUs keep price primary and ESG demands (62% foodservice buyers 2024 Q4) add contract risk.

| Metric | Value |

|---|---|

| 2024 revenue | $4.0B |

| QSR share | ≈60% |

| Private-label share | ≈28% |

| US CPI 2024 | +3.4% |

| Potato price change 2024 | +18% |

| ESG critical (foodservice) | 62% (Q4 2024) |

Preview the Actual Deliverable

Lamb Weston Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Lamb Weston Holdings you’ll receive immediately after purchase—no placeholders or samples; it covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and supporting evidence.