Lampogas SpA Porter's Five Forces Analysis

From Overview to Strategy Blueprint

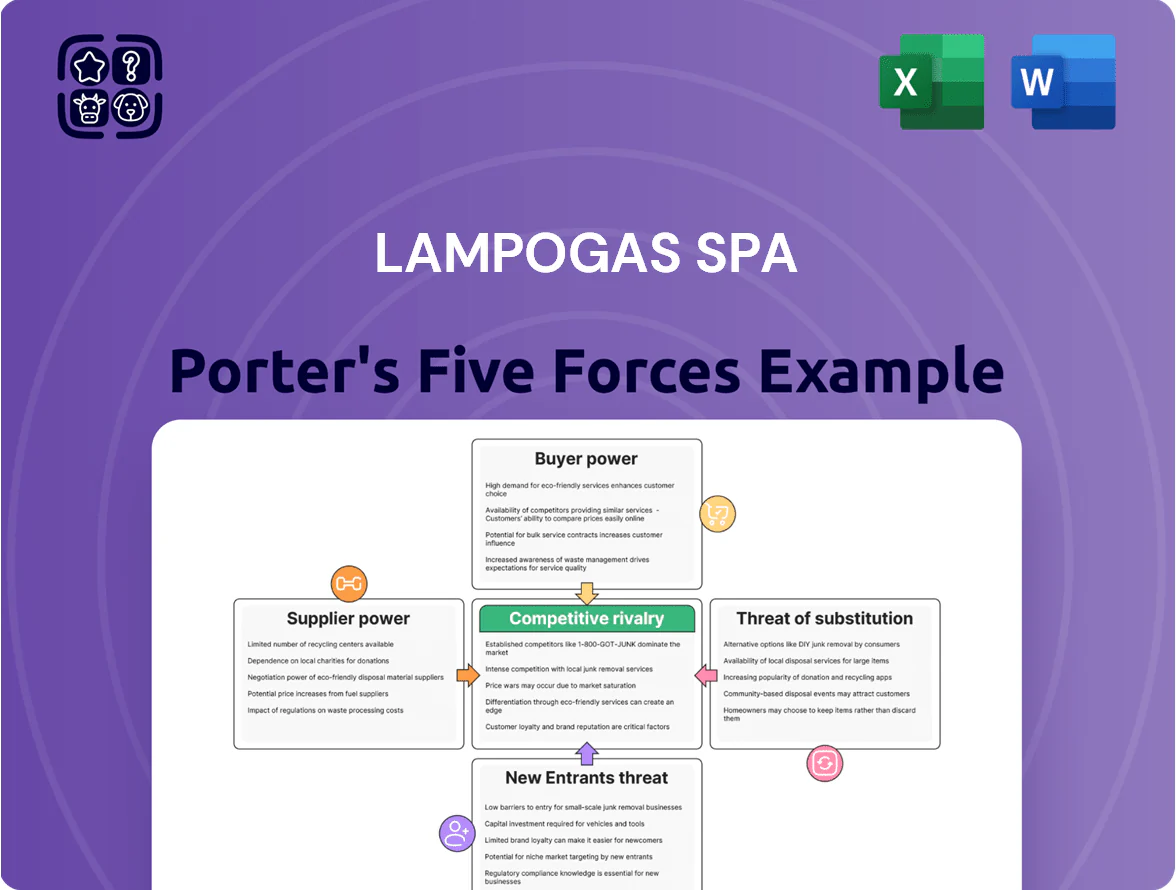

Lampogas SpA faces moderate supplier power and rising competitive rivalry as market entrants and substitutes gain traction, while buyer bargaining remains mixed across segments; regulatory shifts and fuel-price volatility add notable external pressure. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and tactical implications—unlock the full Porter's Five Forces Analysis to get a complete, data-driven strategic roadmap for Lampogas SpA.

Suppliers Bargaining Power

Concentration of Upstream LPG Producers

The Italian LPG market sources over 70% of its supply from five large refineries and international majors (ENI, Shell, BP, TotalEnergies, Vitol), concentrating bargaining power upstream; Lampogas SpA, as a distributor, depends on these suppliers for availability and wholesale pricing.

Supplier leverage spikes during Mediterranean disruptions: 2022–2024 data show LPG export cuts from North Africa rose 38%, driving spot price volatility of ±22% and squeezing Lampogas margins.

Global Commodity Price Indexing

Wholesale LPG prices track Brent crude and Henry Hub natural gas; Brent averaged 92 USD/bbl and Henry Hub 4.5 USD/MMBtu in 2025 so far, keeping LPG volatility high.

Lampogas has no pricing power versus these benchmarks and must absorb or pass cost swings to customers, raising margin pressure—Q3 2025 gross margin for EU LPG retailers averaged ~7%.

That price-taker stance boosts global suppliers’ bargaining power, which effectively sets Lampogas’s raw-material cost structure and limits strategic flexibility.

Logistical and Infrastructure Dependency

Logistical and infrastructure dependence raises supplier power: about 70% of Italy’s LPG terminals are linked to five major energy groups, so Lampogas needs terminal access to serve ~85% of its retail network nationwide; suppliers can raise terminal fees (historical uplifts of 5–12% in 2023–24) or favor internal distributors, squeezing Lampogas’s margins and risking delivery delays during peak winter months.

Regulatory Compliance and Environmental Standards

Suppliers are shifting carbon credit and compliance costs downstream under the EU Emissions Trading System, raising distributor input costs—carbon prices averaged €80/ton CO2 in 2025, up from €25 in 2020.

Upstream producers control Bio-LPG rollout timing toward 2030 targets, so Lampogas must match supplier-led certification and blend schedules to keep market access and avoid fines.

- €80/ton CO2 average price (2025)

- EU 2030 binding target: −55% emissions vs 1990

- Supplier-driven Bio-LPG availability limits product mix

- Non-alignment risks lost sales, fines, higher margin pressure

Lack of Immediate Vertical Integration

Concentrated LPG supply and higher EU ETS squeeze Italian margins amid volatile exports

Suppliers hold strong leverage: five majors supply >70% of Italian LPG, with top exporters (Vitol, Trafigura) at ~35% global share (2024); Lampogas bought ~68% volumes on >2‑yr contracts (2024). Mediterranean export cuts (2022–24 +38%) drove spot volatility ±22%, while EU ETS rose to €80/t CO2 (2025), squeezing margins (EU LPG retailer gross ~7% Q3 2025).

| Metric | Value |

|---|---|

| Supply concentration | >70% |

| Major exporters share (2024) | ~35% |

| Long contracts (2024) | ~68% |

| Spot volatility (2022–24) | ±22% |

| EU ETS price (2025) | €80/t |

| Retail gross margin (Q3 2025) | ~7% |

What is included in the product

Tailored Porter's Five Forces for Lampogas SpA uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers that influence pricing, profitability, and market positioning.

Concise Porter's Five Forces snapshot for Lampogas SpA—instantly highlights competitive pressures and strategic levers to inform boardroom decisions.

Customers Bargaining Power

Fragmented Residential Customer Base

High Leverage of Industrial and Commercial Clients

Switching Costs and Contractual Ties

Domestic customers face switching costs because LPG storage tanks and regulators—often supplied and maintained by Lampogas SpA—require installation and certification; replacing them can cost €150–€400 per household and take 1–3 days.

Contracts commonly include exit fees or reimbursement clauses equal to 30–60% of equipment value, plus technical inspections; these barriers create measurable lock-in, limiting churn after minor price moves.

Price Transparency and Digital Comparison

By end-2025, Italian digital platforms and consumer groups raised energy price transparency; 72% of households used price comparison tools, per Autorità di Regolazione per Energia (ARERA), letting consumers directly compare Lampogas SpA tariffs with national and local rivals.

Better information lets small-scale customers demand promos or switch: Lampogas saw a 1.8% voluntary churn uptick in 2024–25 as comparison tools highlighted cheaper short-term offers.

Government Subsidies and Social Protection

In Italy, 2024 energy subsidies and social tariffs covered about 3.8 million households, lowering LPG effective prices and acting like customer bargaining power by capping what consumers pay and demand.

These policies constrain Lampogas SpA’s pricing freedom—with regulated support reducing price sensitivity in low-income segments and limiting margin-raising during supply shocks (Italy’s 2023 household energy aid budget was ~€5.2bn).

- 3.8M subsidized households (2024)

- €5.2bn energy aid (2023)

- Subsidies cap retail price pass-through

- Limits Lampogas’ pricing flexibility

Mixed customer power: low household leverage vs. dominant B2B accounts, subsidies cap pricing

Customers’ bargaining power is mixed: households (42% revenue in 2024; avg spend €420) have low individual leverage but rising transparency raised churn +1.8% (2024–25); top 10 B2B clients (>35% regional gas revenue) wield high leverage (single account €5–12M). Subsidies cover 3.8M households (2024), capping price pass-through and constraining Lampogas’ pricing freedom.

| Metric | 2023–25 |

|---|---|

| Household rev share | 42% |

| Avg household spend | €420 |

| Churn change | +1.8% |

| Top10 B2B rev | >35% |

| Subsidized households | 3.8M |

Full Version Awaits

Lampogas SpA Porter's Five Forces Analysis

This preview shows the exact Lampogas SpA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Lampogas SpA faces moderate supplier power and rising competitive rivalry as market entrants and substitutes gain traction, while buyer bargaining remains mixed across segments; regulatory shifts and fuel-price volatility add notable external pressure. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and tactical implications—unlock the full Porter's Five Forces Analysis to get a complete, data-driven strategic roadmap for Lampogas SpA.

Suppliers Bargaining Power

Concentration of Upstream LPG Producers

The Italian LPG market sources over 70% of its supply from five large refineries and international majors (ENI, Shell, BP, TotalEnergies, Vitol), concentrating bargaining power upstream; Lampogas SpA, as a distributor, depends on these suppliers for availability and wholesale pricing.

Supplier leverage spikes during Mediterranean disruptions: 2022–2024 data show LPG export cuts from North Africa rose 38%, driving spot price volatility of ±22% and squeezing Lampogas margins.

Global Commodity Price Indexing

Wholesale LPG prices track Brent crude and Henry Hub natural gas; Brent averaged 92 USD/bbl and Henry Hub 4.5 USD/MMBtu in 2025 so far, keeping LPG volatility high.

Lampogas has no pricing power versus these benchmarks and must absorb or pass cost swings to customers, raising margin pressure—Q3 2025 gross margin for EU LPG retailers averaged ~7%.

That price-taker stance boosts global suppliers’ bargaining power, which effectively sets Lampogas’s raw-material cost structure and limits strategic flexibility.

Logistical and Infrastructure Dependency

Logistical and infrastructure dependence raises supplier power: about 70% of Italy’s LPG terminals are linked to five major energy groups, so Lampogas needs terminal access to serve ~85% of its retail network nationwide; suppliers can raise terminal fees (historical uplifts of 5–12% in 2023–24) or favor internal distributors, squeezing Lampogas’s margins and risking delivery delays during peak winter months.

Regulatory Compliance and Environmental Standards

Suppliers are shifting carbon credit and compliance costs downstream under the EU Emissions Trading System, raising distributor input costs—carbon prices averaged €80/ton CO2 in 2025, up from €25 in 2020.

Upstream producers control Bio-LPG rollout timing toward 2030 targets, so Lampogas must match supplier-led certification and blend schedules to keep market access and avoid fines.

- €80/ton CO2 average price (2025)

- EU 2030 binding target: −55% emissions vs 1990

- Supplier-driven Bio-LPG availability limits product mix

- Non-alignment risks lost sales, fines, higher margin pressure

Lack of Immediate Vertical Integration

Concentrated LPG supply and higher EU ETS squeeze Italian margins amid volatile exports

Suppliers hold strong leverage: five majors supply >70% of Italian LPG, with top exporters (Vitol, Trafigura) at ~35% global share (2024); Lampogas bought ~68% volumes on >2‑yr contracts (2024). Mediterranean export cuts (2022–24 +38%) drove spot volatility ±22%, while EU ETS rose to €80/t CO2 (2025), squeezing margins (EU LPG retailer gross ~7% Q3 2025).

| Metric | Value |

|---|---|

| Supply concentration | >70% |

| Major exporters share (2024) | ~35% |

| Long contracts (2024) | ~68% |

| Spot volatility (2022–24) | ±22% |

| EU ETS price (2025) | €80/t |

| Retail gross margin (Q3 2025) | ~7% |

What is included in the product

Tailored Porter's Five Forces for Lampogas SpA uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers that influence pricing, profitability, and market positioning.

Concise Porter's Five Forces snapshot for Lampogas SpA—instantly highlights competitive pressures and strategic levers to inform boardroom decisions.

Customers Bargaining Power

Fragmented Residential Customer Base

High Leverage of Industrial and Commercial Clients

Switching Costs and Contractual Ties

Domestic customers face switching costs because LPG storage tanks and regulators—often supplied and maintained by Lampogas SpA—require installation and certification; replacing them can cost €150–€400 per household and take 1–3 days.

Contracts commonly include exit fees or reimbursement clauses equal to 30–60% of equipment value, plus technical inspections; these barriers create measurable lock-in, limiting churn after minor price moves.

Price Transparency and Digital Comparison

By end-2025, Italian digital platforms and consumer groups raised energy price transparency; 72% of households used price comparison tools, per Autorità di Regolazione per Energia (ARERA), letting consumers directly compare Lampogas SpA tariffs with national and local rivals.

Better information lets small-scale customers demand promos or switch: Lampogas saw a 1.8% voluntary churn uptick in 2024–25 as comparison tools highlighted cheaper short-term offers.

Government Subsidies and Social Protection

In Italy, 2024 energy subsidies and social tariffs covered about 3.8 million households, lowering LPG effective prices and acting like customer bargaining power by capping what consumers pay and demand.

These policies constrain Lampogas SpA’s pricing freedom—with regulated support reducing price sensitivity in low-income segments and limiting margin-raising during supply shocks (Italy’s 2023 household energy aid budget was ~€5.2bn).

- 3.8M subsidized households (2024)

- €5.2bn energy aid (2023)

- Subsidies cap retail price pass-through

- Limits Lampogas’ pricing flexibility

Mixed customer power: low household leverage vs. dominant B2B accounts, subsidies cap pricing

Customers’ bargaining power is mixed: households (42% revenue in 2024; avg spend €420) have low individual leverage but rising transparency raised churn +1.8% (2024–25); top 10 B2B clients (>35% regional gas revenue) wield high leverage (single account €5–12M). Subsidies cover 3.8M households (2024), capping price pass-through and constraining Lampogas’ pricing freedom.

| Metric | 2023–25 |

|---|---|

| Household rev share | 42% |

| Avg household spend | €420 |

| Churn change | +1.8% |

| Top10 B2B rev | >35% |

| Subsidized households | 3.8M |

Full Version Awaits

Lampogas SpA Porter's Five Forces Analysis

This preview shows the exact Lampogas SpA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.