L'AMY Group S.A. (TWC L’AMY Group) Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

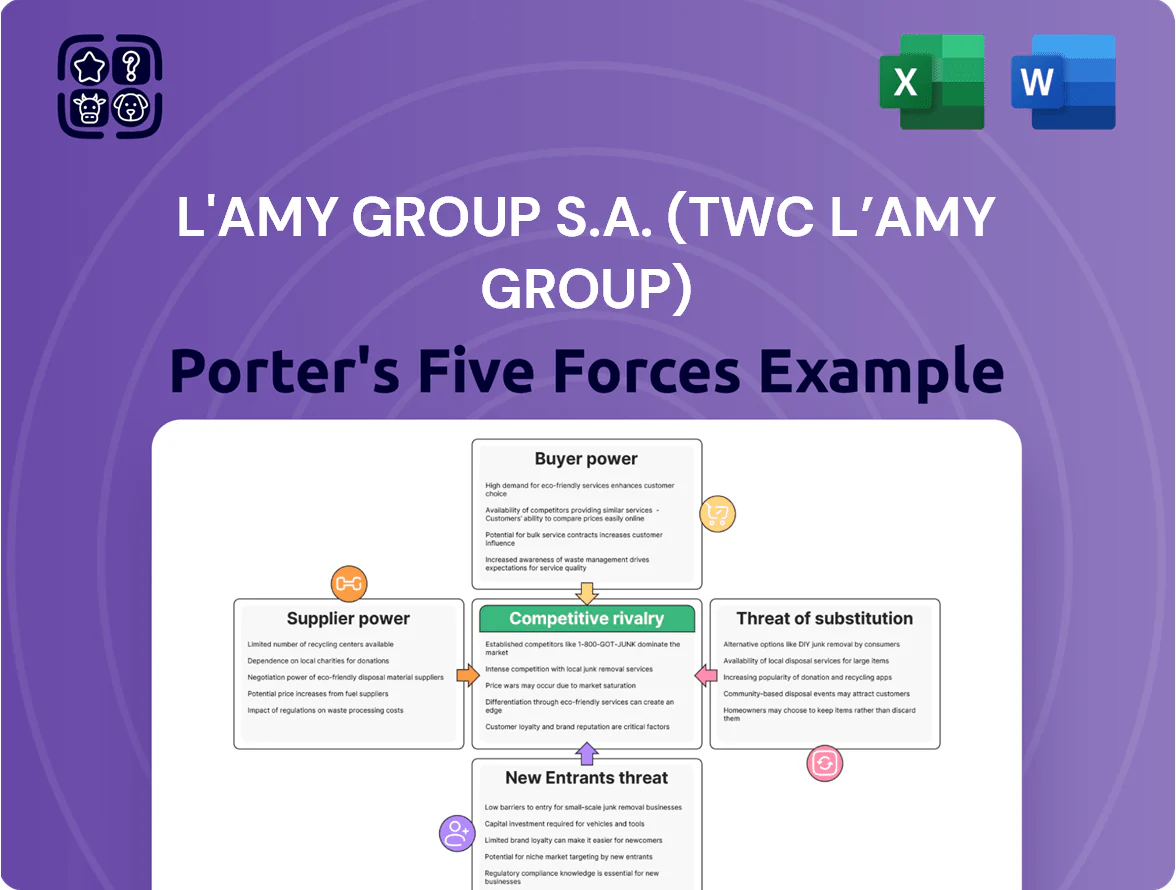

Suppliers Bargaining Power

Dependency on Brand Licensors

LAMY Group S.A. depends on licensing deals with major fashion houses for ~65% of FY2024 product revenue; licensors can set design specs, marketing spend and royalties at renewals, raising supplier bargaining power.

When a key license was lost in 2023, comparable peers saw 12–18% revenue dips; losing a major LAMY license could similarly cut group sales and weaken market position.

Concentration of Specialized Materials

Dominance of Lens Manufacturers

The global ophthalmic lens market is concentrated: EssilorLuxottica, Carl Zeiss Vision, Hoya and Nikon hold roughly 70% market share combined as of 2024, and many also sell frames, increasing their bargaining power over TWC L’AMY Group.

These suppliers control R&D in coatings and digital surfacing—EssilorLuxottica spent €1.3bn on R&D in 2023—so access to their tech is key for premium frame compatibility.

L’AMY must keep strategic supply and licensing ties, co-development deals, or volume guarantees to secure timely access and avoid margin erosion from supplier-driven price or spec changes.

Specialized Labor Costs

- Skilled artisan scarcity increases wage leverage

- France labor cost €36.8/hr (2024)

- Labor may be >25% of premium frame COGS

- Margin pressure on premium collections

Logistical Component Sensitivity

The supply chain for small components—screws, nose pads, specialty cases—is concentrated in industrial hubs like Shenzhen and Dongguan, where about 60% of eyewear fittings were produced in 2024.

Disruptions there (COVID-era port slowdowns cost 8–12% output loss in 2021) can stop L'AMY Group S.A. lines and delay exports to EU and MENA markets.

That concentration gives component makers indirect leverage over production timing and inventory costs; single-source parts raise supplier bargaining power.

- ~60% of fittings made in Shenzhen/Dongguan (2024)

- 8–12% output loss from past port disruptions

- Single-source parts increase schedule vulnerability

High supplier concentration, rising input & labor costs squeeze L’AMY margins

L’AMY faces high supplier power: ~65% FY2024 revenue tied to licensors; 10–15 global material suppliers; acetate prices +18% (2019–24), specialty titanium +12% p.a.; EssilorLuxottica, Zeiss, Hoya, Nikon = ~70% lens share (2024); France labor €36.8/hr (2024), labour >25% of premium COGS; ~60% fittings from Shenzhen/Dongguan (2024), past port slowdowns cut output 8–12% (2021).

| Metric | Value |

|---|---|

| Licensing rev | ~65% FY2024 |

| Material suppliers | 10–15 global |

| Acetate price change | +18% (2019–24) |

| Titanium premium | +12% p.a. |

| Lens market share (top4) | ~70% (2024) |

| France labor cost | €36.8/hr (2024) |

| Fittings origin | ~60% Shenzhen/Dongguan (2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for L'AMY Group S.A. (TWC L’AMY Group) that uncovers competitive intensity, buyer/supplier power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers affecting pricing and profitability.

A concise Porter's Five Forces one-sheet for TWC L’AMY Group that highlights supplier/customer leverage, competitive rivalry, threat of substitutes/entrants, and regulatory pressure—ideal for quick strategic decisions and slide-ready use.

Customers Bargaining Power

Consolidation of Optical Retail Chains

Large-scale retail groups and international optical chains now buy over 40% of global branded eyewear volume, giving them strong bargaining leverage through bulk purchasing.

They push for deeper discounts, extended payment terms (often 60–120 days), and exclusive marketing support, squeezing distributor margins and working capital.

As consolidation continues—top 5 chains account for ~35% of Western European optical sales—L'AMY faces fewer buyers who represent a larger share of its revenue, raising customer power and concentration risk.

Low Switching Costs for Opticians

Independent opticians and small boutiques can switch frame brands easily, driven by fashion cycles and margin offers; industry surveys show 68% of independents stock 10+ competing brands, raising churn risk for L'AMY Group.

Because most shops carry diverse brands, L'AMY must demonstrate sell-through: in 2024 average frame sell-through rates were ~4.2 units/month per SKU, so L'AMY needs stronger POS support and promotions.

Lack of retail exclusivity forces L'AMY to compete on service and price—wholesale margin pressure averaged 9–12% in EU independent channels in 2023—so superior after-sales and incentives matter.

Price Transparency for End Consumers

The rise of online price comparison and e-commerce has made end consumers sharply price-sensitive; 62% of US eyewear buyers used online price checks in 2024, forcing faster price matching across retailers and tighter distributor margins for L'AMY Group S.A. (TWC L’AMY Group).

Easy cross-retailer visibility of a specific frame’s price reduces retailers' tolerance for wholesale hikes, so L'AMY's ability to raise wholesale prices without denting retail volume is limited—retail markdowns rose 4.5% in 2024 in response.

Growth of Buying Groups

Small independent optical retailers are increasingly joining buying cooperatives; in Europe and the US, buying groups now represent about 22% of independents as of 2024, shrinking suppliers’ premium pricing space.

These cooperatives secure collective contracts that force manufacturers to offer bulk-buy rates to even tiny shops, cutting average unit margins by an estimated 150–300 basis points for suppliers like TWC LAMY Group in 2024.

Reduced pricing leverage across the independent channel lowers LAMY’s extractable profitability, pressuring revenue per account and pushing the company toward cost or volume responses to protect margins.

- Buying groups market share ~22% of independents (2024)

- Supplier margin pressure: –150 to –300 bps

- Impact: lower revenue per account, higher volume reliance

Demand for Digital Integration

Modern B2B buyers now expect real-time inventory checks and automated reordering; 68% of wholesale buyers (2024 Forrester survey) prefer suppliers with live stock data, raising switching risk for vendors without APIs.

Retailers favor suppliers offering seamless integration and virtual try-on; companies deploying AR/virtual fittings saw 30% higher conversion in apparel channels (2023 Shopify/Meta data), pressuring L'AMY to upgrade tech.

Absent these services, customers shift to tech-savvy rivals—estimated revenue at risk: 12–18% of L'AMY’s 2024 wholesale sales if integrations lag one year.

- 68% buyers prefer real-time inventory

- 30% higher conversion with virtual try-on

- 12–18% revenue at risk (2024 est.)

Channel consolidation and tech gaps threaten 12–18% revenue, squeezing margins ~150–300bps

Customers hold high bargaining power: large chains buy >40% global volume and top-5 chains ≈35% Western Europe (2024), pushing discounts, 60–120 day terms, and squeezing margins (~–150–300 bps). Independents stock 10+ brands (68%) and 22% join buying groups (2024), raising churn. Tech expectations (68% want real-time inventory) risk 12–18% of 2024 wholesale sales if LAMY lags.

| Metric | 2024 value |

|---|---|

| Chains share | >40% |

| Top-5 W.EU | ≈35% |

| Buying groups | 22% |

| Independents w/10+ brands | 68% |

| Margin pressure | –150–300 bps |

| Revenue at risk | 12–18% |

Preview Before You Purchase

L'AMY Group S.A. (TWC L’AMY Group) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis you'll receive for L'AMY Group S.A. (TWC L’AMY Group)—no placeholders or samples—fully formatted and ready for immediate download upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Dependency on Brand Licensors

LAMY Group S.A. depends on licensing deals with major fashion houses for ~65% of FY2024 product revenue; licensors can set design specs, marketing spend and royalties at renewals, raising supplier bargaining power.

When a key license was lost in 2023, comparable peers saw 12–18% revenue dips; losing a major LAMY license could similarly cut group sales and weaken market position.

Concentration of Specialized Materials

Dominance of Lens Manufacturers

The global ophthalmic lens market is concentrated: EssilorLuxottica, Carl Zeiss Vision, Hoya and Nikon hold roughly 70% market share combined as of 2024, and many also sell frames, increasing their bargaining power over TWC L’AMY Group.

These suppliers control R&D in coatings and digital surfacing—EssilorLuxottica spent €1.3bn on R&D in 2023—so access to their tech is key for premium frame compatibility.

L’AMY must keep strategic supply and licensing ties, co-development deals, or volume guarantees to secure timely access and avoid margin erosion from supplier-driven price or spec changes.

Specialized Labor Costs

- Skilled artisan scarcity increases wage leverage

- France labor cost €36.8/hr (2024)

- Labor may be >25% of premium frame COGS

- Margin pressure on premium collections

Logistical Component Sensitivity

The supply chain for small components—screws, nose pads, specialty cases—is concentrated in industrial hubs like Shenzhen and Dongguan, where about 60% of eyewear fittings were produced in 2024.

Disruptions there (COVID-era port slowdowns cost 8–12% output loss in 2021) can stop L'AMY Group S.A. lines and delay exports to EU and MENA markets.

That concentration gives component makers indirect leverage over production timing and inventory costs; single-source parts raise supplier bargaining power.

- ~60% of fittings made in Shenzhen/Dongguan (2024)

- 8–12% output loss from past port disruptions

- Single-source parts increase schedule vulnerability

High supplier concentration, rising input & labor costs squeeze L’AMY margins

L’AMY faces high supplier power: ~65% FY2024 revenue tied to licensors; 10–15 global material suppliers; acetate prices +18% (2019–24), specialty titanium +12% p.a.; EssilorLuxottica, Zeiss, Hoya, Nikon = ~70% lens share (2024); France labor €36.8/hr (2024), labour >25% of premium COGS; ~60% fittings from Shenzhen/Dongguan (2024), past port slowdowns cut output 8–12% (2021).

| Metric | Value |

|---|---|

| Licensing rev | ~65% FY2024 |

| Material suppliers | 10–15 global |

| Acetate price change | +18% (2019–24) |

| Titanium premium | +12% p.a. |

| Lens market share (top4) | ~70% (2024) |

| France labor cost | €36.8/hr (2024) |

| Fittings origin | ~60% Shenzhen/Dongguan (2024) |

What is included in the product

Tailored Porter’s Five Forces analysis for L'AMY Group S.A. (TWC L’AMY Group) that uncovers competitive intensity, buyer/supplier power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers affecting pricing and profitability.

A concise Porter's Five Forces one-sheet for TWC L’AMY Group that highlights supplier/customer leverage, competitive rivalry, threat of substitutes/entrants, and regulatory pressure—ideal for quick strategic decisions and slide-ready use.

Customers Bargaining Power

Consolidation of Optical Retail Chains

Large-scale retail groups and international optical chains now buy over 40% of global branded eyewear volume, giving them strong bargaining leverage through bulk purchasing.

They push for deeper discounts, extended payment terms (often 60–120 days), and exclusive marketing support, squeezing distributor margins and working capital.

As consolidation continues—top 5 chains account for ~35% of Western European optical sales—L'AMY faces fewer buyers who represent a larger share of its revenue, raising customer power and concentration risk.

Low Switching Costs for Opticians

Independent opticians and small boutiques can switch frame brands easily, driven by fashion cycles and margin offers; industry surveys show 68% of independents stock 10+ competing brands, raising churn risk for L'AMY Group.

Because most shops carry diverse brands, L'AMY must demonstrate sell-through: in 2024 average frame sell-through rates were ~4.2 units/month per SKU, so L'AMY needs stronger POS support and promotions.

Lack of retail exclusivity forces L'AMY to compete on service and price—wholesale margin pressure averaged 9–12% in EU independent channels in 2023—so superior after-sales and incentives matter.

Price Transparency for End Consumers

The rise of online price comparison and e-commerce has made end consumers sharply price-sensitive; 62% of US eyewear buyers used online price checks in 2024, forcing faster price matching across retailers and tighter distributor margins for L'AMY Group S.A. (TWC L’AMY Group).

Easy cross-retailer visibility of a specific frame’s price reduces retailers' tolerance for wholesale hikes, so L'AMY's ability to raise wholesale prices without denting retail volume is limited—retail markdowns rose 4.5% in 2024 in response.

Growth of Buying Groups

Small independent optical retailers are increasingly joining buying cooperatives; in Europe and the US, buying groups now represent about 22% of independents as of 2024, shrinking suppliers’ premium pricing space.

These cooperatives secure collective contracts that force manufacturers to offer bulk-buy rates to even tiny shops, cutting average unit margins by an estimated 150–300 basis points for suppliers like TWC LAMY Group in 2024.

Reduced pricing leverage across the independent channel lowers LAMY’s extractable profitability, pressuring revenue per account and pushing the company toward cost or volume responses to protect margins.

- Buying groups market share ~22% of independents (2024)

- Supplier margin pressure: –150 to –300 bps

- Impact: lower revenue per account, higher volume reliance

Demand for Digital Integration

Modern B2B buyers now expect real-time inventory checks and automated reordering; 68% of wholesale buyers (2024 Forrester survey) prefer suppliers with live stock data, raising switching risk for vendors without APIs.

Retailers favor suppliers offering seamless integration and virtual try-on; companies deploying AR/virtual fittings saw 30% higher conversion in apparel channels (2023 Shopify/Meta data), pressuring L'AMY to upgrade tech.

Absent these services, customers shift to tech-savvy rivals—estimated revenue at risk: 12–18% of L'AMY’s 2024 wholesale sales if integrations lag one year.

- 68% buyers prefer real-time inventory

- 30% higher conversion with virtual try-on

- 12–18% revenue at risk (2024 est.)

Channel consolidation and tech gaps threaten 12–18% revenue, squeezing margins ~150–300bps

Customers hold high bargaining power: large chains buy >40% global volume and top-5 chains ≈35% Western Europe (2024), pushing discounts, 60–120 day terms, and squeezing margins (~–150–300 bps). Independents stock 10+ brands (68%) and 22% join buying groups (2024), raising churn. Tech expectations (68% want real-time inventory) risk 12–18% of 2024 wholesale sales if LAMY lags.

| Metric | 2024 value |

|---|---|

| Chains share | >40% |

| Top-5 W.EU | ≈35% |

| Buying groups | 22% |

| Independents w/10+ brands | 68% |

| Margin pressure | –150–300 bps |

| Revenue at risk | 12–18% |

Preview Before You Purchase

L'AMY Group S.A. (TWC L’AMY Group) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis you'll receive for L'AMY Group S.A. (TWC L’AMY Group)—no placeholders or samples—fully formatted and ready for immediate download upon purchase.