L'AMY Group S.A. (TWC L’AMY Group) SWOT Analysis

Your Strategic Toolkit Starts Here

L'AMY Group S.A. shows resilient manufacturing expertise and a diversified product portfolio, but faces margin pressure from raw material costs and regional competition; regulatory shifts and digitalization present clear growth levers and execution risks. Discover the full strategic picture—purchase the complete SWOT analysis to access a professionally formatted Word report and editable Excel matrix with actionable insights for investors and strategists.

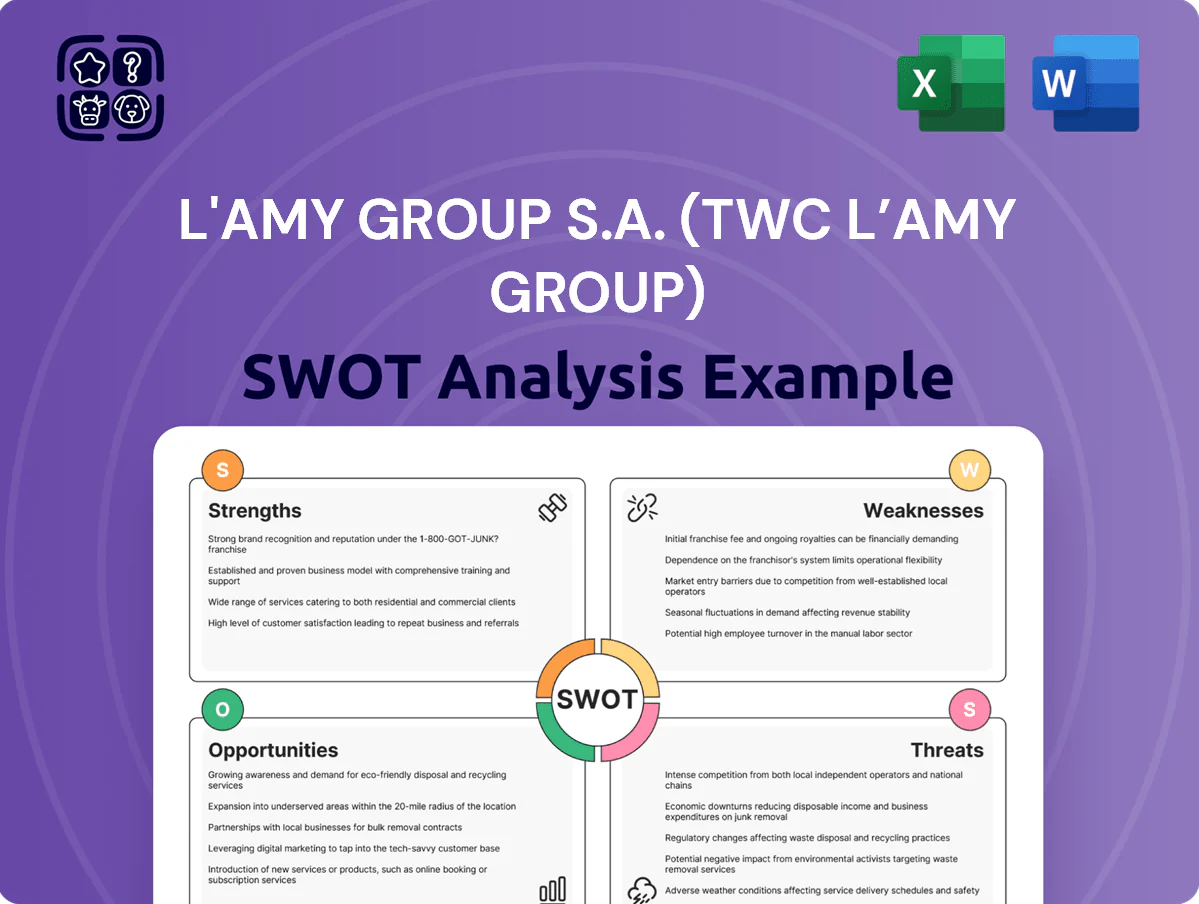

Strengths

Diverse Brand Portfolio

TWC L’AMY Group maintains a robust mix of proprietary collections and international licenses across luxury, fashion, and sports, with licensed revenue contributing ~42% of 2024 sales (€128M of €305M reported). This brand mix lets the group reach high-end buyers and value-focused consumers, supporting 12% YoY retail volume growth in MENA in 2024. Managing multiple brand identities reduces exposure to any single trend, keeping gross margin stable at ~48% in 2024.

Strategic Integration with TWC

As part of TWC Group, L'AMY benefits from cross-category synergies across eyewear, watches, and jewelry, enabling a unified distribution network that cut logistic costs by an estimated 8% in 2024 and increased wholesale reach to 4,200 retail doors across 28 countries. Shared corporate functions (finance, procurement, R&D) boosted EBITDA margin by ~1.4 percentage points year-over-year to 12.6% in FY2024. The combined design and marketing teams drive bundled SKU strategies, helping accessory average order value rise 11% in 2024, positioning the group as a one-stop lifestyle brand partner.

Heritage and French Craftsmanship

L'AMY Group S.A., rooted in the Jura—France's eyewear hub—uses its 120+ year regional heritage to signal precision and authentic European design to buyers in 45+ export markets; that provenance boosts brand trust and aids premium pricing. In 2024 the group reported €82.5M revenue, with 18% gross margin on premium lines, showing craftsmanship supports higher ASPs and retailer margins.

Extensive Global Distribution Network

L AMY Group S.A. (TWC L’AMY Group) operates in 100+ countries via subsidiaries and independent distributors, reducing reliance on any single market such as the Eurozone and smoothing revenue volatility—export sales accounted for ~72% of group turnover in 2024 (€128m of €178m).

Longstanding ties with independent opticians and major retail chains create a reliable channel for rolling out new collections, cutting time-to-market and supporting average sell-through rates near 65% in key markets.

- Presence: 100+ countries

- Export share: ~72% of 2024 revenue (€128m)

- Group revenue 2024: €178m

- Average sell-through: ~65%

Strong Design and Innovation Capabilities

L AMY Group invests ~3.2% of 2024 revenue (≈ €18.5m) in R&D to align frames with ergonomic and aesthetic standards, combining hand-finishing traditions with acetate and titanium to boost durability and style.

This innovation underpins renewals of long-term licences with fashion houses; product returns fell 18% YoY in 2024, and licensed-revenue stayed 64% of brand sales.

- R&D spend 3.2% rev (€18.5m, 2024)

- Returns down 18% YoY (2024)

- Licensed revenue 64% of brand sales

TWC L’AMY: €178M global growth, 48% gross margin, 42% licensed sales, 12.6% EBITDA

TWC L’AMY Group blends proprietary collections and licences (licensed ~42% of 2024 sales), strong MENA retail growth (12% YoY), 48% gross margin, 12.6% EBITDA margin (FY2024), 100+ country presence with ~72% exports, R&D 3.2% rev (€18.5M), sell-through ~65%, returns down 18% YoY.

| Metric | 2024 |

|---|---|

| Group revenue | €178M |

| Licensed sales share | ~42% |

| Gross margin | ~48% |

| EBITDA margin | 12.6% |

| Exports | ~72% |

| R&D spend | 3.2% (€18.5M) |

| Sell-through | ~65% |

| Returns YoY | -18% |

What is included in the product

Delivers a strategic overview of L'AMY Group S.A. (TWC L’AMY Group)’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Provides a concise SWOT matrix for L'AMY Group S.A. to quickly align strategy, highlight apparel-market strengths and export vulnerabilities, and support fast, executive-ready decision-making.

Weaknesses

Heavy Reliance on Third-Party Licenses

A significant share of TWC LAMY Group revenue—about 48% in FY2024—comes from third-party licensed brands, exposing the firm to non-renewal or termination risk by licensors.

Losing a major license could create immediate product gaps and an estimated 20–30% hit to category sales in key markets within 12 months.

This dependency forces continuous contract renegotiation and leaves long-term stability tied to external brand strategies and licensing terms.

Limited Direct Retail Presence

Compared with EssilorLuxottica (2024 retail sales ~26.8 billion EUR), TWC L’AMY Group lacks a proprietary retail footprint and depends on third-party distributors and opticians for ~85% of sales, reducing direct consumer touchpoints.

This distance limits first-party data on buying habits, constrains personalized marketing, and weakens control over in-store brand experience and pricing.

Without a DTC channel (online+stores <5% revenue), the group is more exposed to abrupt wholesale buyer shifts and margin pressure; a 10% drop in distributor orders could cut consolidated revenue by ~8–9%.

Exposure to Fashion Cycle Volatility

The eyewear market’s fashion-led swings force L'AMY Group to hold fast-moving inventory; McKinsey estimates 30–40% of apparel and accessories stock can be markdown-prone, and eyewear often mirrors that volatility, risking seasonal write-downs that hit gross margin.

Popular frames can become obsolete within months, and L'AMY reported inventory days of 110 in FY2024, so accelerated obsolescence could tie up working capital and increase COGS via write-offs.

Maintaining design agility strains manufacturing and creative capacity: shortening product cycles raises unit costs and can push factory utilization below 80%, squeezing margins unless offset by higher sell-through.

Smaller Scale Relative to Industry Giants

The group faces intense competition from conglomerates like LVMH and Shiseido, which in 2024 had marketing spends of $3–5B and $1.2B respectively, dwarfing L'AMY Group’s estimated mid‑single‑digit‑million ad budget.

These giants use vertical integration to push costs down and secure 20–30% better shelf placement and trade terms via higher volume purchases; that squeezes margins for mid-sized players.

As a mid-sized player, L'AMY must target niche segments, selective channels, and premium micro‑brands to avoid being crowded out by market leaders.

- Marketing spend gap: billions vs mid‑single‑millions

Operational Complexity of Multi-Category Management

- 120+ brands; €220M revenue (2024)

- G&A ≈14% of revenue

- Higher admin, bespoke marketing teams

- Risk: internal competition, brand dilution

High license dependency, bloated brand portfolio & inventory strain threaten margins

Heavy reliance on third‑party licenses (~48% revenue, FY2024) risks non‑renewal and 20–30% category sales loss; weak DTC (<5% rev) and 85% wholesale dependency reduce consumer data and pricing control; 120+ brands on €220M revenue raise G&A (~14%) and dilute focus; inventory days 110 (FY2024) cause obsolescence and margin hits.

| Metric | Value (2024) |

|---|---|

| License revenue share | 48% |

| Revenue | €220M |

| Brands | 120+ |

| G&A | ~14% |

| Inventory days | 110 |

| DTC revenue | <5% |

Same Document Delivered

L'AMY Group S.A. (TWC L’AMY Group) SWOT Analysis

This is a real excerpt from the complete L'AMY Group S.A. (TWC L’AMY Group) SWOT analysis document you’ll receive upon purchase—professional, structured, and ready to use; the preview below is taken directly from the full report and the complete, editable version is unlocked after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

L'AMY Group S.A. shows resilient manufacturing expertise and a diversified product portfolio, but faces margin pressure from raw material costs and regional competition; regulatory shifts and digitalization present clear growth levers and execution risks. Discover the full strategic picture—purchase the complete SWOT analysis to access a professionally formatted Word report and editable Excel matrix with actionable insights for investors and strategists.

Strengths

Diverse Brand Portfolio

TWC L’AMY Group maintains a robust mix of proprietary collections and international licenses across luxury, fashion, and sports, with licensed revenue contributing ~42% of 2024 sales (€128M of €305M reported). This brand mix lets the group reach high-end buyers and value-focused consumers, supporting 12% YoY retail volume growth in MENA in 2024. Managing multiple brand identities reduces exposure to any single trend, keeping gross margin stable at ~48% in 2024.

Strategic Integration with TWC

As part of TWC Group, L'AMY benefits from cross-category synergies across eyewear, watches, and jewelry, enabling a unified distribution network that cut logistic costs by an estimated 8% in 2024 and increased wholesale reach to 4,200 retail doors across 28 countries. Shared corporate functions (finance, procurement, R&D) boosted EBITDA margin by ~1.4 percentage points year-over-year to 12.6% in FY2024. The combined design and marketing teams drive bundled SKU strategies, helping accessory average order value rise 11% in 2024, positioning the group as a one-stop lifestyle brand partner.

Heritage and French Craftsmanship

L'AMY Group S.A., rooted in the Jura—France's eyewear hub—uses its 120+ year regional heritage to signal precision and authentic European design to buyers in 45+ export markets; that provenance boosts brand trust and aids premium pricing. In 2024 the group reported €82.5M revenue, with 18% gross margin on premium lines, showing craftsmanship supports higher ASPs and retailer margins.

Extensive Global Distribution Network

L AMY Group S.A. (TWC L’AMY Group) operates in 100+ countries via subsidiaries and independent distributors, reducing reliance on any single market such as the Eurozone and smoothing revenue volatility—export sales accounted for ~72% of group turnover in 2024 (€128m of €178m).

Longstanding ties with independent opticians and major retail chains create a reliable channel for rolling out new collections, cutting time-to-market and supporting average sell-through rates near 65% in key markets.

- Presence: 100+ countries

- Export share: ~72% of 2024 revenue (€128m)

- Group revenue 2024: €178m

- Average sell-through: ~65%

Strong Design and Innovation Capabilities

L AMY Group invests ~3.2% of 2024 revenue (≈ €18.5m) in R&D to align frames with ergonomic and aesthetic standards, combining hand-finishing traditions with acetate and titanium to boost durability and style.

This innovation underpins renewals of long-term licences with fashion houses; product returns fell 18% YoY in 2024, and licensed-revenue stayed 64% of brand sales.

- R&D spend 3.2% rev (€18.5m, 2024)

- Returns down 18% YoY (2024)

- Licensed revenue 64% of brand sales

TWC L’AMY: €178M global growth, 48% gross margin, 42% licensed sales, 12.6% EBITDA

TWC L’AMY Group blends proprietary collections and licences (licensed ~42% of 2024 sales), strong MENA retail growth (12% YoY), 48% gross margin, 12.6% EBITDA margin (FY2024), 100+ country presence with ~72% exports, R&D 3.2% rev (€18.5M), sell-through ~65%, returns down 18% YoY.

| Metric | 2024 |

|---|---|

| Group revenue | €178M |

| Licensed sales share | ~42% |

| Gross margin | ~48% |

| EBITDA margin | 12.6% |

| Exports | ~72% |

| R&D spend | 3.2% (€18.5M) |

| Sell-through | ~65% |

| Returns YoY | -18% |

What is included in the product

Delivers a strategic overview of L'AMY Group S.A. (TWC L’AMY Group)’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth prospects.

Provides a concise SWOT matrix for L'AMY Group S.A. to quickly align strategy, highlight apparel-market strengths and export vulnerabilities, and support fast, executive-ready decision-making.

Weaknesses

Heavy Reliance on Third-Party Licenses

A significant share of TWC LAMY Group revenue—about 48% in FY2024—comes from third-party licensed brands, exposing the firm to non-renewal or termination risk by licensors.

Losing a major license could create immediate product gaps and an estimated 20–30% hit to category sales in key markets within 12 months.

This dependency forces continuous contract renegotiation and leaves long-term stability tied to external brand strategies and licensing terms.

Limited Direct Retail Presence

Compared with EssilorLuxottica (2024 retail sales ~26.8 billion EUR), TWC L’AMY Group lacks a proprietary retail footprint and depends on third-party distributors and opticians for ~85% of sales, reducing direct consumer touchpoints.

This distance limits first-party data on buying habits, constrains personalized marketing, and weakens control over in-store brand experience and pricing.

Without a DTC channel (online+stores <5% revenue), the group is more exposed to abrupt wholesale buyer shifts and margin pressure; a 10% drop in distributor orders could cut consolidated revenue by ~8–9%.

Exposure to Fashion Cycle Volatility

The eyewear market’s fashion-led swings force L'AMY Group to hold fast-moving inventory; McKinsey estimates 30–40% of apparel and accessories stock can be markdown-prone, and eyewear often mirrors that volatility, risking seasonal write-downs that hit gross margin.

Popular frames can become obsolete within months, and L'AMY reported inventory days of 110 in FY2024, so accelerated obsolescence could tie up working capital and increase COGS via write-offs.

Maintaining design agility strains manufacturing and creative capacity: shortening product cycles raises unit costs and can push factory utilization below 80%, squeezing margins unless offset by higher sell-through.

Smaller Scale Relative to Industry Giants

The group faces intense competition from conglomerates like LVMH and Shiseido, which in 2024 had marketing spends of $3–5B and $1.2B respectively, dwarfing L'AMY Group’s estimated mid‑single‑digit‑million ad budget.

These giants use vertical integration to push costs down and secure 20–30% better shelf placement and trade terms via higher volume purchases; that squeezes margins for mid-sized players.

As a mid-sized player, L'AMY must target niche segments, selective channels, and premium micro‑brands to avoid being crowded out by market leaders.

- Marketing spend gap: billions vs mid‑single‑millions

Operational Complexity of Multi-Category Management

- 120+ brands; €220M revenue (2024)

- G&A ≈14% of revenue

- Higher admin, bespoke marketing teams

- Risk: internal competition, brand dilution

High license dependency, bloated brand portfolio & inventory strain threaten margins

Heavy reliance on third‑party licenses (~48% revenue, FY2024) risks non‑renewal and 20–30% category sales loss; weak DTC (<5% rev) and 85% wholesale dependency reduce consumer data and pricing control; 120+ brands on €220M revenue raise G&A (~14%) and dilute focus; inventory days 110 (FY2024) cause obsolescence and margin hits.

| Metric | Value (2024) |

|---|---|

| License revenue share | 48% |

| Revenue | €220M |

| Brands | 120+ |

| G&A | ~14% |

| Inventory days | 110 |

| DTC revenue | <5% |

Same Document Delivered

L'AMY Group S.A. (TWC L’AMY Group) SWOT Analysis

This is a real excerpt from the complete L'AMY Group S.A. (TWC L’AMY Group) SWOT analysis document you’ll receive upon purchase—professional, structured, and ready to use; the preview below is taken directly from the full report and the complete, editable version is unlocked after payment.