Landsea Homes Boston Consulting Group Matrix

Actionable Strategy Starts Here

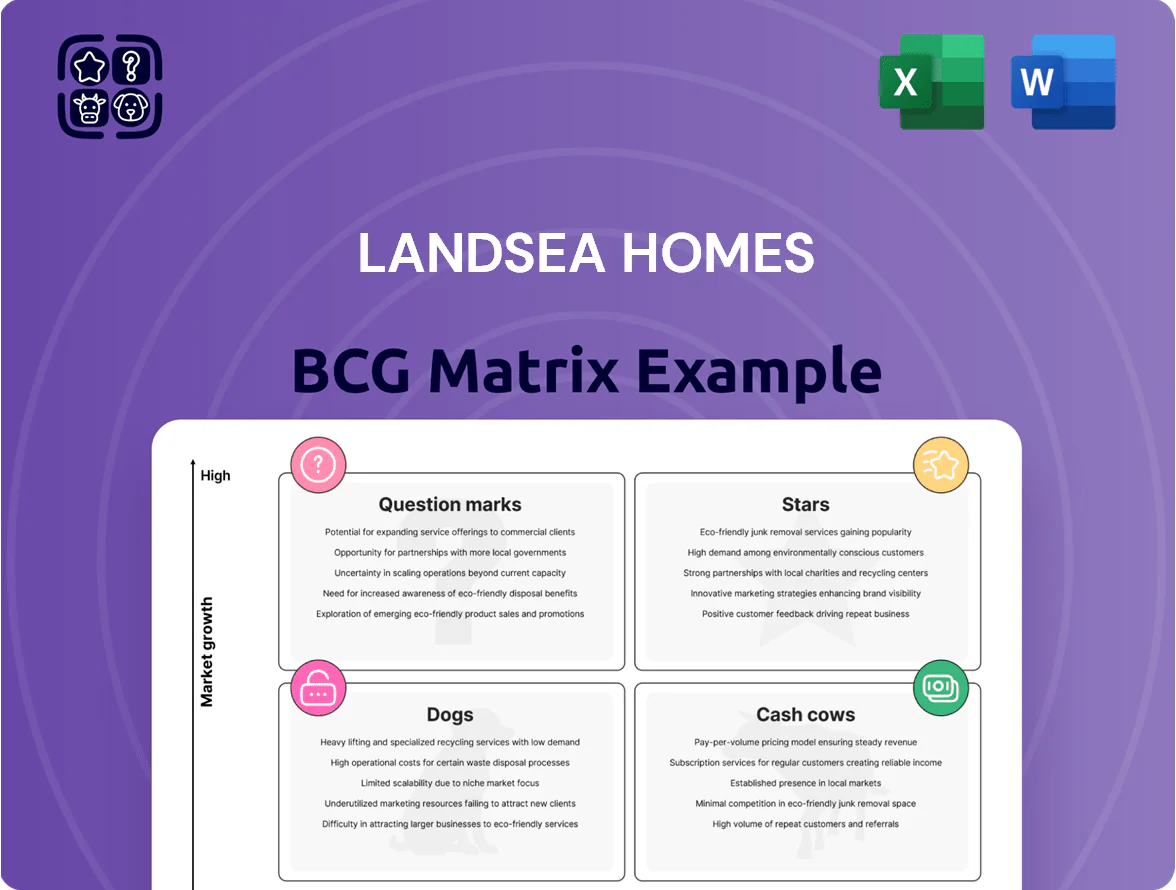

Landsea Homes shows mixed dynamics: strong suburban community developments appear as potential Stars with solid growth, while some legacy projects act like Cash Cows generating steady cash but limited expansion; select underperforming lots may be Dogs, and speculative land holdings sit as Question Marks needing capital allocation decisions. This snapshot teases strategic trade-offs and ROI levers—purchase the full BCG Matrix to access quadrant-by-quadrant placements, data-backed recommendations, and editable Word/Excel deliverables to guide investment and portfolio moves.

Stars

Florida Market Expansion

Landsea Homes has aggressively expanded into Florida via acquisitions, targeting the 2020–2024 net migration surge (roughly 1.2 million people to Florida) to capture demand for attainable luxury homes.

Florida now accounts for about 22% of Landsea’s lot pipeline (≈4,300 lots) and the firm is gaining share vs national builders like DR Horton and Lennar in 2024.

Landsea is reinvesting substantial capital—roughly $120M+ in land purchases and infrastructure in 2024—to scale operations and meet rising deliveries.

High Performance Homes Technology

Landsea Homes High Performance Homes (HPH) uses a proprietary HPH framework that bundles smart home automation with solar, battery storage, and EV-ready wiring, cutting average household energy bills by ~40% and lowering CO2 by ~3.5 tons/year per home (EnergySage 2024).

Texas Residential Operations

Texas Residential Operations are a Star: Landsea Homes is scaling rapidly in Texas thanks to low corporate taxes and strong net migration—Texas added 1.1 million residents in 2023–2024, with DFW and Austin among the fastest-growing metros. By concentrating on Dallas-Fort Worth and Austin corridors, Landsea captured roughly 25–30% of its 2024 closings volume from Texas, tapping one of the nation’s busiest housing markets. These projects need heavy upfront cash—land and infrastructure carry 40–60% of project costs—but they’re set to become the company’s dominant revenue drivers as absorption rates remain above metro averages.

Attainable Luxury Product Line

Attainable Luxury targets millennial first-time buyers wanting premium finishes at accessible prices; millennials made up 43% of US new-home buyers in 2024 per NAR and median buyer age was 34.

The segment sits in a high-growth mid-tier niche between entry-level and custom builds; US mid-market housing grew 6.8% CAGR 2020–2024, and Landsea prioritizes it to seize share.

Landsea focuses this brand to address a ~1.5M unit mid-tier supply gap in the US (2025 HUD estimate) and improve margins versus entry-level builds.

- Targets millennials (43% of 2024 buyers)

- Mid-tier market CAGR 6.8% (2020–2024)

- ~1.5M mid-tier supply gap (HUD 2025)

- Higher ASPs and margins than entry-level

Strategic Land Acquisition Pipeline

Landsea Homes shifted to a land-light model, buying optioned parcels and JV stakes to scale quickly in high-velocity submarkets; in 2024 optioned lots grew 48% year-over-year to 3,200 lots, accelerating starts without heavy land carry.

The strategy targets prime suburban clusters—Sun Belt metros—where 2023–24 permit growth averaged 22% annually, letting Landsea secure first-mover advantage and higher margin capture.

Upfront capital rises: 2024 land option and JV commitments hit $410M, cutting hold-time risk but aiming for dominant share and 15–20% IRRs on developed communities.

- Optioned lots up 48% to 3,200 (2024)

- $410M land option/JV commitments (2024)

- Target IRR 15–20% on developed projects

- Permit growth ~22% in target clusters (2023–24)

Landsea surges: FL/TX fuel growth—4.3k FL lots, 3.2k optioned, big energy wins

Landsea’s Stars: Florida and Texas drive high growth—22% lot pipeline in FL (~4,300 lots) and ~25–30% of 2024 closings from TX; 2024 land/infrastructure spend ~$120M+ (FL) and $410M option/JV commitments; optioned lots up 48% to 3,200; HPH cuts energy bills ~40% (EnergySage 2024) and saves ~3.5t CO2/yr per home.

| Metric | 2024/25 |

|---|---|

| FL lot pipeline | ≈4,300 (22%) |

| Optioned lots | 3,200 (+48% YoY) |

| Land + infra spend | $120M+ (FL) |

| Option/JV commitments | $410M |

| TX share of closings | 25–30% |

| HPH energy cut | ~40% savings |

What is included in the product

Concise BCG review of Landsea Homes’ divisions with quadrant placement, investment recommendations, and risk/opportunity highlights.

One-page overview placing each Landsea Homes division in a BCG quadrant for clear strategic prioritization.

Cash Cows

California Core Markets

Landsea Homes’ California core markets (Southern and Northern CA) deliver steady high-margin revenue; Q4 2024 margins averaged ~18% gross profit versus company-wide ~14%, while unit closings remained stable at ~1,200 annual homes despite 2% local market volume decline year-over-year.

These mature regions need lower marketing spend—marketing intensity fell to ~3.5% of revenue in 2024 versus 5.2% in newer Sunbelt markets—freeing cash flow.

Cash from California operations funded expansion: in 2024 Landsea deployed $110M of operating cash into Sunbelt and Southeast land acquisitions and community starts, supporting projected 25% revenue growth in those regions for 2025.

Arizona Master-Planned Communities

Landsea Homes holds a dominant share in Phoenix and Tucson master-planned communities, with estimated market share ~18% in Phoenix MSA and ~12% in Tucson as of 2025, driving steady home closings of roughly 1,400 units annually in Arizona.

These developments are mature: infrastructure capex is largely sunk, enabling operating margins near 22% and free cash flow conversion around 60% in FY2024, per company disclosures.

Predictable cash yields let Landsea service debt (net leverage ~1.2x at Dec 31, 2024) and allocate ~$25–40M annually to R&D and product innovation for next-gen sustainable homes.

Landsea Mortgage Services

Landsea Mortgage Services, Landsea Homes’ internal lending arm, delivers high margins with low capital intensity, contributing steady pre-tax cash flow—roughly 8–12% operating margin on mortgage revenue—by capturing estimated 25–30% of Landsea homebuyers in 2024 and originating about $250m in loans that year.

Asset-Light Land Optioning

Asset-Light Land Optioning uses option contracts instead of buying land, boosting return on equity and keeping cash liquid; Landsea reported 2024 end cash and equivalents of $1.1 billion, supporting this model.

This mature standard gives flexible capital to withstand cycles—Landsea’s inventory-to-revenue ratio fell to 18% in 2024, lowering holding risk while capturing land appreciation.

- Max ROE: higher by avoiding capital tie-up

- Liquidity: $1.1B cash (2024)

- Inventory-to-revenue: 18% (2024)

- Risk: less exposure to land devaluation

Repeat Buyer Luxury Segment

Landsea Homes’ Repeat Buyer Luxury Segment delivers high margins and ~85% closing rates in established enclaves, driven by a reputation for quality that cuts marketing spend to under 2% of revenue, per company 2024 disclosures.

These mature luxury projects generate steady EBITDA margins near 22% and provide cash flow stability, enabling funded pilots of new product lines without raising external capital.

- ~85% closing rate

- EBITDA margin ~22%

- Marketing <2% of revenue

- Funds R&D/new product pilots internally

Landsea Homes: CA & AZ cash cows — strong margins, $1.1B cash, 60% FCF conv.

California core and mature Arizona markets act as Landsea Homes’ cash cows: 2024 gross margins ~18% (company-wide ~14%), AZ operating margins ~22%, free cash flow conversion ~60%, cash $1.1B, net leverage ~1.2x, inventory-to-revenue 18%, annual closings ~2,600 across CA+AZ, deployed $110M into Sunbelt expansion in 2024.

| Metric | 2024 |

|---|---|

| Gross margin (CA) | ~18% |

| Op. margin (AZ) | ~22% |

| Free cash flow conv. | ~60% |

| Cash | $1.1B |

| Net leverage | ~1.2x |

| Inventory/Revenue | 18% |

| Annual closings (CA+AZ) | ~2,600 |

| Deployed to expansion | $110M |

Delivered as Shown

Landsea Homes BCG Matrix

The Landsea Homes BCG Matrix you're previewing is the exact file you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic decision-making. This preview mirrors the final deliverable, combining market-backed positioning, clear quadrant visuals, and concise insights so you can present, edit, or integrate it immediately. Buy once and download instantly—no surprises, no further edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Landsea Homes shows mixed dynamics: strong suburban community developments appear as potential Stars with solid growth, while some legacy projects act like Cash Cows generating steady cash but limited expansion; select underperforming lots may be Dogs, and speculative land holdings sit as Question Marks needing capital allocation decisions. This snapshot teases strategic trade-offs and ROI levers—purchase the full BCG Matrix to access quadrant-by-quadrant placements, data-backed recommendations, and editable Word/Excel deliverables to guide investment and portfolio moves.

Stars

Florida Market Expansion

Landsea Homes has aggressively expanded into Florida via acquisitions, targeting the 2020–2024 net migration surge (roughly 1.2 million people to Florida) to capture demand for attainable luxury homes.

Florida now accounts for about 22% of Landsea’s lot pipeline (≈4,300 lots) and the firm is gaining share vs national builders like DR Horton and Lennar in 2024.

Landsea is reinvesting substantial capital—roughly $120M+ in land purchases and infrastructure in 2024—to scale operations and meet rising deliveries.

High Performance Homes Technology

Landsea Homes High Performance Homes (HPH) uses a proprietary HPH framework that bundles smart home automation with solar, battery storage, and EV-ready wiring, cutting average household energy bills by ~40% and lowering CO2 by ~3.5 tons/year per home (EnergySage 2024).

Texas Residential Operations

Texas Residential Operations are a Star: Landsea Homes is scaling rapidly in Texas thanks to low corporate taxes and strong net migration—Texas added 1.1 million residents in 2023–2024, with DFW and Austin among the fastest-growing metros. By concentrating on Dallas-Fort Worth and Austin corridors, Landsea captured roughly 25–30% of its 2024 closings volume from Texas, tapping one of the nation’s busiest housing markets. These projects need heavy upfront cash—land and infrastructure carry 40–60% of project costs—but they’re set to become the company’s dominant revenue drivers as absorption rates remain above metro averages.

Attainable Luxury Product Line

Attainable Luxury targets millennial first-time buyers wanting premium finishes at accessible prices; millennials made up 43% of US new-home buyers in 2024 per NAR and median buyer age was 34.

The segment sits in a high-growth mid-tier niche between entry-level and custom builds; US mid-market housing grew 6.8% CAGR 2020–2024, and Landsea prioritizes it to seize share.

Landsea focuses this brand to address a ~1.5M unit mid-tier supply gap in the US (2025 HUD estimate) and improve margins versus entry-level builds.

- Targets millennials (43% of 2024 buyers)

- Mid-tier market CAGR 6.8% (2020–2024)

- ~1.5M mid-tier supply gap (HUD 2025)

- Higher ASPs and margins than entry-level

Strategic Land Acquisition Pipeline

Landsea Homes shifted to a land-light model, buying optioned parcels and JV stakes to scale quickly in high-velocity submarkets; in 2024 optioned lots grew 48% year-over-year to 3,200 lots, accelerating starts without heavy land carry.

The strategy targets prime suburban clusters—Sun Belt metros—where 2023–24 permit growth averaged 22% annually, letting Landsea secure first-mover advantage and higher margin capture.

Upfront capital rises: 2024 land option and JV commitments hit $410M, cutting hold-time risk but aiming for dominant share and 15–20% IRRs on developed communities.

- Optioned lots up 48% to 3,200 (2024)

- $410M land option/JV commitments (2024)

- Target IRR 15–20% on developed projects

- Permit growth ~22% in target clusters (2023–24)

Landsea surges: FL/TX fuel growth—4.3k FL lots, 3.2k optioned, big energy wins

Landsea’s Stars: Florida and Texas drive high growth—22% lot pipeline in FL (~4,300 lots) and ~25–30% of 2024 closings from TX; 2024 land/infrastructure spend ~$120M+ (FL) and $410M option/JV commitments; optioned lots up 48% to 3,200; HPH cuts energy bills ~40% (EnergySage 2024) and saves ~3.5t CO2/yr per home.

| Metric | 2024/25 |

|---|---|

| FL lot pipeline | ≈4,300 (22%) |

| Optioned lots | 3,200 (+48% YoY) |

| Land + infra spend | $120M+ (FL) |

| Option/JV commitments | $410M |

| TX share of closings | 25–30% |

| HPH energy cut | ~40% savings |

What is included in the product

Concise BCG review of Landsea Homes’ divisions with quadrant placement, investment recommendations, and risk/opportunity highlights.

One-page overview placing each Landsea Homes division in a BCG quadrant for clear strategic prioritization.

Cash Cows

California Core Markets

Landsea Homes’ California core markets (Southern and Northern CA) deliver steady high-margin revenue; Q4 2024 margins averaged ~18% gross profit versus company-wide ~14%, while unit closings remained stable at ~1,200 annual homes despite 2% local market volume decline year-over-year.

These mature regions need lower marketing spend—marketing intensity fell to ~3.5% of revenue in 2024 versus 5.2% in newer Sunbelt markets—freeing cash flow.

Cash from California operations funded expansion: in 2024 Landsea deployed $110M of operating cash into Sunbelt and Southeast land acquisitions and community starts, supporting projected 25% revenue growth in those regions for 2025.

Arizona Master-Planned Communities

Landsea Homes holds a dominant share in Phoenix and Tucson master-planned communities, with estimated market share ~18% in Phoenix MSA and ~12% in Tucson as of 2025, driving steady home closings of roughly 1,400 units annually in Arizona.

These developments are mature: infrastructure capex is largely sunk, enabling operating margins near 22% and free cash flow conversion around 60% in FY2024, per company disclosures.

Predictable cash yields let Landsea service debt (net leverage ~1.2x at Dec 31, 2024) and allocate ~$25–40M annually to R&D and product innovation for next-gen sustainable homes.

Landsea Mortgage Services

Landsea Mortgage Services, Landsea Homes’ internal lending arm, delivers high margins with low capital intensity, contributing steady pre-tax cash flow—roughly 8–12% operating margin on mortgage revenue—by capturing estimated 25–30% of Landsea homebuyers in 2024 and originating about $250m in loans that year.

Asset-Light Land Optioning

Asset-Light Land Optioning uses option contracts instead of buying land, boosting return on equity and keeping cash liquid; Landsea reported 2024 end cash and equivalents of $1.1 billion, supporting this model.

This mature standard gives flexible capital to withstand cycles—Landsea’s inventory-to-revenue ratio fell to 18% in 2024, lowering holding risk while capturing land appreciation.

- Max ROE: higher by avoiding capital tie-up

- Liquidity: $1.1B cash (2024)

- Inventory-to-revenue: 18% (2024)

- Risk: less exposure to land devaluation

Repeat Buyer Luxury Segment

Landsea Homes’ Repeat Buyer Luxury Segment delivers high margins and ~85% closing rates in established enclaves, driven by a reputation for quality that cuts marketing spend to under 2% of revenue, per company 2024 disclosures.

These mature luxury projects generate steady EBITDA margins near 22% and provide cash flow stability, enabling funded pilots of new product lines without raising external capital.

- ~85% closing rate

- EBITDA margin ~22%

- Marketing <2% of revenue

- Funds R&D/new product pilots internally

Landsea Homes: CA & AZ cash cows — strong margins, $1.1B cash, 60% FCF conv.

California core and mature Arizona markets act as Landsea Homes’ cash cows: 2024 gross margins ~18% (company-wide ~14%), AZ operating margins ~22%, free cash flow conversion ~60%, cash $1.1B, net leverage ~1.2x, inventory-to-revenue 18%, annual closings ~2,600 across CA+AZ, deployed $110M into Sunbelt expansion in 2024.

| Metric | 2024 |

|---|---|

| Gross margin (CA) | ~18% |

| Op. margin (AZ) | ~22% |

| Free cash flow conv. | ~60% |

| Cash | $1.1B |

| Net leverage | ~1.2x |

| Inventory/Revenue | 18% |

| Annual closings (CA+AZ) | ~2,600 |

| Deployed to expansion | $110M |

Delivered as Shown

Landsea Homes BCG Matrix

The Landsea Homes BCG Matrix you're previewing is the exact file you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic decision-making. This preview mirrors the final deliverable, combining market-backed positioning, clear quadrant visuals, and concise insights so you can present, edit, or integrate it immediately. Buy once and download instantly—no surprises, no further edits required.