Landsea Homes PESTLE Analysis

Skip the Research. Get the Strategy.

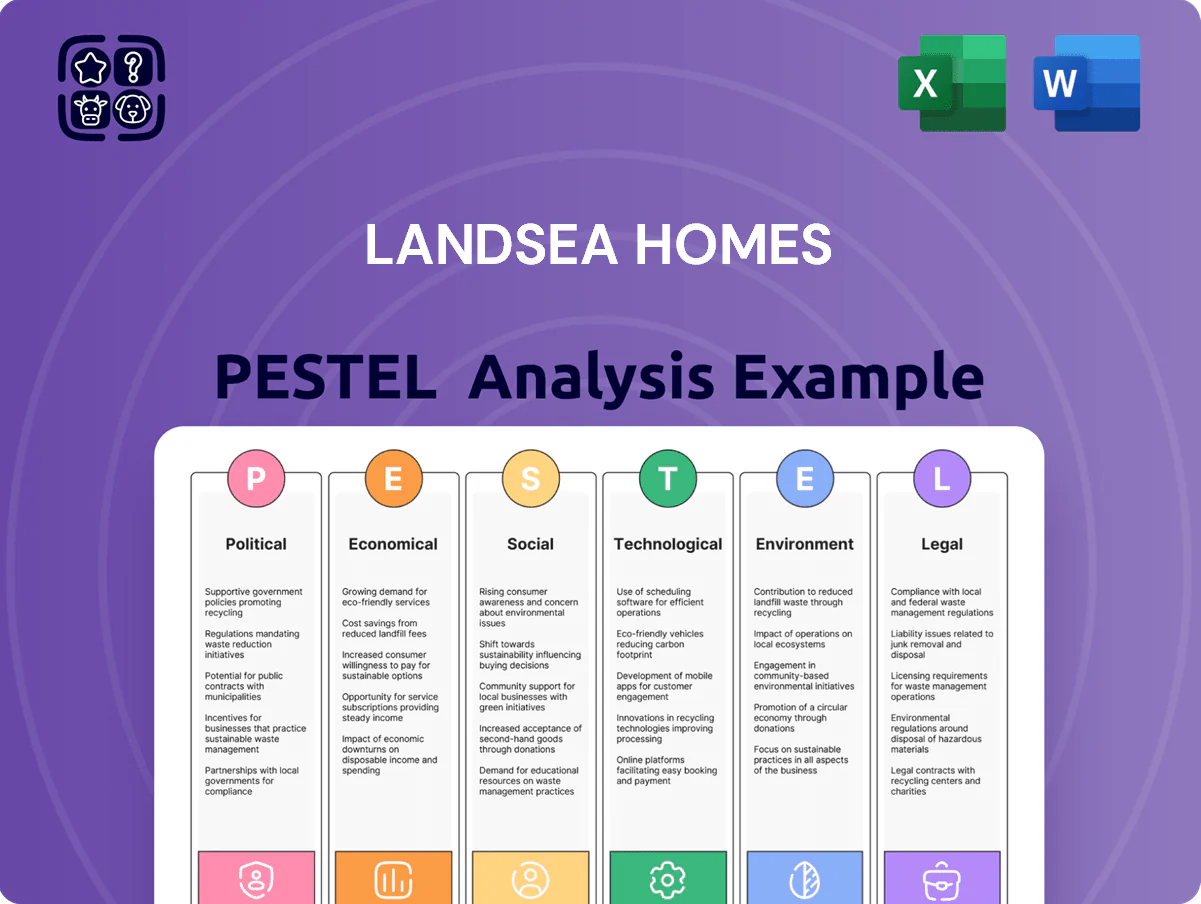

Discover how political shifts, housing demand cycles, and environmental regulations uniquely shape Landsea Homes’ outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment moves. Purchase the full PESTLE Analysis for a complete, actionable breakdown with editable files and immediate download.

Political factors

Federal housing subsidies and tax incentives

Federal incentives like the mortgage interest deduction and targeted first-time buyer credits materially affect demand for Landsea Homes; the mortgage interest deduction supported about 20 million taxpayers in 2023 and reduced effective borrowing costs by roughly 0.2–0.5 percentage points for many households. Recent federal fiscal proposals through 2025 considered capping deductions and expanding refundable credits—changes that could shift after-tax homeownership costs by several thousand dollars annually. Management must monitor Congressional tax discussions and the Biden-era and post-2024 policy signals, since a 1% change in effective mortgage cost can alter national purchase propensity and single-family starts, which totaled 835,000 units in 2024.

Trade tariffs on construction materials

The imposition of tariffs on imported lumber, steel and aluminum can raise Landsea Homes construction costs by an estimated 5–12%, with US timber tariffs in 2024 adding about 8% to lumber import prices and global steel tariffs pushing coil costs up 10% year-over-year; political shifts with Canada and ASEAN suppliers risk sudden spikes, forcing Landsea to absorb margin compression or raise home prices, which could reduce sales volume given US new-home median affordability sensitivity to price increases.

Local zoning and land use regulations

Municipal zoning and land-use rules determine lot availability and density in key markets—California and Texas account for roughly 40% of Landsea Homes’ 2024 deliveries—so restrictive zoning can materially cut pipeline growth.

Shifts in local leadership frequently prompt rezoning; between 2022–2024 over 15 California cities updated housing elements, altering allowable densities for master-planned projects.

Securing entitlements now often adds 12–36 months and millions in carrying costs per community, so proactive local political engagement is critical to maintain a steady stream of buildable lots.

State-level migration and economic policies

Landsea Homes benefits from activity in states like Florida and Arizona, which saw net migration gains of about 373,000 and 85,000 people respectively in 2023–2024, supporting housing demand; Florida’s absence of state income tax and Arizona’s pro-business incentives attract corporate relocations that expand buyer pools.

However, a shift toward higher state taxes or reduced relocation incentives could dampen inflows; Moody’s Analytics projects that a 1% rise in effective state tax rates can lower net migration by ~0.5–1.0%, potentially trimming local new-home demand.

- Florida net migration ~373,000 (2023–24)

- Arizona net migration ~85,000 (2023–24)

- 1% state tax rise → ~0.5–1% migration decline (Moody’s est.)

Geopolitical impact on energy costs

Global political instability drives energy market volatility, with Brent crude swinging 40% in 2022–2024 and U.S. diesel rising ~28% year-over-year in 2023, increasing costs for manufacturing and transporting Landsea’s building materials.

Higher fuel prices raise site development and logistics overhead across Landsea’s multi-state footprint, adding several hundred dollars per home in 2023 estimated transport and equipment-fuel costs.

Landsea must embed macro-political risk premia in forecasts—using energy price sensitivity scenarios (±20–40%)—to protect project budgets and delivery timelines amid ongoing geopolitical uncertainty.

- Brent crude volatility ~40% (2022–24)

- U.S. diesel +28% YoY (2023)

- Fuel adds hundreds $/home in 2023 transport/equipment costs

- Stress-test budgets for ±20–40% energy swings

Tax, tariffs and zoning squeeze Landsea margins as FL/AZ migration cushions demand

Federal tax shifts and mortgage-cost moves (1% change alters starts; 835,000 single-family starts in 2024) plus tariffs (lumber/steel added ~8–10% import cost in 2024) and local zoning/entitlement delays (12–36 months per community) materially affect Landsea’s margins and supply; migration into FL (~373,000) and AZ (~85,000) supports demand while energy volatility (Brent ±40% 2022–24) raises transport fuel costs.

| Factor | Key 2023–24 Data |

|---|---|

| Starts | 835,000 (2024) |

| FL migration | ~373,000 (2023–24) |

| AZ migration | ~85,000 (2023–24) |

| Lumber/steel impact | ~8–10% (2024) |

| Brent volatility | ~40% (2022–24) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Landsea Homes, with data-backed trends, localized regulatory context, and actionable insights to inform strategy, risk management, and investor communications.

A concise, visually segmented Landsea Homes PESTLE summary that clarifies external risks and opportunities for quick alignment in meetings, easily dropped into presentations or shared across teams for streamlined planning.

Economic factors

Mortgage rate volatility and affordability

Fluctuations in the federal funds rate have pushed 30-year fixed mortgage rates from ~6.9% in mid-2024 to about 6.5% by Dec 2025, directly affecting affordability for Landsea Homes’ middle-market buyers.

As rates showed signs of stabilization late 2025, Landsea emphasized financing incentives—seller-paid points and rate buydowns—to sustain sales velocity amid ~15% year-over-year decline in new-home traffic in 2024.

Prolonged high-rate environments require pricing and product shifts—downsized floor plans and stretch financing—so monthly payments stay near median household affordability thresholds (US median income ~$76,000 in 2024).

Inflationary pressure on raw materials

Rising inflation pushed US producer prices for construction materials up 6.8% year‑on‑year in 2024, squeezing Landsea Homes margins as lumber, steel and cement costs rose; effective procurement and hedging are needed to protect project profitability. Landsea must optimize bulk purchasing, long‑term supplier contracts and value engineering to offset rising labor and material expenses that climbed roughly 5–7% in many regions in 2024. Prolonged inflation also reduced real wages and, with US household savings rates roughly 3.5% in 2024, made it harder for buyers to accumulate down payments, pressuring sales velocity and pricing power.

Employment growth in Sun Belt markets

Employment growth in Sun Belt markets like Texas and Arizona underpins Landsea Homes revenue: Texas added about 400,000 jobs in 2024 while Arizona gained ~85,000, supporting rising homebuying; unemployment stood near 3.6% TX and 3.9% AZ (2024 avg), boosting mortgage affordability and long-term demand.

Consumer debt-to-income ratios

Rising U.S. consumer debt—totaling about 17.3 trillion USD in Q3 2025 with student loan debt ~1.6 trillion and credit card balances near 1.2 trillion—reduces the qualified buyer pool for Landsea Homes as high DTI can block access to preferred mortgage rates.

Landsea mitigates this by partnering with preferred lenders to offer financial education and tailored loan products that help buyers lower DTI and secure favorable financing.

- Q3 2025 total consumer debt ~17.3T USD

- Student loans ~1.6T, credit cards ~1.2T

- High DTI limits mortgage eligibility despite adequate income

- Landsea uses lender partnerships, education, tailored loans

Housing market supply-demand imbalance

The persistent shortage of existing-home inventory—U.S. months’ supply fell below 2.5 months in 2024 in many metros vs. a healthy 5–6 months—creates a favorable market for new-home builders like Landsea, driving higher demand and pricing power.

Low resale supply pushes buyers toward new construction for modern amenities and warranties; Landsea targets high-demand Sun Belt and coastal submarkets where new-home absorption rates exceeded 30 homes per 1000 households in 2024.

By positioning developments in constrained markets, Landsea captures premium margins; backlog and reservation trends in 2024 showed new-home price premiums of 8–12% over comparable resales in selected markets.

- U.S. months’ supply <2.5 in many metros (2024)

- New-home absorption >30/1000 households in targeted areas (2024)

- Price premium for new homes 8–12% vs. resale in select markets (2024)

Homebuilders Navigate Tight Margins: High Rates & Costs vs. Sun Belt Demand

High mortgage rates (~6.5%–6.9% in 2024–25) and rising construction costs (+6.8% PPI materials 2024) compress margins and affordability, while Sun Belt job gains (TX +400k, AZ +85k in 2024) and low resale supply (<2.5 months 2024) sustain new-home demand; rising consumer debt (~17.3T Q3 2025) raises DTI risks mitigated by Landsea lender partnerships.

| Metric | Value |

|---|---|

| 30-yr rate | 6.5%–6.9% |

| Materials PPI (2024) | +6.8% |

| Consumer debt Q3 2025 | 17.3T |

| TX jobs 2024 | +400k |

Preview Before You Purchase

Landsea Homes PESTLE Analysis

The preview shown here is the exact Landsea Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, housing demand cycles, and environmental regulations uniquely shape Landsea Homes’ outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment moves. Purchase the full PESTLE Analysis for a complete, actionable breakdown with editable files and immediate download.

Political factors

Federal housing subsidies and tax incentives

Federal incentives like the mortgage interest deduction and targeted first-time buyer credits materially affect demand for Landsea Homes; the mortgage interest deduction supported about 20 million taxpayers in 2023 and reduced effective borrowing costs by roughly 0.2–0.5 percentage points for many households. Recent federal fiscal proposals through 2025 considered capping deductions and expanding refundable credits—changes that could shift after-tax homeownership costs by several thousand dollars annually. Management must monitor Congressional tax discussions and the Biden-era and post-2024 policy signals, since a 1% change in effective mortgage cost can alter national purchase propensity and single-family starts, which totaled 835,000 units in 2024.

Trade tariffs on construction materials

The imposition of tariffs on imported lumber, steel and aluminum can raise Landsea Homes construction costs by an estimated 5–12%, with US timber tariffs in 2024 adding about 8% to lumber import prices and global steel tariffs pushing coil costs up 10% year-over-year; political shifts with Canada and ASEAN suppliers risk sudden spikes, forcing Landsea to absorb margin compression or raise home prices, which could reduce sales volume given US new-home median affordability sensitivity to price increases.

Local zoning and land use regulations

Municipal zoning and land-use rules determine lot availability and density in key markets—California and Texas account for roughly 40% of Landsea Homes’ 2024 deliveries—so restrictive zoning can materially cut pipeline growth.

Shifts in local leadership frequently prompt rezoning; between 2022–2024 over 15 California cities updated housing elements, altering allowable densities for master-planned projects.

Securing entitlements now often adds 12–36 months and millions in carrying costs per community, so proactive local political engagement is critical to maintain a steady stream of buildable lots.

State-level migration and economic policies

Landsea Homes benefits from activity in states like Florida and Arizona, which saw net migration gains of about 373,000 and 85,000 people respectively in 2023–2024, supporting housing demand; Florida’s absence of state income tax and Arizona’s pro-business incentives attract corporate relocations that expand buyer pools.

However, a shift toward higher state taxes or reduced relocation incentives could dampen inflows; Moody’s Analytics projects that a 1% rise in effective state tax rates can lower net migration by ~0.5–1.0%, potentially trimming local new-home demand.

- Florida net migration ~373,000 (2023–24)

- Arizona net migration ~85,000 (2023–24)

- 1% state tax rise → ~0.5–1% migration decline (Moody’s est.)

Geopolitical impact on energy costs

Global political instability drives energy market volatility, with Brent crude swinging 40% in 2022–2024 and U.S. diesel rising ~28% year-over-year in 2023, increasing costs for manufacturing and transporting Landsea’s building materials.

Higher fuel prices raise site development and logistics overhead across Landsea’s multi-state footprint, adding several hundred dollars per home in 2023 estimated transport and equipment-fuel costs.

Landsea must embed macro-political risk premia in forecasts—using energy price sensitivity scenarios (±20–40%)—to protect project budgets and delivery timelines amid ongoing geopolitical uncertainty.

- Brent crude volatility ~40% (2022–24)

- U.S. diesel +28% YoY (2023)

- Fuel adds hundreds $/home in 2023 transport/equipment costs

- Stress-test budgets for ±20–40% energy swings

Tax, tariffs and zoning squeeze Landsea margins as FL/AZ migration cushions demand

Federal tax shifts and mortgage-cost moves (1% change alters starts; 835,000 single-family starts in 2024) plus tariffs (lumber/steel added ~8–10% import cost in 2024) and local zoning/entitlement delays (12–36 months per community) materially affect Landsea’s margins and supply; migration into FL (~373,000) and AZ (~85,000) supports demand while energy volatility (Brent ±40% 2022–24) raises transport fuel costs.

| Factor | Key 2023–24 Data |

|---|---|

| Starts | 835,000 (2024) |

| FL migration | ~373,000 (2023–24) |

| AZ migration | ~85,000 (2023–24) |

| Lumber/steel impact | ~8–10% (2024) |

| Brent volatility | ~40% (2022–24) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Landsea Homes, with data-backed trends, localized regulatory context, and actionable insights to inform strategy, risk management, and investor communications.

A concise, visually segmented Landsea Homes PESTLE summary that clarifies external risks and opportunities for quick alignment in meetings, easily dropped into presentations or shared across teams for streamlined planning.

Economic factors

Mortgage rate volatility and affordability

Fluctuations in the federal funds rate have pushed 30-year fixed mortgage rates from ~6.9% in mid-2024 to about 6.5% by Dec 2025, directly affecting affordability for Landsea Homes’ middle-market buyers.

As rates showed signs of stabilization late 2025, Landsea emphasized financing incentives—seller-paid points and rate buydowns—to sustain sales velocity amid ~15% year-over-year decline in new-home traffic in 2024.

Prolonged high-rate environments require pricing and product shifts—downsized floor plans and stretch financing—so monthly payments stay near median household affordability thresholds (US median income ~$76,000 in 2024).

Inflationary pressure on raw materials

Rising inflation pushed US producer prices for construction materials up 6.8% year‑on‑year in 2024, squeezing Landsea Homes margins as lumber, steel and cement costs rose; effective procurement and hedging are needed to protect project profitability. Landsea must optimize bulk purchasing, long‑term supplier contracts and value engineering to offset rising labor and material expenses that climbed roughly 5–7% in many regions in 2024. Prolonged inflation also reduced real wages and, with US household savings rates roughly 3.5% in 2024, made it harder for buyers to accumulate down payments, pressuring sales velocity and pricing power.

Employment growth in Sun Belt markets

Employment growth in Sun Belt markets like Texas and Arizona underpins Landsea Homes revenue: Texas added about 400,000 jobs in 2024 while Arizona gained ~85,000, supporting rising homebuying; unemployment stood near 3.6% TX and 3.9% AZ (2024 avg), boosting mortgage affordability and long-term demand.

Consumer debt-to-income ratios

Rising U.S. consumer debt—totaling about 17.3 trillion USD in Q3 2025 with student loan debt ~1.6 trillion and credit card balances near 1.2 trillion—reduces the qualified buyer pool for Landsea Homes as high DTI can block access to preferred mortgage rates.

Landsea mitigates this by partnering with preferred lenders to offer financial education and tailored loan products that help buyers lower DTI and secure favorable financing.

- Q3 2025 total consumer debt ~17.3T USD

- Student loans ~1.6T, credit cards ~1.2T

- High DTI limits mortgage eligibility despite adequate income

- Landsea uses lender partnerships, education, tailored loans

Housing market supply-demand imbalance

The persistent shortage of existing-home inventory—U.S. months’ supply fell below 2.5 months in 2024 in many metros vs. a healthy 5–6 months—creates a favorable market for new-home builders like Landsea, driving higher demand and pricing power.

Low resale supply pushes buyers toward new construction for modern amenities and warranties; Landsea targets high-demand Sun Belt and coastal submarkets where new-home absorption rates exceeded 30 homes per 1000 households in 2024.

By positioning developments in constrained markets, Landsea captures premium margins; backlog and reservation trends in 2024 showed new-home price premiums of 8–12% over comparable resales in selected markets.

- U.S. months’ supply <2.5 in many metros (2024)

- New-home absorption >30/1000 households in targeted areas (2024)

- Price premium for new homes 8–12% vs. resale in select markets (2024)

Homebuilders Navigate Tight Margins: High Rates & Costs vs. Sun Belt Demand

High mortgage rates (~6.5%–6.9% in 2024–25) and rising construction costs (+6.8% PPI materials 2024) compress margins and affordability, while Sun Belt job gains (TX +400k, AZ +85k in 2024) and low resale supply (<2.5 months 2024) sustain new-home demand; rising consumer debt (~17.3T Q3 2025) raises DTI risks mitigated by Landsea lender partnerships.

| Metric | Value |

|---|---|

| 30-yr rate | 6.5%–6.9% |

| Materials PPI (2024) | +6.8% |

| Consumer debt Q3 2025 | 17.3T |

| TX jobs 2024 | +400k |

Preview Before You Purchase

Landsea Homes PESTLE Analysis

The preview shown here is the exact Landsea Homes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.