Landsea Homes SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Landsea Homes shows strengths in sustainable building expertise and a diversified regional footprint but faces supply-chain pressures and market cyclicality that could squeeze margins; competitive differentiation and green credentials are clear growth levers. Discover the full strategic picture—purchase the complete SWOT analysis for an investor-ready, editable Word and Excel package with research-backed insights and actionable recommendations.

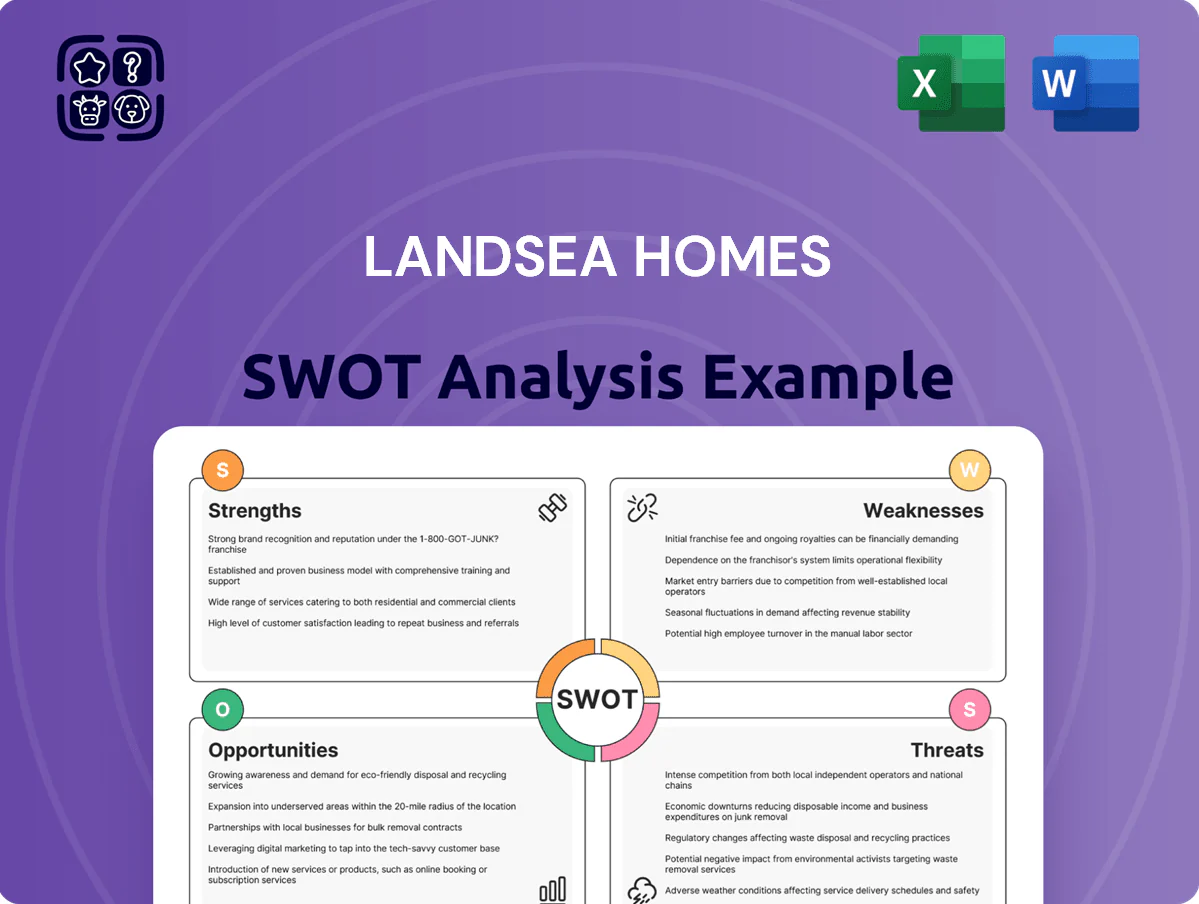

Strengths

High Performance Homes Technology

Landsea Homes’ proprietary High Performance Homes program bundles home automation, sustainability, and energy-efficiency as standard, appealing to eco-conscious and tech-savvy buyers; in 2024 energy-efficient features cut average homeowner bills by ~20% (DOE), boosting resale value by an estimated 3–5% per Zillow research. This tech-first stance strengthens marketing differentiation, supports lower operating costs, and helps command price premiums in coastal and suburban U.S. markets.

Strategic Geographic Diversification

Landsea Homes has grown in Sunbelt states—Arizona, Florida, Texas—where 2024 net migration added ~1.1M, 1.3M, and 1.0M residents respectively, cutting dependence on California which accounted for ~35% of revenue in 2019 but under 20% by 2024.

Asset-Light Business Model

Landsea uses an asset-light land strategy, securing roughly 60–70% of its lots via option contracts rather than outright ownership, which in 2024 helped keep inventory investment low and pushed return on equity to about 22% for the year. This minimizes capital tied in long-term holdings and cuts balance-sheet risk—Landsea’s inventory-to-assets ratio was ~18% in FY2024. The model lets the firm scale land intake up or down quickly as market demand shifts.

Successful M&A Integration

The acquisition of Antares Homes (closed 2023) and other regional builders raised Landsea Homes’ U.S. market share, adding roughly 1,200 homes of annual capacity and expanding presence in Texas and Sun Belt markets.

These deals delivered immediate local know-how and vendor contracts, cutting time-to-market by an estimated 20% and improving gross margin on acquired communities by ~150–200 basis points in 2024.

Successful brand integration with consistent customer NPS and centralized ops shows strong management execution and supports a projected 10–15% revenue CAGR through 2026.

- +1,200 annual home capacity

- ~20% faster time-to-market

- +150–200 bps gross margin on acquired sites

- 10–15% revenue CAGR target (2024–2026)

Focus on Attainable Luxury

- Average selling price: ~$420,000 (2024)

- Absorption: ~6.5 months (FY2024)

- Gross margin: ~22% (2024)

- Cancellation rate: <6% (2024)

Landsea: 22% Margin & ROE, $420K ASP, +1,200 Homes, 10–15% Revenue CAGR

Landsea’s High Performance Homes and asset-light land strategy drove FY2024 gross margin ~22%, ROE ~22%, ~60–70% lots under option, avg selling price ~$420,000, absorption ~6.5 months, cancellation <6%, +1,200 annual capacity from Antares, ~20% faster time-to-market, and 10–15% revenue CAGR target (2024–2026).

| Metric | 2024 |

|---|---|

| Gross margin | ~22% |

| ROE | ~22% |

| Lots via options | 60–70% |

| Avg SP | $420,000 |

| Absorption | 6.5 mo |

| Cancellation rate | <6% |

| Added capacity | +1,200 homes |

| Time-to-market | -20% |

| Revenue CAGR target | 10–15% |

What is included in the product

Delivers a concise SWOT overview of Landsea Homes, outlining its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Provides a concise SWOT overview of Landsea Homes for rapid strategic alignment and stakeholder briefings.

Weaknesses

Geographic Concentration in California

Despite expansion, about 55% of Landsea Homes’ revenue and over 60% of its land inventory remained in California as of FY2024, concentrating exposure to state risks.

That ties the firm to California’s strict environmental rules and higher labor costs—average construction wages ~20% above national levels in 2024—and elevated property taxes.

A California housing slowdown or law change (e.g., CEQA reforms or local zoning shifts) could cut margins and cash flow, hitting overall performance disproportionately.

Higher Leverage Ratios

Landsea Homes has carried higher debt-to-capital than many peers — about 48% net debt-to-capital at FY2024 vs. a 30–35% peer median, which supported faster expansion and acquisitions.

That leverage raises interest-rate and refinancing risk: a 100bp rise in rates would add roughly $6–8m in annual interest, squeezing margins on FY2024 gross margin of ~22%.

Controlling debt costs and preserving liquidity (cash + revolver availability $220m at end-2024) is therefore critical to avoid forced deleveraging in tighter credit cycles.

Limited Scale Versus National Giants

As a mid-sized builder, Landsea Homes faces intense competition from national firms like D.R. Horton and Lennar, which in 2024 reported gross margins ~25–27% versus Landsea’s ~18–20%, giving them stronger economies of scale and purchasing power.

These giants negotiate 5–10% lower supplier and subcontractor costs per sqft, pressuring Landsea to protect margins while competing for the same limited skilled labor pool, where national recruiters secure workers with higher pay and benefits.

Operational Complexity from Rapid Growth

The speed of Landsea Homes' expansion—12 acquisitions and entry into 8 new states from 2020–2024—has raised operational and cultural integration strains, increasing overhead and coordination costs.

Managing dispersed regional offices and maintaining uniform quality across 15+ active construction markets demands stronger internal controls and ERP-grade systems; without these, inefficiencies could shave off 150–300 basis points of gross margin.

- 12 acquisitions (2020–2024)

- 8 new states entered

- 15+ active construction markets

- 150–300 bps potential margin erosion

Sensitivity to Mortgage Rate Volatility

The company’s focus on first-time and move-up buyers makes revenue highly rate-sensitive; a 1 percentage-point rise in 30-year mortgage rates cut affordability for a median-priced U.S. home by about 10% in 2024, shrinking the qualified buyer pool.

Even small rate upticks slowed Landsea Homes’ community sales velocity in 2023–2024 compared with luxury-focused peers, increasing quarter-to-quarter revenue volatility and inventory carrying costs.

High CA concentration, heavy leverage and rising costs threaten margins and demand

Concentration: ~55% revenue, >60% land in California (FY2024) raises regulatory and tax risk; construction wages ~20% above US avg (2024). Leverage: net debt-to-capital ~48% vs peer median 30–35% (FY2024); +100bp rates → ~$6–8m extra interest. Scale/ops: 12 acquisitions, 8 new states, 15+ markets (2020–2024) → potential 150–300 bps margin erosion. Demand: 1ppt mortgage rise ≈10% affordability drop (2024).

| Metric | Value (FY2024) |

|---|---|

| Revenue in CA | ~55% |

| Land in CA | >60% |

| Net debt-to-capital | ~48% |

| Peer median | 30–35% |

| Cash + revolver | $220m |

| Gross margin | ~22% |

| Construction wage premium | ~20% |

| Acquisitions (2020–2024) | 12 |

| States entered (2020–2024) | 8 |

| Markets active | 15+ |

| Margin erosion risk | 150–300 bps |

| Affordability sensitivity | 1ppt → ≈10% |

Preview Before You Purchase

Landsea Homes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Landsea Homes shows strengths in sustainable building expertise and a diversified regional footprint but faces supply-chain pressures and market cyclicality that could squeeze margins; competitive differentiation and green credentials are clear growth levers. Discover the full strategic picture—purchase the complete SWOT analysis for an investor-ready, editable Word and Excel package with research-backed insights and actionable recommendations.

Strengths

High Performance Homes Technology

Landsea Homes’ proprietary High Performance Homes program bundles home automation, sustainability, and energy-efficiency as standard, appealing to eco-conscious and tech-savvy buyers; in 2024 energy-efficient features cut average homeowner bills by ~20% (DOE), boosting resale value by an estimated 3–5% per Zillow research. This tech-first stance strengthens marketing differentiation, supports lower operating costs, and helps command price premiums in coastal and suburban U.S. markets.

Strategic Geographic Diversification

Landsea Homes has grown in Sunbelt states—Arizona, Florida, Texas—where 2024 net migration added ~1.1M, 1.3M, and 1.0M residents respectively, cutting dependence on California which accounted for ~35% of revenue in 2019 but under 20% by 2024.

Asset-Light Business Model

Landsea uses an asset-light land strategy, securing roughly 60–70% of its lots via option contracts rather than outright ownership, which in 2024 helped keep inventory investment low and pushed return on equity to about 22% for the year. This minimizes capital tied in long-term holdings and cuts balance-sheet risk—Landsea’s inventory-to-assets ratio was ~18% in FY2024. The model lets the firm scale land intake up or down quickly as market demand shifts.

Successful M&A Integration

The acquisition of Antares Homes (closed 2023) and other regional builders raised Landsea Homes’ U.S. market share, adding roughly 1,200 homes of annual capacity and expanding presence in Texas and Sun Belt markets.

These deals delivered immediate local know-how and vendor contracts, cutting time-to-market by an estimated 20% and improving gross margin on acquired communities by ~150–200 basis points in 2024.

Successful brand integration with consistent customer NPS and centralized ops shows strong management execution and supports a projected 10–15% revenue CAGR through 2026.

- +1,200 annual home capacity

- ~20% faster time-to-market

- +150–200 bps gross margin on acquired sites

- 10–15% revenue CAGR target (2024–2026)

Focus on Attainable Luxury

- Average selling price: ~$420,000 (2024)

- Absorption: ~6.5 months (FY2024)

- Gross margin: ~22% (2024)

- Cancellation rate: <6% (2024)

Landsea: 22% Margin & ROE, $420K ASP, +1,200 Homes, 10–15% Revenue CAGR

Landsea’s High Performance Homes and asset-light land strategy drove FY2024 gross margin ~22%, ROE ~22%, ~60–70% lots under option, avg selling price ~$420,000, absorption ~6.5 months, cancellation <6%, +1,200 annual capacity from Antares, ~20% faster time-to-market, and 10–15% revenue CAGR target (2024–2026).

| Metric | 2024 |

|---|---|

| Gross margin | ~22% |

| ROE | ~22% |

| Lots via options | 60–70% |

| Avg SP | $420,000 |

| Absorption | 6.5 mo |

| Cancellation rate | <6% |

| Added capacity | +1,200 homes |

| Time-to-market | -20% |

| Revenue CAGR target | 10–15% |

What is included in the product

Delivers a concise SWOT overview of Landsea Homes, outlining its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Provides a concise SWOT overview of Landsea Homes for rapid strategic alignment and stakeholder briefings.

Weaknesses

Geographic Concentration in California

Despite expansion, about 55% of Landsea Homes’ revenue and over 60% of its land inventory remained in California as of FY2024, concentrating exposure to state risks.

That ties the firm to California’s strict environmental rules and higher labor costs—average construction wages ~20% above national levels in 2024—and elevated property taxes.

A California housing slowdown or law change (e.g., CEQA reforms or local zoning shifts) could cut margins and cash flow, hitting overall performance disproportionately.

Higher Leverage Ratios

Landsea Homes has carried higher debt-to-capital than many peers — about 48% net debt-to-capital at FY2024 vs. a 30–35% peer median, which supported faster expansion and acquisitions.

That leverage raises interest-rate and refinancing risk: a 100bp rise in rates would add roughly $6–8m in annual interest, squeezing margins on FY2024 gross margin of ~22%.

Controlling debt costs and preserving liquidity (cash + revolver availability $220m at end-2024) is therefore critical to avoid forced deleveraging in tighter credit cycles.

Limited Scale Versus National Giants

As a mid-sized builder, Landsea Homes faces intense competition from national firms like D.R. Horton and Lennar, which in 2024 reported gross margins ~25–27% versus Landsea’s ~18–20%, giving them stronger economies of scale and purchasing power.

These giants negotiate 5–10% lower supplier and subcontractor costs per sqft, pressuring Landsea to protect margins while competing for the same limited skilled labor pool, where national recruiters secure workers with higher pay and benefits.

Operational Complexity from Rapid Growth

The speed of Landsea Homes' expansion—12 acquisitions and entry into 8 new states from 2020–2024—has raised operational and cultural integration strains, increasing overhead and coordination costs.

Managing dispersed regional offices and maintaining uniform quality across 15+ active construction markets demands stronger internal controls and ERP-grade systems; without these, inefficiencies could shave off 150–300 basis points of gross margin.

- 12 acquisitions (2020–2024)

- 8 new states entered

- 15+ active construction markets

- 150–300 bps potential margin erosion

Sensitivity to Mortgage Rate Volatility

The company’s focus on first-time and move-up buyers makes revenue highly rate-sensitive; a 1 percentage-point rise in 30-year mortgage rates cut affordability for a median-priced U.S. home by about 10% in 2024, shrinking the qualified buyer pool.

Even small rate upticks slowed Landsea Homes’ community sales velocity in 2023–2024 compared with luxury-focused peers, increasing quarter-to-quarter revenue volatility and inventory carrying costs.

High CA concentration, heavy leverage and rising costs threaten margins and demand

Concentration: ~55% revenue, >60% land in California (FY2024) raises regulatory and tax risk; construction wages ~20% above US avg (2024). Leverage: net debt-to-capital ~48% vs peer median 30–35% (FY2024); +100bp rates → ~$6–8m extra interest. Scale/ops: 12 acquisitions, 8 new states, 15+ markets (2020–2024) → potential 150–300 bps margin erosion. Demand: 1ppt mortgage rise ≈10% affordability drop (2024).

| Metric | Value (FY2024) |

|---|---|

| Revenue in CA | ~55% |

| Land in CA | >60% |

| Net debt-to-capital | ~48% |

| Peer median | 30–35% |

| Cash + revolver | $220m |

| Gross margin | ~22% |

| Construction wage premium | ~20% |

| Acquisitions (2020–2024) | 12 |

| States entered (2020–2024) | 8 |

| Markets active | 15+ |

| Margin erosion risk | 150–300 bps |

| Affordability sensitivity | 1ppt → ≈10% |

Preview Before You Purchase

Landsea Homes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.