Lannett Company PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how regulatory shifts, pricing pressure, and supply-chain dynamics are shaping Lannett Company's outlook in our concise PESTLE snapshot—perfect for investors and strategists seeking fast, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, growth opportunities, and strategic recommendations you can apply immediately.

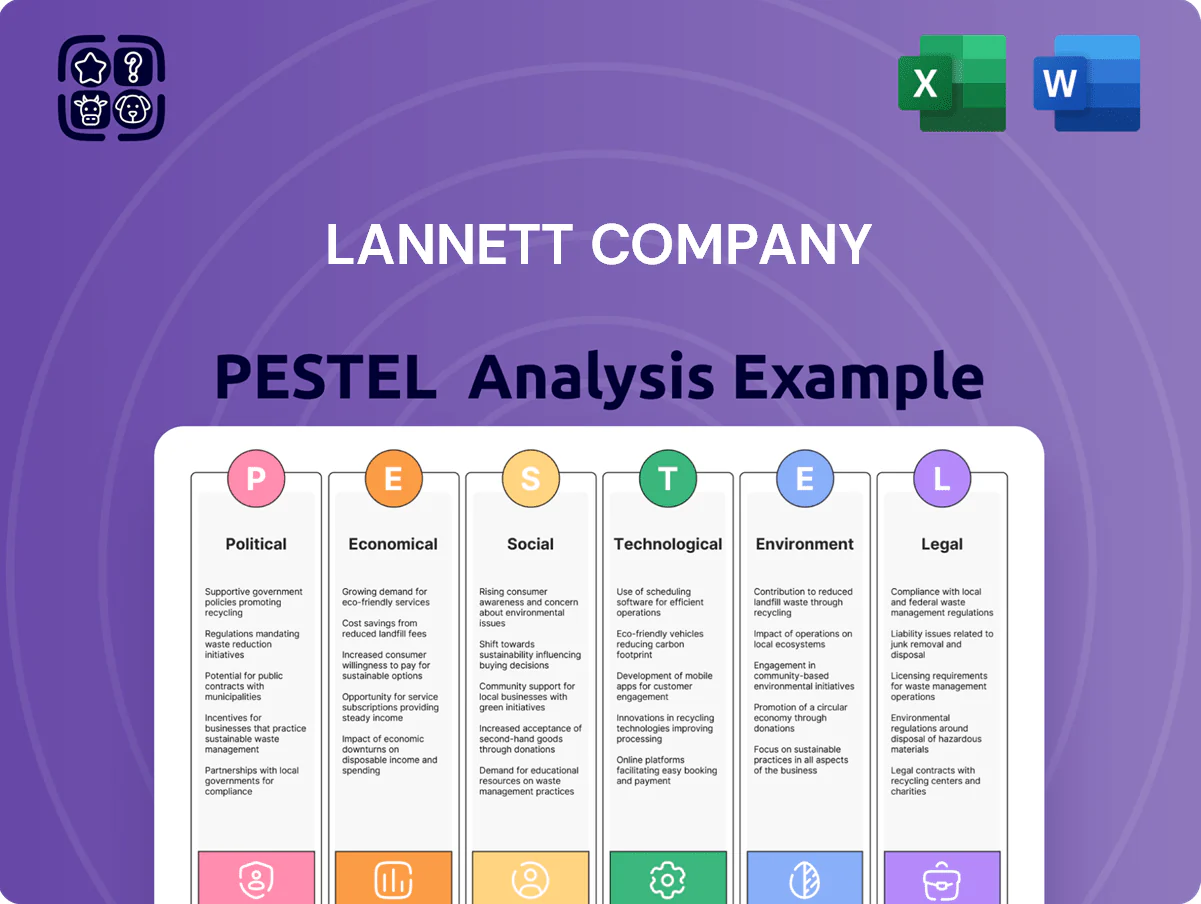

Political factors

Drug Pricing Legislation and Reform

Government initiatives to lower prescription drug costs, including provisions from the 2022 Inflation Reduction Act, pressure generics makers by enabling Medicare negotiation—projected to save Medicare $100 billion through 2031—forcing price compression across the market.

Policies capping Medicare Part D OOP and allowing inflation rebates have driven downward pricing trends; generic ASP deflation of 5–10% in some therapeutic classes in 2024 affected margins industrywide.

Lannett must adjust pricing, contract strategies, and production to protect its 2024 revenue base—$220 million reported revenue in FY2024—while managing reimbursement risk and negotiating formularies to sustain profitability.

FDA Regulatory Oversight and Approval Processes

The political climate shapes FDA funding and priorities—federal appropriations rose to $5.6 billion in FY2025, influencing review capacity and timelines for Abbreviated New Drug Applications (ANDAs).

Leadership or policy shifts can accelerate or tighten approval cycles: median ANDA approval time moved from 36 months in 2022 to 30 months in 2024 under targeted review initiatives.

Lannett depends on efficient regulatory pathways to launch generics early; a 6-month faster approval can capture market share and materially affect revenues given thin generic margins.

International Trade and Supply Chain Policies

Political tensions and shifting trade agreements directly impact Lannett’s sourcing of APIs from China and India, which supply an estimated 60-70% of generic pharmaceutical APIs globally; disruptions could raise input costs and compress margins on its $287M 2024 revenue base.

New tariffs or export controls—such as recent US-China tech tariffs and sporadic Indian export curbs—could add 5-12% to API costs or delay shipments, risking production slowdowns across Lannett’s U.S. manufacturing sites.

Lannett must continuously monitor geopolitical stability and trade policy changes to safeguard a steady raw-material flow, hedge price volatility, and avoid inventory-driven disruptions that could impact quarterly output and revenue recognition.

Healthcare Infrastructure Funding

Government spending on public health programs drives demand for affordable generics; US federal and state drug spending rose 4.2% in 2024, boosting volume-sensitive players like Lannett.

Policy changes to Medicaid enrollment—which covered 82 million people in 2024—directly affect prescription volumes; expansions increase generic dispensing.

State policies favoring generic substitution as a cost-containment tool support Lannett’s market share and pricing stability.

- 2024 US drug spending +4.2%

- Medicaid enrollees 82M (2024)

- Generic substitution policies => higher volume for Lannett

National Security and Domestic Manufacturing Incentives

Rising U.S. policy focus on reshoring pharma manufacturing—driven by 2023–2025 supply chain disruptions—offers Lannett access to incentives; the CHIPS and Science Act-like momentum and state grant programs have directed billions in manufacturing support, with federal manufacturing tax credits discussed in 2024 potentially lowering capex payback for domestic plants.

With Lannett operating U.S. facilities, it can capture grants/tax breaks to boost capacity, improving resilience and market share; leveraging incentives could reduce effective manufacturing costs and enhance margins amid rising generic demand.

- Federal/state grants and tax credits (billions allocated 2023–2025)

- U.S. facility ownership positions Lannett to qualify for incentives

- Incentives can shorten capex payback and strengthen supply-chain resilience

Medicare IRA, ASP deflation and API risks squeeze drug margins amid +4.2% spending

Political drivers compress prices via Medicare negotiation (IRA) saving Medicare $100B through 2031, ASP deflation 5–10% in 2024, and faster ANDA reviews (median 30 months in 2024) while API trade risks (60–70% supply from China/India) and potential 5–12% tariff-driven cost increases threaten margins; US drug spending +4.2% (2024), Medicaid 82M enrollees.

| Metric | Value (2024/25) |

|---|---|

| Medicare IRA savings | $100B thru 2031 |

| Generic ASP deflation | 5–10% |

| ANDA median time | 30 months |

| API reliance | 60–70% |

| US drug spending growth | +4.2% |

| Medicaid enrollees | 82M |

What is included in the product

Explores how macro-environmental factors specifically influence Lannett across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives and investors.

A concise, shareable PESTLE summary of The Lannett Company that highlights regulatory, market, and patent risks alongside economic and technological drivers, ideal for dropping into presentations or strategy sessions.

Economic factors

Generic Market Competition and Pricing Pressure

The generic pharmaceutical sector sees fierce price competition; average U.S. generic drug prices fell about 9% year-over-year in 2024 amid rising supplier count, squeezing margins—industry gross margins for commodity generics often dip below 20%. As entrants proliferate, Lannett faces downward price pressure on standard molecules and should prioritize complex generics and niche, high-barrier products where ASPs and margins remain materially higher.

Interest Rate Volatility and Debt Servicing

Fluctuations in interest rates directly raise Lannett’s cost of capital and affect its ability to service $250–300 million of reported debt; a 100-basis-point rise in 2025 would increase annual interest expense materially. High rates through late 2025 constrain cash flow for R&D and potential acquisitions, reducing discretionary spending. Lannett’s capital structure — with leverage ratios above industry median in 2024—requires active refinancing and rate-hedging to manage macroeconomic risk.

Inflationary Impacts on Manufacturing Costs

Rising energy, labor and raw material costs have compressed pharma margins; US headline CPI averaging 3.4% in 2024 and global oil prices near $80/bbl raised production expenses for manufacturers like Lannett, which reported gross margin pressure in 2024 financials. While Lannett pursues supply-chain optimization, persistent inflation requires scaling cost-saving programs and efficiency gains to protect operating income.

Currency Exchange Rate Fluctuations

Currency exchange rate volatility affects Lannett’s cost of goods sold and reported earnings, as a stronger US dollar versus key supplier currencies reduced import costs in FY2024 when the dollar rose ~6% vs. the euro, while a weaker dollar would increase COGS and compress margins.

Lannett reports using hedging instruments to mitigate FX exposure; as of 2024 the company disclosed active short-term forward contracts covering a portion of anticipated foreign purchases to stabilize purchasing power and cash flow.

- FY2024: US dollar up ~6% vs. EUR, lowering import costs

- FX swings directly affect COGS and gross margin volatility

- Company uses short-term forwards to hedge supplier payment exposure

Consumer Purchasing Power and Healthcare Spending

Broad economic trends affect disposable income and out-of-pocket healthcare spending; US personal consumption expenditures grew 3.6% in 2024, but real wage stagnation keeps price-sensitive patients shifting to generics.

During downturns, generic uptake rises—generic market share was ~90% of dispensed prescriptions in 2024—benefiting Lannett's volume and margin mix.

However, recessions can cut overall utilization; CMS data shows physician visits fell ~5% during 2023-24 regional slowdowns, risking total sales.

- Higher generic share (~90% of scripts in 2024) boosts Lannett volume

- Real wage pressure limits patients' ability to pay out-of-pocket

- Healthcare utilization dips (~5% regionally) can reduce total sales

Lannett margin pressure as generics plunge 9% and $250–300M debt raises rate risk

Intense price deflation in generics (US generic prices down ~9% YoY in 2024) squeezes margins, pushing Lannett toward complex/niche products; debt of $250–300m raises sensitivity to 2025 rate moves; US CPI ~3.4% and $80/bbl oil lifted COGS in 2024; USD ↑ ~6% vs EUR in 2024 provided temporary import relief; generics = ~90% of scripts, boosting volume but price-sensitive demand.

| Metric | 2024/2025 |

|---|---|

| Generic price change | -9% YoY (2024) |

| Debt | $250–300m |

| CPI (US) | 3.4% (2024) |

| Oil | $~80/bbl (2024) |

| USD vs EUR | +~6% (2024) |

| Generic share scripts | ~90% (2024) |

Full Version Awaits

Lannett Company PESTLE Analysis

The preview shown here is the exact Lannett Company PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how regulatory shifts, pricing pressure, and supply-chain dynamics are shaping Lannett Company's outlook in our concise PESTLE snapshot—perfect for investors and strategists seeking fast, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, growth opportunities, and strategic recommendations you can apply immediately.

Political factors

Drug Pricing Legislation and Reform

Government initiatives to lower prescription drug costs, including provisions from the 2022 Inflation Reduction Act, pressure generics makers by enabling Medicare negotiation—projected to save Medicare $100 billion through 2031—forcing price compression across the market.

Policies capping Medicare Part D OOP and allowing inflation rebates have driven downward pricing trends; generic ASP deflation of 5–10% in some therapeutic classes in 2024 affected margins industrywide.

Lannett must adjust pricing, contract strategies, and production to protect its 2024 revenue base—$220 million reported revenue in FY2024—while managing reimbursement risk and negotiating formularies to sustain profitability.

FDA Regulatory Oversight and Approval Processes

The political climate shapes FDA funding and priorities—federal appropriations rose to $5.6 billion in FY2025, influencing review capacity and timelines for Abbreviated New Drug Applications (ANDAs).

Leadership or policy shifts can accelerate or tighten approval cycles: median ANDA approval time moved from 36 months in 2022 to 30 months in 2024 under targeted review initiatives.

Lannett depends on efficient regulatory pathways to launch generics early; a 6-month faster approval can capture market share and materially affect revenues given thin generic margins.

International Trade and Supply Chain Policies

Political tensions and shifting trade agreements directly impact Lannett’s sourcing of APIs from China and India, which supply an estimated 60-70% of generic pharmaceutical APIs globally; disruptions could raise input costs and compress margins on its $287M 2024 revenue base.

New tariffs or export controls—such as recent US-China tech tariffs and sporadic Indian export curbs—could add 5-12% to API costs or delay shipments, risking production slowdowns across Lannett’s U.S. manufacturing sites.

Lannett must continuously monitor geopolitical stability and trade policy changes to safeguard a steady raw-material flow, hedge price volatility, and avoid inventory-driven disruptions that could impact quarterly output and revenue recognition.

Healthcare Infrastructure Funding

Government spending on public health programs drives demand for affordable generics; US federal and state drug spending rose 4.2% in 2024, boosting volume-sensitive players like Lannett.

Policy changes to Medicaid enrollment—which covered 82 million people in 2024—directly affect prescription volumes; expansions increase generic dispensing.

State policies favoring generic substitution as a cost-containment tool support Lannett’s market share and pricing stability.

- 2024 US drug spending +4.2%

- Medicaid enrollees 82M (2024)

- Generic substitution policies => higher volume for Lannett

National Security and Domestic Manufacturing Incentives

Rising U.S. policy focus on reshoring pharma manufacturing—driven by 2023–2025 supply chain disruptions—offers Lannett access to incentives; the CHIPS and Science Act-like momentum and state grant programs have directed billions in manufacturing support, with federal manufacturing tax credits discussed in 2024 potentially lowering capex payback for domestic plants.

With Lannett operating U.S. facilities, it can capture grants/tax breaks to boost capacity, improving resilience and market share; leveraging incentives could reduce effective manufacturing costs and enhance margins amid rising generic demand.

- Federal/state grants and tax credits (billions allocated 2023–2025)

- U.S. facility ownership positions Lannett to qualify for incentives

- Incentives can shorten capex payback and strengthen supply-chain resilience

Medicare IRA, ASP deflation and API risks squeeze drug margins amid +4.2% spending

Political drivers compress prices via Medicare negotiation (IRA) saving Medicare $100B through 2031, ASP deflation 5–10% in 2024, and faster ANDA reviews (median 30 months in 2024) while API trade risks (60–70% supply from China/India) and potential 5–12% tariff-driven cost increases threaten margins; US drug spending +4.2% (2024), Medicaid 82M enrollees.

| Metric | Value (2024/25) |

|---|---|

| Medicare IRA savings | $100B thru 2031 |

| Generic ASP deflation | 5–10% |

| ANDA median time | 30 months |

| API reliance | 60–70% |

| US drug spending growth | +4.2% |

| Medicaid enrollees | 82M |

What is included in the product

Explores how macro-environmental factors specifically influence Lannett across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives and investors.

A concise, shareable PESTLE summary of The Lannett Company that highlights regulatory, market, and patent risks alongside economic and technological drivers, ideal for dropping into presentations or strategy sessions.

Economic factors

Generic Market Competition and Pricing Pressure

The generic pharmaceutical sector sees fierce price competition; average U.S. generic drug prices fell about 9% year-over-year in 2024 amid rising supplier count, squeezing margins—industry gross margins for commodity generics often dip below 20%. As entrants proliferate, Lannett faces downward price pressure on standard molecules and should prioritize complex generics and niche, high-barrier products where ASPs and margins remain materially higher.

Interest Rate Volatility and Debt Servicing

Fluctuations in interest rates directly raise Lannett’s cost of capital and affect its ability to service $250–300 million of reported debt; a 100-basis-point rise in 2025 would increase annual interest expense materially. High rates through late 2025 constrain cash flow for R&D and potential acquisitions, reducing discretionary spending. Lannett’s capital structure — with leverage ratios above industry median in 2024—requires active refinancing and rate-hedging to manage macroeconomic risk.

Inflationary Impacts on Manufacturing Costs

Rising energy, labor and raw material costs have compressed pharma margins; US headline CPI averaging 3.4% in 2024 and global oil prices near $80/bbl raised production expenses for manufacturers like Lannett, which reported gross margin pressure in 2024 financials. While Lannett pursues supply-chain optimization, persistent inflation requires scaling cost-saving programs and efficiency gains to protect operating income.

Currency Exchange Rate Fluctuations

Currency exchange rate volatility affects Lannett’s cost of goods sold and reported earnings, as a stronger US dollar versus key supplier currencies reduced import costs in FY2024 when the dollar rose ~6% vs. the euro, while a weaker dollar would increase COGS and compress margins.

Lannett reports using hedging instruments to mitigate FX exposure; as of 2024 the company disclosed active short-term forward contracts covering a portion of anticipated foreign purchases to stabilize purchasing power and cash flow.

- FY2024: US dollar up ~6% vs. EUR, lowering import costs

- FX swings directly affect COGS and gross margin volatility

- Company uses short-term forwards to hedge supplier payment exposure

Consumer Purchasing Power and Healthcare Spending

Broad economic trends affect disposable income and out-of-pocket healthcare spending; US personal consumption expenditures grew 3.6% in 2024, but real wage stagnation keeps price-sensitive patients shifting to generics.

During downturns, generic uptake rises—generic market share was ~90% of dispensed prescriptions in 2024—benefiting Lannett's volume and margin mix.

However, recessions can cut overall utilization; CMS data shows physician visits fell ~5% during 2023-24 regional slowdowns, risking total sales.

- Higher generic share (~90% of scripts in 2024) boosts Lannett volume

- Real wage pressure limits patients' ability to pay out-of-pocket

- Healthcare utilization dips (~5% regionally) can reduce total sales

Lannett margin pressure as generics plunge 9% and $250–300M debt raises rate risk

Intense price deflation in generics (US generic prices down ~9% YoY in 2024) squeezes margins, pushing Lannett toward complex/niche products; debt of $250–300m raises sensitivity to 2025 rate moves; US CPI ~3.4% and $80/bbl oil lifted COGS in 2024; USD ↑ ~6% vs EUR in 2024 provided temporary import relief; generics = ~90% of scripts, boosting volume but price-sensitive demand.

| Metric | 2024/2025 |

|---|---|

| Generic price change | -9% YoY (2024) |

| Debt | $250–300m |

| CPI (US) | 3.4% (2024) |

| Oil | $~80/bbl (2024) |

| USD vs EUR | +~6% (2024) |

| Generic share scripts | ~90% (2024) |

Full Version Awaits

Lannett Company PESTLE Analysis

The preview shown here is the exact Lannett Company PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.