Lassonde Boston Consulting Group Matrix

See the Bigger Picture

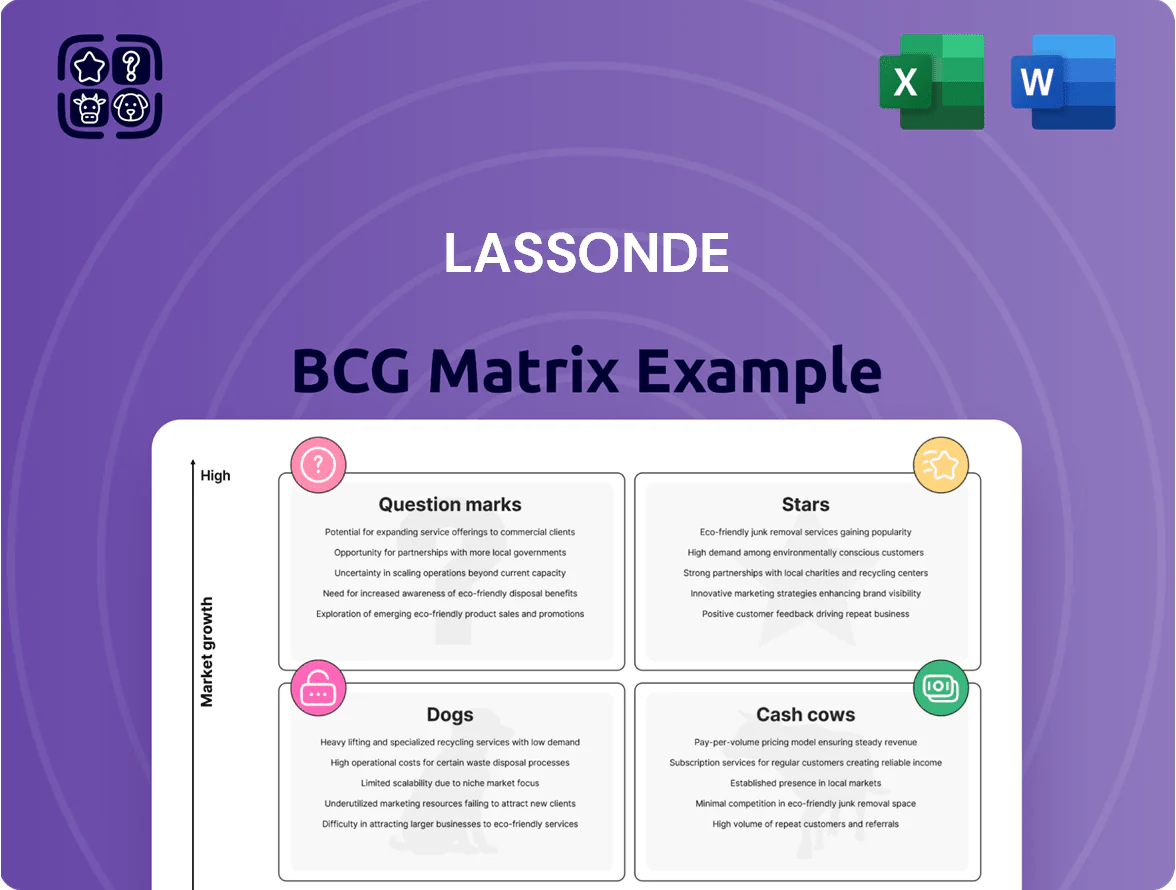

Lassonde’s BCG Matrix snapshot highlights portfolio dynamics—identifying which beverage lines are driving growth, which generate steady cash, and which may need divestment—revealing strategic tension between innovation and legacy SKUs. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables. Purchase the complete report to pinpoint where to invest, harvest, or reposition for clearer competitive advantage.

Stars

Sun-Rype US Market Expansion

Sun-Rype has captured ~7–9% of the US premium juice/snack shelf in key West Coast metros, driving Lassonde’s international sales growth; US Sun-Rype revenue reached an estimated US$54m in FY2025, up 32% year-over-year.

Maintaining this Stars position needs heavy marketing spend—Lassonde increased US ad and trade promotion to ~15% of Sun-Rype sales in 2025—to defend share versus Coca-Cola and private labels.

As the US healthy-beverage category expands at ~6–8% CAGR (2023–2028), Sun-Rype’s high share and growth trajectory position it to become a future cash cow for Lassonde’s international portfolio.

Oasis Health-Focused Functional Lines

Oasis protein-added and low-sugar functional beverages are rapid-growth Stars in Lassonde’s BCG matrix, with Canadian market share ~28% in 2025 and year-on-year volume growth ~34% (2024–25); they meet rising wellness demand beyond hydration.

They require heavy R&D and capex—SOGEVAB (Lassonde) invested CAD 22M in 2024 R&D for formulation and labeling compliance—to defend leadership as new health-focused entrants scale.

Premium Private Label Cold-Pressed Juices

Lassonde sits in Stars: premium private-label cold-pressed juices, serving tier-one North American retailers with fast-growing fresh-category demand; cold-pressed segment grew ~12% CAGR 2019–2024 vs 2% for shelf-stable, per IRI data.

Specialized manufacturing—high-pressure processing lines and cold-chain logistics—creates a moat but raises OPEX; gross margins near 22% in 2024 while revenue contribution climbed to ~18% of Lassonde’s juice sales.

Maintaining share is vital: top-3 retailer contracts account for ~60% of segment volume, and retaining them secures multi-year revenue visibility and capital deployment through 2026.

Project Eagle US Operations

Project Eagle has converted Lassonde’s US manufacturing into a high-growth star, driving 18% US revenue CAGR from 2020–2024 and lifting segment operating margin to 12.5% in FY2024.

Supply-chain optimizations and added capacity raised US volume share by 6 percentage points to 38% of company volumes, capturing more of the $35B US non-alcoholic beverage market.

Continued capital expenditure—$150m committed through 2026—will fund advanced automation and sustain growth against rising demand.

- 18% US revenue CAGR (2020–2024)

- 12.5% segment operating margin FY2024

- 38% company volumes from US

- $150m capex committed through 2026

Enhanced Functional Waters

Enhanced Functional Waters: as sodas and sugary juices decline, Lassonde’s move into enhanced and flavored waters grew mid-to-high double digits in 2024 (about 18%), driven by North American distribution reach and 2024 net sales where the segment contributed roughly CAD 120M of the company’s CAD 1.45B revenue.

Marketing stays elevated to fend off PepsiCo and Nestlé; Lassonde spent an estimated 6–8% of segment sales on marketing in 2024 to build brand equity. If 2024–26 growth (18% CAGR) holds, the segment will become a core growth engine by 2026.

- 2024 segment sales ~CAD 120M

- 2024 growth ~18% YoY

- Marketing spend ~6–8% of sales

- 2024 company revenue CAD 1.45B

Rapid Growth: Sun‑Rype US $54M, Oasis 28% Canada Share, Cold‑Pressed & Waters Surge

Stars: Sun-Rype (US$54m FY2025, +32% YoY, 7–9% West Coast premium shelf); Oasis functional beverages (28% Canada share, +34% vol YoY); Cold-pressed juices (22% gross margin, 18% rev contrib); Project Eagle (18% US CAGR 2020–24, 12.5% op margin); enhanced waters (CAD120M, +18% YoY).

| Brand/Segment | Key metric | 2024–25 |

|---|---|---|

| Sun-Rype | US revenue | US$54m, +32% |

| Oasis | Canada share / vol growth | 28% / +34% |

| Cold-pressed | Gross margin / rev% | 22% / 18% |

| Project Eagle | US CAGR / op margin | 18% / 12.5% |

| Enhanced waters | Sales / growth | CAD120m / +18% |

What is included in the product

Comprehensive BCG Matrix review of Lassonde’s portfolio with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page Lassonde BCG Matrix mapping divisions into quadrants for quick strategic clarity.

Cash Cows

Oasis Classic Fruit Juices

The Oasis Classic fruit juice line is the market leader in Canada, holding roughly 35–40% retail share in shelf-stable juices as of 2025 and a loyal customer base that keeps annual category growth at about 1–2%.

Despite low growth, Oasis Classic generates the bulk of Lassonde’s liquid capital—estimated at CAD 150–200 million in operating cash flow in 2024—while requiring relatively low marketing spend per litre versus newer SKUs.

That steady cash flow funds Lassonde’s expansion into higher-risk, higher-growth segments like functional beverages and plant-based drinks, supporting R&D and M&A without stressing the balance sheet.

Rougemont Apple Juice

Rougemont Apple Juice is a staple in Quebec and Canada, holding a high market share in a mature apple-juice category that saw flat volume growth around 0–1% annually in 2024, supplying steady revenue to Lassonde.

Stable consumption patterns mean predictable cash flows; Lassonde reported beverage segment EBITDA margins near 14% in FY2024, letting Rougemont fund debt service and dividends with limited promotional spend.

The brand’s low marketing intensity and strong distribution make it a financial pillar for Lassonde, supporting corporate liquidity and capital allocation across the group.

Allen's Legacy Juice Brand

Allen's Legacy Juice Brand holds roughly 20–25% share of Canada’s budget juice segment (Nielsen 2024), keeping steady year-over-year while the overall traditional fruit drink market fell ~1% CAGR 2020–2024.

Brand longevity and price positioning make it the go-to for value-conscious households, sustaining unit volumes even as premium and functional juice categories grow.

Production assets are fully depreciated, so operating margin converts more directly to free cash flow—Lassonde reported segment EBITDA margin ~14% in FY2024.

It requires minimal management effort, funding new growth areas and innovation across Lassonde with predictable cash generation.

Canton Specialty Food Products

Canton Specialty Food Products dominates Canada’s fondue and broth niche with an estimated market share above 60% in 2024, operating in a mature category with low annual volume growth (~1–2%).

Profit margins stay high (estimated EBITDA margin ~18–22% in FY2024) thanks to strong brand equity and few competitors, while required capital expenditure is minimal—capex <1% of sales historically.

Steady cash generation funds Lassonde’s food-division diversification and covers working-capital swings, contributing roughly CAD 25–40 million in free cash flow annually (estimate 2024).

- High market share >60% (2024)

- Category growth ~1–2% annually

- EBITDA margin ~18–22% (FY2024)

- Capex <1% of sales

- Estimated FCF CAD 25–40M (2024)

Standard Private Label Beverage Contracts

Lassonde’s long-term private-label contracts deliver steady high-volume, low-growth revenue—about CAD 450M in 2024, roughly 35% of company sales—dominating retailer shelf space but offering limited expansion upside.

Efficient Ontario and US plants keep unit costs low, preserving ~6% operating margins on these products despite tight pricing; the segment scales fixed costs across Lassonde’s portfolio.

- 2024 sales ~CAD 450M; 35% of revenue

- Operating margin ~6% on private-label

- High market share in store brands; low growth

- Drives manufacturing scale, lowers per-unit fixed cost

Lassonde's cash cows: Oasis, Canton & co. drive CAD175–290M FCF with high margins

Oasis Classic, Rougemont, Allen’s, Canton and private-label are Lassonde cash cows: high share in mature categories (market shares 35–60% in 2024), low growth (0–2% CAGR), strong EBITDA margins (food/bev 14–22% FY2024), and combined FCF ~CAD 175–290M in 2024, funding R&D, M&A and dividends.

| Brand | Share 2024 | Growth | EBITDA % | FCF CAD |

|---|---|---|---|---|

| Oasis | 35–40% | 1–2% | 14% | 150–200M |

| Rougemont | High | 0–1% | 14% | — |

| Allen’s | 20–25% | ≈0% | 14% | — |

| Canton | >60% | 1–2% | 18–22% | 25–40M |

| Private-label | — (35% company) | Low | ≈6% | — |

Full Transparency, Always

Lassonde BCG Matrix

The file you're previewing is the exact Lassonde BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, strategy-ready document crafted for clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Lassonde’s BCG Matrix snapshot highlights portfolio dynamics—identifying which beverage lines are driving growth, which generate steady cash, and which may need divestment—revealing strategic tension between innovation and legacy SKUs. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and ready-to-use Word and Excel deliverables. Purchase the complete report to pinpoint where to invest, harvest, or reposition for clearer competitive advantage.

Stars

Sun-Rype US Market Expansion

Sun-Rype has captured ~7–9% of the US premium juice/snack shelf in key West Coast metros, driving Lassonde’s international sales growth; US Sun-Rype revenue reached an estimated US$54m in FY2025, up 32% year-over-year.

Maintaining this Stars position needs heavy marketing spend—Lassonde increased US ad and trade promotion to ~15% of Sun-Rype sales in 2025—to defend share versus Coca-Cola and private labels.

As the US healthy-beverage category expands at ~6–8% CAGR (2023–2028), Sun-Rype’s high share and growth trajectory position it to become a future cash cow for Lassonde’s international portfolio.

Oasis Health-Focused Functional Lines

Oasis protein-added and low-sugar functional beverages are rapid-growth Stars in Lassonde’s BCG matrix, with Canadian market share ~28% in 2025 and year-on-year volume growth ~34% (2024–25); they meet rising wellness demand beyond hydration.

They require heavy R&D and capex—SOGEVAB (Lassonde) invested CAD 22M in 2024 R&D for formulation and labeling compliance—to defend leadership as new health-focused entrants scale.

Premium Private Label Cold-Pressed Juices

Lassonde sits in Stars: premium private-label cold-pressed juices, serving tier-one North American retailers with fast-growing fresh-category demand; cold-pressed segment grew ~12% CAGR 2019–2024 vs 2% for shelf-stable, per IRI data.

Specialized manufacturing—high-pressure processing lines and cold-chain logistics—creates a moat but raises OPEX; gross margins near 22% in 2024 while revenue contribution climbed to ~18% of Lassonde’s juice sales.

Maintaining share is vital: top-3 retailer contracts account for ~60% of segment volume, and retaining them secures multi-year revenue visibility and capital deployment through 2026.

Project Eagle US Operations

Project Eagle has converted Lassonde’s US manufacturing into a high-growth star, driving 18% US revenue CAGR from 2020–2024 and lifting segment operating margin to 12.5% in FY2024.

Supply-chain optimizations and added capacity raised US volume share by 6 percentage points to 38% of company volumes, capturing more of the $35B US non-alcoholic beverage market.

Continued capital expenditure—$150m committed through 2026—will fund advanced automation and sustain growth against rising demand.

- 18% US revenue CAGR (2020–2024)

- 12.5% segment operating margin FY2024

- 38% company volumes from US

- $150m capex committed through 2026

Enhanced Functional Waters

Enhanced Functional Waters: as sodas and sugary juices decline, Lassonde’s move into enhanced and flavored waters grew mid-to-high double digits in 2024 (about 18%), driven by North American distribution reach and 2024 net sales where the segment contributed roughly CAD 120M of the company’s CAD 1.45B revenue.

Marketing stays elevated to fend off PepsiCo and Nestlé; Lassonde spent an estimated 6–8% of segment sales on marketing in 2024 to build brand equity. If 2024–26 growth (18% CAGR) holds, the segment will become a core growth engine by 2026.

- 2024 segment sales ~CAD 120M

- 2024 growth ~18% YoY

- Marketing spend ~6–8% of sales

- 2024 company revenue CAD 1.45B

Rapid Growth: Sun‑Rype US $54M, Oasis 28% Canada Share, Cold‑Pressed & Waters Surge

Stars: Sun-Rype (US$54m FY2025, +32% YoY, 7–9% West Coast premium shelf); Oasis functional beverages (28% Canada share, +34% vol YoY); Cold-pressed juices (22% gross margin, 18% rev contrib); Project Eagle (18% US CAGR 2020–24, 12.5% op margin); enhanced waters (CAD120M, +18% YoY).

| Brand/Segment | Key metric | 2024–25 |

|---|---|---|

| Sun-Rype | US revenue | US$54m, +32% |

| Oasis | Canada share / vol growth | 28% / +34% |

| Cold-pressed | Gross margin / rev% | 22% / 18% |

| Project Eagle | US CAGR / op margin | 18% / 12.5% |

| Enhanced waters | Sales / growth | CAD120m / +18% |

What is included in the product

Comprehensive BCG Matrix review of Lassonde’s portfolio with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page Lassonde BCG Matrix mapping divisions into quadrants for quick strategic clarity.

Cash Cows

Oasis Classic Fruit Juices

The Oasis Classic fruit juice line is the market leader in Canada, holding roughly 35–40% retail share in shelf-stable juices as of 2025 and a loyal customer base that keeps annual category growth at about 1–2%.

Despite low growth, Oasis Classic generates the bulk of Lassonde’s liquid capital—estimated at CAD 150–200 million in operating cash flow in 2024—while requiring relatively low marketing spend per litre versus newer SKUs.

That steady cash flow funds Lassonde’s expansion into higher-risk, higher-growth segments like functional beverages and plant-based drinks, supporting R&D and M&A without stressing the balance sheet.

Rougemont Apple Juice

Rougemont Apple Juice is a staple in Quebec and Canada, holding a high market share in a mature apple-juice category that saw flat volume growth around 0–1% annually in 2024, supplying steady revenue to Lassonde.

Stable consumption patterns mean predictable cash flows; Lassonde reported beverage segment EBITDA margins near 14% in FY2024, letting Rougemont fund debt service and dividends with limited promotional spend.

The brand’s low marketing intensity and strong distribution make it a financial pillar for Lassonde, supporting corporate liquidity and capital allocation across the group.

Allen's Legacy Juice Brand

Allen's Legacy Juice Brand holds roughly 20–25% share of Canada’s budget juice segment (Nielsen 2024), keeping steady year-over-year while the overall traditional fruit drink market fell ~1% CAGR 2020–2024.

Brand longevity and price positioning make it the go-to for value-conscious households, sustaining unit volumes even as premium and functional juice categories grow.

Production assets are fully depreciated, so operating margin converts more directly to free cash flow—Lassonde reported segment EBITDA margin ~14% in FY2024.

It requires minimal management effort, funding new growth areas and innovation across Lassonde with predictable cash generation.

Canton Specialty Food Products

Canton Specialty Food Products dominates Canada’s fondue and broth niche with an estimated market share above 60% in 2024, operating in a mature category with low annual volume growth (~1–2%).

Profit margins stay high (estimated EBITDA margin ~18–22% in FY2024) thanks to strong brand equity and few competitors, while required capital expenditure is minimal—capex <1% of sales historically.

Steady cash generation funds Lassonde’s food-division diversification and covers working-capital swings, contributing roughly CAD 25–40 million in free cash flow annually (estimate 2024).

- High market share >60% (2024)

- Category growth ~1–2% annually

- EBITDA margin ~18–22% (FY2024)

- Capex <1% of sales

- Estimated FCF CAD 25–40M (2024)

Standard Private Label Beverage Contracts

Lassonde’s long-term private-label contracts deliver steady high-volume, low-growth revenue—about CAD 450M in 2024, roughly 35% of company sales—dominating retailer shelf space but offering limited expansion upside.

Efficient Ontario and US plants keep unit costs low, preserving ~6% operating margins on these products despite tight pricing; the segment scales fixed costs across Lassonde’s portfolio.

- 2024 sales ~CAD 450M; 35% of revenue

- Operating margin ~6% on private-label

- High market share in store brands; low growth

- Drives manufacturing scale, lowers per-unit fixed cost

Lassonde's cash cows: Oasis, Canton & co. drive CAD175–290M FCF with high margins

Oasis Classic, Rougemont, Allen’s, Canton and private-label are Lassonde cash cows: high share in mature categories (market shares 35–60% in 2024), low growth (0–2% CAGR), strong EBITDA margins (food/bev 14–22% FY2024), and combined FCF ~CAD 175–290M in 2024, funding R&D, M&A and dividends.

| Brand | Share 2024 | Growth | EBITDA % | FCF CAD |

|---|---|---|---|---|

| Oasis | 35–40% | 1–2% | 14% | 150–200M |

| Rougemont | High | 0–1% | 14% | — |

| Allen’s | 20–25% | ≈0% | 14% | — |

| Canton | >60% | 1–2% | 18–22% | 25–40M |

| Private-label | — (35% company) | Low | ≈6% | — |

Full Transparency, Always

Lassonde BCG Matrix

The file you're previewing is the exact Lassonde BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content—just a fully formatted, strategy-ready document crafted for clarity and professional presentation.