Lassonde SWOT Analysis

Make Insightful Decisions Backed by Expert Research

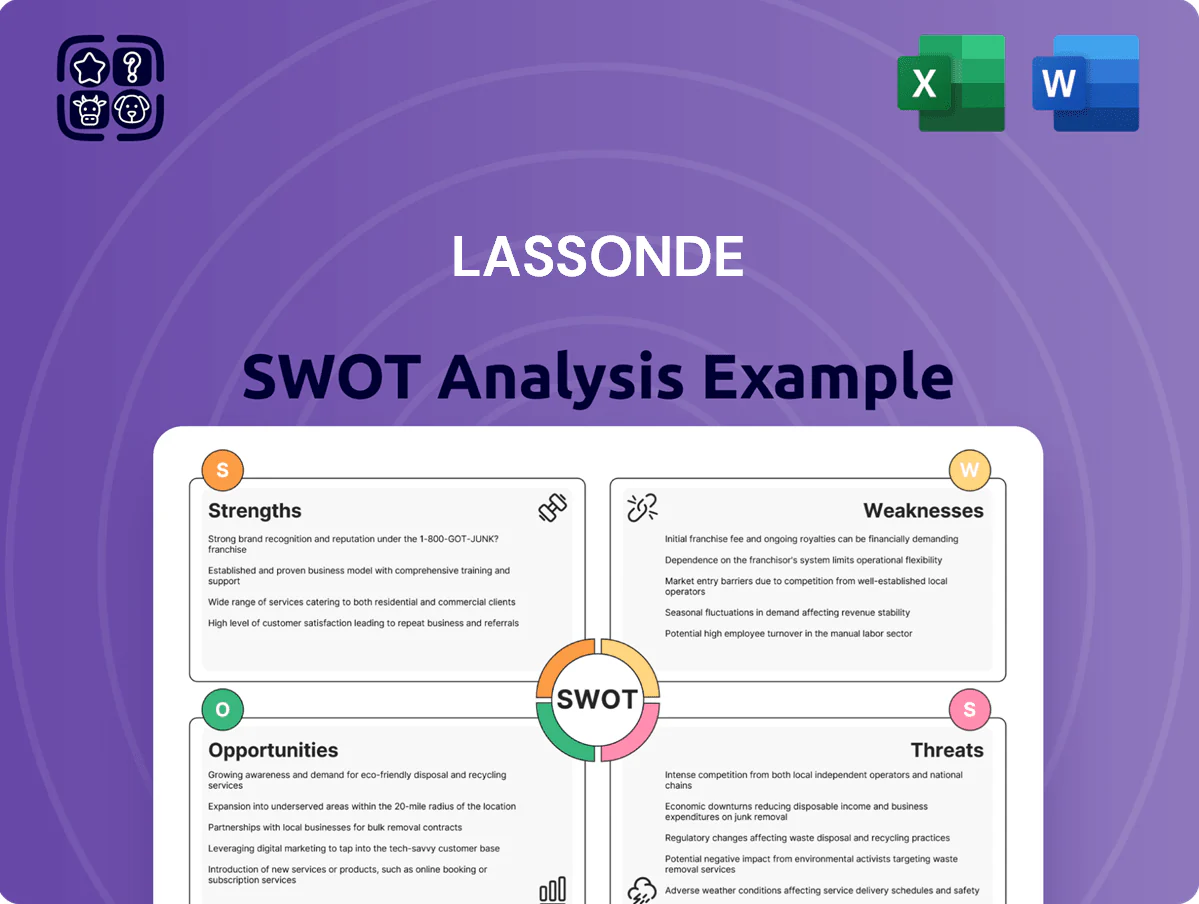

Lassonde’s SWOT snapshot highlights strong brand equity, diversified beverage lines, and growing retail partnerships, balanced against supply-chain pressure and intense category competition; opportunities include premiumization and export growth, while regulatory shifts pose risks. Purchase the full SWOT analysis to access a thorough, editable report and Excel deliverable—perfect for investors, strategists, and advisors seeking actionable, research-backed recommendations.

Strengths

Dominant Canadian Market Position

Lassonde holds roughly 40% share of the Canadian refrigerated juice market (2024 NielsenIQ), led by Oasis and Rougemont, giving strong shelf placement and repeat purchase rates—brand loyalty lifts SKU velocity by an estimated 12–18% versus private labels. This domestic strength generated CA$612M revenue in FY2024, funding US expansion where market share is below 5% and M&A and distribution investments accelerate growth.

Robust Private Label Expertise

Lassonde has become a top private-label partner for major North American retailers, supporting roughly 35% of its 2024 beverage volumes via private-label contracts and driving CAD 420 million in 2024 net sales from private-label and co-manufacturing.

Demand for value-oriented products rose as food inflation peaked at 6.2% in 2022–2023, and private-label penetration in beverages climbed to 22% in 2024, benefiting Lassonde’s stable order book.

The company’s end-to-end manufacturing and packaging capabilities—15 plants in North America and a 2024 capacity utilization near 88%—make Lassonde indispensable for large grocery chains managing SKU rationalization and cost pressure.

Diversified Product Portfolio

Beyond its core juice business, Lassonde expanded into soups, sauces and dressings, with non-beverage products contributing about 28% of 2024 revenue CAD 1.12B (company filings, FY2024), which cushions seasonal dips in juice demand.

Extensive Manufacturing and Distribution Network

- 14 plants across Canada/US

- FY2024 sales CAD 2.03B, 92% North America

- ~18% lower inbound transport

- ~22% faster replenishment vs peers

Strong Financial Health and Cash Flow

Lassonde Industries shows disciplined capital management: as of FY2024 (year ended Sept 30, 2024) net debt/EBITDA stood near 1.1x and operating cash flow was CAD 142M, supporting steady cash generation and a strong balance sheet.

This stability funded two small acquisitions in 2024 and CAD 28M in plant upgrades without large new debt, making investors comfortable with its resilience to short-term macro swings.

- Net debt/EBITDA ~1.1x (FY2024)

- Operating cash flow CAD 142M (FY2024)

- Capex on upgrades CAD 28M (2024)

- Completed 2 acquisitions (2024)

Lassonde: ~40% Canadian juice share, CAD2.03B sales, strong cash flow & low leverage

Lassonde commands ~40% of Canadian refrigerated juice (NielsenIQ 2024), drove CAD 2.03B sales in FY2024 with 92% North America exposure, and maintains 14 plants (88% capacity utilization) supporting ~18% lower inbound transport and ~22% faster replenishment versus peers; net debt/EBITDA ~1.1x and operating cash flow CAD 142M enabled CAD 28M capex and two 2024 acquisitions.

| Metric | Value |

|---|---|

| Canadian juice share | ~40% (2024) |

| FY2024 sales | CAD 2.03B |

| Plants | 14 (NA) |

| CapUtil | ~88% |

| Net debt/EBITDA | ~1.1x (FY2024) |

| Operating CF | CAD 142M (FY2024) |

What is included in the product

Provides a concise SWOT assessment of Lassonde, highlighting its core strengths, internal weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a focused Lassonde SWOT summary that accelerates strategic alignment and decision-making across teams.

Weaknesses

Geographic Concentration in North America

Lassonde’s net sales remain heavily North America‑centric: in FY2024 about 95% of revenue came from Canada and the U.S. (CAD 2.1B of CAD 2.2B total), exposing the company to regional GDP swings and consumer trends.

Unlike peers such as Coca‑Cola Co. (over 60% sales outside North America in 2024), Lassonde lacks emerging‑market exposure that could offset mature‑market stagnation and slower per‑capita juice consumption.

This concentration raises sensitivity to USMCA/Canada trade shifts and state/provincial regulatory changes—changes to US sugar or labeling rules could materially affect margins and compliance costs.

Sensitivity to Commodity Price Volatility

Heavy Reliance on Mature Product Categories

A large share of Lassonde Industries’ revenue—about 40% of FY2024 Canadian/US beverage sales—still comes from traditional fruit juices, a category down ~2–3% annual volume in North America since 2019, making growth harder.

As consumers shift from high‑sugar drinks, promotion and price investments rose 150–200 bps of gross margin in 2023 to defend share, raising unit costs.

Retail shelf space is contested by sparkling waters and functional drinks, which grew double digits in 2023, forcing higher trade spend and innovation expense to stay relevant.

Exposure to Currency Fluctuations

Operational Complexity of Multiple Segments

- Gross margin down to 20.8% (2024)

- Capex CAD 78.4m in FY2024 (+18% YoY)

- SG&A 12.6% of sales (2024)

- Risk: resource competition, diluted innovation focus

Lassonde risks: NA concentration, FX/commodity swings & margin squeeze

Lassonde is highly North America‑concentrated (95% FY2024 revenue), exposed to regional demand swings, USD/CAD FX (≈C$12–18m net-income swing 2023–24) and commodity volatility (juice concentrate +22% YoY 2024) that compressed gross margin to 20.8% (2024). Heavy legacy juice mix (~40% beverage sales) and rising promo/trade spend (150–200 bps) pressure growth and margins.

| Metric | Value (2024) |

|---|---|

| North America revenue | 95% |

| Gross margin | 20.8% |

| Capex | CAD 78.4m |

| FX swing | C$12–18m |

Preview the Actual Deliverable

Lassonde SWOT Analysis

This is the actual Lassonde SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Lassonde’s SWOT snapshot highlights strong brand equity, diversified beverage lines, and growing retail partnerships, balanced against supply-chain pressure and intense category competition; opportunities include premiumization and export growth, while regulatory shifts pose risks. Purchase the full SWOT analysis to access a thorough, editable report and Excel deliverable—perfect for investors, strategists, and advisors seeking actionable, research-backed recommendations.

Strengths

Dominant Canadian Market Position

Lassonde holds roughly 40% share of the Canadian refrigerated juice market (2024 NielsenIQ), led by Oasis and Rougemont, giving strong shelf placement and repeat purchase rates—brand loyalty lifts SKU velocity by an estimated 12–18% versus private labels. This domestic strength generated CA$612M revenue in FY2024, funding US expansion where market share is below 5% and M&A and distribution investments accelerate growth.

Robust Private Label Expertise

Lassonde has become a top private-label partner for major North American retailers, supporting roughly 35% of its 2024 beverage volumes via private-label contracts and driving CAD 420 million in 2024 net sales from private-label and co-manufacturing.

Demand for value-oriented products rose as food inflation peaked at 6.2% in 2022–2023, and private-label penetration in beverages climbed to 22% in 2024, benefiting Lassonde’s stable order book.

The company’s end-to-end manufacturing and packaging capabilities—15 plants in North America and a 2024 capacity utilization near 88%—make Lassonde indispensable for large grocery chains managing SKU rationalization and cost pressure.

Diversified Product Portfolio

Beyond its core juice business, Lassonde expanded into soups, sauces and dressings, with non-beverage products contributing about 28% of 2024 revenue CAD 1.12B (company filings, FY2024), which cushions seasonal dips in juice demand.

Extensive Manufacturing and Distribution Network

- 14 plants across Canada/US

- FY2024 sales CAD 2.03B, 92% North America

- ~18% lower inbound transport

- ~22% faster replenishment vs peers

Strong Financial Health and Cash Flow

Lassonde Industries shows disciplined capital management: as of FY2024 (year ended Sept 30, 2024) net debt/EBITDA stood near 1.1x and operating cash flow was CAD 142M, supporting steady cash generation and a strong balance sheet.

This stability funded two small acquisitions in 2024 and CAD 28M in plant upgrades without large new debt, making investors comfortable with its resilience to short-term macro swings.

- Net debt/EBITDA ~1.1x (FY2024)

- Operating cash flow CAD 142M (FY2024)

- Capex on upgrades CAD 28M (2024)

- Completed 2 acquisitions (2024)

Lassonde: ~40% Canadian juice share, CAD2.03B sales, strong cash flow & low leverage

Lassonde commands ~40% of Canadian refrigerated juice (NielsenIQ 2024), drove CAD 2.03B sales in FY2024 with 92% North America exposure, and maintains 14 plants (88% capacity utilization) supporting ~18% lower inbound transport and ~22% faster replenishment versus peers; net debt/EBITDA ~1.1x and operating cash flow CAD 142M enabled CAD 28M capex and two 2024 acquisitions.

| Metric | Value |

|---|---|

| Canadian juice share | ~40% (2024) |

| FY2024 sales | CAD 2.03B |

| Plants | 14 (NA) |

| CapUtil | ~88% |

| Net debt/EBITDA | ~1.1x (FY2024) |

| Operating CF | CAD 142M (FY2024) |

What is included in the product

Provides a concise SWOT assessment of Lassonde, highlighting its core strengths, internal weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a focused Lassonde SWOT summary that accelerates strategic alignment and decision-making across teams.

Weaknesses

Geographic Concentration in North America

Lassonde’s net sales remain heavily North America‑centric: in FY2024 about 95% of revenue came from Canada and the U.S. (CAD 2.1B of CAD 2.2B total), exposing the company to regional GDP swings and consumer trends.

Unlike peers such as Coca‑Cola Co. (over 60% sales outside North America in 2024), Lassonde lacks emerging‑market exposure that could offset mature‑market stagnation and slower per‑capita juice consumption.

This concentration raises sensitivity to USMCA/Canada trade shifts and state/provincial regulatory changes—changes to US sugar or labeling rules could materially affect margins and compliance costs.

Sensitivity to Commodity Price Volatility

Heavy Reliance on Mature Product Categories

A large share of Lassonde Industries’ revenue—about 40% of FY2024 Canadian/US beverage sales—still comes from traditional fruit juices, a category down ~2–3% annual volume in North America since 2019, making growth harder.

As consumers shift from high‑sugar drinks, promotion and price investments rose 150–200 bps of gross margin in 2023 to defend share, raising unit costs.

Retail shelf space is contested by sparkling waters and functional drinks, which grew double digits in 2023, forcing higher trade spend and innovation expense to stay relevant.

Exposure to Currency Fluctuations

Operational Complexity of Multiple Segments

- Gross margin down to 20.8% (2024)

- Capex CAD 78.4m in FY2024 (+18% YoY)

- SG&A 12.6% of sales (2024)

- Risk: resource competition, diluted innovation focus

Lassonde risks: NA concentration, FX/commodity swings & margin squeeze

Lassonde is highly North America‑concentrated (95% FY2024 revenue), exposed to regional demand swings, USD/CAD FX (≈C$12–18m net-income swing 2023–24) and commodity volatility (juice concentrate +22% YoY 2024) that compressed gross margin to 20.8% (2024). Heavy legacy juice mix (~40% beverage sales) and rising promo/trade spend (150–200 bps) pressure growth and margins.

| Metric | Value (2024) |

|---|---|

| North America revenue | 95% |

| Gross margin | 20.8% |

| Capex | CAD 78.4m |

| FX swing | C$12–18m |

Preview the Actual Deliverable

Lassonde SWOT Analysis

This is the actual Lassonde SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.